What’s Happening in the Memory Sector? A Breakdown of the Three-Way Tug-of-War Behind the Recent Decline and Key July Milestones

Within just two days, the AI industry has released two major signals: Meta plans to lease out its idle AI computing capacity, while Anthropic is proactively seeking collaboration with Samsung to co-develop AI chips.

On the surface, these moves by the two tech giants appear unrelated, but they point to the same underlying trend—the past two years of unrestrained, cost-agnostic 'arms race' in computing power is approaching an inflection point. Leading companies are now quietly shifting strategic focus, prioritizingreturn on investment (ROI)over sheer scale of capital expenditure.

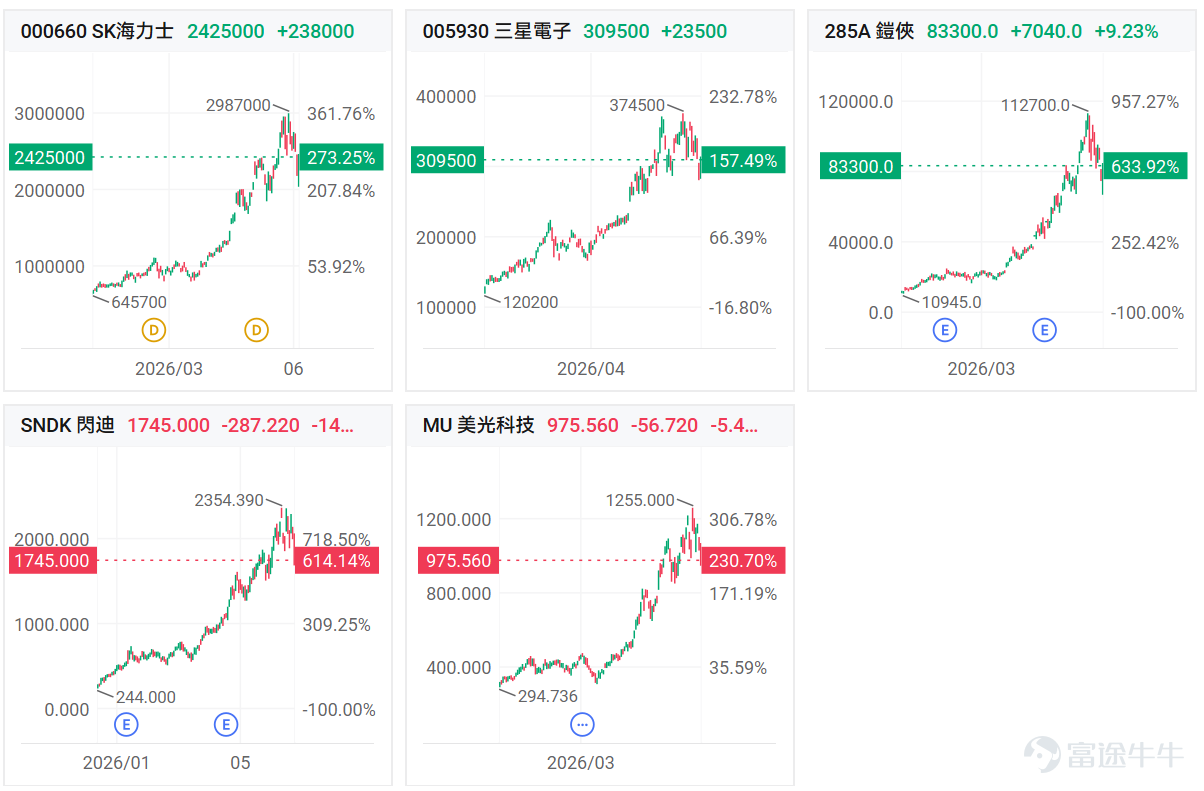

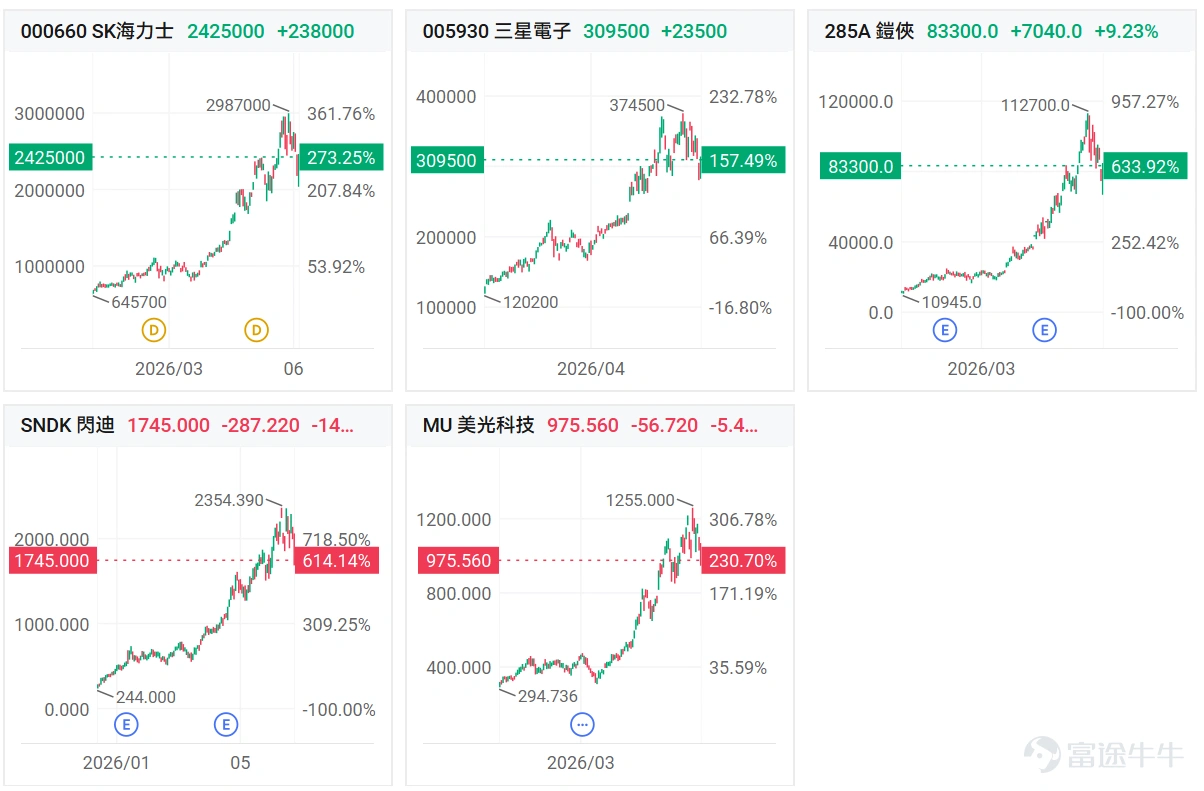

Meanwhile, capital markets have responded swiftly. Recently, the AI hardware sector has seen a broad pullback, particularly weighing heavily on $Micron Technology (MU.US)$ 、 $Samsung Electronics (005930.KR)$ 、 $SK hynix (SKHY.US)$as well as$SanDisk (SNDK.US)$、 $Kioxia Holdings (285A.JP)$ leading memory chipmakers.

However, this does not mean the 'memory industry upcycle has been disproven'; rather, it is the result of three converging market forces:namely, still-strong industry fundamentals, macro liquidity driving sector rotation, and short-term supply-side pressure on individual stock holdings at the micro level.

Industry Signal: Sellers’ Pricing Power Continues to Strengthen

From a fundamental industry perspective, sellers’ pricing power in the memory sector has not weakened—in fact, it continues to strengthen. Two recent developments are particularly telling:

The first signal is that Samsung is still raising prices.According to ZDNet, citing industry sources in Korea,Samsung Electronics is currently negotiating with customers over the average selling price (ASP) of standard DRAM for the third quarter, aiming for a price increase of up to 20% compared to the previous quarter.The company also plans to raise prices for low-power DRAM (LPDDR)—used in both servers and mobile devices, where both segments face bottlenecks—by more than 20%, underscoring its firm stance in pricing negotiations.

