Overseas Consumption Sector: Intensive Release of Consumption-Boosting Policies; Focus on the Recovery of Offline Consumption Scenarios Post-Pandemic

Core Argument

1. Consumption-boosting policies have been introduced frequently, and recently many regions have adjusted their COVID-19 prevention and control measures, bolstering market confidence.

Epidemic prevention policies have been adjusted, and the orderly resumption of population mobility is underway.On June 28, the ninth edition of the COVID-19 Prevention and Control Plan was released, optimizing and adjusting the duration and methods of isolation management for individuals at risk, standardizing the criteria for designating lockdown zones and medium- and high-risk areas, preventing the layer-by-layer escalation of policies, and requiring the timely elimination of inconsistent measures.

In the catering sector, Shanghai will resume dine-in services in an orderly manner starting June 29; in tourism, travel restrictions are being gradually relaxed, the peak summer travel season is approaching, and bookings for inter-provincial group tours have clearly rebounded. Beijing Universal Resort and Shanghai Disneyland will resume operations.

Since late May, a flurry of policies and measures to stimulate consumption have been rolled out, with local governments actively introducing their own initiatives. We expect further local measures to follow, as bolstering consumption within regions is crucial for underpinning regional economic recovery and ensuring steady growth.

2、A Review of Recent Consumer Data: Online Retail Recovery Was Prominent in May, with the "618" Mega Sale Showing a Weak Rebound

Under the theme of resuming work and production, total retail sales of consumer goods improved overall in May, benefiting from factors such as supply-chain and logistics enhancements.From a structural perspective, commodity consumption has rebounded relatively quickly, while offline dining has recovered more slowly and remains at a lower level. E-commerce consumption bottomed out in May; given that the "618" shopping festival accounts for a significant share of June's online retail sales of physical goods, we expect June's online retail sales of physical goods to recover further compared with April and May.

Looking back at the 618 shopping festival data, the overall picture shows a weak recovery, with GMV growth slowing and integrated e-commerce performing slightly below expectations, while livestream e-commerce posted strong growth.During the 2022 "618" shopping festival (from 8:00 PM on May 31, 2022, to midnight on June 18, 2022), total GMV across all platforms reached RMB 695.9 billion, up 8.2% year on year.

3、The direction of consumption recovery in the second half of the year is relatively clear, but some restraining factors still remain.

With the gradual implementation of consumption-boosting policies across regions and the easing of pandemic-related disruptions, sentiment in the consumer sector has rebounded markedly, and some high-quality consumer companies remain at valuation lows.Against the backdrop of economic headwinds, the theme of consumption recovery in the second half of the year is relatively well-defined, with the sustainability of the recovery process serving as the core determinant. While the overarching direction is clear, several restraining factors remain: in the first quarter, there was a marked increase in business closures, rising unemployment has dampened disposable income, consumer willingness to spend has declined, and a cautious wait-and-see attitude prevails. These adverse factors are unlikely to reverse quickly in the short term, thereby limiting the extent of the rebound in this round of consumption recovery.

Investment Recommendation

Discretionary consumption is more resilient in the post-pandemic era; we recommend focusing on the recovery of offline channels.During the pandemic, both discretionary and essential consumption were significantly impacted; however, discretionary consumer goods generally exhibited greater profit volatility, particularly in offline consumption scenarios, which demonstrated greater post-pandemic elasticity.

Following the impact of the pandemic, the recovery of offline consumption scenarios will gradually gain momentum. In particular, sportswear, dining, travel, and hospitality are expected to demonstrate stronger resilience in their rebound.(1) Sports footwear and apparel: Favorable government policies are underpinning strong industry momentum, with domestic sports brands continuing to enjoy steady and positive growth, benefiting from the relaxation of consumption restrictions and the resulting increase in demand for outdoor activities. (2) Dining: Improving COVID-19 conditions in many regions have spurred a rapid recovery in the downstream dining sector, with Shanghai's resumption of dine-in service boosting market confidence; as consumption scenarios fully reopen, pent-up consumer demand from the earlier period is expected to be unleashed. (3) Tourism, travel, and hospitality: With the peak summer travel season approaching, Ctrip's booking volumes and passenger traffic at Hainan's airports both point to an accelerating rebound in the tourism market, while market consolidation is likely to benefit leading companies.

Risk Warning

Recurring COVID-19 outbreaks and a slower-than-expected post-pandemic recovery have dampened consumer confidence.

