美團Q4財報出爐,股價大幅拉升

Despite the loss, Meituan's dream of dominating local life is still full | Depth of Wealth

Since February, Meituan$MEITUAN-W (03690.HK)$Under the impact of a series of events, it ushered in the darkest two months since the launch. On February 18, the Ministry of Commerce called on takeaway platform companies to reduce fees for takeout merchants in areas with severe epidemics, causing market panic. Since then, Meituan has begun a rapid wave of sharp declines of up to 60%. During this period, people's congress deputies also saw popular searches calling for young people to go to the factory instead of delivering takeout, which once again pushed Meituan to the forefront. Since March, due to the spread of the epidemic across the country, Meituan Cash's dairy delivery business has been seriously affected, and fundamental concerns have accelerated another round of decline.

In the past year, Meituan's days couldn't be described as sad. Under anti-monopoly pressure, Meituan had quite the meaning of becoming a “street rat,” and everyone shouted. For young Meituan, this is both a pain and an experience. Having experienced huge anti-monopoly fines, they have also focused on rectifying the act of choosing one of the two, and have continuously responded to the country's call to actually implement fee reduction measures.

In the current context of multiple outbreaks of the epidemic, Meituan is still using its own actions to contribute its value to the normal operation of the city. This value is one of the foundations for maintaining the efficient operation of the entire city. Many cities have “slowed down” because of the epidemic, yet Meituan is still “in full swing”.

At this point, Meituan, which has fallen below the trillion dollar mark, is it still worth being optimistic about? Has the borderless expansion of local life supremacy come to an end once and for all? This is probably everyone's biggest concern right now.

We believe that Meituan's core business roots have not wavered. The main views are as follows:

1. Under the epidemic, the process of “digitalization” of local life has accelerated markedly. This process is irreversible, and Meituan will still benefit deeply from this trend:In the two years since the outbreak of the epidemic, Meituan's B-side and C-side penetration rates have increased rapidly. As of the fourth quarter, Meituan's number of trading users was 690 million, an increase of more than 200 million compared to before the pandemic. The number of B-side merchants also increased steadily, and the increase in the number of users gave Meituan the possibility of more monetization. Judging from business data, whether it was the average number of purchases per user per year or the monetization rate, which was not greatly affected. Behind Meituan, the trend of digital transformation of the entire lifestyle is irreversible.

2. The local lifestyle dominates the closed loop of high-frequency and low-frequency traffic. It is still intact. The competitive pattern was optimized after capital inflow was reduced:Meituan's boundaries continue to expand. From in-store business to takeout to community group purchases, Meituan has built a strong business foundation step by step. That is, in difficult times like '21, Meituan's community group buying is still heavily invested, and under the intensification of anti-monopoly, community group buying participants, including Orange Heart Preferred, Xing Sheng Preferred, and Ten Hui Group, have successively broken down, and Meituan community group buying has maintained steady growth. As long as Meituan's underlying ecological logic remains unchanged, in the future, Meituan will still benefit deeply from the continuous increase in residents' overall income income. After all, Meituan is already the most important member of Community Zero.

3. The in-store cash cow business has maintained steady growth and continues to increase its share. However, the results of the community group buying war are basically clear, with Meituan Preferential leading the way:Under pressure, Meituan's takeout business has maintained very good resilience. The overall takeout monetization rate is still increasing, and losses in community group buying are also narrowing. We judge that the competition for community group buying is nearing its end. Meituan is undoubtedly the biggest winner right now.

Next, let's look for some answers from Meituan's latest financial report.

The overall 21Q4 earnings report exceeded market expectations, showing tenacity in the midst of pessimism

Judging from Bloomberg's unanimous expectations, Meituan's quarterly results were all in line with expectations on the revenue side. On the profit side, expectations were greatly exceeded. The main points that exceeded expectations were takeout operating profits and the extent of losses in innovative businesses. This sets the tone for Meituan's overall performance this quarter, which is very good.

Judging from the financial report for the fourth quarter, the following points are worth paying attention to:

First, the penetration rate at both the B and C ends has further increased: after all, the number of trading users is at the 700 million mark, and the number of B-side merchants is still growing steadily

First, let's take a look at Meituan's various operating data. These data are important indicators for us to observe Meituan's expansion period, and are also a reference for observing Meituan's revenue quality and loss trends.

The number of trading users of Meituan increased again in the fourth quarter. In the quarter, it received 23 million new trading users, reaching 690 million. 690 million. In the short term, under the current domestic internet penetration situation, Meituan has basically covered all the users it may have covered.The reason why the number of trading users grew in '21 is the penetration of community group buying into lower-tier cities and the penetration of grandmothers and grandparents (older people who hardly use takeout and don't use in-store businesses).

Now, after getting their group of users, Meituan community group purchases have also basically covered all regions.The stage of large-scale advertising and subsidies to acquire customers is almost over. Along with high-pressure policies such as anti-monopoly and anti-unfair competition, it is similar to Pinduoduo's strategy. The marginal effects of further customer acquisition may be far less than tapping into the higher consumer demand of existing active users。

As a result, the number of new Meituan users is declining quarterly, which is understandable; this is not a very bad concern.