Supply shortages persist. Continued investment by global tech giants in AI infrastructure has driven strong demand for server DRAM, high-bandwidth memory (HBM), and LPDDR, making it unlikely that the tight supply situation will ease in the near term. Industry insiders note thatalthough the pace of future price increases may moderate, memory makers like Samsung Electronics are expected to sustain high profitability into next year.

This indicates a key shift: while the pace of price increases may be moderating, the pricing cycle is far from over. Over the past few quarters, memory prices have already undergone a sharp recovery. The subsequent quarter-over-quarter price hikes—falling from 50%–60% to 15%–20%—do not signal a reversal in market conditions, but rather a transition from extreme price surges to sustained high levels.

The second signal is that SK Hynix now has stronger long-term contract terms.

According to the latest report from Digitimes, SK Hynix has recently signed long-term supply agreements (LTAs) with customers using a no-price-cap model, clearly distinguishing itself from competitors like Micron, which typically include 'price caps' in their contracts.This arrangement makes SK Hynix the only memory supplier in the current market not bound by price ceilings.

This development is more significant than price hikes alone.While price increases reflect current supply-demand tightness, LTAs without price caps indicate that customers are no longer merely accepting 'high prices'—they are now accepting the risk of 'further price increases in the future.' In other words, customers are now more worried about securing supply than about high prices.

This marks the biggest difference between the current memory cycle and previous ones. Historically, memory was a classic cyclical product, where customers sought to lock in prices through long-term agreements and suppliers used such agreements to smooth out volatility. Now, however, AI-driven demand has reshaped the pricing structure: for cloud providers, server makers, and AI infrastructure clients, guaranteed supply has become more important than short-term pricing.

TrendForce previously noted that Samsung and SK Hynix are strengthening their long-term supply agreements, with customers willing to pay higher upfront payments and accept more stringent pricing terms to secure medium- to long-term supply. Some of SK Hynix’s long-term DRAM agreements with major clients even include advance payments of around 10%–30% and minimum pricing clauses.

In other words, memory suppliers are shifting from being 'price takers in a cyclical market' to becoming 'bottleneck-based price setters.'

Market dynamics: Identifying the threefold pressures behind the recent pullback

Given that the underlying industry logic remains unchanged (AI infrastructure expansion continues to drive up overall memory demand, and shortages in segments like HBM are unlikely to be resolved in the short term), the recent decline in memory stocks should be viewed more as a release of trading-related pressure:

The first source of pressure is rotation within the AI sector.Previously, the market was pricing in 'absolute scarcity of AI compute power,' which led to sustained gains in 'picks-and-shovels' segments such as GPUs, HBM, memory, advanced packaging, and optical communications. However, after reports emerged that Meta is considering launching a cloud business and selling excess AI compute capacity, investors began reassessing profit allocation across the AI infrastructure chain. According to Reuters, Meta may sell raw AI compute capacity, positioning it as a potential competitor to neocloud providers like CoreWeave and NEBIUS. Following the announcement, Meta’s stock rose, while CoreWeave and NEBIUS came under pressure.

This news hit neocloud providers more directly, as it fundamentally alters the question of 'who rents out compute capacity and who captures cloud profits.' However, for memory suppliers, regardless of whether the compute capacity ultimately resides on Meta’s, CoreWeave’s, Google’s, Amazon’s, or Microsoft’s balance sheets, demand for server DRAM, HBM, LPDDR, and enterprise SSDs will not vanish—as long as AI infrastructure continues to expand. The difference lies in short-term capital rotation: funds are shifting from 'hardware picks-and-shovels' toward 'cloud platforms, applications, and software monetization,' causing memory chips to be temporarily sidelined.

The second source of pressure is profit-taking.

Represented by companies like Micron and SK Hynix, memory stocks have already posted very strong performance this year. After such significant gains, any 10%–20% pullback should not be overinterpreted. The greater the price appreciation, the more sensitive the market becomes to marginal disturbances.

