港股石油股多數高開,中石油漲超4%

The crude oil game is heating up: what investment opportunities are being nurtured?

Recently, the crude oil market has been particularly exciting. On Monday, US oil and oil both plummeted by more than 3%, and continued to fall on Tuesday, but soon reversed their sharp rise and recovered short-term downside. Currently, ICE oil has regained its position at $81, and NYMEX crude oil is approaching $79.

(NYMEX crude oil chart, source: Wind)

Behind the fierce battle over capital in the crude oil market, the game between the US and OPEC+ over oil prices is heating up.

01

US VS OPEC+

Last week, the US requested the release of oil reserves from many countries, and Russia immediately refused, South Korea clearly refused, and Japan made no clear statement. However, a lot has changed in the last 2 days. A number of major consumer countries have begun to release strategic oil reserves in response to US calls:

US White House:Sales of 18 million barrels of strategic petroleum reserve (SPR) crude oil approved by Congress will be accelerated; 32 million barrels of crude oil will be traded in the next few months, and 32 million barrels of crude oil will be added to the strategic petroleum reserve (SPR) within the next few years. The US is considering banning crude oil exports, and none of the options have been ruled out. US President Joe Biden continues to focus on other instruments related to oil prices.

India:5 million barrels of crude oil will be released from reserves.

UK:1.5 million barrels of oil will be released from reserves.

Japan:The government plans to release about 4.2 million barrels of oil from reserves, equivalent to the country's needs for 1-2 days. The tender will be held as soon as this year, and it will be completed by the end of March. The Japanese government will consider releasing further oil reserves if necessary. By the end of September, Japan has reserves that can meet about 240 days of demand, of which government reserves can meet 145 days of demand.

South Korea:It will participate with oil consumers such as Japan and India in the joint release of oil reserves proposed by the United States. The specific release scale, time, and method will be announced at a later date. It is expected that the scale of release will be on par with previous examples of international cooperation between South Korea and the International Energy Agency (IEA).

Saudi Arabia's reaction to this was quite intense. According to reports, if major consumers release crude oil from their reserves, or if the pandemic suppresses demand again, OPEC+ may adjust plans to increase oil production capacity. Meanwhile, in March of last year, Saudi Arabia teamed up with Russia to fight an oil price war, triggering a crude oil crisis and further triggering a crisis in the financial market.

Oil producers, led by Saudi Arabia vs. consumer countries led by the US, are in a tit-for-tat match, and the game is heated.

Taken together, this round of oil release reserves is roughly 70 million barrels, which is lower than market expectations, and has also faced fierce opposition from OPEC+.Currently, global oil consumption is close to 100 million barrels per day, and the amount of oil reserves released is less than a day's consumption; it cannot have a decisive impact on oil prices at all.This is an important logic for oil prices to rise instead.

02

A major inflection point in oil prices?

This year, crude oil significantly outperformed the performance of major financial assets. There are 3 main logics:

First, the global economy is recovering strongly, leading to a strong improvement in demand for crude oil; second, supply recovery is slower than demand growth; third, loose global currency liquidity has not changed.

