UberQ2財報後跌超7%,你如何解讀?

Uber's EBITDA loss in the second quarter, after adjustments, exceeded expectations, falling 7% post-market to a nine-month low | Financial Report Watch

After the post-market trading on Wednesday, August 4th, the American online car-hailing giant uber technologies$Uber Technologies (UBER.US)$ (uber) released its financial report for the second quarter of the 2021 fiscal year ending on June 30.

Despite the total revenue and net income for the quarter being better than market expectations, the profit core indicator that the company values—adjusted EBITDA, still showed a loss, and the loss was higher than expected., post-market trading saw a 7% drop in uber’s stock price, which briefly fell below $39, potentially hitting the lowest point in several months since November last year. Yesterday's financial report mentioned that Lyft, the competitor that had its first quarterly profit in the second quarter, also fell by 1%.

Uber fell the most on Wednesday, dropping more than 3% and closing down more than 2% at $41.81, a year-to-date decline of 18%, underperforming the S&P 500 index by more than 17%, and down nearly 35% from its all-time high of $64.05 on February 10, deeply mired in a technical bear market.

However, Uber surged 71.5% last year, significantly outperforming the S&P with a 16.3% gain, with a total ROI of nearly 44% over the past year, also higher than the S&P's total ROI of 35.4%. Its stock price has been declining continuously since May, as the market is concerned that recruiting gig drivers post-pandemic may impact profits. It is reported that major shareholder SoftBank of Japan is considering reducing its Uber stake by a third, which is also unfavorable for the latter's share price.

Nevertheless, prior to the financial report release, Wall Street was quite optimistic about Uber's future performance. Out of 37 analysts surveyed by FactSet, 32 gave a rating of "buy", only 2 rated it as "sell", with an average target price of $69.53, indicating a potential increase of 66%.

Revenue ended four consecutive declines, achieving unexpected net income from "stock trading", reaffirming EBITDA adjustments by year-end.Profitable

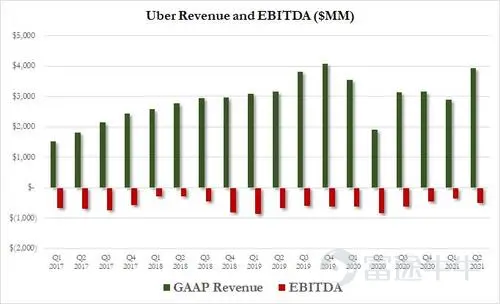

The financial report shows that in the second quarter of this year, Uber's total revenue was $3.93 billion, higher than the market's expected $3.75 billion, with a 35% increase QoQ, 105% YoY, and 95% YoY growth calculated at a fixed exchange rate, almost doubling from the same period last year.

This means Uber's total revenue has returned to the level of the second quarter of 2019 (pre-pandemic).also since2020For the first time since the first quarter of the fiscal year, there was a year-on-year increase, ending the continuous four-quarter year-on-year decline trend that began in the second quarter of last year.Accompanied by a rebound in the core online car-hailing business from the low point of the epidemic.

Net income for the quarter was $1.1 billion, benefiting from unrealized gains from equity investments in Didi and autonomous driving startup Aurora totaling $1.871 billion. This resulted in an unexpectedly high EPS of 58 cents, compared to market expectations of a loss of 51 cents per share.

However, adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) still showed a loss of $0.509 billion, an increase of $0.15 billion from the first quarter, exceeding market expectations of a $0.325 billion loss. Nevertheless, the loss narrowed by $0.328 billion compared to the second quarter of last year, a 40% reduction, marking the first time since the company's establishment that adjusted EBITDA is profitable. The operating loss in the second quarter was $1.19 billion.

Chief Financial Officer Nelson Chai reiterated the milestone of achieving a turnaround in adjusted EBITDA from loss to profit in the fourth quarter of this year, expecting the third-quarter adjusted EBITDA loss to improve to less than $0.1 billion, with a record high total booking volume of $22 billion to $24 billion.

CEO Dara Khosrowshahi stated that in the second quarter they 'invested in drivers to invest in recovery' and made significant progress. The number of active drivers and couriers in the USA increased by nearly 0.42 million from February to July, with a 75% increase in driver numbers in the second quarter. 90% of idle drivers plan to return to work in September, with nearly half of the total booking volume generated by consumers using mobile travel and delivery services.

Revenue from food delivery and the total order volume continue to exceed that of the core online car-hailing service, with an overall record high total order volume.

