SpaceX officially joins the Nasdaq 100—can it spark a rebound rally?

Is SpaceX, valued at $2.6 trillion, overpriced? Breaking down profitability, valuation, and follow-on buying interest

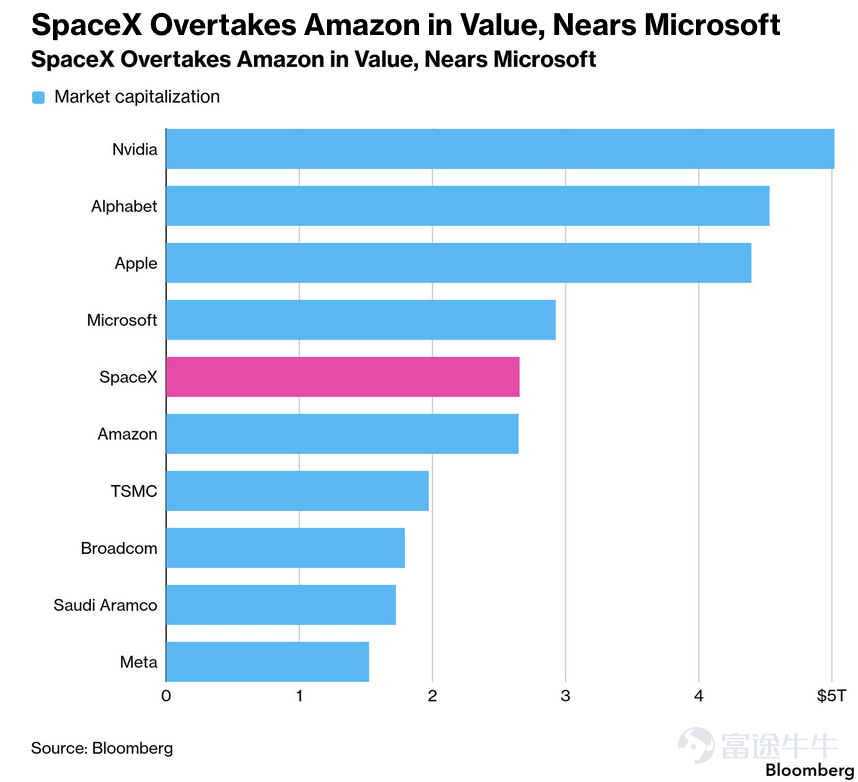

As of June 16, $SpaceX (SPCX.US)$ closed at $201.80, up approximately 49.5% from its IPO price of $135, with a market capitalization of around $2.66 trillion, surpassing Amazon to become the fifth-largest company in the U.S. stock market。Intraday, it peaked at $225.64 before giving back most of its gains. The rally was accompanied by extremely heavy trading volume, with a turnover rate as high as 57.99%, reflecting intense tug-of-war between bulls and bears after breaking through key price levels.

Up 50% over three days—so is it overvalued now?

Based on current earnings, the price looks extremely expensive.

SpaceX reported revenue of USD 18.674 billion in 2025, adjusted EBITDA of USD 6.584 billion, and a net loss of approximately USD 4.9 billion. Based on a market valuation of USD 2.66 trillion, the price-to-sales ratio is approximately 142x,and the enterprise value to adjusted EBITDA ratio is approximately403x;

However, even under Wall Street's most optimistic 2030 forecast, there is still some room for justification.

According to the Financial Times, citing Goldman Sachs' forecast model presented to potential IPO investors, Goldman Sachs projects SpaceX’s revenue could rise from USD 18.7 billion in 2025 to USD 474 billion by 2030, with AI-related revenue potentially reaching USD 322 billion. Morgan Stanley’s forecast is relatively more conservative, at around USD 330 billion.

This set of projections is quite aggressive.Growing from $18.7 billion in 2025 to $474 billion in 2030 implies roughly a 25-fold increase in revenue over five years,representing a compound annual growth rate of nearly 91%.If fully realized, the current market capitalization would equate to approximately 5.6 times 2030 revenue.

Of course, this growth rate requires multiple conditions to be met simultaneously, such as:

AI computing capacity leasing contracts rapidly converting into revenue;

xAI models and enterprise customer business have expanded significantly;

Data centers continue to receive heavy investment and maintain high utilization rates;

Starship improves the efficiency of satellite deployment and space-based computing infrastructure development;

Massive capital expenditures can continue to secure financing.

Returning to fundamentals, can SpaceX truly generate profits?

Currently, among SpaceX's three main business segments, only Starlink has achieved profitability. The AI segment is now the largest source of losses, dragging down the company's overall earnings.

SpaceX has demonstrated its ability to generate profits—Starlink has already proven this. Whether the group achieves sustained net profit depends on the pace of AI-related capital expenditures. If management slows its expansion, achieving overall profitability would not be difficult; however, under the current investment plan, GAAP losses over the next few years would also be normal.

1. Starlink has already demonstrated clear profitability

In 2025, the Connectivity segment—primarily comprised of Starlink—is projected to generate $11.387 billion in revenue, $4.423 billion in operating profit, and adjusted EBITDA of $7.168 billion. In Q1 2026, the segment reported $3.257 billion in revenue and $1.188 billion in operating profit.Starlink has already become SpaceX’s true cash flow engine internally.

2. Rocket business is nearing EBITDA profitability, but Starship development remains heavily capitalized.

The Space segment generated $4.086 billion in revenue in 2025, with an operating loss of $657 million and adjusted EBITDA of $653 million. During the same period, Starship-related R&D expenses totaled approximately $3 billion.In other words, Falcon launches and government contracts already have a commercial foundation, whereas Starship remains in a high-investment phase.