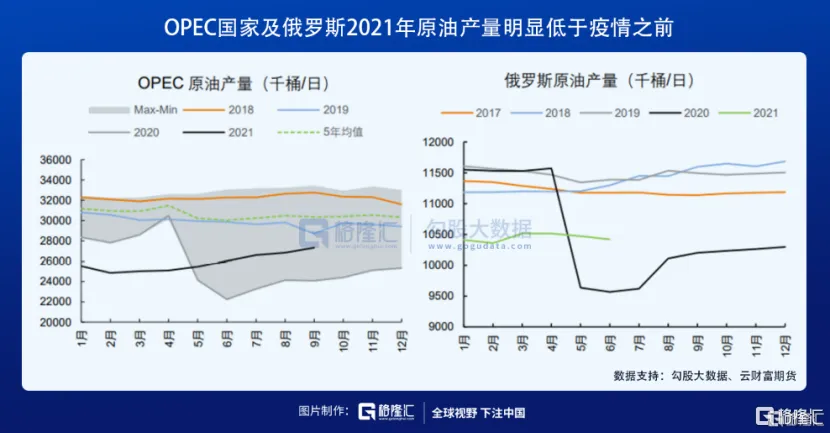

In April of last year, OPEC+ confirmed a production reduction agreement: production will be cut by 10 million b/d from May 1, 2020 for a period of two months; production will be reduced by 8 million b/d from July to December; and production will be cut by 6 million b/d from January 2021 to April 2022. In 2020, the total global crude oil supply was 94.45 million b/d, a year-on-year decrease of 6.53%. The sharp contraction in supply is one of the most important logics for pulling oil prices out of the quagmire.

In July of this year, OPEC+ launched a major meeting. It decided to extend the production reduction agreement, which was originally due to expire in April 2022, until the end of 2022, and increase crude oil production by 400,000 b/d each month starting in August this year until the production limit policy is finally completely lifted. At the September meeting, OPEC+ maintained the July resolution to increase production by 400,000 barrels despite huge pressure from the US.

Currently, there is still a large gap between crude oil production and demand (demand in 2020 was 92.91 million b/d, down 7.68% year on year), which is an important factor supporting the current high oil prices. Next, supply-side disruptions will be significant.

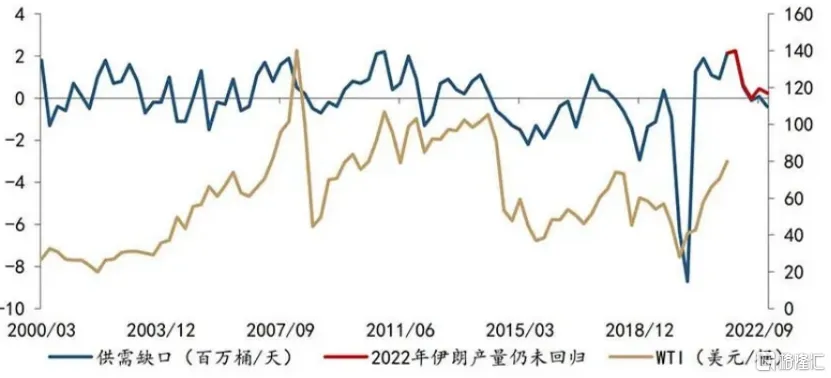

(Crude oil supply and demand gap and oil prices, source: Societe Generale Research)

If the US lifts economic sanctions against Iran or Venezuela under the pressure of high inflation, it will have a major impact on market expectations, and crude oil prices will also have some downward pressure. Iran previously said that as long as the US relaxes its economic restrictions, the country's crude oil production can easily increase to 6 million barrels per day in the short term. Also, once OPEC+ and the US side increase production drastically, it will change the current pattern of strong crude oil.

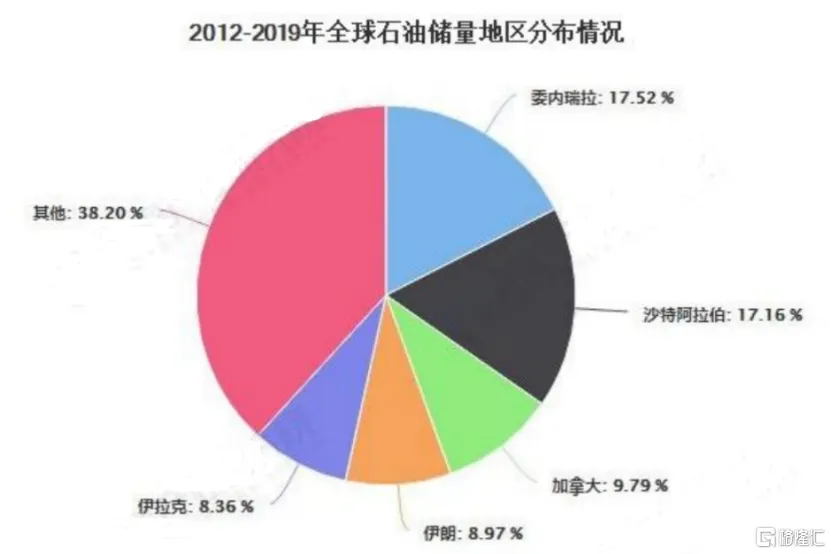

(Source: Forward-looking Research Institute)

It is worth noting that negotiations between the US and Iran will resume at the end of November.