Main Text

1. Consumption-boosting policies have been introduced frequently, and recently many regions have adjusted their COVID-19 prevention and control measures, bolstering market confidence.

The ninth edition of the COVID-19 Prevention and Control Plan, released on June 28, optimizes and adjusts the duration and methods of quarantine for at-risk individuals, standardizes the criteria for designating lockdown zones and medium- and high-risk areas, and seeks to prevent the imposition of increasingly stringent measures at each administrative level.Specifically, the quarantine and management period for close contacts and inbound travelers has been adjusted from '14 days of centralized quarantine for medical observation plus 7 days of home health monitoring' to '7 days of centralized quarantine for medical observation plus 3 days of home health monitoring'; the control measures for secondary close contacts have been adjusted from '7 days of centralized quarantine for medical observation' to '7 days of home isolation for medical observation,' with nucleic acid testing on days 1, 4, and 7. The concept of medium- and high-risk areas is now uniformly applied, thereby establishing a new framework for delineating and managing risk zones. The National Health Commission emphasizes that all localities and departments must strictly implement the 'Prevention and Control Plan for Novel Coronavirus Pneumonia (9th Edition),' resolutely enforcing measures that must be enforced, fully implementing those that must be implemented, and promptly abolishing those that should be abolished; any inconsistent measures are to be rectified within a specified time limit.

Recently, many regions have adjusted their epidemic prevention policies, leading to an orderly resumption of population mobility.According to incomplete statistics: 1) Hefei has suspended routine nucleic acid testing. 2) Starting at midnight on June 25, Hangzhou in Zhejiang Province has extended the frequency of routine nucleic acid testing from every 72 hours to every seven days; on the 24th, Zhoushan in Zhejiang announced the suspension of the requirement for residents to undergo routine nucleic acid testing once every seven days. 3) On June 22, Hubei announced that the province would adjust its nucleic acid testing regime from 'once every three days' to 'once every five days.' 4) Hainan has relaxed entry restrictions: effective June 22, non–epidemic-affected-area travelers entering Hainan are required only to undergo a nucleic acid test upon arrival and to conduct seven days of self-health monitoring; residents of Beijing and Shanghai who come from streets not classified as medium- or high-risk areas are no longer required to undergo centralized quarantine upon entering Hainan; in Shanghai, only Jing'an, Baoshan, and Putuo districts remain designated as 'general epidemic-affected areas,' subject to three days of home-based health monitoring.

In the catering sector, Shanghai will gradually resume dine-in services starting June 29.Effective June 29, dining-in at restaurants will be gradually resumed in subdistricts and towns within the jurisdiction that have no medium-risk areas and have reported no community-transmitted cases in the past week. The specific areas where dining-in is permitted will be determined by the respective district governments after a comprehensive assessment of the epidemic prevention and control situation.

In the tourism sector, travel restrictions are gradually being eased, the peak summer travel season is approaching, and bookings for inter-provincial group tours have rebounded markedly.。Starting June 25, Beijing Universal Resort will gradually resume operations with visitor capacity limits. Shanghai Disneyland will resume operations on June 30.Since the start of the Dragon Boat Festival, local governments across the country have rolled out a series of favorable policies to support the recovery and development of the cultural and tourism sectors, thereby boosting the rebound of the cultural and tourism market. On May 31, the Ministry of Culture and Tourism issued a notice further refining the 'circuit-breaker' mechanism for inter-provincial group tours down to the county (city, district, or banner) level, while many regions have launched cultural and tourism consumption vouchers to invigorate the market.

Since late May, a flurry of policies and measures to stimulate consumption have been rolled out. At the central level, the focus is on automobiles and household appliances, while at the local level, the emphasis is on automobiles, household appliances, cultural and tourism activities, and the catering sector. Local governments have been proactive in introducing consumption-stimulating policies, with a large number of initiatives covering a broad range of areas. The primary approach has been the issuance of consumption vouchers, offering one-time subsidies or spend-and-save discounts for purchases of household appliances, automobiles, furniture, and goods at supermarkets and hypermarkets.We expect that additional local measures to stimulate consumption will be introduced going forward. As first-tier cities such as Beijing and Shanghai enter the post-pandemic era, stepping up efforts to boost intra-regional consumption is crucial for underpinning regional economic recovery and ensuring stable growth.

