Waller's new policy measures are in the works! How should investors respond?

Kevin Warsh's Monetary Policy Analysis

By Chen Ningdi and Ma Xingkong

On May 22, 2026, Kevin Warsh officially assumed office as Chair of the Federal Reserve. What is Warsh's monetary policy philosophy? And what impact will a Fed under his leadership have on the U.S. and global economies?

01

Warsh's Policy Positions

Warsh has articulated his policy views on numerous public occasions, which can be summarized into the following three points:

1. Prioritizing inflation control, with a hawkish stance;

2. Strongly defending the Federal Reserve's independence;

3. A combination of 'balance sheet reduction' and 'interest rate cuts';

Warsh stated that the Federal Reserve committed a 'fatal policy error' in 2021–2022. At the time, the Fed believed that the high inflation seen during the pandemic was merely transitory, leading to delayed tightening measures. This resulted in soaring and nearly uncontrollable inflation after 2022. Post-pandemic, cumulative price increases for many essential goods reached 25%–35%, causing significant hardship for American households.

During the pandemic, the Fed launched its fourth round of quantitative easing (QE), enacting large-scale monetary stimulus. While this boosted U.S. asset prices, it also exacerbated wealth inequality, resulting in a K-shaped recovery: asset prices rose for the wealthy, while ordinary households bore the brunt of rising consumer prices.

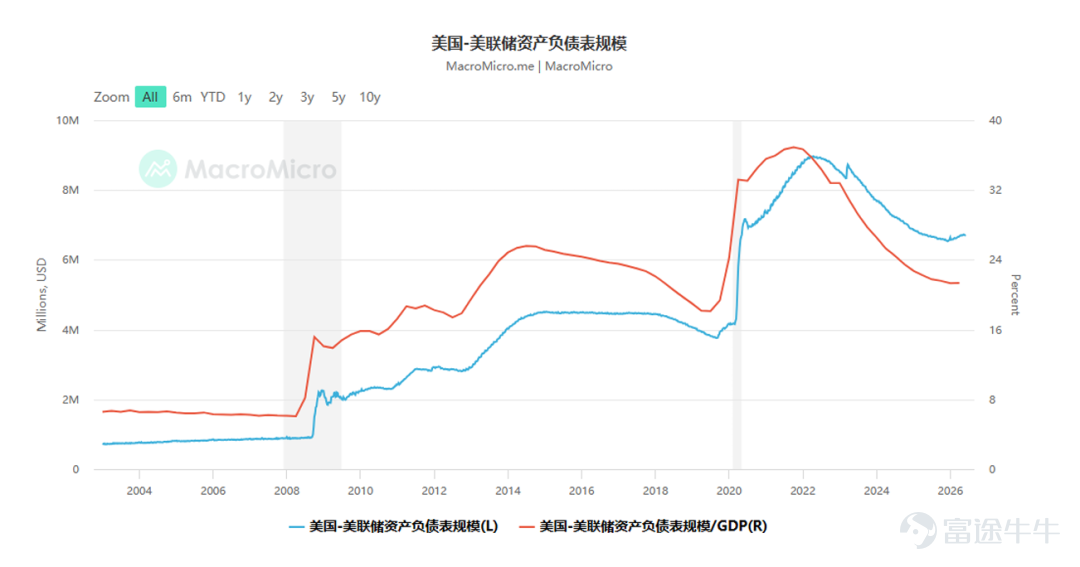

And 'balance sheet reduction' plus 'interest rate cuts' constitute the specific policy path proposed by Warsh. Warsh believes the Fed's balance sheet is currently bloated. Before 2008, the Fed’s balance sheet stood at only around $800 billion. After the financial crisis erupted, to stabilize the financial system, the Fed implemented quantitative easing (QE) by purchasing massive amounts of U.S. Treasuries and mortgage-backed securities (MBS), causing its balance sheet to swell to approximately $9 trillion at its peak.

Figure 1: The Federal Reserve's balance sheet has expanded rapidly since 2008. Source: MacroMicro

Warsh argues that the Fed should selectively unwind its MBS holdings and return to aportfolio consisting solely of Treasury securitiesstructure. The Fed’s monetary policy framework should shift back from an 'ample-reserves regime' to ascarce-reserves regime.”。

What is the 'scarce-reserves regime'?

02

Pre-financial crisis: scarce-reserves regime

Prior to the 2008 financial crisis, the Federal Reserve operated under a 'scarce-reserves regime.' Under this framework, the Fed could significantly influence the federal funds rate through modest open market operations involving Treasury securities. This approach relied on the premise that banks held minimal excess reserves, leaving the banking system structurally short of reserves.

