Zhongji Xuchuang is now in hot IPO subscription! Around 80% of new listings in 2026 rose on their fi

New IPO Spotlight | HiClear Intelligence in Hot Subscription: Three Core Strengths Highlight Its Value as a Leading 'AI + Hardware' Play

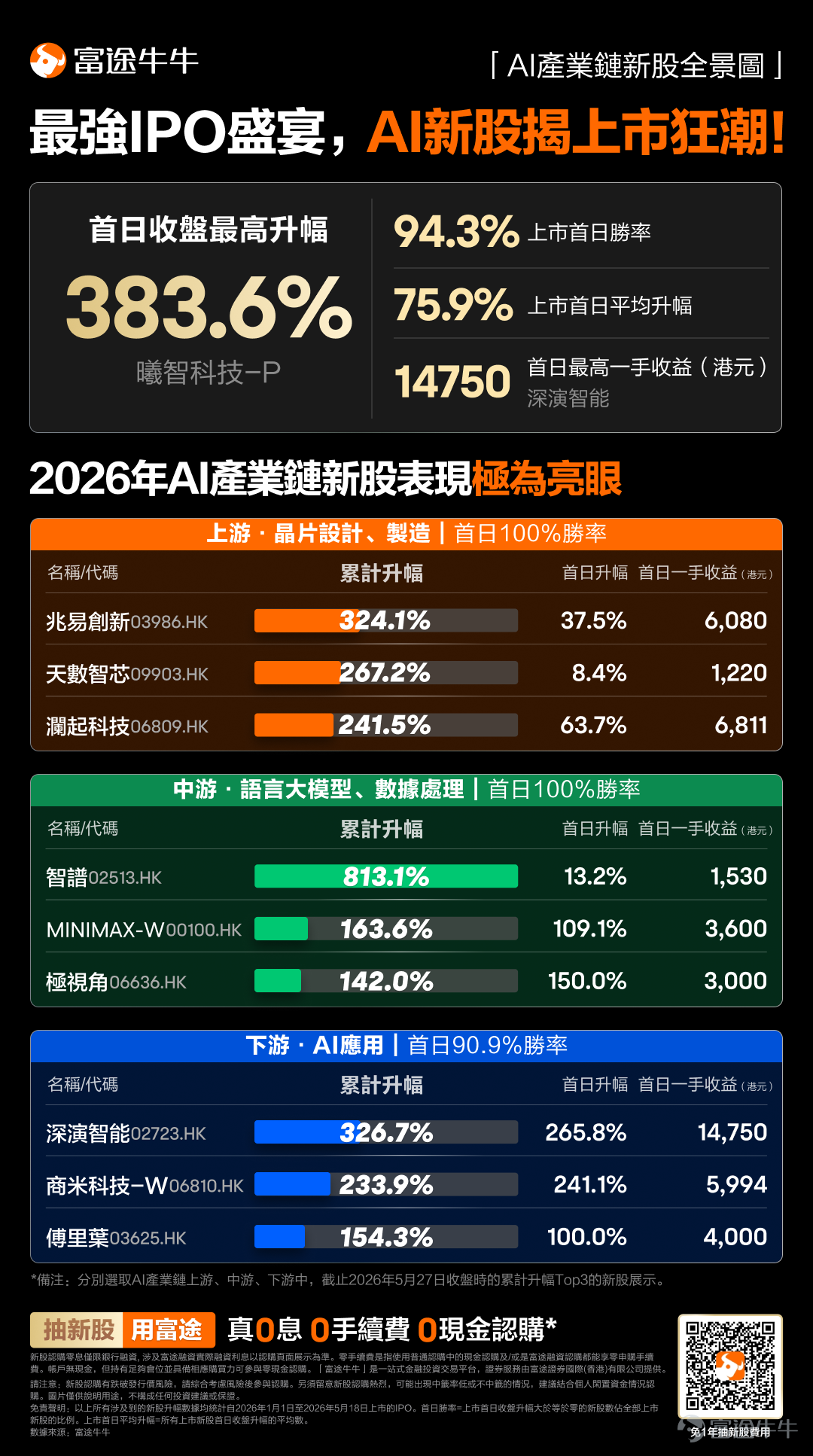

The Hong Kong IPO market has delivered strong performance in 2026, with over 90% of new listings rising on their debut day year-to-date!

Among them, AI-related IPOs have stood out the most. As of this writing, the multispectral AI leader $HQVT (01392.HK)$ is in hot subscription!

I. Company’s Core Business

HiClear Intelligence’s core products revolve around 'multispectral' technology:Ordinary cameras capture only visible light—the portion perceivable by the human eye. Multispectral devices, however, can simultaneously detect visible light, near-infrared, far-infrared, and even ultraviolet wavelengths, covering a spectrum from 400 nanometers to 1,000 micrometers. In simple terms, they can 'see' what conventional cameras cannot—heat sources in total darkness, human figures through smoke, or disguised heat-emitting equipment.

