Innovative drugs continue to be strong! Have you jumped on this wave?

ASCO 2026 wraps up—will Chinese pharmaceutical companies take center stage this time?

1. Akeso Inc. takes the Plenary Session stage $AKESO (09926.HK)$

Strategic significance: The Plenary Session is ASCO's highest-profile platform. Positive overall survival (OS) data for Ivonescimab indicates that the PD-1×VEGF bispecific antibody could establish a new global standard of care for first-line treatment of squamous non-small cell lung cancer (NSCLC).

1.1. Head-to-head data

1.2. FDA approval still requires further readout from Summit’s HARMONi-3 trial.

The main reason for the stock's high open followed by a decline is that the data did not meet the FDA’s approval pathway requirements.This trial enrolled only Chinese patients. The FDA is highly cautious about data from trials conducted solely in China—the ICH E17 guideline requires multi-regional clinical trial (MRCT) data, and China-only trials need additional bridging studies or global trials to support an NDA.

Additionally, HARMONi-6 used tislelizumab plus chemotherapy as the comparator, whereas the globally recognized standard of care (SoC) accepted by the FDA is pembrolizumab (Keytruda) plus chemotherapy.

In the future, FDA approval hinges more on Summit Therapeutics’ HARMONi-3 trial—a global, multicenter study comparing against pembrolizumab plus chemotherapy—which is the type of registrational trial the FDA would accept.The overall survival (OS) data from HARMONi-6 primarily serves as scientific proof of concept and supports the pathway for approval by China’s NMPA.

1.3. Performance of Other Competitors

After Akeso Inc. released its clinical data, its stock came under pressure—not only due to pending data validation and policy uncertainties in both the U.S. and China, $Merck & Co (MRK.US)$ but also largely because of commentary during ASCO presentations.

Merck & Co. has taken a pivotal strategic shift regarding MK-2010, a PD-1/VEGF bispecific antibody in-licensed from LianBio:It will advance MK-2010 to Phase 3 readiness and position it as a strategic successor to Keytruda (K drug).

Although the earlier collaboration already secured pipeline rights, Merck’s prior public statements were conservative, limiting combination use to existing standard-of-care regimens. Within just two months, however, its strategy has undergone a comprehensive upgrade—driven fundamentally by the continued clinical validation of MK-2010. Leveraging Merck’s deep expertise in the PD-1 plus VEGF space, MK-2010 has rapidly progressed into a Phase 3 registrational trial, elevating it from an early-stage candidate to a key asset in the company’s portfolio.

In terms of combination strategies, Merck & Co. has clearly prioritized next-generation therapeutics such as ADCs and precision-targeted agents. Notably, Kelun Pharma’s SAC-TMT (a Trop2 ADC) has been highlighted as a benchmark combination partner, thereby unlocking substantial commercial potential for PD-1×VEGF bispecific antibodies.

1.4. Impact on the ADC Sector

(1) The opportunity for ADC monotherapy to enter first-line treatment of squamous NSCLC may be constrained.

If Yivoxi becomes the new standard of care in the first-line setting, the comparator regimen would shift from Keytruda plus chemotherapy to PD-1 & VEGF inhibitor plus chemotherapy. This PD-1 & VEGF inhibitor plus chemotherapy regimen simultaneously blocks the PD-1 immune checkpoint and tumor angiogenesis while delivering cytotoxic killing. Under this scenario, the marginal benefit that ADC monotherapy could additionally provide is significantly diminished.

(2) Impact on IO 2.0 + ADC

As a form of 'precision chemotherapy,' ADCs are expected to be combined with PD-1/VEGF inhibitors to form a new first-line treatment paradigm, especially as Merck & Co. has described such combinations as 'the combinations of the future.'