How should we understand this entire framework?

First, we need to understand the concept of reserve requirements. Reserve requirements refer to the portion of each deposit that commercial banks are mandated by the central bank to hold at the central bank itself. The original intent of this requirement was to mitigate bank run risks by ensuring that banks maintain a certain amount of liquidity at the central bank to meet potential depositor withdrawals. Over time, reserve requirements evolved into a key tool for central banks to manage liquidity across the banking system.

When the central bank raises reserve requirements, banks must hold a larger portion of their deposits as reserves, reducing the amount of funds available for lending. This decreases the overall money supply in the market and leads to an increase in the federal funds rate. Conversely, when the central bank lowers reserve requirements, banks have more lendable funds, increasing market liquidity and pushing down the benchmark interest rate.

The Federal Reserve adjusts reserve requirements in real time based on market conditions. For example, on December 20, 2007, the U.S. lowered the threshold for the 10% reserve requirement from $45.8 million to $43.9 million. This change resulted in an additional $57 million in required reserves, which—amplified by banks’ leverage effect—tightened market liquidity.

Figure 2: Changes in the Federal Reserve’s reserve requirement ratios around December 20, 2007. Source: Fed

At that time, reserves earned no interest, so banks held only the minimum required amount. Any excess funds were lent out in the interbank market to earn interest income. Banks maintained very little excess reserves and, when facing temporary funding needs, borrowed from either the Federal Reserve or the interbank market to meet daily liquidity requirements—this was known as the scarce-reserves system.

Under these circumstances, the Federal Reserve could influenceopen market operationsto directly adjust the total level of bank reserves. Open market operations refer to the central bank buying or selling government securities in the open market. When the Fed purchases Treasury securities, it pays the selling bank, increasing the balance in that bank’s reserve account at the Fed. Conversely, when the Fed sells Treasuries, banks’ reserve balances decrease. Because excess reserves were minimal, even a small shortage of reserves would heighten banks’ willingness to borrow, thereby pushing up the federal funds rate.

This was the monetary policy framework under the 'scarce-reserves system.' The United States operated under this framework prior to the 2008 financial crisis. The People’s Bank of China currently manages monetary policy through open market operations as well.

Figure 3: Federal Reserve balance sheet as of December 26, 2007 (in millions of USD). Source: Fed

The chart above shows the Federal Reserve’s balance sheet at the end of 2007. On the asset side, U.S. Treasury securities accounted for the vast majority—nearly 80%. On the liability side, reserves totaled only $5.8 billion, less than 1% of the total balance sheet size.

Let’s take another look at the Federal Reserve’s balance sheet at the end of 2015, and we’ll notice that it had already undergone structural changes:

Figure 4: Federal Reserve Balance Sheet as of December 31, 2015 (in millions of U.S. dollars), Source: Fed

First, the size of the Federal Reserve’s balance sheet expanded significantly. In 2007, the Fed’s balance sheet stood at just $900 billion, but by the end of 2015, it had grown to $4,538.2 billion—nearly fivefold.

The composition of both assets and liabilities also changed. On the asset side, the share of mortgage-backed securities (MBS) rose sharply, reaching $1.7 trillion. These MBS functioned similarly to Treasury securities, injecting substantial base money into the market. As banks held more idle cash, excess reserves on the liability side of the Fed’s balance sheet surged to $2.3 trillion.

This structural shift began after 2008 and is known as the 'ample reserves regime.' As the name suggests, ample reserves refer to a massive volume of excess reserves. Under this regime, open market operations ceased to serve as the primary tool for interest rate control, and monetary policy no longer relied on daily, fine-tuned open market operations.

Figure 5: Excess reserves surged significantly after the 2008 financial crisis, Source: Fed

Why did this turning point occur?

03

Post-financial crisis: Ample reserves and quantitative easing

The transition from a 'scarce reserves' to an 'ample reserves' regime occurred during the 2008 financial crisis. Without rehashing the details of the crisis, suffice it to say that, during this period, to prevent the collapse of major financial institutions and avoid systemic financial turmoil, the Federal Reserve deployed a series of facilities to purchase large quantities of unwanted mortgage-backed securities (MBS), thereby injecting massive liquidity into the market. This excess liquidity eventually became banks’ excess reserves held at the Fed.