From the perspective of active merchants, this data may be very contrary to everyone's basic concept. The number of active businesses in Meituan began to grow rapidly after the pandemic, and has continued to increase by more than 500,000 per quarter since the second quarter of this year. Also, I remember that the second quarter was the quarter where the General Administration of Market Regulation chose one against the other. The result was that platforms such as Hungry and word of mouth, which lured merchants to choose one by giving rebates and red envelopes, lost their appeal to merchants, so merchants voted with their legs and looked at it together on the Meituan platform last time.

We have always emphasized that although Meituan is a B2B2C platform, it is also considered the largest SaaS provider in the catering and service industry. It's just that he doesn't charge SaaS subscription fees, but instead earns money through commissions。

Here's what I wrote in Meituan's earnings report:

“On the merchant side, we continue to help millions of restaurants implement digital operations by providing integrated services and online marketing tools, bringing more business volume to merchants and helping them generate revenue in this challenging environment. Since it can effectively promote consumer demand, more and more merchants are starting to use our online marketing products and increase their online promotion efforts.”

“We are increasing our penetration into low-tier cities across the country, expanding our coverage, and helping accelerate the digital transformation of underdeveloped markets of services. Categories such as leisure and entertainment, fitness, nursing services, medical care and pet services are gaining momentum; while categories such as handicraft activities, recording studios, interactive light and video centers, and decompression experience centers have become new consumption trends. Furthermore, we continue to launch customized products and services for all types of merchants to help them improve their online operation level.”

Improve the digital operation methods of low-tier cities, give them high-quality marketing tools, and launch customized products and services for all kinds of merchants. This operation has slipped away like the best PLG SaaS company in the US. If Zhenmeituan doesn't have any quality or changes its revenue method to generate subscription fee revenue, will it be 30 times PS right away?

Moreover, this kind of support for businesses in low-tier cities only hopes that a certain percentage of the transaction amount can be deducted from the free service. To a certain extent, this is also implementing “common prosperity,” so that information technology can benefit more groups.

How to determine that Meituan can tap deeper consumer demand and usage stickiness depends on the average number of transactions per transaction user per year.

However, there is no doubt that judging from the number of users and transactions, it is difficult to replicate such high growth in the previous stage. Therefore, Meituan's high valuation of 400 yuan or more is expected to be difficult to meet for some time to come.We must also be reminded here that it is not possible to extrapolate linearly during the high growth phase of the company's time, location, and people.

In the fourth quarter, the number of transactions reached 35.8 times per year per Meituan user, increasing steadily quarterly starting in Q2 '20. We saw a high point in Q4 '19, then began to decline in Q1 and Q2 in '20. The main reason was that the pandemic made it impossible to spend outside. Then, with the end of the large-scale blockade, the average number of annual transactions increased, and as the number of new Meituan community group buyers acquired it, the total number of trading users also increased, and Meituan ushered in a stage of rapid development of COVID-19 dividends.

However, there is no doubt that judging from the number of users and transactions, it is difficult to replicate such high growth in the previous stage. Therefore, Meituan's high valuation of 400 yuan or more is expected to be difficult to meet for some time to come.We must also be reminded here that it is not possible to extrapolate linearly during the high growth phase of the company's time, location, and people.

Looking at the takeout business, the overall takeout GTV growth rate declined, and it declined quarter by quarter, recording 20.69%. Two of these reasons:

l The low base effect caused by the epidemic is that the growth rate in the first quarter and second quarter was ridiculously high

l The macroeconomy is bad, and the consumption growth rate itself is very poor. Social zero growth rates were 4.9%, 3.9%, and 1.7% respectively from October to December '21. Combined, it was 3.46% year on year in the fourth quarter. Meituan still surpassed the market by nearly 17 percentage points compared to the market

In this regard, takeout's share of all consumers' meals is still increasing, and the takeout penetration rate is further increasing. But on the other hand, are we hungry? We can see some clues from Ali's local lifestyle business. Ali's local lifestyle business merged Gaode and Flying Pig in the third quarter, and Gaode began expanding the taxi business in the third quarter. Under such circumstances, the growth rate of local lifestyle Q4 was only about 20%, so we can see that Meituan's market share is still increasing further, reducing the living space of hungry people.

This growth rate of takeout GTV, when split, is mainly due to an increase in the number of takeout orders, rather than an increase in GTV per unit.

Judging from the average GTV, it is basically stable and remains between 48 yuan and 49 yuan. It seems that it is indeed difficult to break through the 50 yuan mark once again. Of course, it is not ruled out that this year's inflationary pressure is due to inflation, not the increase in the number of items per order point. So it is likely that in the case where the stable average GTV per order we are currently observing is 48-49 yuan, the price increase due to inflation will reduce the average number of takeout transactions per day.

Judging from the average number of takeout transactions per day, the trend is similar to Total Takeout GTV. According to the company, the increase in orders is due to the addition of breakfast, afternoon tea, and supper. Takeout is not just about food delivery; it can also deliver milk tea, skewers, and crayfish. Of course, this is also changing as young people's consumption habits change. The penetration rate of afternoon tea and supper is also increasing as everyone's consumption capacity increases, so consumption in the fourth quarter and the first quarter of this year may also be downgraded due to macroeconomic changes, changing from crayfish to hot pot.