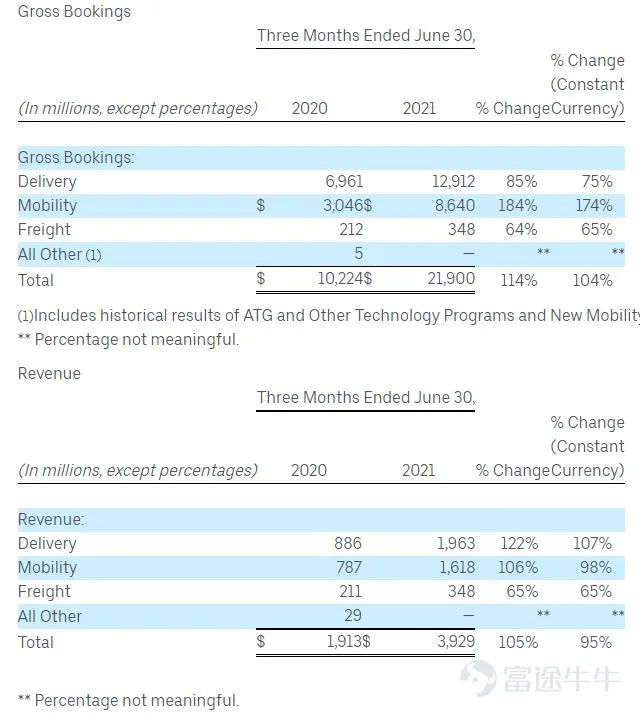

In its financial report, Uber divides its main business into three parts: mobile transportation mainly based on online car-hailing (Mobility), food delivery and distribution (Delivery), and freight (Freight).

In the second quarter of this year, revenue from food delivery and distribution once again exceeded that of the mobile transportation business, continuing the trend since the outbreak of the epidemic.Among them, revenue from food delivery and distribution reached $1.96 billion in the second quarter, an increase of 13% month-on-month and a doubling year-on-year (up 122%); revenue from mobile transportation was $1.62 billion, excluding the historical accrual of contingent liabilities for reclassifying gig drivers as employees in the first quarter of the UK, with a month-on-month increase of 11% and a year-on-year increase of 98%.

Analysts say that shared transportation was Uber's main source of revenue and core business until the epidemic last year, while the food delivery service launched in 2016 after a trial in 2014 is becoming the future growth engine. In the third quarter of last year, Uber's food delivery revenue exceeded that of the core taxi business for two consecutive quarters, and during the epidemic, the growth of the food delivery business offset the sharp decline in taxi business.

In the market, more attention is paid to indicators closely related to revenue—total order volume (Gross Bookings).)In terms of Uber,In the second quarter, Uber's total order volume reached 219.Historic high of 1 billion US dollars, doubling year-on-year (114% increase), exceeding expectations by 1 billion US dollars. Among them, the total order value for mobile travel was 8.6 billion US dollars, an increase of 184% year-on-year; while the total order value for takeaway and delivery was 12.9 billion US dollars, an increase of 85% year-on-year.

In terms of profit indicators, the adjusted EBITDA for the mobile travel division was a profit of 0.179 billion US dollars, a decrease of 0.119 billion US dollars from the previous period, but an increase of 0.129 billion US dollars year-on-year; the adjusted EBITDA for the takeaway and delivery division was a loss of 0.161 billion US dollars, narrowing losses by 31% compared to the same period last year, and also narrowing losses by 39 million US dollars compared to the same loss indicators in the first quarter of this year.

In addition, the revenue from the freight business was 0.348 billion US dollars, an increase of 65%, and at this trend's annualized revenue run rate will reach 1.4 billion US dollars; the adjusted EBITDA was a loss of 41 million US dollars, narrowing losses by 16% compared to the same period last year.

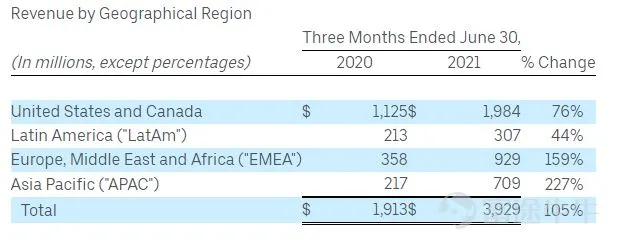

The company emphasized that the total order value of the takeaway and delivery business achieved triple-digit strong growth year-on-year in Europe, the Middle East, and Africa markets, and also achieved a considerable double-digit percentage increase in North America, Latin America, and the Asia-Pacific region. The total order value of the mobile travel business in the initial Asia-Pacific region all achieved at least 10% growth month-on-month, but due to the severe outbreak of the Indian epidemic dragging down the Asia-Pacific order value by 9% month-on-month.

Previously, the market was concerned that Uber would have to increase incentives for recruiting drivers in the post-epidemic era to cope with the situation of supply exceeding demand, which would harm profits. This financial report confirms the negative impact of these efforts, namely a 280 basis point month-on-month decrease and a sharp 710 basis point year-on-year decrease in the revenue-to-total order amount ratio (realization rate, Take Rate) of the mobile travel division to 18.7%, the company attributed this to 'increased investment in the area of restoring available drivers, especially in the US market'.