Currently, IO 2.0 + ADC combinations remain in early stages, with pipeline progress in the Hong Kong-listed innovative drug sector still at Phase I/II trials. Akeso’s pipeline development is primarily focused on the following:

II. LBA (Late-Breaking Abstracts) – Key Hong Kong and U.S.-listed Stocks

III. Key Hong Kong and U.S.-listed Stocks Featured in Oral Presentations

IV. Hengrui Pharma

$HENGRUI PHARMA (01276.HK)$ Over 90 oncology studies presented—leading all Chinese pharmaceutical companies in scale

Fluzoparib + AA-P as first-line treatment for mCRPC – Oral presentation

Multiple ADCs showcased, including HRS-4642 (KRAS G12D) and SHR-1826 (c-MET ADC)

Major business development deal: entered into a global strategic collaboration with BMS, with an upfront payment of USD 600 million and total potential milestones of USD 15.2 billion, covering 13 early-stage pipeline assets

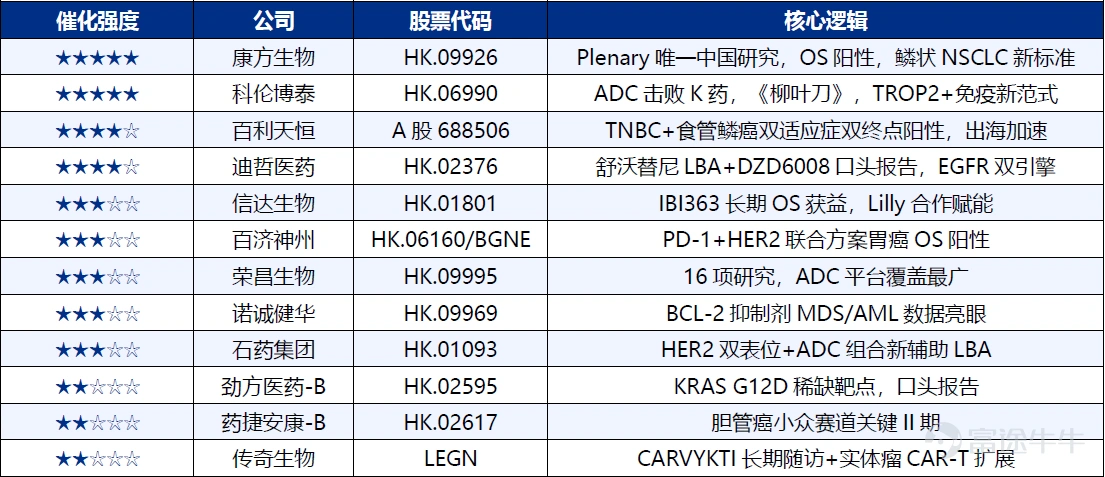

5. Key Stocks to Watch – Quick Reference Table

6. Other Hot Topics at ASCO

Most notably, Daraxonrasib demonstrated a doubling of overall survival (OS) in pancreatic cancer. The breakthrough of this RAS(ON) inhibitor lies in the fact that:Rather than targeting only specific mutations like G12C or G12D, it targets RAS proteins in their active state—logically covering over 90% of pancreatic cancer patients.This was the only dataset at ASCO to receive a standing ovation from the entire audience. RMMD.US: The standard second-line treatment for pancreatic cancer is about to be rewritten; FDA Expanded Access Program (EAP) is already open, with a clear NDA pathway. The global second-line PDAC market represents a $2B+ opportunity.

7. Recent Policy-Related Market Volatility

The entire innovative drug sector is currently under collective pressure, primarily due tointerest rate hikes and policy-related uncertainties in the biotech sectors of both China and the United States, with China more concerned about technology leakage and 'premature harvesting' of assets, while the U.S. is more focused on supply chain security in the biotech sector.

7.1. China’s Policies

Last week, news reports indicated that the Ministry of Commerce held meetings with certain pharmaceutical companies and may introduce new policies governing BD licensing for innovative drugs.If implemented, this would be bearish for small and mid-sized biotech firms—transactions between multinational corporations (MNCs) and Chinese biotechs would face an additional step requiring notification to and approval by China’s Ministry of Commerce, increasing transaction uncertainty.

However, the policy has not yet been formally enacted. It is expected to primarily target extreme cases involving core technologies—specifically, full transfers of a company’s entire patent portfolio (i.e., bundled transfers of entire technology platforms that prohibit the transferor from continuing development within China). The prevailing out-licensing model, which is primarily product-focused, would largely remain unaffected.

However, 'Ministry of Commerce approval'Once incorporated into the business development (BD) process, MNCs will incur higher waiting costs. Short-term caution is genuinely present in the market, posing liquidity risks for small and mid-sized biotechs that rely on upfront payments to stay afloat.

