April Fund Monthly Report

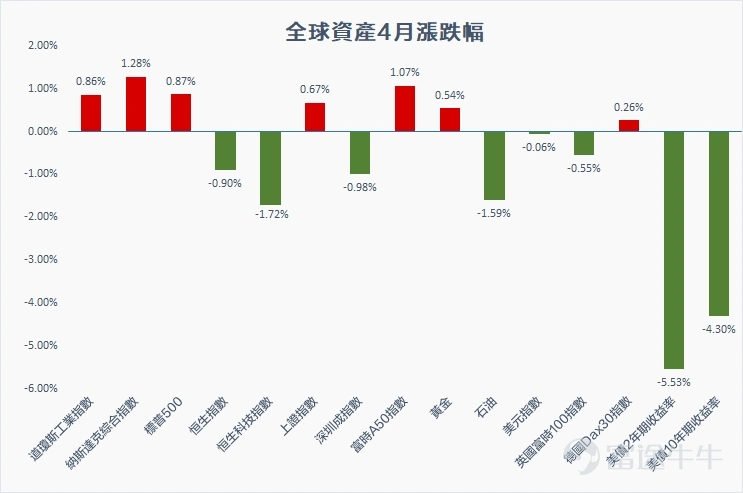

The performance of overseas assets and Greater China assets is divided

(Data source: Wind, cutoff date: 20230430, weekly rise and fall rate of global assets)

1. The performance of overseas assets and Greater China assets diverged in April.

2. The mixed US economic data released in April (such as the slowdown in US GDP growth in the first quarter, the recovery in manufacturing PMI, the easing of supply and demand pressure in the labor market, etc.) caused market performance to fluctuate. However, the financial reports of some large technology star stocks for the previous quarter were superior to market expectations, which led to a rise in the three major US stock indices. Among them, the Nasdaq index, which is dominated by the technology sector, performed better.

3. Although China's GDP growth rate for the first quarter announced within the month was better than market expectations, the performance of the Chinese and Hong Kong stock markets was poor due to reports indicating that US President Joe Biden will sign an executive order restricting US companies from investing in China. In addition, market transactions are relatively quiet.

4. Since the market anticipated that the Federal Reserve would continue to raise interest rates in May, the high level of interest rates raised market concerns about the slowdown in US economic growth and the slowdown in crude oil demand, which offset the impact of tight supply to a certain extent and suppressed the trend in crude oil prices.