2. Online retail rebounded markedly in May, with the "618" shopping festival showing a weak recovery.

Under the theme of resuming work and production in May, total retail sales of consumer goods improved overall thanks to factors such as supply-chain and logistics enhancements, but remained relatively weak.On June 15, the National Bureau of Statistics released retail sales data for May 2022. In May 2022, China's total retail sales of consumer goods amounted to RMB 3.35 trillion, down 6.7% year on year (compared with an 11.1% decline in April), with the year-on-year decline narrowing on a month-on-month basis and consumer demand showing some improvement. Excluding automobiles, retail sales of consumer goods totaled RMB 3.04 trillion, down 5.6% year on year.

From a structural perspective, commodity consumption has rebounded relatively quickly, while offline dining has recovered more slowly and remains at a lower level.In May, retail sales of goods fell 5.0% year on year, with the decline narrowing by 4.7 percentage points from the previous month; catering revenue declined 21.1% year on year, with the drop narrowing by 1.6 percentage points from the previous month, reflecting ongoing gaps in offline consumption scenarios under pandemic control policies.

From a category perspective, essential consumption performed relatively well, while discretionary consumption remains weak.In May, among the 15 categories of retail sales of consumer goods, only food and oil products, tobacco and alcohol beverages, pharmaceuticals, and petroleum products posted positive growth. These categories are characterized by essential demand and immediate consumption. Meanwhile, discretionary spending categories such as apparel, cosmetics, gold and silver jewelry, and household appliances and audiovisual equipment continued to experience negative growth, though the rate of decline has narrowed.

Figure: Month-on-Month Year-on-Year Growth Rate of Total Retail Sales of Consumer Goods, %

Figure: Month-on-Month and Year-on-Year Growth in Retail Sales of Goods Above the Designated Size by Category, %