(1) Key technology areas affected

(2) Key transaction types affected

7.2. U.S. Policy

(1) COINS Act

Signed into law on December 18, 2025, as part of the FY2026 National Defense Authorization Act (P.L. 119-60), and now in effect.

Core rationale: This measure controls outbound U.S. capital flows and supersedes and upgrades the Biden administration’s Outbound Investment Security Program (OISP).It restricts U.S. persons and U.S.-controlled entities from investing in entities located in 'countries of concern' that operate in 'specified technology sectors.'

Covered transaction types:

① Equity acquisition (including convertible equity interests)

② Debt financing with equity-like features (profit-sharing, board seats)

③ Joint venture (JV) established with a subject of concern

③ Chinese ownership stake in a NewCo structure (e.g., involving specific technologies)

Outbound licensing (License-Out) is currently not covered: pure License-Out transactions—where a U.S. company pays upfront and milestone payments to a Chinese biotech for IP rights—do not constitute 'investment,' and the current text of the COINS Act does not cover them. However, clear pressure for expansion has emerged:

On May 12, BMS announced a $15.2 billion licensing deal with Hengrui Pharma. On May 21, House Select Committee on China Chairman John Moolenaar sent a letter to Treasury Secretary Bessent explicitly urging that biotechnology be added to the list of prohibited sectors under COINS.If biotech is added to Treasury regulations, all transactions involving 'U.S. capital investing in Chinese biotech' will be subject to controls. If enacted, while the policy would not directly block licensing deals, it would systematically depress valuations and financing capacity for Chinese biotech firms.

(2) CFIUS review

If the EO draft is signed and authorized transactions are subjected to CFIUS review, the closing timeline will stretch from weeks to months—or even face rejection—systematically disrupting the overseas expansion logic of Chinese biotech firms.The $15.2 billion BMS–Hengrui Pharma deal marks a watershed moment: Washington has already been pushing for 'decoupling and supply chain disruption' with China in recent years through tools like the Biological Security Act, and the sheer scale of this single transaction has sent political shockwaves through the U.S. system, ensuring that political resistance will only intensify.

More importantly, this transaction covers joint development of 13 early-stage innovative drug candidates in one go,signaling that top-tier U.S. pharmaceutical companies no longer view China as a 'bargain hunting ground for cheap pipelines,' but rather as a 'source of core original technologies.' This deep reliance on China’s foundational R&D capabilities has struck a raw nerve in U.S. political circles over 'supply chain sovereignty.'

(3) House Appropriations Committee FY2027 oral report (April 29, 2026)

The FY2027 FDA appropriations bill committee report proposes prohibiting the FDA from accepting, reviewing, or considering clinical trial site data from China, Russia, Iran, and North Korea to support IND applications.Crucially, the restricted data applies not only to the NDA/BLA stage but extends back to the earlier IND stage—meaning Phase I/II data packages themselves could not be used to file for U.S. clinical trials.

Once enacted into law, Chinese Phase I/II data would no longer support U.S. IND filings, fundamentally invalidating the 'Chinese data + U.S. development' model and forcing U.S. partners to restart Phase I trials from scratch in the United States—requiring a complete overhaul of BD valuation frameworks.

(4) Overview of U.S. policy risks

1️⃣ COINS Act (biotechnology expansion)

📍 Current status: Remains at the congressional letter → Treasury Department stage; no NPRM (Notice of Proposed Rulemaking) issued yet

⚖️ Nature/Impact: Requires multinational corporations (MNCs) to file declarations + case-by-case review (rather than a blanket prohibition)

2️⃣ CFIUS-reviewed authorized transactions (Executive Order draft)

📍 Current status: Draft leak has exceeded nine months; no signing to date

📊 Probability of passage: Approximately 25–35% chance of being signed into law within 2026

3️⃣ FY2027 Appropriations Report Language (Harris provision)

📍 Current status: Only a committee verbal report so far; not formal legislative text

📊 Probability of passage: Roughly 5–15% chance of being codified in appropriations law; if pursued via the NDAA route, approximately 30–40%

Summary: None of the three measures have been formally enacted. COINS leans toward declaration review, while near-term passage probabilities for both CFIUS and the Harris provision remain low—though continued monitoring is warranted.