Figure 6: Changes in the liability side of the Federal Reserve’s balance sheet during the financial crisis, Source: Ben Bernanke, 'The Federal Reserve and the Financial Crisis'

As shown in the chart above, reserve balances surged from less than $10 billion before the crisis to over a trillion dollars, shifting the banking system from a 'structural' shortage to an 'excess reserves' environment.

The reason was that after the crisis erupted, the Federal Reserve rapidly cut its benchmark interest rate. By December 2008, the federal funds rate had essentially fallen to zero—the lower bound—leaving no room for further conventional rate cuts. Traditional monetary policy tools were exhausted, and open market operations could no longer influence liquidity in the banking system. The Fed therefore turned to unconventional monetary policy measures—quantitative easing.

Figure 7: U.S. Federal Funds Target Rate in 2008, Source: Fed

Quantitative easing refers to the Federal Reserve directly purchasing assets in the market, primarily U.S. Treasuries and mortgage-backed securities (MBS)—which were largely unwanted at the time. When the Fed buys large quantities of securities, bond yields decline. Lower yields correspond to higher bond prices. Thus, quantitative easing directly lowers long-term interest rates and pushes up asset prices. The Fed hoped this unconventional monetary policy would reduce long-term rates and stimulate economic growth. Starting in 2008, the Fed implemented four rounds of QE, continuously expanding its balance sheet.

First round of QE:2009–2010: QE1 involved direct purchases of $1.75 trillion in housing-related securities.

Second round of QE:2010–2011: Purchased approximately $600 billion in long-term U.S. Treasury securities.

Third round of QE:2012–2014: Open-ended purchases totaling approximately $1.6 trillion by the end of the program.

Fourth round of QE:2020–2022: Unlimited QE, exceeding USD 4 trillion in scale.

Figure 8: The Federal Reserve implemented four rounds of quantitative easing, driving its balance sheet to nearly USD 9 trillion. Source: Fed

After the fourth round of QE ended, the Federal Reserve’s balance sheet reached USD 8.9 trillion, peaking at over 36% of GDP. Initially, QE was only intended to address liquidity shortages under extreme circumstances. However, following the crisis, in 2019, the Fed formally announced that an ample reserves regime would serve as its long-term policy framework. In March 2020, the Fed reduced reserve requirement ratios to 0% across the board, fully transitioning to the ample reserves framework.

At this point, the Fed realized that when it pushed the federal funds rate down to zero and sought monetary easing, these excess reserves were harmless. However, when the Fed needed to raise rates to curb inflation, it had to pay interest on these excess reserves—otherwise, its interest rate policy would become ineffective. This explains why the Interest on Reserve Balances (IORB) aligns with the federal funds target rate and is also one reason behind the Fed’s operating losses.

Figure 9: U.S. Federal Funds Rate. Source: MacroMicro

The chart below shows the latest Federal Reserve balance sheet (as of end-2025), which exhibits no fundamental changes on either the asset or liability side. On the asset side, mortgage-backed securities (MBS) remain the second-largest asset class after U.S. Treasuries; on the liability side, reserves continue to be the largest liability item.

Figure 10: Federal Reserve Balance Sheet as of December 29, 2025 (in millions of USD). Source: Fed

This is the decade-long status quo facing Kevin Warsh, who now seeks sweeping reforms to this system.

04

Kevin Warsh: Returning to a 'Scarce Reserves' Framework

Kevin Warsh’s monetary policy approach fundamentally aims to correct the Federal Reserve’s past actions and calls for a return to a 'scarce reserves' regime. Warsh particularly opposes the last three rounds of quantitative easing (QE), arguing that using QE to stimulate the economy was unnecessary. He believes the Fed’s long-standing maintenance of an oversized balance sheet has distorted market-based pricing of money, weakened fiscal discipline, damaged the Fed’s credibility, and primarily benefited financial capital. Therefore, although Warsh supports interest rate cuts, he opposes relying on continuous balance sheet expansion to suppress rates.

Kevin Warsh seeks to shrink the balance sheet and restore policy credibility to create room for maneuvering with the policy rate. He posits that reducing the Fed’s massive balance sheet inherently exerts a tightening effect. In his view, every $1 trillion reduction in bond holdings is roughly equivalent to freeing up about 50 basis points of room for lowering the policy rate. This is because the current Fed heavily intervenes in private funding markets; abundant liquidity has effectively eliminated the traditional interbank lending market, and large amounts of funds prefer earning interest from the Fed rather than being lent out. Whenever market turbulence arises, the Fed calms panic by expanding its balance sheet. Warsh argues thatthe Fed has deprived private markets of their ability to identify risk through price signals, and balance sheet runoff can restore this capacity.ultimately encouraging banks to earn profits in the market, expand credit supply, and support the real economy.

