Nobel Laureate Calls Elon Musk a Ponzi Scheme; Investors Forced to Foot the Bill for SpaceX

On the first day of SpaceX’s listing, Elon Musk became the first trillionaire in human history.

On the same day, Paul Krugman, the 2008 Nobel laureate in economics, published an article titled 'Elon Musk, Human Ponzi Scheme,' directly labeling Musk as a 'real-life Ponzi scheme.'

In this scathing piece, he criticized Musk for having 'destroyed X’s business model after acquiring Twitter, turning it into a cesspool,' driving away advertisers and leaving banks stuck with $13 billion in debt. The platform later didn’t recover thanks to its core business but was instead kept alive by Trump’s political comeback and the AI boom.

At the end of the article, Krugman stated bluntly:"Elon Musk’s massive Ponzi scheme will inevitably collapse."

In Krugman’s view, Musk’s wealth-generating machine has long ceased to rely solely on rockets, electric vehicles, and satellite internet. Instead, it resembles a capital cycle built around the 'Musk genius myth': investors believe Musk can create the future, so they keep buying shares in his companies; rising valuations then reinforce the belief that Musk truly can shape the future.

The SpaceX IPO has pushed this cycle to its most perilous stage yet.

Because this time, the buyers won't just be Musk's believers, Wall Street players, and proactive investors.

Even those who don’t believe in Musk might be forced to buy in.

01

A real-life Ponzi scheme

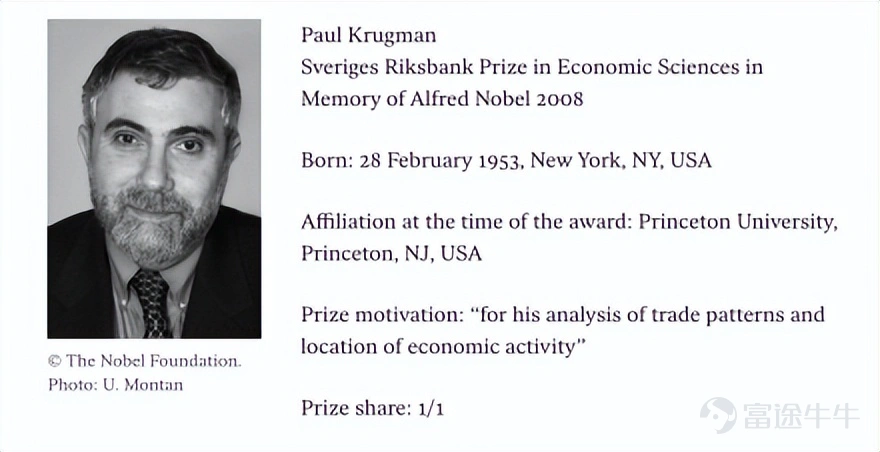

Paul Krugman isn’t just an ordinary Elon Musk critic.

He is the 2008 Nobel laureate in economics and has long written a column for The New York Times, consistently placing himself at the forefront of debates on U.S. economic and political issues.

His article 'Elon Musk, Human Ponzi Scheme' begins with a dry joke:

Krugman says he stepped out yesterday—first boarding a Hyperloop through underground tunnels dug by The Boring Company, then summoning a fully autonomous Tesla taxi via a brain-computer interface, and casually catching up on the latest news from a Mars colony along the way.

Of course, none of that actually happened.

There’s no operational Hyperloop, no commercially scaled underground tunnel network, no fully realized Tesla full self-driving capability, and no Mars colony.

Yet over the past decade, Musk has repeatedly promised that all these things would be achieved by 2025 at the latest—or even sooner.

What Krugman is trying to say is this: Musk’s greatest talent isn’t turning every future vision into reality, but rather using appealing promises to get capital markets to pay for those futures in advance.

He acknowledges that Musk isn’t without real successes. Tesla did indeed lead the electric vehicle wave at one point, and Starlink is genuinely an important and viable business.

