AI infrastructure is heating up! Hardware stocks rally across the board

From supporting role to essential component: How do MLCCs power AI computing?

I. Industry Definition and Global Landscape (00:00 ~ 04:00)

MLCCs (Multilayer Ceramic Capacitors), known as the 'rice of the electronics industry,' are passive components offering high capacitance, small size, high-voltage tolerance, and operation above 105°C. In the AI era, their role has fundamentally evolved—from ordinary passive components to critical elements ensuring power integrity.

Foreign institutions began recommending Japanese capacitor stocks in 2024, but investor interest remained muted due to demand not exceeding expectations; however, NVIDIA’s GTC conference reignited demand expectations following broader adoption forecasts for rack-level solutions.

🔍 Global Market Landscape:

$Murata Manufacturing (6981.JP)$ Market share over 41%, $Samsung Electro-Mechanics (009150.KR)$ Approximately 20%, $Taiyo Yuden (6976.JP)$ Approximately 10%,

Mainland Chinese MLCC manufacturers hold less than 10% of the global market share, placing them in the third tier.

Demand has surged by an order of magnitude, while supply-side capacity has been heavily absorbed by high-end products, resulting in uneven industry prosperity—this explains why some are talking about it in '24 but the real speculation won’t start until '26.

💡 Core view: The more concentrated the market share, the higher the industry barriers and the clearer the visibility on gross margins.