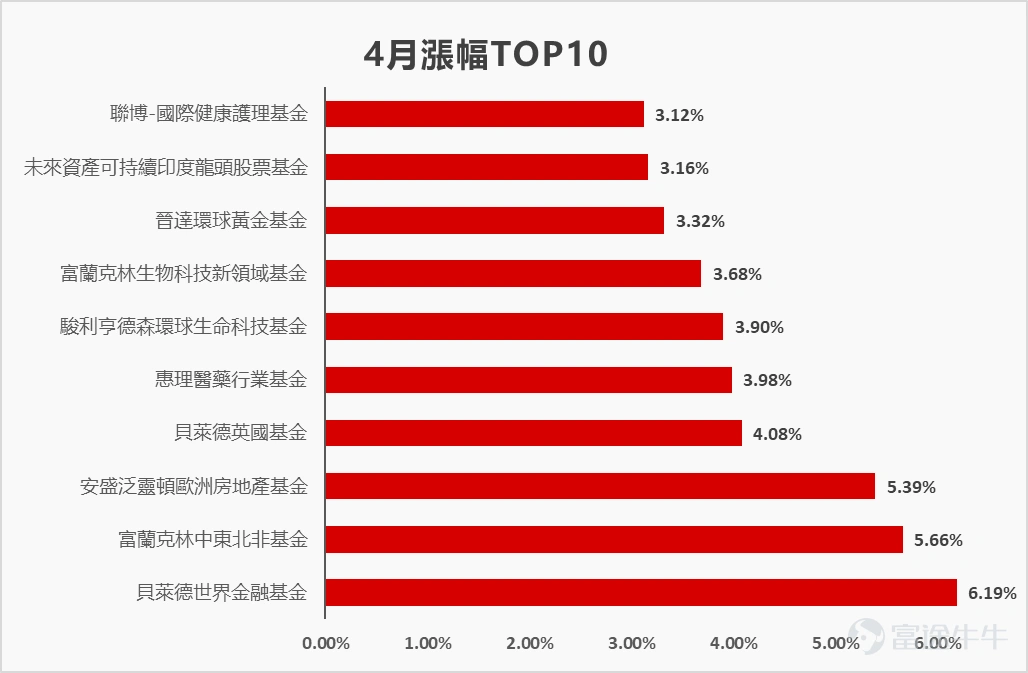

The financial sector rebounded sharply

(Data source: Morning Star (compiled by Futu), cutoff date: 20230430, the best performing fund on the platform last week); Earnings data is for reference only, and past performance does not indicate future performance.

Note 1: If the fund has shares in Hong Kong dollars and US dollars, priority will be given to the Hong Kong dollar share data. There may be differences in the data for different currency shares; when the fund has a dividend share, priority will be given to the cumulative share data. Since the fund's net worth will be released after T+1 or T+2 time, the date of fund net worth data extraction will be based on the fund's latest net worth of April 30, 2023 (that is, last Friday) published by the fund at 10:00 a.m. on May 4, Hong Kong time. Investors should seek professional advice if they have any questions.

Note 2: Futu Compiled Fund's monthly return is calculated by net fund value (net fund value at the end of the month - net fund value at the end of the previous month) /net fund value at the end of the previous month and displayed as a percentage)

1. Although the financial sector was previously suppressed by the European and American banking crisis, the first-quarter results of major banks announced during the month remained steady. Coupled with the ability of the European and American authorities to quickly address the symptoms of the crisis, spurring the financial sector to rebound from a low level. However, investors need to keep an eye on the current situation of small to medium banks.

2. Currently, loan momentum in the Eurozone continues to weaken, causing the market to reinforce expectations that the ECB will slow down interest rate hikes during the month. As a result, the real estate industry, which is more sensitive to interest rates, was boosted, and the performance of funds invested in related sectors picked up.

3. Boosted by the performance forecasts announced by leading biotechnology companies within the month, it is expected that demand for diagnostic testing and medical technology equipment will remain strong this year. Investments in related biotechnology sector funds have performed brilliantly as a result.