But in Krugman’s view, these genuine achievements aren’t enough to explain the scale of Musk’s current wealth. What truly underpins Musk’s status as the world’s richest person is a self-fulfilling belief.

He wrote in his article:“Musk’s wealth has always been primarily built on self-fulfilling beliefs—investors convinced of Musk’s genius have poured into the stocks of companies he controls, and the resulting surge in those companies’ valuations has further reinforced his reputation as a genius.”

Krugman argues this is a 'Ponzi scheme': it appears successful because new investors keep flowing in, and it attracts new investors precisely because it appears successful.

Musk’s empire doesn’t run on fulfilling all its promises, but rather on using the next bigger promise to cover up the previous one that wasn’t delivered. Before fully realizing autonomous driving, he’s already talking about robots; before fixing X, he’s merging it with xAI; before reaching Mars, he’s already pitching space-based computing power.

But Musk’s real strength lies in his consistent ability to make markets believe:This time hasn’t materialized yet because something truly groundbreaking is still ahead.

Krugman especially singles out X for criticism.

After Elon Musk acquired Twitter, Krugman said he destroyed X's business model, turning it into a 'cesspool,' causing advertisers to flee and leaving banks stuck with $13 billion in debt.

But X didn’t recover through its core business. Its survival relied on two factors: Trump and the AI boom. After Trump’s election victory, advertisers began returning to X because they needed to appease both Musk and Trump. In March 2025, Musk further merged xAI into X, riding the AI wave to boost X’s valuation again and simultaneously repair his own personal balance sheet.

To Krugman, this is a textbook example of the Musk playbook: when the business runs into trouble, switch to an even bigger story. When the old narrative can no longer hold up, attach it to a newer, hotter, and harder-to-disprove vision of the future.

That’s why he says SpaceX’s IPO has made things even clearer: 'Musk’s greatest skill isn’t developing futuristic products—it’s his mastery of financial engineering and leveraging insider connections.'

Elon Musk himself is the engine driving this 'wealth-creation machine.'

02

SpaceX, Sold to the Moon

SpaceX’s IPO has perfectly spotlighted the very system Krugman most wants to criticize.

Although this company isn’t one of those bubble firms that only have pitch decks and no real business—SpaceX’s technology, revenue, and industry standing are all genuine. Starlink has already become its biggest cash cow. According to its prospectus, SpaceX reported total revenue of approximately $18.67 billion in 2025, with connectivity services (primarily Starlink) contributing about $11.387 billion and generating an operating profit of roughly $4.423 billion.

But Krugman argues thatthe price capital markets have assigned to SpaceX has far exceeded what its underlying business justifies.

SpaceX priced its IPO at $135 per share, raising $75 billion and achieving a valuation of approximately $1.77 trillion. On its first day of trading, the stock continued to surge, closing with a market capitalization exceeding $2 trillion, making Elon Musk the world's first trillionaire.

Based on the IPO valuation and projected 2025 revenue, SpaceX’s price-to-sales (P/S) ratio already approached 94x; calculated using its market cap at the end of the first trading day, the P/S ratio exceeded 112x.

By comparison, NVIDIA—already at the epicenter of the AI computing wave—has been one of the most sought-after tech companies in global capital markets over the past few years, with a P/S ratio of roughly 20x. Yet SpaceX has been valued by the market at over 100x.

What investors are buying is no longer just Starlink subscription revenue or rocket launch contracts—those tangible businesses are merely the foundation of this valuation frenzy.

What truly skyrockets the valuation are Starship, space-based computing power, AI data centers—the distant, grandiose, and unverifiable futures.

However, SpaceX’s actual financials are far from rosy. According to its prospectus, the company reported revenue of approximately $18.67 billion in 2025 but still posted a net loss of about $4.9 billion and an operating loss of around $2.6 billion. Additionally, Fortune reports that as of March 31, 2026, SpaceX had accumulated total losses of $41.3 billion.