[Investment Advisory Information]

Freya Sun | SFC Central Reference Number: BWS708

Risk Disclosure

This material is provided by Futu Securities International (Hong Kong) Limited. The data and referenced data are for reference only. Past performance of the relevant assets does not indicate future performance and cannot guarantee accuracy, completeness, or reliability. The content herein does not constitute investment, legal, accounting, or tax advice, has not taken into account any individual’s investment objectives, financial situation, or particular needs, and does not constitute any recommendation, invitation, offer, or solicitation to buy or sell structured products. Investors should note that structured products are unsecured; if the issuer or guarantor becomes insolvent or defaults, investors may not recover part or all of the amounts receivable. Prices of structured products can rise or fall sharply, and investors may suffer a total loss. Investors rely solely on the creditworthiness of the issuer and guarantor when purchasing these products. Callable bull/bear certificates (CBBCs) are subject to mandatory call mechanisms and may be terminated early, in which case (i) investors in Type N CBBCs will receive no payment, and (ii) the residual value of Type R CBBCs may become worthless. Investors should carefully review the listing documents (including any subsequent supplements) and supplementary listing documents regarding the relevant risks and details of the structured products and assess the risks independently. The products described on this page are structured investment products involving derivatives. They have not been authorized by the Securities and Futures Commission of Hong Kong ("SFC") for public offering in Hong Kong, are not intended for investment by the Hong Kong public, and are not protected by the Investor Compensation Fund. Investing in structured investment products is not equivalent to investing in their underlying reference assets. The structured investment products described herein may not be listed or may lack an active or liquid secondary market. Investors assume the credit and insolvency risks of the issuer, guarantor, and/or other identified counterparties, as applicable. Investors should also note that the issuer may terminate the investment early. Investment involves risk, and investors should act prudently with respect to these products and fully understand that they may lose their entire investment. Before making any investment decision, investors should carefully read and fully understand the offering documents and terms and conditions (including the risk disclosures contained therein) relating to the relevant investment products and should not base their decision to invest in structured products solely on the content herein. Where necessary, investors should seek appropriate professional advice.

General Disclaimer

The author(s) of this report are licensed by the Securities and Futures Commission of Hong Kong. The analyst(s) and/or their associates do not hold any financial interest in the listed corporations covered in this research report. This report is prepared by Futu Securities International (Hong Kong) Limited (“Futu Securities”). By receiving and/or viewing this report (including any attachments), the recipient acknowledges and warrants that they are entitled to receive this report under the conditions set forth below and agrees to be bound by the restrictions contained herein. Any failure to comply with these restrictions may constitute a breach of applicable laws. Without prior written consent from Futu Securities, neither this report nor any information contained herein may be (i) reproduced, copied, or stored in any form, or (ii) distributed or transmitted directly or indirectly to any other person for any purpose. Futu Securities shall not be liable for any direct or indirect losses arising from the use of the materials contained in this report. The information in this report is derived from sources believed by Futu Securities to be accurate and reliable at the time of publication. However, this report is not intended to include all information necessary for investor decision-making and may be affected by delays, obstructions, or interceptions in transmission. Futu Securities makes no express or implied representation or warranty regarding the adequacy, accuracy, completeness, reliability, or fairness of any such information or opinions. Accordingly, Futu Securities and its affiliates (collectively, the “Futu Group”) shall not be liable for any losses of any kind (including, without limitation, direct, indirect, or consequential losses) arising from any actions taken by third parties in reliance on the content of this report.

The content, products, and services described in this report are intended solely for users in the Hong Kong Special Administrative Region and are provided for general circulation only. They do not constitute an offer or solicitation to buy or sell any investment product. This report does not take into account any individual’s specific investment objectives or financial circumstances. Individual investors should seek independent financial advisory or professional advice and refer to the relevant ETF offering documents and/or other latest published materials, including risk factors concerning the suitability of specific investment products. Data included in this report is sourced from publicly available information, which the analyst believes to be reliable. All investments involve risk, and investors may lose their entire invested capital. Past performance, estimates, forecasts, or simulated results do not necessarily indicate future performance of any investment. The ETFs referenced herein have not been and will not be authorized by the Securities and Futures Commission of Hong Kong under Section 104 of the Securities and Futures Ordinance. This report does not constitute, under Section 103 of the Securities and Futures Ordinance, an advertisement, invitation, or document inviting the Hong Kong public to acquire interests in or participate in a collective investment scheme.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

2