At the performance conference call last night, management said that the average daily order peak now exceeds 50 million orders. Looking forward to the future, the company hopes to reach the level of 100 million orders per day, and the in-store business to reach the level of 10 million orders per day. Let's make a rough estimate. An average of 100 million takeout orders per day represents the eating problem of 100 million people. When I arrived at the store, three or five groups of friends went out to dinner and hang out. Roughly speaking, 3 people represented 30 million people. Taken together, this is equivalent to Meituan's platform solving the eating and entertainment problems of 130 million people a day, accounting for 1/5 of the total number of current users. Actually, it's not that difficult to achieve.

The last item is the number of nights spent at the hotel. There was a slight year-on-year decline in the number of nights in hotels this quarter. In fact, the reason is also simple: the pandemic has caused blockades in some regions and reduced consumers' desire to travel. The year-on-year decline was not significant, from 119.70 million in Q4 2020 to 115.30 million.

This decline is actually not significant. Compared with OTA peers, Tongcheng Travel's GTV fell 11% year over year, and Ctrip's GTV fell 14% year over year. Although it is a bit inappropriate compared to other people's GTV, I can see that the industry can't do this. Meituan's decline doesn't seem as amazing as its two peers.

Second, they finally chose not to be so “good” for users. After user subsidies were reduced, takeout profit margins continued to take off

Amid criticism from various parties demanding that Meituan reduce fees for merchants, the market is worried that Meituan Takeout's profit margin will deteriorate further. However, after digging deeper into UE for takeout, everyone discovered that Meituan is too good for users, so the market is looking forward to when Meituan will not be as good for users and make profits. Meituan's financial report for the fourth quarter uses data to tell you the answer, which is to begin cutting fees in this quarter and redistribute profits from users to businesses and Meituan itself.

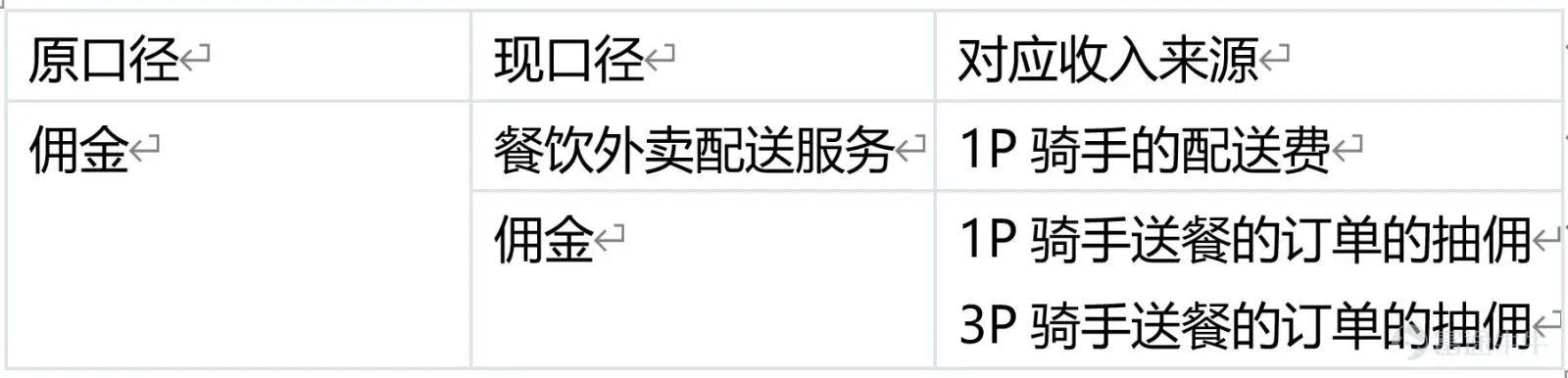

The first is takeout revenue. Food and beverage takeout revenue for the quarter was $26.127 billion, up 21.30% year over year. Revenue was slightly higher year over year for GTV, less than 1% year over year. The overall take rate was 0.1% higher than in the fourth quarter of last year.

If food and beverage takeout revenue is split, starting this quarter, Meituan further split the original commission revenue scale into commission income and food takeout delivery revenue. It also clarified the two sources of revenue for the market:

Therefore, we can see in detail how much the actual commission rate of Meituan actually is also considered to have blocked the mouths of some people who spray Meituan vampires from day to night.

If we look at the actual commission rate, it was 4.12% for the quarter, up 0.26% from 3.86% last year. Looking at the whole year, the actual commission rate in '21 was 4.07%, which is 0.29% higher than in '20. In other words, the average GTV order was 48 yuan, and Meituan actually drew 1.98 commissions, which is 0.12 yuan higher than the same period last year.

If we look at the actual commission rate, it was 4.12% for the quarter, up 0.26% from 3.86% last year. Looking at the whole year, the actual commission rate in '21 was 4.07%, which is 0.29% higher than in '20. In other words, the average GTV order was 48 yuan, and Meituan actually drew 1.98 commissions, which is 0.12 yuan higher than the same period last year.

