漲勢延續,國際油價能否「破百」?

危機再度來臨,油市風雨已起

雖然但是……好吧,之前我們對油價的預測還是稍微保守了一點,目前油市的走勢有一點快速上漲的趨勢,停滯的苗頭少得可憐。

剛剛過去的這個週末,布倫特和WTI油價相繼上升,目前全部站在90美元/桶之上,這也是過去近10個月的高位。如果把時間稍稍拉遠,從6月底7月初的70美元/桶到現在,國際油價在兩個來月的時間漲了接近三分之一。

資料來源:金十數據

如上圖所示,油價在今年經歷了一次深度的、幅度較大的波動,徹底告別上半年漲一陣跌一陣的走勢,從6月底開始一直保持漲勢。隨着油價繼續上漲,已經基本可以下一個判斷,也是我們之前就強調過的:

由“口罩”和俄烏衝突共同推動的這一輪國際原油週期峯值還沒過去,高價還將繼續。

不過,有一個預期可能需要調整一下。從最近幾個月的走勢可以明顯看出,產油國能夠接受的油價“底線”發生了變化——70美元/桶。過去這個算得上是中等偏高的價位,幾乎可以認爲是未來很長一段時間裏,產油國可以接受的油價底線,一旦下跌突破這個底線,他們就會採取強硬手段力挺價格。

同時,縈繞在國際油市上空的不僅是產油國的控制意願,目前庫存、成品油價格等等因素,都對油價起到了較強的支撐作用;相比之下,聯儲局和各個西方國家央行的加息預期,受到經濟衰退可能性的制約,很難再對油價起到什麼掣肘的作用。

接下來,我們會再度梳理一下目前國際油市的基本面,明確一些未來可能出現的新變化。

01 需求,還是需求。

對於傳統能源來說,一個很難避免的事實是,諸如煤炭、石油和天然氣這樣的化石燃料的需求,可能在未來永久性地下滑。當然,這種判斷在很長時間以來不絕於耳,但隨着這些能源的價格接連創下新高,人們很容易反駁這些關於他們會迎來衰退的說法。

可事實就是事實。隨着中國經濟走向高質量發展,這個過去二十年全球石油需求最大的引擎,正在向着更高效、更清潔的經濟結構轉型;光伏、風電,加上正在風行的電動汽車,正在全球範圍內一點點替代傳統的能源供需結構。這種演變的速度可能沒有那麼快,但它已經是既定的趨勢。

根據國際能源署(IEA)的預測,就算全球各國政府從今年開始,不再出臺任何清潔能源的政策、不再進行額外的能源消耗控制,化石能源需求的峯值也會在十年內出現。可以說,這個世界對能源的需求,越來越接近歷史性轉折的時刻,將使全球溫室氣體排放的峯值提前到來。

真正理解這一點,是解釋目前許多現狀的答案,有助於分析原油市場的諸多現象。爲何沙特和俄羅斯在今年供需本就偏緊的狀況下,還要力推減產;再比如,煤炭、天然氣和石油的勘探開發投資,即便在過去兩年價格飛漲的情況下,依然看不到什麼大幅擴張的跡象等等。

正是因爲市場已經形成了化石能源需求峯值正在加速到來的共識,許多事情就變得有跡可循。

當然,需求的下降不會是迅速的,更不會是線性的,而是緩慢的、波動的。例如,短時間內的能源短缺,可能會增加化石能源的需求量;再比如,一些國家快速的經濟發展勢頭,大幅度提升了能源需求量,導致全球總需求出現波動等等。

同時,正是由於這樣的需求預期建立,能源安全也變得更具挑戰性,不同國家的應對方式也不一樣。作爲全球化石能源需求第一大國,中國並沒有放慢化石能源開發的腳步,石油、天然氣和煤炭的產量都在逐年增長。特別是前兩類能源,在前幾年開始的增儲上產戰略下,所有的中國石油企業都在加大國內國際兩個資源的開發投入,力求在全球能源供應格局不確定性加大的未來,儘可能保障國內的能源供應。

也是因此,簡單地把需求預期變差和油價下降、投資減少之間畫等號是錯誤的。全球的每一個國家,特別是經濟大國,對於同樣預期的應對方式都會有差別,有些甚至是南轅北轍。作爲投資者,應該結合這個國家的資源稟賦、地理位置、國際影響力等等因素綜合判斷,才能作出最科學的決策。

02 供給,兩大國的“鋼鐵盟約”

正是基於無可辯駁、極其確定性的長期需求預期走弱,沙特和俄羅斯兩個大國開始協同救市。

先別誤會,我們絕對沒有把沙特和俄羅斯之間在油價控制上的協同,影射成納粹德國和意大利之間的狼狽爲奸,只不過覺得這個“鋼鐵一般的合作”用在現在的沙特和俄羅斯身上特別貼切而已。

當然,如果是西方媒體的語境之下,這倆國家目前的協同狀態還真有點那個意思。

先來看一個數據,這是過去十年的油價走勢圖。

資料來源:Bloomberg

從這張圖裏可以明顯地看到,2015年之前和2022年之後,是最近的兩輪油價高峰期。而夾雜在中間的,則是以沙特爲首的歐佩克,和俄羅斯的兩次合作破裂。2015年,爲了在崛起的美國頁岩油生產商手中搶回失去的份額,沙特大幅度增產發動價格戰;2020年,在“口罩”發生後不久,沙特再度發動原油價格戰,而這次的目標則直指俄羅斯。

時過境遷,沙俄鬧掰之後不久,兩國就發現事情不太對,明明彼此有着非常廣泛的利益基礎——油價,卻因爲一些小的問題給彼此整得都挺狼狽。2022年,俄烏衝突爆發,西方國家開始對俄羅斯進行能源制裁,伴隨着沙特脫離美國控制的自主性越來越強,兩個原油大國開始形成了協同。