2. Requirements

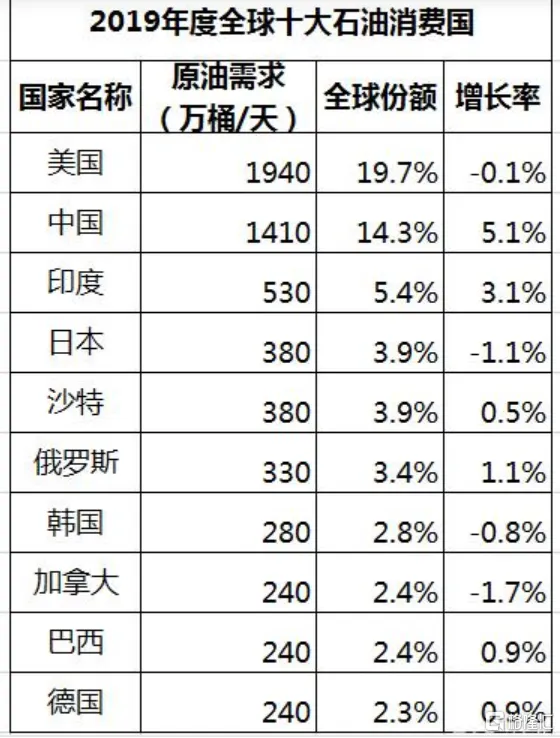

Prior to the pandemic, the top 3 global oil consumers in 2019 were the United States, China, and India, accounting for 19.7%, 14.3%, and 5.4% of the global share, respectively. It can be clearly seen that the US has a strong position in the world, but China's strong demand for oil is also growing by a large margin. The oil consumption of the US, China, and India accounts for 40% of the world's total oil consumption, which has a significant impact on the world's oil consumption pattern and market situation. Of course, Japan, South Korea, and the European Union, which includes Germany, are major oil consumers.

The demand side of global oil consumption mainly depends on the performance of the economies of China and the US, India, the European Union, Japan, and South Korea. Overall, next, oil demand is less optimistic.

Looking at China, from January to October, fixed asset investment increased 6.1% year on year, slightly lower than the expected value of 6.2%. Compared with the 7.3% growth rate in the previous September and the 8.9% growth rate in the previous 8 months, the decline was significant. Among them, real estate investment fell 5.4% year on year in October, and the new construction area fell by 33.14%. Infrastructure investment fell 4.8% year on year in October. In terms of consumption, the year-on-year increase in October was 4.9%, higher than the expected value of 3.5%, and picked up for two consecutive months. Overall, however, the downward pressure on the economy is strong.

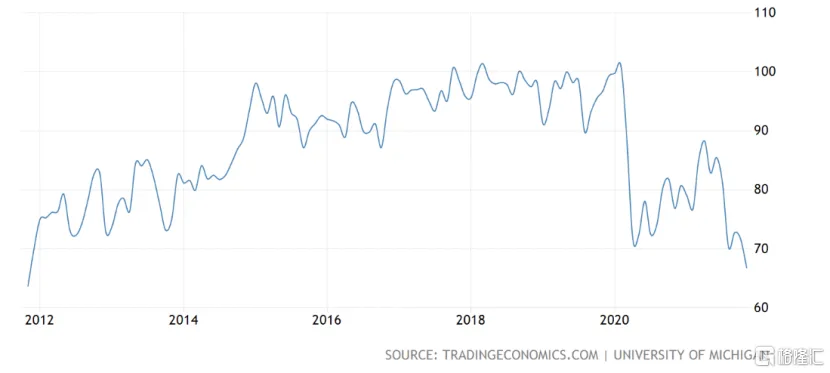

On the US side, the consumer confidence index continued to fall from 71.7 in October to 66.8, far below market expectations of 72.4, and hit a new low in nearly 10 years. The impact of inflation on consumers' daily expenses is likely to be greater than the Federal Reserve and market consensus can imagine.