The other part is delivery revenue. Meituan has begun implementing a transparent delivery fee system across the country, telling merchants and consumers clear delivery service fee rules based on factors such as delivery distance and weather, and has been extended to most regions. This quarter, Meituan also began to separately list the revenue and costs of distribution services to achieve transparency.

Comparing revenue and costs, it can be seen that Meituan has always been unable to make ends meet in the revenue from delivery services. At least, based on the data he disclosed for the four periods, this is the case. Among them, this subsidy covered more than 4 billion riders in the fourth quarter of '21, and more than 12.7 billion dollars for the full year of '21.

After implementing a transparent system, riders' income was clarified. It is expected that the Meituan subsidy level will also drop further, and judging from actual data, merchant delivery costs have also been reduced. The average rider cost dropped from 4.88 yuan in the fourth quarter of last year to 4.68 yuan.

Then there is the other segment, which accounts for the majority of the takeout business, online marketing revenue. Online marketing revenue recorded 3.23 billion yuan in the quarter, accounting for a further increase in the share of total food and beverage revenue, reaching 12.34%. This business mainly involves merchants increasing the exposure of their stores by participating in events or purchasing rankings, etc., and participating in full reduction activities to increase the amount of takeout per order for users. One of the increases in revenue is an increase in overall GTV, and the second is an increase in advertising monetization rates. This revenue is Meituan's high-margin business, and the increase in share has further released Meituan Takeaway's operating profit.

The increase in monetization rates indicates that merchants are more willing to participate in activities and advertise on the Meituan platform. However, this is probably also what the merchants criticized the most. After participating in the event, their actual income decreased, causing them to be unable to make ends meet. If you don't participate, other merchants will participate, and your order volume will drop significantly. In fact, as long as regional managers who can control Meituan do not maliciously downgrade the rights of businesses that do not participate in the event, this kind of campaign has become an open source tool for all merchants. In an open market-based competitive environment, this is also irreproachable, because sending out leaflets, shouting, and offline event membership cards for 1,000 to get 200 free is actually about the same as Meituan's online marketing expenses.

In terms of profit margins, the operating margin of Meituan's takeout business returned to more than 5% in the quarter, reaching 6.6%:

On a year-on-year basis, operating profit increased 96.7% from 882.4 million yuan in Q4 2020 to 1.7 billion yuan in the same period in '21, and operating profit margin increased from 4.10% to 6.64%, mainly due to an increase in the number of transactions, a decrease in seasonal incentives for takeout riders, and revenue contributions from online marketing services. On a month-on-month basis, operating profit increased from 876.1 million yuan to 1.7 billion yuan in Q3 '21, and operating profit margin increased from 0.33% to 6.64%, mainly due to reduced user incentives and seasonal decline in food and beverage takeaway riders.

Comparing the month-on-month and year-over-year data, it can be clearly seen that the most obvious thing from Q3 to Q4 is that Meituan began to reduce the level of subsidies to users, so profit margins can be released.This quarter's data and this year's data were not disclosed in the financial report, but according to previous tracking, Meituan's subsidy for users was 0.66 yuan in '19 and 0.56 yuan in '20. Looking at our previous analysis, Meituan's actual commission in 2020 was 1.86 yuan per order, which is equivalent to subsidizing 1/3 of the commission income to users. This reduction, or continued reduction in the future, will actually increase the operating profit margin of each order in the takeout business, and is a strong guarantee for achieving an average operating profit of 1 yuan per order in 2025.

Furthermore, our further analysis found that even though user incentives declined, there was no significant decline in the total number of orders placed by Meituan Takeaway, the stickiness of users using takeout has been fully cultivated, and in the process of Meituan's further or market share, it is basically equivalent to a monopoly market position.In this situation, it is true that user incentives are gradually reduced to maintain user stickiness. Instead, the marginal effects of good merchants with good delivery and service will be more obvious, and they will also contribute more to their own profit margins.

Therefore, do we also need to worry that Q1 Meituan's subsidies to regions and merchants with severe epidemics will reduce Meituan's own profit margins?

I think this concern can be mitigated slightly. I can't guarantee that Meituan will continue to release profit margins in the first quarter when the epidemic is severe, but at least he has room for 0.56 yuan to cut fees. What is even more worrisome is the impact of the macro-decline on total order volume and average GTV per order. Fortunately, it is impossible not to end the epidemic. Due to the rapid recovery in consumption after the epidemic was lifted, it was also confirmed by management during this performance conference call. The impact of short-term fluctuations further determined Meituan's competitive advantage and moat.

Third, stable cash cows, in-store business advertising revenue boosting profit margins

The in-store business is still as stable as ever, serving as a cash cow for the entire Meituan company. However, the situation this quarter, like the takeout business, has been impacted by the epidemic, and the impact will be even greater, because the store business will be hit even harder by the pandemic.

The in-store business achieved revenue of 8.722 billion dollars in the quarter, an increase of 22.24% over the previous year.In this section, let's compare it with the GDP of the tertiary sector of GDP. The tertiary sector's GDP recorded a 4.60% year-on-year growth rate in the fourth quarter of '21, and Meituan outperformed the overall market by nearly 18%.