3. The biggest variable stems from AI.

AI segment revenue in 2025 is projected at $3.201 billion, with an operating loss of $6.355 billion and capital expenditures of $12.727 billion. In Q1 2026 alone, AI capital expenditures reached $7.723 billion, with an operating loss of $2.469 billion.A significant portion of Starlink’s earnings is being absorbed by AI computing infrastructure buildout and xAI investments.

The AI business has also secured significant orders. SEC filings show that under one agreement with Anthropic, payments could reach up to $1.25 billion per month through May 2029; under another agreement, Google plans to pay $920 million per month from October 2026 to June 2029, subject to GPU delivery volumes and termination clauses.While the order size is substantial, revenue recognition and profitability will still depend on equipment deliveries, energy costs, and compute utilization rates.

What conditions are needed for further upside? What’s the trading-level conclusion?

SpaceX can continue rallying,primarily because its total market cap is very large, yet tradable shares are extremely limited—creating conditions for further near-term upside.Price action is currently being driven by share scarcity, index-related buying, and options market makers’ hedging activities.

Currently, only about 4%–5% of the total shares are actually circulating in the market. For a company valued at over $2 trillion, short-term prices are effectively determined by this small fraction of tradable shares. As long as incremental capital flows in concentratedly, adding hundreds of billions to its market cap does not require an equivalent amount of buying.

The launch of options has amplified stock price volatility.On the first day, approximately 1.8 million option contracts were traded, setting a record for the highest first-day volume of any single-stock options listing on U.S. exchanges. The call-to-put volume ratio was roughly 1.3:1. After selling call options, market makers needed to buy the underlying stock to hedge their delta exposure,and rising share prices forced them to keep increasing their holdings, creating a gamma feedback loop.

However, a call/put ratio of 1.3x is not extreme.Some of these calls may also be covered calls, spreads, or institutional risk management positions; the full 1.8 million contracts should not be interpreted as purely bullish bets.

SpaceX has obtained an expensive 'equity currency.'The company’s current high market valuation enables it to acquire AI assets with minimal equity dilution—for example, by using stock to acquire Anysphere, the parent company of Cursor.A high share price itself enhances fundraising and M&A capabilities, creating a positive feedback loop in the near term.

For further upside ahead, the following conditions need to be monitored:

1. The arrival of three waves of index-related capital as expected

As of June 17, 2026, SpaceX has already been included in the Nasdaq Composite Index but has not yet been added to major passive investment benchmarks such as the Nasdaq-100, MSCI, or FTSE Russell indices. The timing for subsequent inclusions is already fairly clear.

The most comprehensive and relatively transparent estimate currently available comes from FT Alphaville combined with Morningstar's fund database. Morningstar analyzed 6,006 U.S. mutual funds, 5,100 ETFs, and 3,203 benchmarks, covering approximately $41.1 trillion in assets. Based on this, FT Alphaville estimates that SpaceX could see around $14.2 billion in benchmark-driven passive buying:

2. The Q2 earnings report must demonstrate that revenue is beginning to catch up with valuation.

The market needs to see: continued growth in Starlink subscribers and profitability; AI contracts starting to translate into revenue; no further deterioration in AI segment losses; steady progress in Starship testing and commercial launch cadence; and capital expenditure growth covered by financing and operating cash flow.

The current share price no longer allows the company to rely solely on long-term narratives—quarterly results must quickly deliver.

Passive inflows can generate short-term buying pressure, but they cannot establish a permanent floor. When everyone knows the purchase date in advance, part of the positive catalyst is often already priced into the stock. The real signal worth watching is whether the stock price can continue to reach new highs after index-related buying has been executed.

3. Trading-level conclusions

Technical indicators are based on only three days of data, limiting their reliability—they’re better suited for gauging short-term positioning dynamics. On June 16, trading volume reached 322 million shares, with a turnover rate still as high as 57.99%,The extremely high turnover indicates thorough position reshuffling, but also implies significant near-term profit-taking and unwinding pressure from previously trapped positions.

Looking at the three-day data, fund flows show a 'high-then-low' pattern. The latest trading day (June 16) reveals that on June 12, institutional investors recorded a substantial net inflow of RMB 3.776 billion, whereas by June 16, this turned into a net outflow of RMB 371 million.This may suggest that some institutional funds took profits at higher price levels.

The odds here primarily depend on index buying pressure and options gamma squeeze—in the short term

– $220–$225 range: key resistance zone; a sustained move above this level would constitute a breakout.

– $245–$250 range: a strong bullish scenario, assuming smooth index-driven buying materializes and options continue to push prices higher.

– Around $300: corresponds to a market capitalization of approximately $3.9 trillion, requiring sustained gamma squeeze and extremely optimistic sentiment.

– $190–$195 range: first support level, aligning with the upper edge of the recent gap; this is a critical defensive line for maintaining the current bullish structure. A pullback to $190–$195 accompanied by shrinking volume and stabilization could present opportunities for staged observation.

– $175–$180 range: important support near the IPO’s first-day high and lock-up expiration terms. A break below $175 would necessitate reassessment of whether the market has begun pricing in lock-up expiration and valuation risks.

– $160–$165 range: vicinity of the first-day closing price and the launch platform for the initial rally; this serves as strong support once sentiment cools down.

Therefore, SpaceX still presents trading opportunities, but it has now entered a phase of high volatility and elevated expectations.How much further it can rise depends on whether index-related capital flows in as expected, whether call option positions continue to expand, and whether the company’s fundamentals can quickly catch up with its valuation.

Index inclusion can generate temporary demand, but it cannot sustain valuation over the long term.As portfolio rebalancing gradually completes, market attention will ultimately return to Starlink profitability, AI-related revenue, Starship development progress, and upcoming share lock-up expirations.

One simple trick to easily track smart money flows!

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (97)

to post a comment

137

366