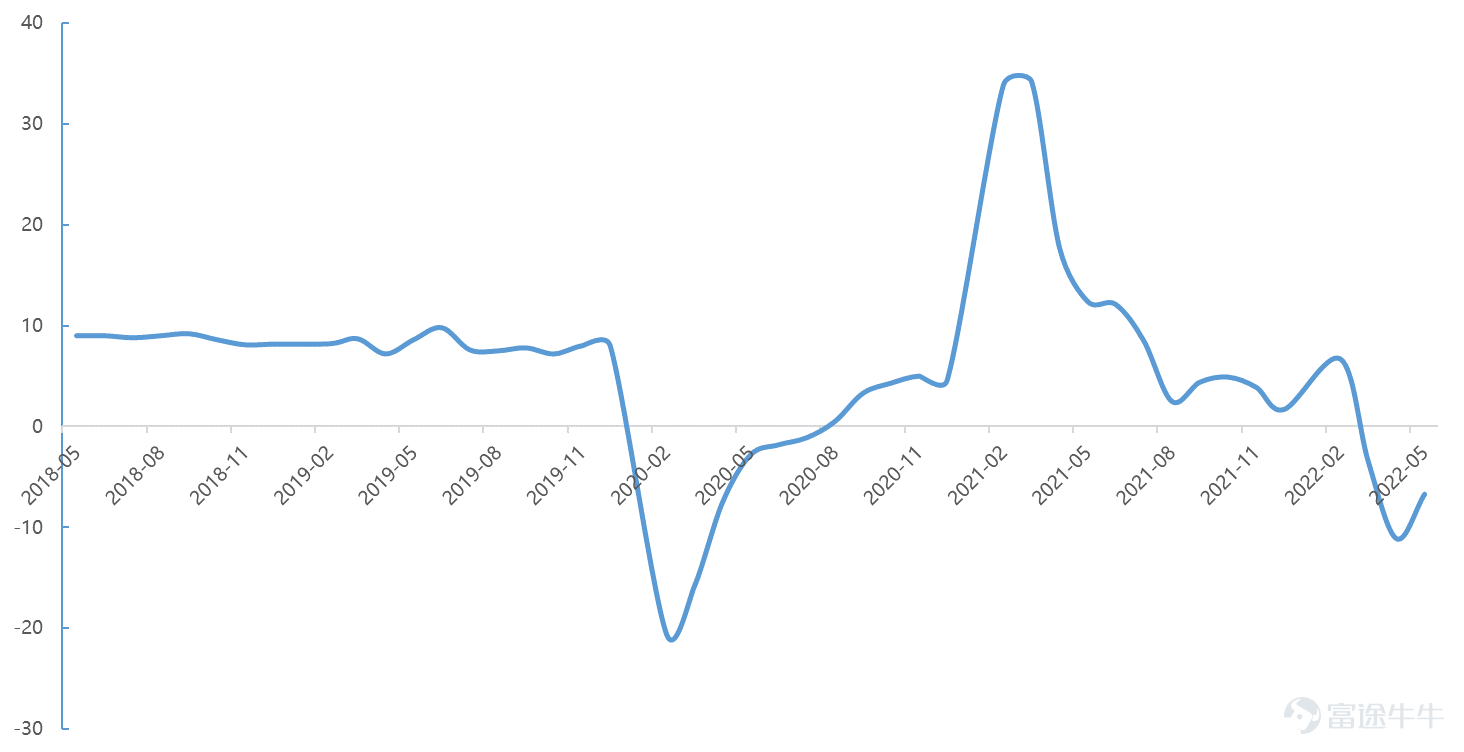

E-commerce consumption bottomed out and rebounded in May. Given that the "618" shopping festival accounts for a significant share of June's online retail sales of physical goods, we expect June's online retail sales of physical goods to recover further compared with April and May.In May, the year-on-year growth rate of online retail sales of physical goods turned positive for the first time, rising by 14.3%—a result of the recovery in express delivery services and the rebound in consumer spending.

Figure: Online Retail Sales of Physical Goods and Year-on-Year Growth Rate, in RMB 100 million

Looking back at the 618 shopping festival data, the overall picture shows a weak recovery, with GMV growth slowing and integrated e-commerce performing slightly below expectations, while livestream e-commerce posted strong growth.According to data from Xingtu, during the 2022 "618" shopping festival (from 8:00 PM on May 31, 2022, to midnight on June 18, 2022), total GMV across all platforms reached RMB 695.9 billion, up 8.2% year on year (calculated using last year's combined e-commerce and livestreaming e-commerce figures versus this year's overall platform GMV). Specifically, GMV from traditional e-commerce totaled RMB 582.6 billion, up 0.7% year on year (compared with a 26.5% growth rate in 2021); livestreaming e-commerce recorded RMB 144.5 billion, a year-on-year increase of 124%, accounting for 20.8% of total platform sales—a 9.7 percentage-point rise from the previous year.

Figure: Total e-commerce transaction volume and its growth rate during the 618 shopping festival, in billion yuan

During the '618' shopping festival, essential categories such as cleaning and personal care performed well, while sports goods posted robust growth; however, discretionary spending on fashion items like beauty products declined. Supported by subsidy policies, big-ticket discretionary purchases—led by home appliances—experienced a rebound.During this year's 618 shopping festival, omnichannel sales of personal care and cleaning products as well as convenient ready-to-eat meals increased by 33.7% and 27.5% year on year, respectively, while beauty and skincare products and fragrances and color cosmetics saw year-on-year declines of 18.9% and 22.1%, respectively. Across all online channels, home appliance sales rose 6.7% year on year, driven by enhanced subsidy policies and the release of pent-up demand that had been suppressed during the pandemic; prior to this, home appliance sales had posted negative growth from March to May. Meanwhile, the sports and outdoor category recorded total online sales of RMB 24.9 billion, up about 9% year on year, with the robust recovery during the 618 period effectively offsetting weaker offline performance.

Figure: Year-on-Year Sales Growth Rate of Key Product Categories During the 618 Shopping Festival, in Percent

3. Consumption patterns are relatively well-defined, but certain constraints still exist.

With the gradual implementation of consumption-boosting policies across regions and the easing of pandemic-related disruptions, sentiment in the consumer sector has rebounded markedly, and some high-quality consumer companies remain at valuation lows. Against the backdrop of economic headwinds, the theme of a second-half recovery in consumption is relatively certain, with the sustained nature of the recovery serving as the core driver.。

With the broad direction now set, the consumption recovery in the second half of the year will still face certain constraints.For instance, in the first quarter, there was a marked increase in business closures, which, coupled with rising unemployment, constrained disposable income, dampened consumers' willingness to spend, and fostered a cautious, wait-and-see attitude. These adverse factors are unlikely to reverse quickly in the short term, thereby limiting the strength of the current rebound in consumption. In May, the surveyed urban unemployment rate reached 5.9%, nearing the peak level seen during the previous wave of the pandemic. A significant negative correlation exists between per capita disposable income and the unemployment rate, and the uncertainty surrounding future income has already begun to influence household consumption decisions.