When semiconductor valuations become crowded, the AI infrastructure narrative faces disruptions, and capital starts seeking new directions, memory—a segment that has led the rally—is naturally among the first to see positions unwound. In other words, this is not a fundamental thesis being disproven, but rather a rebalancing of positions within a strong-performing sector trading at elevated levels.

The third source of pressure stems from market skepticism about the sustainability of price increases.

Historically, the memory industry has been highly cyclical, and after every price rally, markets instinctively worry about capacity expansion, inventory buildup, and subsequent price declines. But this time is different.AI demand is reshaping the cyclical rhythm. HBM is consuming advanced DRAM capacity, creating simultaneous shortages in server DRAM and LPDDR. Enterprise SSDs are benefiting from AI inference, causing this cycle of supply-demand tightness to last longer than traditional cycles.

Forward-Looking Calendar: July 'Catalyst' Timeline for the Memory Sector

With share prices facing profit-taking pressure at elevated levels, market sentiment will ultimately anchor back to fundamental data. Throughout July, the memory sector will enter an exceptionally dense 'event verification period.' This phase will not only serve as a litmus test for the strength of the current bull run but also represent the pivotal juncture determining whether relevant stocks can break through their valuation ceilings:

July 7–8 | Samsung Q2 Preliminary Earnings: The 'Starting Gun' for Market Sentiment

◦ Event Preview: The company only discloses two key metrics: revenue and operating profit.

◦ Game logic: If earnings beat expectations, it will immediately reaffirm to the market the rigidity of memory demand, further solidifying investor consensus on 'tight supply-demand dynamics + sustained price increases.'

July 10 | 'Dual Resonance' of Industry Cycles and Valuations

◦ Taiwan Semiconductor June Revenue: As the undisputed leader in AI and HPC chip foundry services globally, its monthly revenue figures serve as the best 'thermometer' for gauging downstream AI industry momentum, indirectly validating whether upstream memory demand remains robust.

◦ SK Hynix US listing: Closely monitor its opening performance. If the premium exceeds expectations, it will immediately expand the market's valuation imagination for the HBM leader and potentially trigger a valuation reset across the entire memory sector.

July 16 | Taiwan Semiconductor Q2 official earnings: The 'stabilizing anchor' of AI infrastructure

◦ Event preview: Provide more detailed forward guidance on AI/HPC demand.

◦ Game logic: The market will use this as a key benchmark to assess the pace of global AI infrastructure expansion and the long-term sustainability of underlying memory demand.

Late July | Samsung & SK Hynix Q2 official earnings: The 'ultimate test' for HBM

◦ Event preview: The two memory giants will reveal their full earnings hand.

◦ Game logic: Investors will scrutinize every detail with a magnifying glass. HBM-related revenue contribution, actual shipment volumes, ASP (average selling price), gross margin performance, and full-year guidance. This is the most critical battle determining pricing power and market direction for the memory sector in the second half of the year.

Outlook: Focus on three key validation indicators

Memory stocks have entered a more complex phase of market博弈: fundamentals continue to improve, but trading dynamics are starting to price in recent gains. The real risk to watch isn’t a sudden collapse in memory prices, but rather an exaggerated market reaction to any marginal negative news after the substantial run-up in share prices.

To assess whether memory stocks can regain strength, we recommend filtering out short-term sentiment noise and closely monitoring the following three industry signals:

1. Price trends: Whether DRAM, HBM, LPDDR, and NAND prices from Samsung, SK Hynix, and Micron continue to rise.

2. Long-term agreement terms: Whether long-term supply agreements (LTAs) continue to strengthen (including provisions such as higher prepayment ratios, minimum price guarantees, and absence of price caps).

3. Capital expenditures: Whether AI infrastructure capital expenditures can continue to substantively support demand for server DRAM, HBM, and enterprise SSDs.

Summary

Fundamentals in the memory sector are still driving price increases, long-term contracts remain strong, yet stock prices are already pricing in these gains. The recent sharp short-term decline in memory stocks is largely due to sector rotation and cooling sentiment after a run-up.What’s being sold off right now isn’t fundamentals—it’s trading sentiment.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (24)

to post a comment

116

267