There is no doubt that the impact of the pandemic will continue to weigh on Meituan's in-store business revenue, and macroeconomic factors will also reduce consumers' desire to spend. However, as we mentioned above, the situation observed by management through data showed signs of a rapid recovery in consumption after the blockade was lifted in regions blocked due to the epidemic.

One important reason why Meituan was able to outperform the market by 18% is that Meituan and Volkswagen Dianping have become tools for stores to quickly recover from the pandemic. Includes low-tier markets, as well as new consumer categories. According to the company's financial report, the transaction volume, transaction amount, and number of active merchants in the company's point-to-point business all hit record highs. Strengthen the penetration of low-tier cities that seize power, expand coverage, and help accelerate digital transformation serving underdeveloped markets.

Looking at the share of online marketing in in-store revenue, the quarter also reached a record high. Online marketing accounted for 53.15% of total in-store revenue, up 3.5% year on year, and 1.08% month on month. It shows that as the epidemic continues to this stage, when the offline catering and offline service industries are becoming more difficult, everyone instead needs a strong open source channel to quickly resume their store business. Therefore, the number of active stores can naturally reach a new high, and the transformation in underdeveloped regions, we can understand that after community group buying opens up users in the low-tier market, it will naturally be possible to divert them from the high-frequency grocery shopping business to the low-frequency but highly profitable in-store business.

As a result, with the increase in the share of online marketing, the operating profit margin of the in-store business also gradually increased, eliminating the extreme value of Q1 in 2020, when the epidemic was worst. Now, the share of online marketing revenue is the highest in history, so the profit margin of the in-store business has also reached a record high of 44.68%.

According to the company's financial report, the year-on-year increase was due to improved marketing efficiency and changes in revenue structure, that is, an increase in the share of online marketing revenue. The reason for the month-on-month increase was a reduction in marketing investment related to hotels and tourism. As the company sinks further, the company's share of consumer mentality has further increased, gradually reducing investment in marketing and optimizing advertising efficiency on services and platforms, and the company can further expand the operating profit margin of this business.

During the performance call, some investors asked how the company should respond to the entry of short video platforms into the local lifestyle circuit. The company's response was that Meituan and Dazhong Dianping have accumulated more than 10 billion user reviews. This is a very important reference data for the supply side.Although the company doesn't have an advantage in short videos, and short videos do have a huge amount of traffic, the company has strong advantages in other tools, such as location-based tools, which can better match consumers and merchants, and actually created a new high transaction volume for merchants in the fourth quarter.

In fact, concerns about short videos began to be heard in the first quarter of '21. However, the actual situation dispelled these doubts in the market through Meituan's number of active merchants and the year-on-year increase in business revenue arriving at the store.

Fourth, new businesses open up resources and save money, and community group buying losses have narrowed: the community group buying war is basically coming to an end. The future focus is to reduce losses

The biggest feeling for me about the entire new business is that this quarter is in the process of adjusting the strategy. New business revenue for the quarter was the fastest year-on-year increase of all business revenue due to base issues.Q4 recorded revenue of 14.674 billion yuan, a year-on-year increase of 58.74%. The growth rate is slowing down quarter by quarter. One reason is that the fourth quarter of last year was the first quarter where community group buying began. Second, the growth rate of the community group buying business actually declined.

Looking at it from a month-on-month perspective, you can actually see the development of the new business. If you look at it month-on-month, it is quite obvious that the growth rate is slowing down. The fourth quarter increased by only 6.93% compared to the third quarter, and the absolute value of revenue increased by less than 1 billion dollars.

At the same time, according to the company's financial reports and some data provided by the telephone conference, it can be seen that Meituan's express delivery business is developing very fast.

The company's financial report mentioned that in December 2021, the peak number of orders for Meituan Express in a single day exceeded 6.3 million, and categories such as flowers, supermarkets and convenience stores continued to maintain a high growth trend.In the company conference call, it was mentioned that Flash Delivery's GTV already accounts for 12% of food and beverage takeout GTV, or the level of 84.2 billion. Considering that Flash Delivery's business model is the same as takeout and calculated at the same monetization rate, Flash Delivery provided more than 1 billion yuan in revenue in 2021. Furthermore, there are 230 million active users of Flash Delivery, accounting for 33% of all Meituan users.

The company's financial report mentioned that in December 2021, the peak number of orders for Meituan Express in a single day exceeded 6.3 million, and categories such as flowers, supermarkets and convenience stores continued to maintain a high growth trend.In the company conference call, it was mentioned that Flash Delivery's GTV already accounts for 12% of food and beverage takeout GTV, or the level of 84.2 billion. Considering that Flash Delivery's business model is the same as takeout and calculated at the same monetization rate, Flash Delivery provided more than 1 billion yuan in revenue in 2021. Furthermore, there are 230 million active users of Flash Delivery, accounting for 33% of all Meituan users.