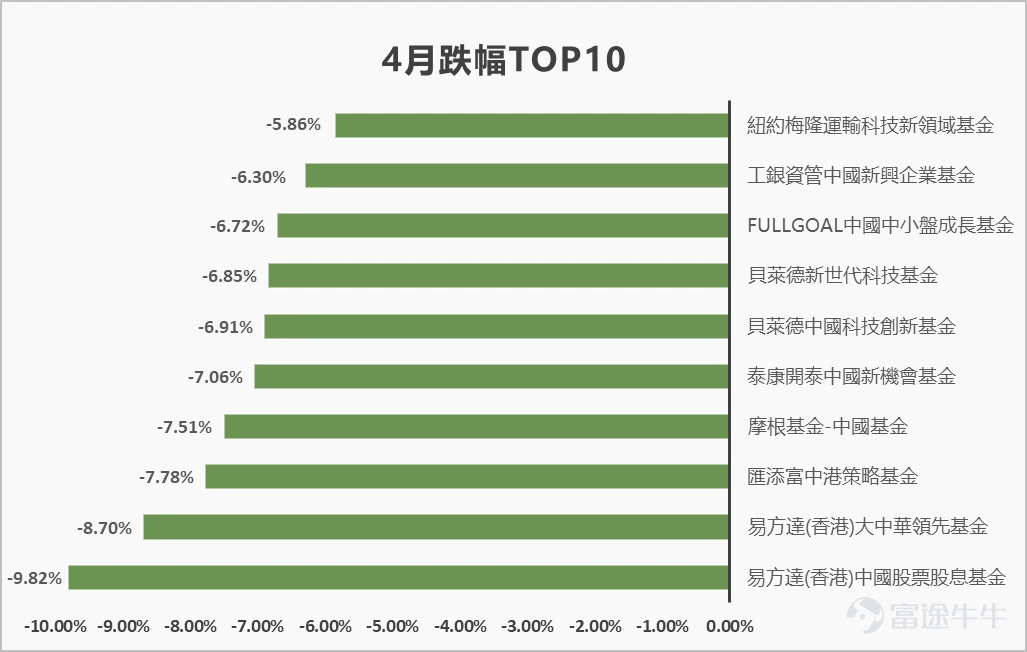

The decline in China-Hong Kong stock funds is obvious

(Data source: Morning Star (compiled by Futu), deadline: 20230430, the worst performing fund on the platform last week); Earnings data is for reference only, and past performance does not indicate future performance.

Note 1: If the fund has shares in Hong Kong dollars and US dollars, priority will be given to the Hong Kong dollar share data. There may be differences in the data for different currency shares; when the fund has a dividend share, priority will be given to the cumulative share data. Since the fund's net worth will be released after T+1 or T+2 time, the date of fund net worth data extraction will be based on the fund's latest net worth of April 30, 2023 (that is, last Friday) published by the fund at 10:00 a.m. on May 4, Hong Kong time. Investors should seek professional advice if they have any questions.

Note 2: The weekly return of Futu compiled funds is calculated on the net value of the fund (net value of the fund last Friday - the net value of the fund last Monday) /the net value of the fund from last Monday and displayed as a percentage)

1. Although China's economic growth rate in the first quarter exceeded market expectations, the market is concerned that the economic recovery will be difficult to continue. Coupled with the continuing tension in Sino-US relations, the performance of funds invested in the Chinese and Hong Kong stock markets during the month was poor. Among them, IT, essential consumption, and real estate construction performed less well.

2. Due to the slowdown in global economic growth and the relatively moderate recovery rate of China after the blockade was lifted, semiconductor demand was under pressure. The Philadelphia Semiconductor Index, which represents the semiconductor sector, fell about 6.8% during the month, causing funds that account for a relatively large share of this sector to record a strong decline.

Future market outlook for overseas assets

1. The May FOMC meeting decided to continue to raise interest rates by 25 bp, raising the benchmark interest rate to a level in the 5-5.25% range, in line with market expectations. The chairman of the Federal Reserve believes that the end of interest rate hikes is now approaching or has been reached, and future meeting decisions will be decided one by one based on economic data.

2. Recently, market trends are expected to be volatile due to continued bank risk fermentation, the imminent debt ceiling, and the April CPI data. In addition, the current US stock market has taken into account the probability of a soft landing in the US economy, but it has not taken into account the tightening of credit conditions, the decline in corporate profits, and the risk of relatively high valuations due to the banking crisis (the current 12-month forward price-earnings ratio of the S&P 500 index is 18.8 times, a 16% premium over the average of the past 10 years).

3. In the current situation where market interest rates are still in disagreement with the Federal Reserve, investors can maintain ultra-short-term investment-grade bond allocations, all because of their higher credit ratings, which often perform relatively steadily when the market falls, and can also bring stable returns in an environment with high interest rates. In terms of asset allocation, the diversified asset allocation form mixed with stocks and bonds can fulfill the goal of risk diversification to withstand market fluctuations.

Future asset market outlook for Greater China

1. The number of domestic travelers and domestic tourism revenue achieved during the May 1st holiday period have all exceeded the same period in 2019, reflecting residents' high enthusiasm for travel and extremely active consumer activity during the holiday season.

2. However, investors should pay attention to the unexpected fall of China's manufacturing PMI index to 49.2 in April, falling below the boom-and-bust line. Among them, production and new orders declined significantly, reflecting a slowdown in supply, while the demand side was relatively weak.