這種能源生產戰略的協同,讓俄羅斯在面對西方制裁時依然有着不錯的原油收入,繼續供着這個國家和烏克蘭之間的拉扯;也讓沙特有了更多的資本,投資國內的其他產業,培育除了原油之外的經濟增長點。

特別是沙特,從建立與美國職業高爾夫巡迴賽相抗衡的賽事,到大肆砸錢請來內馬爾和C羅加盟他們的國內足球職業聯賽,沙特不惜投入在這些影響力強大的體育賽事上;與中國達成各類產業、投資上的合作,同時和伊朗冰釋前嫌,力圖在地緣政治上發揮更大的作用。

一切的動作都圍繞一個核心點:就算沒了美國,沙特依然能活得很好。當然,活得好,得建立在有錢的基礎之上。爲此,沙特和俄羅斯一起,把國際油價的底線推高至70美元以上,在過去,不到50美元/桶以下,很難說這個油價“低了”。

現在,壓力來到了美國這兒。去年,爲了應對俄烏衝突帶來的能源價格暴漲,美國把自己的原油庫存降到了40年前的水平;今年,隨着油價的持續上升,還能有多少的手段呢?

03 加息or not,兩難的選擇

自2022年以來,除了釋放庫存原油儲備之外,應對油價高漲還有一個辦法——加息。但是,加息並沒有有效遏制通脹的預期,更沒有對油價形成有效控制。

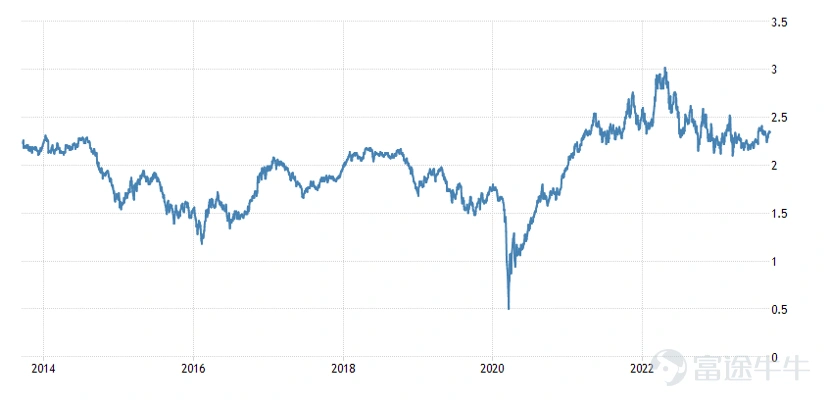

(過去十年10年期美國盈虧平衡通脹率)

資料來源:BEA

(過去十年布倫特油價變動)

可以看到這兩張圖裏的走勢,幾乎是完全正相關的。根據基數效應,我們可以知道,當下的油價上漲,意味着未來通脹預期的下降,但事實是相反的。即便是接連加息的狀況下,10年期美國盈虧平衡通脹率也有2.35%,這個水平可並不算低。

當地時間9月13日,美國8月消費者價格指數(CPI)環比增長0.6%,漲幅高於此前一個月的0.2%。同比上漲3.7%,漲幅較上月擴大0.5個百分點,爲14個月來最大環比漲幅。但仔細觀察這一數據不難發現,剔除波動較大的能源價格後,核心CPI環比上漲0.3%,同比上漲4.3%,能源價格飆漲成爲CPI漲幅擴大的主因。

在海的另一邊,加息的靴子已經落地。9月14日,歐洲中央銀行召開貨幣政策會議,決定將歐元區三大關鍵利率分別上調25個點子。這是歐洲央行自去年7月以來的第十次加息,加息後歐元區的利率水平已經達到1999年歐元問世以來的最高點。

但是,上週末繼續飆漲的油價,成爲了對加息最爲強硬的回應。在西方國家已經偏高的利率基礎上,進一步加息將會對經濟發展帶來巨大的風險,特別是歐洲,法德兩國對加息的支持,極有可能損害周邊國家正在擴張的財政狀況,進一步加大經濟衰退的可能。

更糟糕的是,加息控制不了沙特和俄羅斯挺價的意願,更沒辦法緩解如今成品油的供需失衡。

長期以來,煉油一直是石油市場中可預測性較高的領域之一,但現在卻因爲氣候政策陷入困境。特別是在美國、歐洲和新興經濟體,人們對於燃料的需求正在上升,但是煉油廠的新增產能正在下滑。

供不應求,成爲煉油和下游環節的主旋律,這也就意味着,成品油環節的供不應求還將持續很長一段時間。

因此,在現在這個情況下,加息已經很難對抑制能源價格上漲起到特別關鍵的作用了,即便能源價格高企,是否加息也將基於更加宏觀的經濟狀況通盤進行考慮。根據市場預期,聯儲局在9月份維持利率不變的概率接近99%,後續是否進一步加息,還要看經濟的預期。

最後,說回在目前油市的狀況下,應該關注的幾類標的。一類,就是像中石油和中海油這樣,在國內有着高質量大型油田的石油開發企業,當然,中石油是中國進口俄羅斯原油的主力,還能享受到後者現在一點點的油價折扣;另一類,是煉油企業,能夠面向海外出口或在海外有煉廠的,如中石化、恒逸石化等。$中國海洋石油 (00883.HK)$$中國石油股份 (00857.HK)$$中國石油化工股份 (00386.HK)$

聲明:本文僅用於學習和交流,不構成投資建議。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論(1)

發表評論

13

8