However, after the Meituan Grocery Shopping Company has carried out sufficient tests, it is currently only doing business in first-tier cities and is not expanding further regionally. In 2021, the number of users and transaction amounts of Meituan Grocery Shopping continued to increase. Now, the company's main focus in this area of business is to optimize SKU, strengthen warehousing and logistics capabilities, improve Yu Ning of the front warehouse, and promote the improvement of UE.

The flash delivery and grocery shopping business grew very rapidly in January-February of this year, particularly Meituan Express's fresh delivery. The entire flash delivery business grew by about 70%-80% during the Lunar New Year period.

Well, the community group buying business, which has received the most attention among the new businesses, based on previous analysis of flash delivery and grocery shopping, Meituan Premium's revenue in the fourth quarter is likely to be close to zero. However, Meituan Preferred Business is still in the process of development, mainly due to savings.

In fact, with the third quarter and the fourth quarter, the Meituan and Pinduoduo community group buying businesses basically covered most of the country's logistics network and team leader network, and the stage of rapid expansion of money was actually basically over.Furthermore, on the entire community group buying circuit, we can also see a clear decline. Ten Hai Group, Tongcheng Life, and Orange Heart Preferred have gone out of business or withdrawn one after another. In the situation where the two superteams of the community group buying circuit are competing, the regional competition has basically come to an end. Coupled with the further tightening of regulations, everyone has no energy or need to further subsidize customers. Instead, optimize products, optimize delivery logic, and optimize unit economic efficiency (UE).

Indeed, according to Meituan's own earnings reports and phone calls for this quarter, Meituan Preferred is doing these things in this quarter:

“In 2021, we will continue to optimize the operation of each node to improve operational efficiency and unit economic efficiency. The “next day delivery” third-level warehousing and logistics network system created by Meituan Premium has now covered most communities and rural areas in 30 provinces across the country. We continue to provide a richer and more diverse product range while improving fulfillment efficiency and reliability. Our “Direct Farming” program enables us to efficiently match production and demand through centralized procurement and customized procurement models, thereby generating additional income for farmers. Rural residents can also more easily obtain the rich and cost-effective necessities of life that previously only urban residents could obtain, eliminate the consumption gap between urban and rural areas, and further empower modern agriculture.”

“Community e-commerce actually had good growth in 2021. We have also carried out many rounds of iterations. We have further optimized in terms of warehousing, logistics and distribution, and we will further optimize product selection or category.”

