虧損收窄,美版“餓了麼”DASH漲超15%

DoorDash飆漲30%,但北美的外賣神話真的可以延續嗎?

01

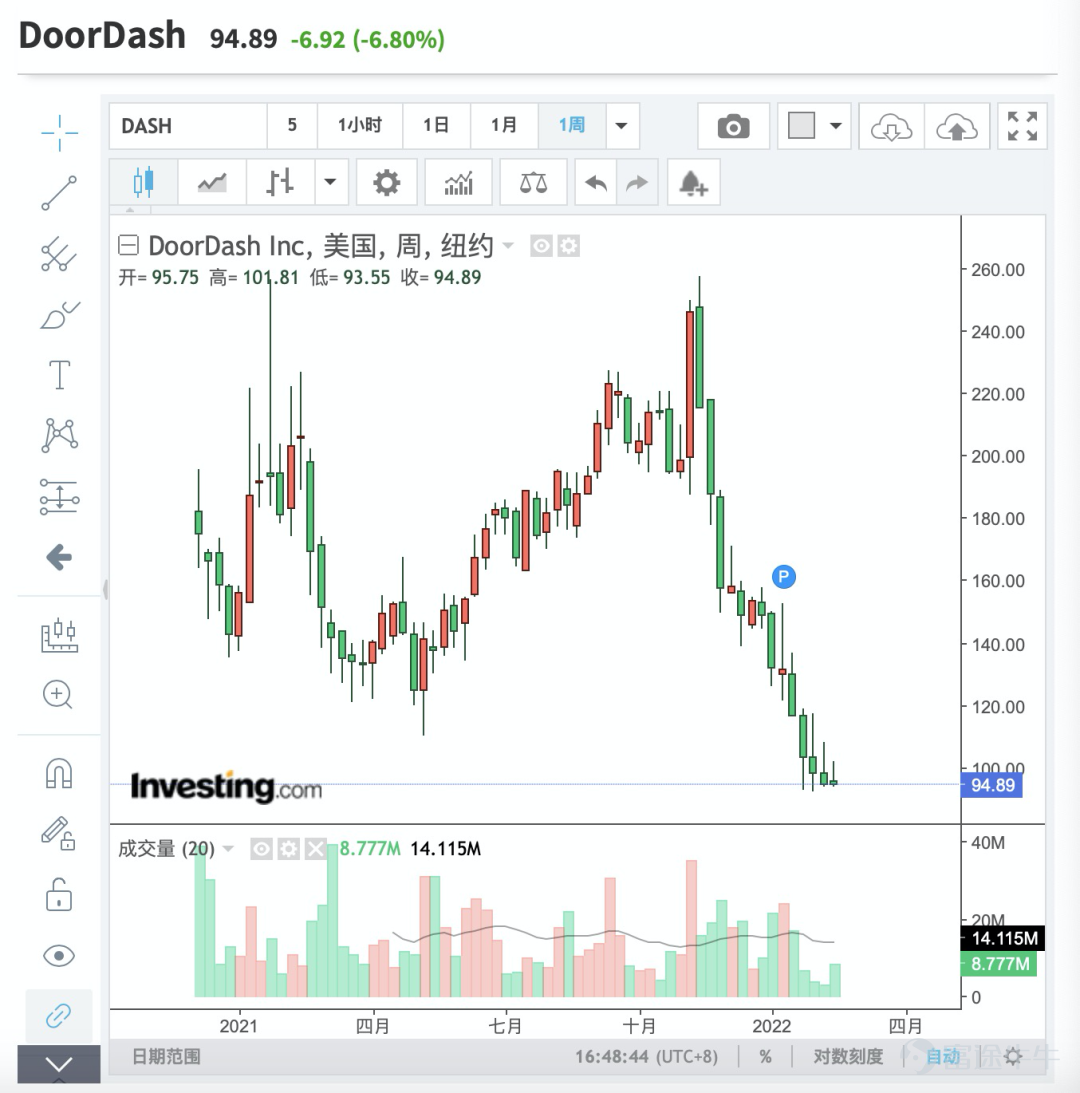

北美外賣服務巨頭DoorDash週三盤後公佈了強勁的四季度業績報告,隨後該股在盤後交易時段飆升超過27%,這是該股從去年11月的高點257美元/股跌至目前94美元水平後,難得的一次上漲。

北美外賣服務巨頭DoorDash週三盤後公佈了強勁的四季度業績報告,隨後該股在盤後交易時段飆升超過27%,這是該股從去年11月的高點257美元/股跌至目前94美元水平後,難得的一次上漲。

(DoorDash周線圖來自英爲財情Investing.com)

