Chip stocks lead as China's AI industry chain faces a revaluation rally?

Zhipu AI (02513.HK): The world's first large AI model stock—what has already been priced into its RMB 800 billion market cap?

First published on AceCamp’s official website on July 8—get the freshest insights faster!

(This article constitutes analytical discussion on the AI large-model industry and related companies; financial data and market information verified via Wind, as of July 8, 2026. "Market cap potential" represents scenario-based estimates and does not constitute investment advice, nor does it forecast stock prices or target prices. Please assume all risks yourself.)

I. Market Supply and Demand and Competitive Landscape: From the 'Hundred-Model War' to 'Consolidation Among Leaders'

On the supply side, consolidation is underway. China's large-model players broadly fall into four categories: internet giants (Alibaba’s Tongyi, ByteDance’s Doubao, Tencent’s HunYuan, Baidu’s Wenxin), independent model companies (Zhipu AI, MiniMax, Moonshot AI, StepFun, DeepSeek, etc.), vertical-industry-specific models, and open-source ecosystems. After two years of market shakeout, resources are concentrating among leading players. Zhipu AI positions itself as an independent general-purpose large-model company + MaaS (Model-as-a-Service) platform + on-premise deployment provider. Backed by Tsinghua University’s technical heritage, it ranks among the top Chinese large-model firms in both technological capability and commercialization.

On the demand side, focus is shifting from consumer-facing chat applications to enterprise adoption. Revenue for large models is moving away from 'consumer chat' toward on-premise deployments for government and enterprises, cloud-based API calls, and use cases like intelligent agents, office productivity tools, and code generation. Zhipu AI’s revenue structure confirms this trend: RMB 724 million in 2025 revenue (up 131.9% YoY), comprising RMB 534 million (73.7%) from on-premise deployments and RMB 190 million (up 292.7% YoY, 26.3% share) from cloud deployments. In short—the current core business is B2B private deployments, while growth optionality lies in cloud/API services.

Competitive landscape: strengths and weaknesses are both pronounced. According to Frost & Sullivan and prospectus data, by 2024 revenue, Zhipu AI ranked first among China’s independent general-purpose large-model developers, second among all general-purpose large-model developers, with a market share of approximately 6.6%. Its advantages include its Tsinghua-rooted technology, strong government and enterprise client base, on-premise deployment capabilities, and the open/open-source GLM ecosystem. However, its shortcomings are equally clear—significant losses, margin pressure, and a business model still under validation. Moreover, formidable competitors surround it: internet giants possess advantages in traffic, cloud infrastructure, and capital; DeepSeek exerts pressure through open-source efficiency; and rivals like MiniMax and Moonshot AI are rapidly catching up via capital markets.

II. New Catalysts: Scarce Listed Asset + Model Iteration + Improved Commercialization Structure

First, capital market access and scarcity. Zhipu AI is Hong Kong’s ‘first pure-play large-model stock’ globally and is advancing IPO counseling and fundraising expectations for the STAR Market. Being a ‘scarce listed pure-play large-model asset’ itself acts as a valuation catalyst—investors lack direct exposure to a ‘Chinese OpenAI,’ creating scarcity-driven premium. However, this also implies heightened volatility around lock-up expirations, liquidity, and valuation.

Second, new model launches as catalysts. Public reports indicate that new versions of the GLM series (e.g., full public release, 1M-token context length, API launch/open-sourcing) have repeatedly fueled market expectations for technological advancement and increased API usage. **It’s important to be objective: these reflect expectations of future growth, not yet realized revenue.**

Third, the commercialization structure is improving. Cloud deployment revenue grew 292.7% YoY in 2025. If API calls, agent-based services, and industry cloud offerings continue to gain traction, gross margins and revenue scalability should improve. However, on-premise deployments still account for 70% of revenue and remain heavily project-driven, meaning the company is still far from achieving a ‘light-asset, high-margin SaaS’ model.

III. Valuation and ‘Market Cap Upside’: Two Research-Oriented Approaches

(Note: The following represents research-oriented valuation methodologies; comparable market caps reflect objective facts, while ‘market cap upside’ refers to scenario-based estimates under specific assumptions. Neither constitutes a target price nor a forecast.)

First, assess how forward-looking the current valuation is. According to Wind (as of July 8, 2026), Zhipu AI (HKEX: 2513) has a market capitalization of approximatelyHK$813.7 billion、Negative P/E ratio; using a rough estimate of approximately RMB 724 million in revenue for 2025,the static price-to-sales (PS) ratio is already in the thousands(even based on the previously reported market capitalization of approximately HK$495.8 billion, the static PS ratio would still be around 576x). The conclusion is clear: **Zhipu cannot be valued based on profit, and even traditional PS ratios have lost their relevance; the valuation can only be understood through the lens of "long-term revenue plus platform monetization scenarios."