Consumers remain cautious and adopt a wait-and-see approach, with average order values declining in more than half of product categories during the '618' shopping festival. According to data from Magic Mirror Intelligence, unlike the across-the-board increase in average order values across all categories during the 2021 '618' event, this year more than half of the top 10 categories on Tmall saw a decline in average order value during the '618' period.

Figure: Decomposition of Factors Influencing Consumption Recovery

Figure: Urban Unemployment Rate in China, %

4. Discretionary consumption exhibits greater post-pandemic resilience; we recommend focusing on the recovery of offline channels.

During the pandemic, both discretionary and essential consumer goods were significantly impacted; however, discretionary consumer goods generally exhibited greater profit volatility.The essential consumption sector is defensive in nature, with relatively stable demand; however, it lacks high-growth potential during the recovery phase. Moreover, as post-pandemic at-home scenarios diminish, demand for certain essential consumer goods that were purchased during the pandemic due to stockpiling may decline as inventory levels rise.

Figure: Decomposition of the Impact of Consumption Recovery on Consumer Goods

Meanwhile, discretionary consumption exhibits greater elasticity, and we are more optimistic about its post-pandemic recovery, particularly as offline consumption scenarios gradually begin to rebound.Specifically, sportswear, food and beverage, travel, and hospitality are expected to demonstrate greater resilience.

Athletic footwear and apparel: Favorable government policies are driving strong industry growth, with domestic sports brands continuing to demonstrate steady and positive momentum, benefiting from the relaxation of consumption restrictions and the resulting increase in demand for outdoor activities.The Sports Law, revised and adopted on June 24, continues to provide policy and regulatory support for the development of the sports industry and related sportswear and footwear sectors. During the "618" shopping festival, Nike and Anta Sports delivered outstanding performance in the sportswear and footwear category, both posting year-on-year growth of more than double—up 218% and 136%, respectively. Li Ning and Xtep also posted year-on-year growth of 10% and 23%, respectively, highlighting the strong growth potential of the sportswear segment. Coupled with the heightened health awareness among consumers following the pandemic, sportswear is poised for a relatively rapid recovery, which will gradually unfold as the recovery process progresses. We recommend paying close attention to Li Ning (02331.HK), Anta Sports (02020.HK), and Xtep International (01368.HK).

Food and Beverage: Improving COVID-19 conditions in many regions have spurred a rapid recovery in the downstream dining sector, with Shanghai's resumption of dine-in service boosting market confidence. As dining scenarios fully reopen, pent-up consumer demand from the earlier period is expected to be unleashed.In May, the catering industry remained under pressure due to the impact of COVID-19 in some regions, with valuations for certain restaurant operators still at low levels. We recommend paying attention to Jiu Mao Jiu (09922.HK), which boasts an efficient single-store model and is in a growth phase.

Travel and Hospitality: With the peak summer travel season underway and restrictions easing, Ctrip's booking data indicate that the tourism market is accelerating its recovery.According to data from Ctrip, as of June 21, bookings for interprovincial package tours during the summer travel season increased by 291% week-on-week over the previous week, while bookings for interprovincial hotel stays rose by 151% week-on-week. Ctrip's average daily order volume in June has already surpassed the level recorded during the same period last year. Following the relaxation of travel restrictions, Hainan Airport handled 427,000 passenger trips from June 13 to June 19, a week-on-week increase of 18.24%, bringing traffic back to 62.04% of the level seen in the same period of 2019 and 152.60% of the level one month earlier.

The three-year pandemic has had a prolonged impact on the hotel industry, accelerating industry consolidation. Leading companies, leveraging their risk resilience, have expanded their footprint against the market trend, resulting in significant increases in chain penetration and industry concentration. With the boost from pro-consumption policies and the waning of pandemic-related disruptions, the hotel sector—previously hard hit by the crisis—is expected to reach an inflection point. Meanwhile, the pandemic has reshaped consumer habits, with heightened awareness of hygiene and safety, making branded, chain-operated hotels the preferred choice; leading chain operators are likely to benefit. We recommend focusing on industry leaders such as Huazhu Group (01179.HK), Jinjiang Hotels, and the scenic-area entertainment sector.

Risk Warning

Recurring COVID-19 outbreaks and a slower-than-expected post-pandemic recovery have dampened consumer confidence.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

19