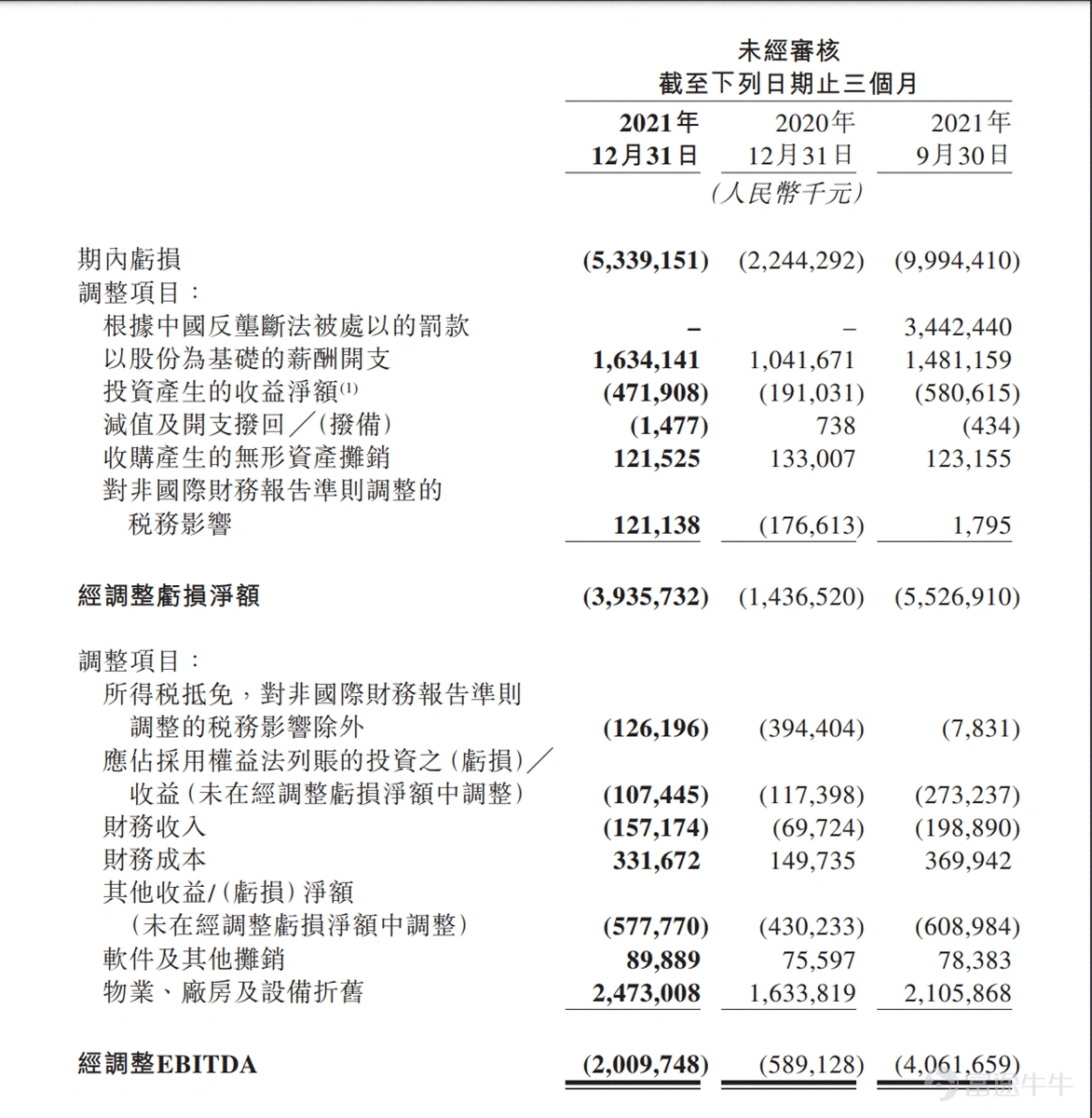

As a result, the loss margin of Meituan's new business this quarter was much better than expected by the market. Bloomberg unanimously anticipated a loss of 11.4 billion dollars from the new business, and an actual loss of 10.2 billion dollars. The operating margin narrowed from -79.47% in the third quarter to -69.55%. Although the amount of loss is still exaggerated, it has indeed achieved the lowest level after large-scale expansion of the community group buying business.

However, there is still a big gap between this profit margin and Pinduoduo. Judging from Pinduoduo's profit situation this quarter, the extent of losses in Duoduo Grocery Shopping has decreased a lot, and it is even possible to make a profit. Judging from the follow-up judgment, the gap between these two is mainly due to the following three reasons:

l Different procurement strategies. In Pinduoduo's procurement KPI, the price priority is the highest. Only the headquarters has the right to select suppliers; in Meituan's case, quality and price need to be considered together, and procurement itself has certain decision-making power. Therefore, the quality of Pinduoduo products will be slightly worse

l Pinduoduo's deep cultivation in the source area began very early, 1-2 years earlier than Meituan. Pinduoduo, which knows all about the country's agricultural products, has also begun to support agriculture through 10 billion agricultural research, so it uses greater control and price advantages for the upstream. Furthermore, the logistics system that Pinduoduo once established to sell agricultural products was reused at this time, while Meituan needed to start from scratch. Depreciation is also expected to be quite different between the two.

l At the logistics level, according to consumer reactions, Pinduoduo's delivery timeliness rate will be even lower. Meituan still guarantees delivery to the team leader before 11:00 on the same day as much as possible.

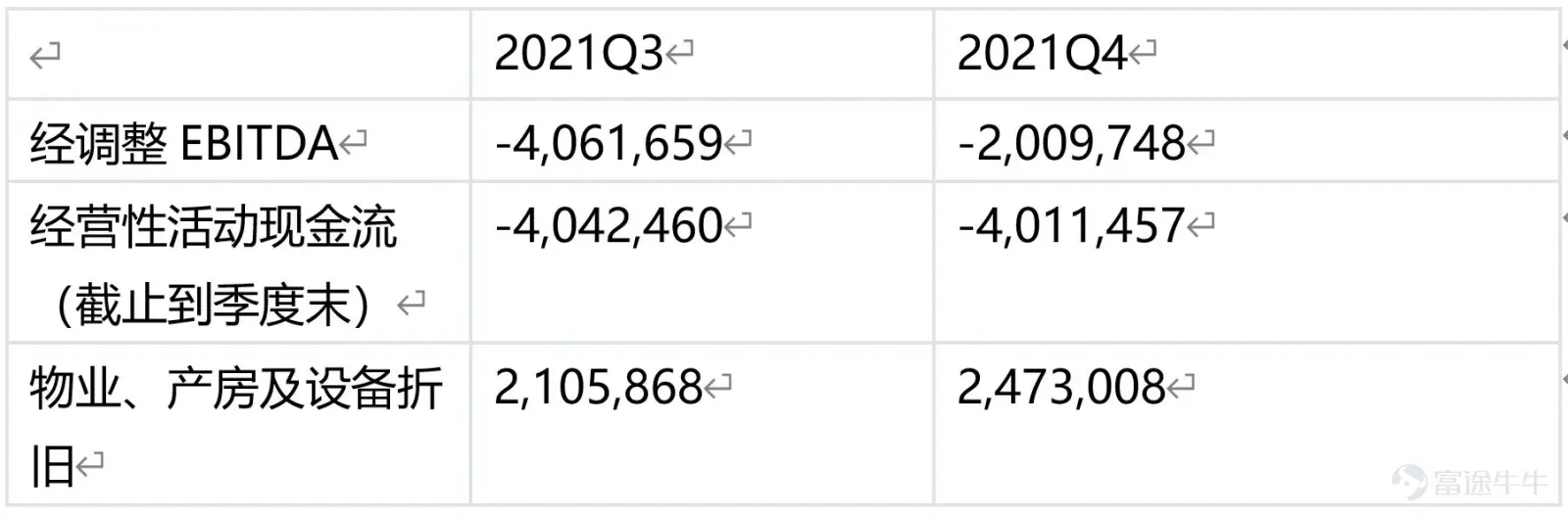

Therefore, Meituan Preferred is likely to be worse than Pinduoduo in terms of gross margin and operating profit margin. However, judging from the company's operating cash flow and EBITDA situation, there has indeed been a significant improvement in the economic efficiency of the units selected by Meituan in addition to the effects of depreciation.