這家在疫情時期爆發式增長的外賣企業,此前可謂是華爾街炙手可熱的“疫情概念股”之一,2020年12月DoorDash在美股上市後,是當年美國最大的IPO之一,股價暴漲,市值一度超過500億美元。平台也一躍成爲了美國最大的外賣平台,市場份額達到50%以上。

但是,隨着歐美各國疫苗的普及推廣,經濟重新開放,人們開始重返餐廳。而此時,那些在疫情期間獲益匪淺的公司業績,也開始出現放緩。DoorDash就是值得擔心的疫情概念股之一。

根據英爲財情Investing.com的行情數據顯示,公司在去年11月抵達257美元的高位後開始極速下跌,直到跌破102美元的發行價,截至週三收盤,累計跌幅已經高達63%。

那麼,在一份超出市場預期並不是太多的業績過後,DoorDash的股價是否真的要翻身了?這27%的盤後漲幅究竟是“曇花一現”還是另一波暴漲的序幕?

我們不妨首先來看看這份業績:

第四季度,DoorDash第四季度營收13億美元,高於分析師預期的12.8億美元,同比增長34%;同時,每股虧損0.45美元,低於分析師預期每股虧損0.25美元;展望未來,DoorDash預計第一季度市場總訂單總額在114億美元至118億美元之間,分析師預期在114億美元至116億美元之間。

營收方面,公司的數據雖然超出市場預期,但是超出的並不多,這仍然是公司2020年12月上市以來的最慢增長。此前,公司的營收增長率在2021年第一季度是351%,隨後急劇下降到2021年二季度的242%,而到了三季度,增長率僅剩45%,而這個季度的34%就更低了。

另一方面,DoorDash仍然尚未盈利,淨虧損1.55億美元,與去年同期相比有所收窄,鑑於後疫情時代外賣行業的不確定性較大,且公司仍然面臨較大的同行競爭壓力,公司恐怕不會很快開始盈利。

在用戶方面,第四季度,市場總訂單總額(所有應用程序訂單和訂閱費用)爲112億美元,高於分析師預期的106億美元,同比增長36%;市場總訂單量3.69億份,同樣高於分析師預期,與去年同期相比增長35%。值得關注的是,公司四季度的月活人數超過2500萬人,同比增長22%,創歷史紀錄,2021年12月,來自非餐廳商家下單的月度活躍用戶人數在總人數中佔比上升到14%。

這是一份不算太差的成績單,但是這足夠了嗎?

我們在周初的文章中曾經提醒過該股的一些潛在風險,包括同行競爭,以及疫情紅利的結束等,而這些利空因素並沒有消失。

首先,和中國市場中美團(HK:3690)和餓了麼雙寡頭格局不同,美國的外賣市場競爭相對較爲激烈,雖然市場佔比超過50%,但DoorDash仍然面臨來自Uber Eats(NYSE:UBER)、Grubhub(NYSE:GRUB)、Postmates另外三家外賣巨頭的激烈競爭。

而且此第一非比第一,雖然美國的餐飲規模比中國更大,(2019年的數據是,中國餐飲規模爲4.67萬億,而美國餐飲規模6.03萬億。),但是,公司無論是在營收還是市值上,和美團都還有很大距離。

其次,即使是在疫情中,外賣平台開始被很多美國人認識和使用,但是美國本土的一些消費習慣和地域限制,還是導致了這些外賣巨頭事實上的擴張舉步維艱。一方面,美國大部分城市地廣人稀,人們的住宅分佈非常分散,這必然會降低單位時間送餐的效率,並且提高成本;而且,美國的人力成本較高,高人力成本使得美國外賣平台的配送費達到中國的3-5倍。

最後,美國的外賣平台也正面臨着更爲嚴格的監管和規範。其中,針對外賣平台的抽成問題,美國一些州都出臺了相應的第三方服務機構提供餐飲外賣的費用限價令。而針對外賣員,美國各州也有嚴格的規定,平台必須爲外賣員提供福利費等,以提高外賣員的福利,這導致平台的成本相應提高。

與此同時,聯邦貿易委員會(FTC)主席此前也收到了幾個州議員的函件,提出美國美食外送業界已經由三大巨頭把持,應調查美食外送產業整並的影響,認爲外送平台可能進行不公平商業行爲,包括收取“過高費用和佣金”。美國監管機關已留意到這些現象,並且已採取行動出臺新的法規以保護消費者權益。

總體而言,DoorDash在一份超預期的業績過後,路還很長,投資者需要做好判斷,謹防風險。

這家在疫情時期爆發式增長的外賣企業,此前可謂是華爾街炙手可熱的“疫情概念股”之一,2020年12月DoorDash在美股上市後,是當年美國最大的IPO之一,股價暴漲,市值一度超過500億美元。平台也一躍成爲了美國最大的外賣平台,市場份額達到50%以上。