In Krugman’s view, the SpaceX IPO is not just another tech listing—it is the ultimate showcase of Elon Musk’s wealth machine: a sliver of real success leveraged to inflate a much grander myth of the future.

Krugman asks: How can SpaceX’s 'astronomical valuation' possibly be justified?

His answer: Part of the IPO’s premise is that retail investors will buy shares not because they’ve rationally assessed SpaceX’s business, but because they believe they’re buying a stake in 'the genius Elon Musk.'

But even this base of devoted believers may not be enough—Musk’s Wall Street allies are also rewriting the rules of the game for him.

Major indices such as the Nasdaq 100 and FTSE Russell have recently revised their rules, allowing SpaceX to be included almost immediately after its listing.

This means that once SpaceX joins a major index, index funds will be required to buy its shares. Because index funds are designed to replicate index performance, inclusion automatically triggers new buying demand.

In the past, major indices typically waited at least one year after a company’s IPO—letting things settle first—before considering inclusion. But this time, the rules tilted in SpaceX’s favor.

Krugman argues this demonstrates yet again Elon Musk’s ability to 'co-opt and corrupt key institutions.'

Notably, the S&P 500 has resisted the pressure and still requires SpaceX to be publicly listed for at least one year before it can be considered for inclusion.

03

Ordinary investors are forced to foot the bill

If only Musk’s true believers were buying SpaceX shares, that would still be an active choice.

Some believe Elon Musk will send humans to Mars; others think space-based computing power will become the next critical infrastructure. Some are willing to bet on that future—and whether they win or lose, it’s their own decision.

But index funds have changed the nature of this dynamic.

Many ordinary investors don’t buy individual stocks directly. Instead, they invest through mutual funds, ETFs, pension accounts, and index products in their 401(k) plans.

Index rules dictate that once a company is included in a major index, funds tracking that index must buy it. Portfolio managers may not like the stock, and retail investors may not understand it—but if the rules require its inclusion in the portfolio, it will be included.

Krugman cited a statistic: today, about 52% of mutual fund assets are invested in index or index-linked products, and more than half of American households hold mutual funds.

In other words, once SpaceX enters an index, the story is no longer just a game among the wealthy, institutions, and Musk’s fans—ordinary retail investors, whether they believe in Musk or not, will be forced to buy in.

An individual might distrust Elon Musk, choose not to invest in SpaceX, ignore rocket launches, and care nothing about colonizing Mars. But as long as their pension, mutual fund, or ETF tracks the relevant index, they could unknowingly become part of Musk’s capital game.

Krugman argues that Musk’s wealth-creation myth will eventually run into trouble: the future cannot be postponed indefinitely, and narratives cannot forever substitute for cash flows. The moment the market stops believing 'Musk will always deliver the next miracle,' the cycle will reverse.

A valuation decline would weaken Musk’s aura of genius; a weaker aura would prompt more investors to exit; and investor exits would further depress valuations…

That’s why Krugman bluntly states at the end of his article:‘Elon Musk’s massive Ponzi scheme will inevitably collapse. Traditional Ponzi schemes only exploit investors who voluntarily participate. But this time, a significant portion of the funding propping up Musk’s scheme will come from ordinary Americans who are forced to participate.’

SpaceX is merely the first case to bring this issue into the open.

Next, AI giants like OpenAI and Anthropic will gradually enter public markets, and their valuations, too, are not based solely on today’s revenues.

When these companies are packaged as 'infrastructure for the AI era,' they naturally gain eligibility for inclusion in indices, mutual funds, and pension portfolios.

By then, it will be hard for anyone to avoid them.

Ordinary investors may not participate in this wealth-creation game, yet they could still bear the consequences when the bubble bursts. $SpaceX (SPCX.US)$$SpaceX Ecosystem (LIST24213.US)$$SpaceX concept (LIST24026.SH)$$Space (LIST2556.US)$$Space Themed ETF (LIST24173.US)$$Financials (LIST20758.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

2