In other user metrics, Uber did not provide the exact number of employed drivers, but stated that its drivers and couriers had a total revenue of 7.9 billion US dollars in the second quarter, an increase of 144% year-on-year, exceeding the 114% year-on-year increase in total order value. The company achieved 1.51 billion trips on the platform, a 4% increase month-on-month and a 105% increase year-on-year, with both mobile travel and delivery travel experiencing month-on-month growth. Monthly active platform consumers (MAPC) reached 0.101 billion, a 3% increase month-on-month and an 84% year-on-year increase, with an average monthly spending per MAPC of 72 US dollars, showing increases both year-on-year and month-on-month.

Diversification strategies are favored by Wall Street, focusing on UberWhen will the company turn losses into profits and maintain high growth in the delivery business.

Investors will particularly focus on the changes in Uber's online car-hailing business total booking volume, which is a key indicator of revenue for the mobile travel sector. Previously, it suffered severe blows during the epidemic period due to a sharp drop in ride-hailing demand and many businesses/companies being forced to close.

The market is also concerned about the overall performance of Uber's diversified businesses such as mobile travel, delivery, freight, and others.After continuously losing billions of dollars since its founding, some key business indicators have now shown signs of turning losses into profits.

Brokerage analyst John Blackledge pointed out that Uber's core online car-hailing platform has achieved profitability based on each trip, and the company is expected to gain and maintain market share in several rapidly growing regions globally and adjacent spaces. The company's plan to acquire the logistics technology company Transplace for $2.25 billion will help accelerate the complete turnaround of the freight business in the fourth quarter of next year.

Uber CEO Dara Khosrowshahi reiterated in May during the first-quarter earnings release that it still expects to achieve positive quarterly EBITDA (earnings before interest, taxes, depreciation, and amortization) this year, a message welcomed by the capital markets.

However, the company also warned that it will spend $0.25 billion on driver incentive programs as the recovery rate of passenger demand has exceeded the ability to recruit new drivers in the United States with the easing of the COVID-19 pandemic, and the demand for deliveries continues to outpace supply, squeezing the company's profit margin.

Some analysts believe that the post-pandemic shortage of contract workers is expected to continue into the third quarter of this year, posing a threat to the recovery of gig economy leaders like Uber and Lyft. Both companies urgently need to find long-term solutions. Uber's North American driver operations manager, Carrol Chang, also acknowledged this as a matter worthy of 'deep introspection and reflection,' bringing significant uncertainty to the online car-hailing business model.

In addition to demonstrating the ability to overcome labor shortages without significantly increasing costs, Uberalso needs to maintain the high-speed growth of its food delivery and delivery business,which significantly offset the weakness of its core online car-hailing business during the epidemic.

In addition to the acquisition of Transplace mentioned above, Uber has recently also formed partnerships with the largest chain membership warehouse store Costco, the largest food and pharmaceutical retailer Albertsons Companies in the US, and floral company FTD, increasing its delivery business in daily groceries and more pre-packaged food and pharmaceuticals.

Compared to its competitor Lyft, which focuses on mobile travel,Uber's "multi-leg" approach is clearly favored by Wall Street.Brokerage Gordon Haskett analyst Robert Mollins believes that Uber's target price for the next 12 months is $65, which would set a new historical high, as its business flourishes across the board and continues to deepen into consumers' daily lives, increasing market share in online car-hailing and delivery, which is beneficial for enhancing revenue and profitability in the coming years.

Gordon Haskett brokerage analyst Robert Mollins believes that Uber's target price in the next 12 months is $65, which can set a new all-time high. The reason is that its business is in full bloom and deeply integrated into consumers' daily lives, increasing market share in online car-hailing and delivery services, which will enhance revenue and profitability in the coming years.

In the short term, Uber's mobile travel business has caught the economic reopening trend, while its food delivery and grocery delivery business can withstand the long-term coexistence with the epidemic. The value of its freight business is also underestimated, and the company is expected to become a leader in the freight brokerage industry. As a "super one-stop app", Uber will outperform Lyft, which focuses on the taxi business.

Regarding the regulatory risks of whether online car-hailing drivers should be classified as "temporary contract workers" or employees, analysts acknowledge the increasing regulatory pressure on the online car-hailing industry globally, while also believing that the policies in some states of the USA favor Uber. Previously, more and more countries are requiring gig workers to be considered as employees, and some work benefits enjoyed by employees may erode company profits.

Nomura Securities analyst James Lee stated that unlike the UK's ruling in March this year to classify Uber drivers as company employees, key states such as New York and Massachusetts in the USA are negotiating gig labor laws based on Proposition 22 in California. The latter was a voter initiative passed in California last year, allowing gig workers for companies like Uber to be treated as independent contractors rather than employees.

Feel free to like and share, and also welcome everyone to discuss in the comments section below the post~

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

2

5