Figure 11: Federal Reserve Balance Sheet – Assets Side, Source: Fed

From a policy implementation standpoint, Warsh’s proposed combination of 'balance sheet runoff' plus 'rate cuts' could take several years to execute. On one hand, such a tightening policy would require majority support from the Federal Open Market Committee (FOMC), yet the U.S. fiscal deficit remains elevated in fiscal year 2026, making it difficult to sustain without continued debt issuance—hence, implementation will not be smooth. On the other hand, the prolonged Iran crisis has heightened future inflation expectations, limiting the scope for rate cuts within the year. More importantly, Warsh’s stance potentially conflicts with the Trump administration’s desire for rapid and substantial rate cuts, posing a test to the Fed’s independence.

1

Reserve requirements account for 15% of commercial banks’ total deposits.

SinceMarch 26, 2020the Federal Reserve lowered the reserve requirement ratio for all depository institutions nationwide to0%and has maintained it at that level ever since. This means that, in theory, U.S. commercial banks could recycle money infinitely—as long as borrowers exist, the U.S. money multiplier could become infinite. However, these funds have not been lent out; instead, they sit idle on the Fed’s balance sheet, earning interest, amounting to approximately $3 trillion today. This results in extremely low capital utilization. Once forced balance sheet reduction begins—i.e., the Fed sells $3 trillion worth of MBS and Treasuries—commercial banks would need to use their excess reserves to purchase these securities. How much additional liquidity could these $3 trillion in assets generate once back on commercial banks’ balance sheets? Our estimate is at least $12 trillion!

Figure 12: Reserves / Commercial Bank Deposits, Source: Publicly Available Data

2

The U.S. money multiplier is 4.17

Figure 13: U.S. Money Multiplier, Source: MacroMicro

The current U.S. money multiplier stands at 4.17. It’s important to note that this figure has been generated under an ample-reserves regime. Should these excess reserves cease earning high interest and rapidly flow into the commercial market to participate in credit creation, the U.S. money multiplier would rise accordingly. Prior to the current easing cycle, the U.S. money multiplier was around 8x. Assuming it reverts to that level, the injection of USD 3 trillion into commercial banks could generate approximately USD 24 trillion in liquidity. This would significantly stimulate the U.S. economy and reignite upward momentum in capital markets. I believe this is Kevin Warsh’s ultimate objective.

05

Conclusion

1. Prior to 2008, the Federal Reserve implemented a 'scarce reserves' framework for monetary policy, managing interest rates through open market operations;

2. After 2008, the Fed shifted to an 'ample reserves' framework, causing its balance sheet to expand dramatically. On the asset side, it purchased large quantities of MBS and Treasury securities; on the liability side, banks deposited massive amounts of excess reserves. Traditional monetary policy tools became ineffective, and the Fed began relying on the Interest on Reserves (IOR) rate to influence market rates.

3. Warsh advocates 'balance sheet reduction' plus 'rate cuts,' which effectively means returning to the pre-financial-crisis 'scarce reserves' framework. He supports significantly shrinking the Fed’s balance sheet and reverting to a system primarily backed by Treasury securities.

4. Assuming Kevin Warsh successfully implements USD 3 trillion in balance sheet reduction, it could generate at least USD 12 trillion—and optimistically up to USD 24 trillion—in market liquidity, driving global asset prices higher.。

Author Bio:

Ningdi Chen, a graduate of the University of Chicago with an Honors Bachelor's degree in Economics and Statistics, has over 26 years of experience in the global financial industry. He founded Delin Securities and Delin Family Office and was previously a licensed responsible person for Type 1, 4, and 6 licenses granted by the Hong Kong Securities and Futures Commission. He currently serves as Chairman of the Board, Executive Director, and Chief Executive Officer of Delin Holdings Group, Vice President of the Hong Kong Limited Partnership Fund Association, and authored 'The Era of Wealth Transformation: Discovering Counter-Cyclical Survival Wisdom.'

Ma Xingkong graduated with a bachelor's degree from the Chinese University of Hong Kong and a master's degree from Tsinghua University. He served as the chief planner of 'Caijing Langyan' and is currently the chief economist at Delin Holdings, as well as the executive dean of the Delin New Economy Research Institute. He is a licensed holder of Hong Kong SFC Type 4 license and authored several best-selling books, including 'Trade Capability Shapes National Capability,' 'Where Are Your Investment Opportunities,' and 'Hope Amidst Depression.'

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1