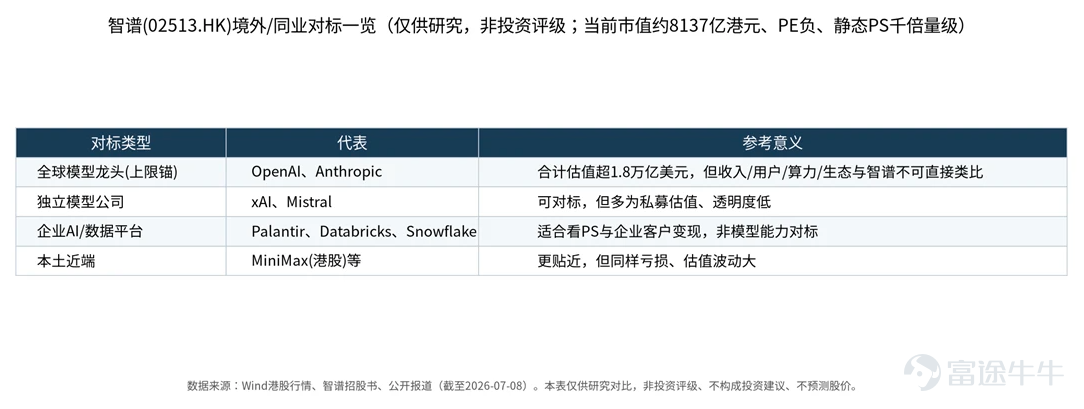

Method 1: Benchmark against overseas peers.

Assessment: Zhipu is not currently undergoing a "low-valuation recovery," but rather represents a "scarce large-model asset receiving an extremely high option-like valuation"; this valuation must be gradually validated through revenue scale expansion, increased cloud API contribution, and narrowing losses.

Method 2: Backward calculation from "market size × market share" (scenario-based projection). Three scenarios are outlined below (no target price provided):

– • Conservative: Future revenue of RMB 5 billion, with a high-growth AI platform PS ratio of 20–30x → implied market cap of approximately RMB 100–150 billion;

– • Base case: Future revenue of RMB 10 billion, PS ratio of 30–50x → implied market cap of approximately RMB 300–500 billion;

– • Bull case: Future revenue of RMB 20 billion, price-to-sales (PS) ratio of 40–60x → implied market cap of approximately RMB 800–1,200 billion.

Key reminder: Zhipu AI currently has a market cap of approximately HK$813.7 billion, already approaching the midpoint of the 'bull-case' scenario. This implies that the market is already pricing in its potential to become a 'leading Chinese large-model platform,' rather than just a company generating RMB 700 million in revenue. Whether further upside remains hinges on its ability to convert expectations into actual revenue and gross profit; otherwise, the current extremely high valuation inherently carries significant downside risk.

Risk Disclosures and Notes

① Still deeply unprofitable: According to the prospectus, net losses were approximately -RMB 1.44 billion, -RMB 7.88 billion, -RMB 29.58 billion, and -RMB 23.58 billion for 2022, 2023, 2024, and H1 2025, respectively, with high R&D spending and an unclear path to profitability. ② High proportion of on-premise deployments and heavy reliance on project-based/implementation-based revenue models mean its valuation cannot be fully benchmarked against asset-light SaaS companies. ③ Intense competition from big tech firms and open-source models could trigger price wars or API price cuts, compressing gross margins. ④ Hong Kong-listed shares exhibit extreme volatility (previously surged close to HK$1 trillion before a notable pullback); the 'market cap upside' presented here is a research-based scenario analysis, not a definitive conclusion. ⑤ All companies and estimates referenced herein are for research purposes only and do not constitute investment advice or predictions about future stock prices.

Disclaimer: This document constitutes research-oriented discussion on the AI large-model industry and related companies. All facts cited are derived from public reports, company prospectuses/annual reports, and Wind data (as of July 8, 2026). The 'market cap upside' scenarios are based on publicly available assumptions and are strictly for illustrative purposes—they do not constitute investment recommendations or trading advice, nor do they forecast any company's future stock price or market capitalization. Past performance and current conditions are not indicative of future results. Data sources: Wind HK equity data, Zhipu AI prospectus/2025 annual report, Frost & Sullivan, and public reports from 21st Century Business Herald, Caixin, and 36Kr.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

2