但是,隨着歐美各國疫苗的普及推廣,經濟重新開放,人們開始重返餐廳。而此時,那些在疫情期間獲益匪淺的公司業績,也開始出現放緩。DoorDash就是值得擔心的疫情概念股之一。

根據英爲財情Investing.com的行情數據顯示,公司在去年11月抵達257美元的高位後開始極速下跌,直到跌破102美元的發行價,截至週三收盤,累計跌幅已經高達63%。

那麼,在一份超出市場預期並不是太多的業績過後,DoorDash的股價是否真的要翻身了?這27%的盤後漲幅究竟是“曇花一現”還是另一波暴漲的序幕?

02

我們不妨首先來看看這份業績:

第四季度,DoorDash第四季度營收13億美元,高於分析師預期的12.8億美元,同比增長34%;同時,每股虧損0.45美元,低於分析師預期每股虧損0.25美元;展望未來,DoorDash預計第一季度市場總訂單總額在114億美元至118億美元之間,分析師預期在114億美元至116億美元之間。

營收方面,公司的數據雖然超出市場預期,但是超出的並不多,這仍然是公司2020年12月上市以來的最慢增長。此前,公司的營收增長率在2021年第一季度是351%,隨後急劇下降到2021年二季度的242%,而到了三季度,增長率僅剩45%,而這個季度的34%就更低了。

另一方面,DoorDash仍然尚未盈利,淨虧損1.55億美元,與去年同期相比有所收窄,鑑於後疫情時代外賣行業的不確定性較大,且公司仍然面臨較大的同行競爭壓力,公司恐怕不會很快開始盈利。

在用戶方面,第四季度,市場總訂單總額(所有應用程序訂單和訂閱費用)爲112億美元,高於分析師預期的106億美元,同比增長36%;市場總訂單量3.69億份,同樣高於分析師預期,與去年同期相比增長35%。值得關注的是,公司四季度的月活人數超過2500萬人,同比增長22%,創歷史紀錄,2021年12月,來自非餐廳商家下單的月度活躍用戶人數在總人數中佔比上升到14%。

03

這是一份不算太差的成績單,但是這足夠了嗎?

我們在周初的文章中曾經提醒過該股的一些潛在風險,包括同行競爭,以及疫情紅利的結束等,而這些利空因素並沒有消失。

首先,和中國市場中美團(HK:3690)和餓了麼雙寡頭格局不同,美國的外賣市場競爭相對較爲激烈,雖然市場佔比超過50%,但DoorDash仍然面臨來自Uber Eats(NYSE:UBER)、Grubhub(NYSE:GRUB)、Postmates另外三家外賣巨頭的激烈競爭。

而且此第一非比第一,雖然美國的餐飲規模比中國更大,(2019年的數據是,中國餐飲規模爲4.67萬億,而美國餐飲規模6.03萬億。),但是,公司無論是在營收還是市值上,和美團都還有很大距離。

其次,即使是在疫情中,外賣平台開始被很多美國人認識和使用,但是美國本土的一些消費習慣和地域限制,還是導致了這些外賣巨頭事實上的擴張舉步維艱。一方面,美國大部分城市地廣人稀,人們的住宅分佈非常分散,這必然會降低單位時間送餐的效率,並且提高成本;而且,美國的人力成本較高,高人力成本使得美國外賣平台的配送費達到中國的3-5倍。

最後,美國的外賣平台也正面臨着更爲嚴格的監管和規範。其中,針對外賣平台的抽成問題,美國一些州都出臺了相應的第三方服務機構提供餐飲外賣的費用限價令。而針對外賣員,美國各州也有嚴格的規定,平台必須爲外賣員提供福利費等,以提高外賣員的福利,這導致平台的成本相應提高。

與此同時,聯邦貿易委員會(FTC)主席此前也收到了幾個州議員的函件,提出美國美食外送業界已經由三大巨頭把持,應調查美食外送產業整並的影響,認爲外送平台可能進行不公平商業行爲,包括收取“過高費用和佣金”。美國監管機關已留意到這些現象,並且已採取行動出臺新的法規以保護消費者權益。

總體而言,DoorDash在一份超預期的業績過後,路還很長,投資者需要做好判斷,謹防風險。

作者:李英維

免責聲明:本文內容及觀點僅供參考,不構成任何投資建議,投資有風險,入市需謹慎。

風險及免責聲明:以上內容僅代表作者個人觀點,不代表富途任何立場,亦不構成任何投資建議,富途對此不作任何保證與承諾。更多信息

評論(3)

發表評論

4

10