(US Consumer Confidence Index, Source: Economic Net)

The US CPI soared to 6.2% in October, hitting a 31-year high, and the risk of the economy “stagnating” is increasing. With the exception of China and the US, India, Japan, South Korea, and the European Union, the current economy has not recovered to what it was before the pandemic, but the downward pressure is increasing.

In addition to this, the global economy is currently facing a resurgence of the COVID-19 pandemic. Among them, Europe and Austria announced the fourth round of “city closures”. Germany, which is the locomotive of the European economy, has recently seen a daily increase of more than 60,000 cases, a record high. Meanwhile, in the US, the number of new cases in a single day recently once again surpassed 100,000, returning to the peak level of COVID-19 in the summer of August.

Vaccination rates in Europe and the US are already at a high level, but they have not contained the epidemic; instead, they are developing in an increasingly serious direction. If it continues, it will be a major blow to the extremely fragile economic recovery.

3. Currency

In March of last year, the Federal Reserve released a base currency of 4 trillion US dollars in one go, superimposed currency multipliers, and tens of trillions of dollars poured into the financial market and the real economy, thus creating a huge bubble in the financial market and economic recovery. At the same time, super-large water discharge is also an important factor in the overall sharp rise in inflation.

In October, the US inflation rate broke through 6.2%, and the Eurozone surpassed 4.1% (Germany's CPI may be close to 6% in November). The former hit a 31-year high, while the latter hit a 13-year high, all far above the target level of 2%.

(US currency chart, source: Economic Net)

Under high inflationary pressure, major central banks have taken action. The Federal Reserve clearly initiated the Taper process at the November interest rate meeting.

Recently, two former chairmen of the Federal Reserve said that the reduction in debt purchases may increase. Instead of the current 15 billion US dollars per month, it will probably be 30 billion US dollars, which has completely doubled. Meanwhile, the Federal Reserve may have to raise interest rates to 3%, or even higher. Former New York Federal Reserve Chairman Dudley believes that the peak rate hike will be far higher than the 1.75% expected by the US Treasury bond market, and may reach 3% to 4%. They are not ordinary people, but the former chairman of the New York Federal Reserve. They represent a decisive voice within the financial market. The meaning of the briefing is quite obvious.

Currently, the US dollar index has soared sharply to 96.6, a new high since July last year. The 10-year US Treasury yield soared rapidly, approaching a high of 1.7%. Furthermore, yields on 1-year, 2-year, and 3-year treasury bonds all reached new highs during the year, and yields on January and March-6 treasury bonds were inverted.

There are various signs that the market is worried about inflation getting out of control, and it is expected that the Federal Reserve will raise interest rates early.As can be seen from the above analysis, there are clear signs of a shift at both the demand and monetary levels, and there is still a gap on the supply side. The three combined efforts have led to the current overall oil price at an absolute high level, but the major inflection point may have already appeared around October 25.

03

Epilogue

Over time, oil prices peaking and falling are basically a no-brainer, because the combination of weak demand and currency shifts will gradually exceed the logic of the supply gap. On the supply side, measures taken by the US to suppress oil prices due to high inflation, or negotiations between the US and Iran will all cause disturbances and are positive.

After the general direction has been determined, it is currently risky to go long on crude oil commodities. Perhaps the wiser approach is to open short positions in batches.Specifically, when it comes to the stock market, if you take the opportunity to sell securities, the chances of winning will be greater, especially in the first half of next year. However, at present, oil prices are fluctuating very drastically. The wind is high and the waves are raging, so act with caution.

$PetroChina (601857.SH)$$PETROCHINA (00857.HK)$

$PetroChina (601857.SH)$$PETROCHINA (00857.HK)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

11

25