3. In addition, the market has recently been affected by geopolitical risks, and investors can continue to maintain high-rated bond allocations to spread subsequent risks.

4. Among them, assets in the high-rated bond category can be invested more soundly. Their corporate credit quality is higher, and their business and cash flow are more stable. Unless systemic risks occur, the default rate of investment grade bonds is generally relatively low, so performance is relatively resistant to decline. Currently, the yield on Asian investment grade bonds is 5.1%, which is higher than the average of the past ten years and is relatively attractive.

Hot topic 1

The Federal Reserve raised interest rates by 25 basis points and removed forward-looking guidance

1. This week, the Federal Reserve raised interest rates by 25 basis points as expected by the market, bringing the federal funds rate to 5% to 5.25%.

2. The current interest rate meeting statement removed the forward-looking guidance and no longer mentions anticipated further interest rate hikes. The chairman of the Federal Reserve believes that the end of interest rate hikes is now approaching or has been reached, and that future meeting decisions will be decided one by one based on economic data.

3. Judging from the ADP data released recently, the US employment situation is still quite resilient, and there is a high probability that future decisions of the Federal Reserve will be influenced by inflation data.

4. Although the Federal Reserve still says that inflation is currently too high and it is inappropriate to cut interest rates too soon, market interest rate pricing has brought forward the first interest rate cut to July.

5. After the interest rate meeting, market pricing will be unstable for a period of time. Investors should observe 1-2 more trading days before determining the pricing situation in the market.

Hot topic 2

China's manufacturing PMI unexpectedly declined

1. Last week, the manufacturing PMI announced by the National Bureau of Statistics unexpectedly declined and recorded 49.2, lower than the previous value of 51.9. Meanwhile, the Caixin manufacturing PMI announced this week also showed the same situation. It recorded 49.5, lower than the previous value of 50 and the expected 50.3. Falling below the 50 boom line meant that the manufacturing industry was shrinking.

2. Looking at each item, the PMI for production and new orders has declined to a large extent, which shows a situation where both supply and demand are weak.

3. The current data shows that the post-epidemic recovery on the production side is over, and weakness on the demand side is beginning to drag down the production side.

4. Therefore, this data will be a negative factor for Greater China risk assets. Investors may consider increasing high-rated bond assets in Greater China to calm portfolio risk.

5. In the current situation where the central bank of China continues to maintain an easy monetary policy, high-rated bonds will be a relatively beneficial asset.

Related funds

(1) Greater China Investment Grade Bond Fund (the screening principle is bond type, the investment theme is Greater China, and the top five performers in the past year)

Bosch Greater China Bond Fund

Hongshou High Yield Volatility Management Bond Fund

Value Partners Greater China High Yield Fund

E-Fonda (Hong Kong) Short-Term Bond Fund

BlackRock China Bond Fund

(2) US investment grade bond funds (the screening principle is bond type, the investment theme is the US and the top five performers in the past year)

Franklin US Government Fund

Hanya invests in US premium bond funds

BlackRock US Government Mortgage Bond Impact Fund

New York Mellon US Municipal Infrastructure Bond Investment Fund

Hanya invests in US premium bond funds

Securities Regulatory Commission Licensee: Kwong Chi-kit CE No: BNU325

Disclaimers

The content of this document is for reference only. It is not and should not be construed as an offer or recommendation from Futu Securities International (Hong Kong) Limited (“Futu Securities”), nor should it be interpreted as professional advice or investment advice. You should fully understand the risks and benefits before making any investment decision, and should consult a professional advisor if necessary.

Futu Securities strives for the objectivity and impartiality of the data and quoted data in this document, but cannot guarantee its accuracy, completeness and reliability.

Futu Securities and its associated companies will not be liable for any losses arising from reliance on or use of the contents of this file.

This document is for users within the Hong Kong Special Administrative Region only. Non-Hong Kong investors are responsible for complying with all applicable laws and regulations of their relevant jurisdiction.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

4