Here we look at the month-on-month data, because in terms of month-on-month comparison, Meituan's preferred size is relatively close.

So, here's a summary of Meituan's Choice.There is probably no increase in the revenue level due to the decline in the pace of expansion this quarter, but since the business focused on reducing costs and increasing efficiency in this quarter, we have indeed seen relatively obvious results. At present, the expansion is over, and customer acquisition has also reached 690 million annual transaction users. Similar to Pinduoduo, the marginal benefits of further customer acquisition are not as good as doing a good job in service and expanding UE. Therefore, Meituan's strategy is correct, and it is expected that Meituan's preferred business will soon turn a loss into a profit.

Fifth, has Meituan reached the current configuration range?

Meituan has never been very profitable, so it is not suitable to use PE for valuation. From the perspective of PS valuation, PS is currently only 3.768, which is basically at the lowest historical valuation level, close to negative two times the standard deviation of the historical average.

Considering the highest valuation in history, the changes Meituan is facing are as follows:

l Policy pressure prohibits “choose one of two”, “nine must not” community group purchases, and social security issues for takeaways;

l The high growth rate of users declined, and the number of users reached a phased peak

l The increase in users' spending capacity has been suspended, and may even decline in the macroeconomic environment. This is mainly reflected in the lack of growth in GTV per average takeout

l The story of the rapid expansion of community group buying comes to an end

These changes all reflect that Meituan's revenue side growth will face a decline. This is indeed a problem faced by all internet companies. The end of borderless expansion means the end of burning money in exchange for growth. It turned into organic growth, qualitative revenue and profit growth.

After the Financial Services Commission's speech, we can determine that the policy base has basically emerged, and there is no possibility that the first policy risk we have summarized above will continue to worsen. Furthermore, the country's measures such as tax cuts and fee cuts are all activating the vitality of the market economy, so changes in Article 3 will show signs of improving from bottom to bottom in the near future, that is what we call the bottom of the market.

However, the increase in users and the rapid expansion of community group buying actually reflect the fact that Meituan's sinking logic has achieved phased results. Compared with the 2020Q3 (before community group buying was launched), 220 million new users were acquired, making it even more difficult to obtain users, and the cost performance ratio decreased.Therefore, over the next period of time, the guideline for Meituan's future growth based on user growth will decline. Instead, we should pay more attention to the average number of transactions per transaction user per year and the average GTV for takeout orders. In other words, Meituan will further meet the needs of consumers and further enhance consumers' stickiness by returning to its original heart and providing good services.

The epidemic will eventually end, and there seems to be no possibility of further tightening of regulations. Macroeconomic indicators such as the economy and per capita disposable income will definitely continue to grow. Meituan's moat has not been impacted by the epidemic but has been strengthened, and the competitive landscape has been optimized to varying degrees.

At this stage, it's still the same as Tencent$TENCENT (00700.HK)$ At the end of the review, Caijun wrote the same thing.

Therefore, there is no doubt that this stage is at the bottom of Meituan's valuation. The process of killing the valuation is over. What can be expected is that the 4 changes mentioned above, that is, the continuous easing of the 4 concerns, will lead to a real rebound.

At this stage, it's still the same as Tencent$TENCENT (00700.HK)$ At the end of the review, Caijun wrote the same thing.

Anyway, the winter is already so cold, can it be any colder?

No winter is insurmountable, and no spring will not arrive. This time, Meituan's commercial roots have not wavered. What we need to wait for is confidence and the implementation of regulations that are still unpredictable.

I believe that the state's regulation of the Internet is not to control the Internet. As an important competitive advantage in the data economy era, the Internet is still the foundation of people's digital lives. Antitrust clarifies boundaries. In the long run, it helps giants to calm down and focus on basic innovation, cultivate the real economy, empower the real economy, and achieve better integration between the virtual economy and the real economy.

$Tencent (TCEHY.US)$$Xiaomi Corp. (XIACF.US)$$XIAOMI-W (01810.HK)$$KUAISHOU-W (01024.HK)$$BABA-W (09988.HK)$$JD-SW (09618.HK)$$JD HEALTH (06618.HK)$$HSI Futures Current Contract (HSIcurrent.HK)$

$$E-mini S&P 500 Futures (SEP6) (ESmain.US)$$E-mini Dow Futures (SEP6) (YMmain.US)$$E-mini NASDAQ 100 Futures (SEP6) (NQmain.US)$

$$E-mini S&P 500 Futures (SEP6) (ESmain.US)$$E-mini Dow Futures (SEP6) (YMmain.US)$$E-mini NASDAQ 100 Futures (SEP6) (NQmain.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (34)

to post a comment

27

156