This sensing capability means the company’s clients are primarily concentrated in sectors such as security, industrial inspection, and government surveillance—areas that demand extremely high image precision and reliability and exhibit relatively low price sensitivity.

HiClear Intelligence’s main business consists of three segments:

The first segment is modules (accounting for 31.3% of revenue in 2025). These are embedded components sold to AI hardware manufacturers and system integrators for integration into their own products. This business segment scaled up earliest but faced significant pricing pressure—the average selling price (ASP) of modules was proactively reduced from RMB 695 in 2022 to RMB 510 in 2024 to capture market share. The trade-off was a gross margin decline from 21.4% to 7.6%. By 2025, the ASP rebounded to RMB 675, with gross margins recovering accordingly.

The second segment is perception terminals (accounting for 13.9% of revenue). These are ready-to-use standalone devices that operate independently of the cloud. The main product forms include thermal imaging security terminals and AI-powered access control systems. With an average selling price of approximately RMB 1,276, this segment generates the most stable cash flow among the three business lines.

The third segment is large-model services (accounting for 53.1% of revenue). This is currently the company’s key growth narrative. Leveraging its proprietary 'Zhiyuan Origin Large Model,' the company delivered AI services that generated RMB 114 million in revenue during its first commercial year in 2024, which surged to RMB 355 million in 2025—a 212% year-over-year increase—making it the largest revenue contributor.

The training data for the large model comes from the company’s years of accumulated perception hardware deployments: over 10 million multispectral perception data points, records of more than 100,000 real-world hazardous incidents, and over 10,000 nodes in safety engineering knowledge graphs. Deployment is primarily on-premises, enabling clients to run the model on their own servers—a highly competitive feature for government and telecom operator clients who are extremely sensitive about data leakage.

The three business lines are not simply parallel; rather, they form a cohesive value chain. Modules serve as the entry point for perception data, terminals provide scenario-based validation, and large-model services monetize the data and operational experience accumulated from the first two segments. Hardware leads, software follows—it’s a logical sequence.

II. Positioning within the AI Industry Chain

To understand an AI company, one must first clarify its position across the entire industry value chain.

The AI industry chain is broadly divided into three layers: upstream includes chips and foundational computing power; midstream comprises industry-specific algorithms and sensing devices; and downstream consists of AI applications targeting end users.

Haiqing Zhiyuan primarily operates in the lower midstream—more precisely, it functions as a 'vertically integrated player extending downstream.'—Its module business falls within the midstream, constrained by upstream sensor chip suppliers and facing price competition from peers. Its terminal business sits in the lower midstream, directly entering specific application scenarios. Its large-model services are even closer to the downstream.

In terms of market potential, according to forecasts by Frost & Sullivan, China's multispectral AI industry is projected to reach RMB 58.8 billion by 2029, with a compound annual growth rate (CAGR) of approximately 31% between 2024 and 2029. The market remains highly fragmented, with the top five players collectively holding only a 10.9% market share.Haiqing Zhiyuan ranks first with a 3.5% market share,but leads the second-place player by merely 0.5 percentage points. This indicates that an oligopolistic structure has yet to emerge, and the value of its first-mover advantage hinges on whether it can widen this gap going forward.

III. Why Haiqing Zhiyuan’s listing merits attention

Against this backdrop, Haiqing Zhiyuan’s debut presents several noteworthy factors:

First is its scarcity value. There are currently no comparable listings on the Hong Kong stock exchange—the combination of 'multispectral sensing hardware + edge-side AI algorithms + vertical large-model services' is unique in the Hong Kong market. Among A-share companies, ArcSoft focuses primarily on smartphone imaging algorithms, Gridsum DeepView specializes in urban computer vision, Luster LightTech emphasizes industrial machine vision, and CloudWalk Technology concentrates on human-AI collaboration—each with distinct strategic focuses.

Second, it has genuine profitability as a solid foundation. It returned to profitability in 2024, reporting a net profit of RMB 293.5 million on the books in 2025 and an adjusted net profit of RMB 552.5 million. Most AI-related new listings go public while still unprofitable; Haiqing Zhiyuan at least provides the market with a valuation anchor.

Third, its business structure is undergoing a fundamental transformation.Revenue from large-model services, which was nearly zero in 2023, rose to 53.1% within two years. Markets typically assign higher valuation multiples to 'software-driven transitions' because software businesses theoretically have lower marginal costs and stronger economies of scale. If large-model services become more standardized going forward and gross margins rebound above 40%, the overall earnings elasticity would be substantial.

Fourth, management has put real money behind its confidence. In July 2025, the company completed its Series D financing round, during which management voluntarily contributed an additional RMB 500 million.

The above content is based on Haiqing Zhiyuan's publicly filed prospectus and disclosed financial data. Data is current as of June 2026, and market conditions may change at any time. This document does not constitute investment advice of any kind.

The golden season for new stock subscriptions has arrived! Use Futu for new stock subscriptions—zero interest, zero handling fees, and zero cash subscription. Participants now have the chance to have their new stock subscription fees waived for a year.Come and experience it now >>

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

17

36