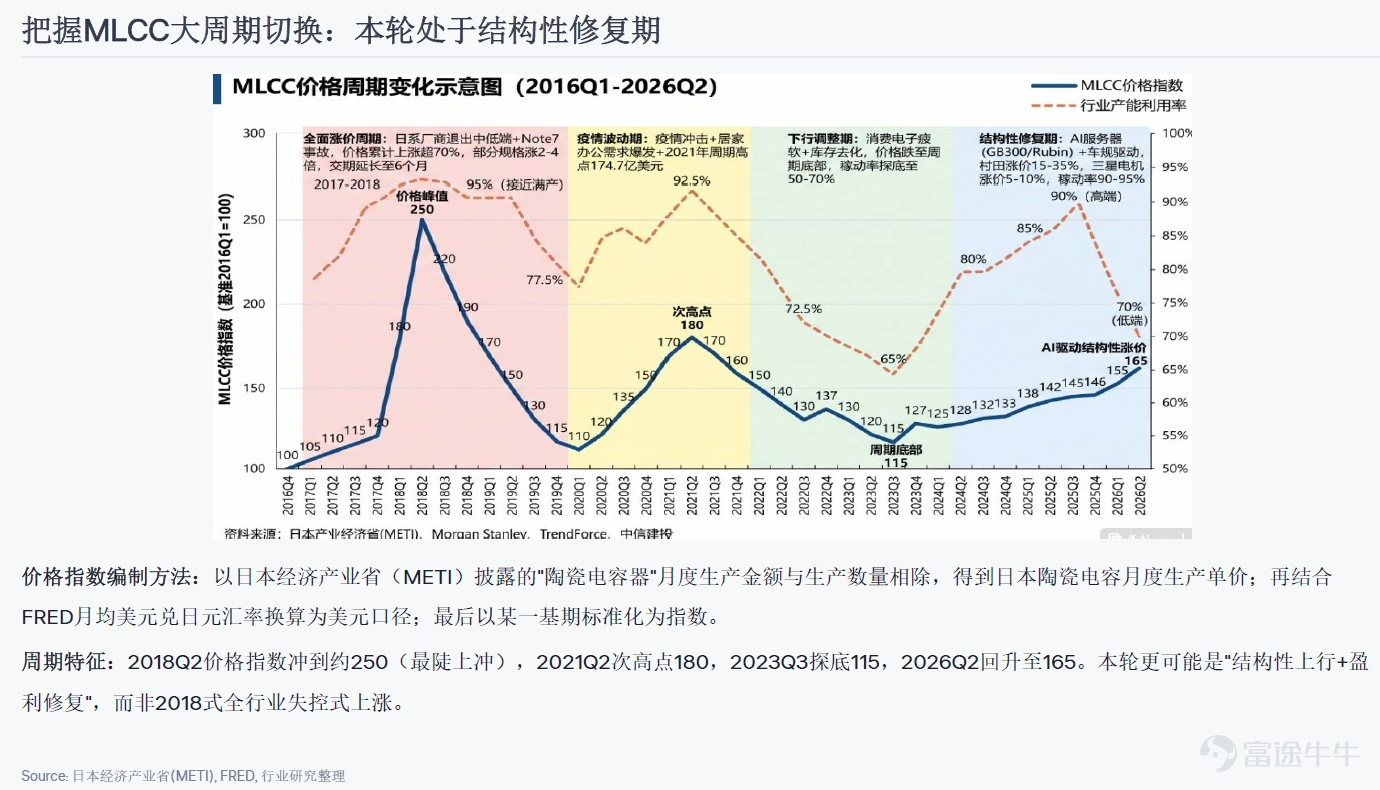

II. Price Cycle Stage: Early Phase of Profit Recovery (12:00 ~ 16:00)

The price index (converted into USD based on Japan's monthly ceramic capacitor output/value and production volume) indicates that current industry capacity utilization is around 70% (nearing 90% at peak), with the price index still at a low level.

Core assessment: The industry remains in the early stage of structural profit recovery, with further momentum ahead. The current price increase is not driven by general consumer demand, but by the expanding demand for high-capacitance, high-voltage, and high-temperature-resistant products.

Logical analogy:MLCCs could follow a similar trajectory as high-end memory (HBM), transitioning from cyclical stocks back to growth stocks.

III. Three Key Drivers of Price Transmission (16:00 ~ 22:00)

Structural price increasesDriven by upgrading demand, amplified through power delivery architecture and product specifications, and further reinforced by constraints in materials and capacity.

Driver One – Rising Power: GPU TDP has increased from approximately 700W for H100/H200 → ~1000W for GB200 → ~1400W for GB300 → 1800–2300W in the Rubin era, directly raising requirements for power supply stability.

Driver Two – Power Delivery Architecture: Shift toward 400V/800V HVDC, which further amplifies demand for high-voltage, high-frequency decoupling.

Driver Three – Triple Inflation: Simultaneous upgrades in unit count, capacitance value, and specifications, coupled with limited PCB area, are forcing a shift toward 'higher capacitance in smaller form factors'—the most direct driver behind ASP increases.

Four factors supporting sustainability: continued rise in power density, high-capacitance mix yet to peak, supply lagging demand, and rare earth export controls plus reliance on Japanese equipment.

IV. Key Company Analysis

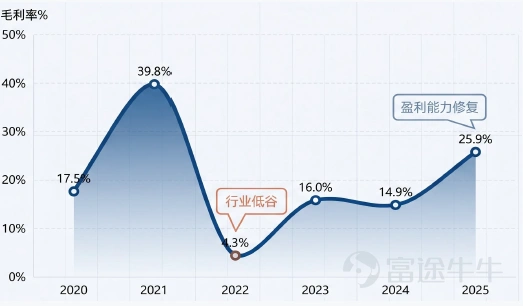

MLCC accounts for approximately 50% of total revenue, with a profit margin of around 27% (about 15 percentage points higher than other business segments).

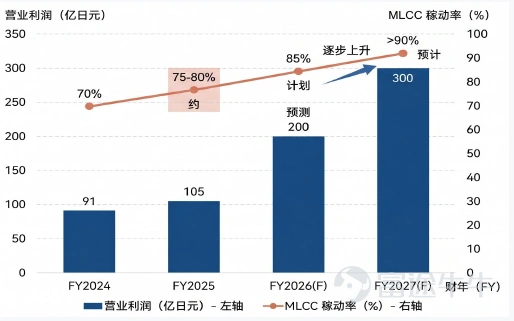

Average capacitor selling prices are expected to increase by 5–10% in fiscal year 2026, with data center MLCC revenue projected to grow 85–90% year-over-year.

Core thesis: High visibility, leading competitiveness, and poised to capture a dominant share of the premium market. Expansion from AI servers into edge and physical AI will fully leverage its advantages in miniaturization and lightweight design.

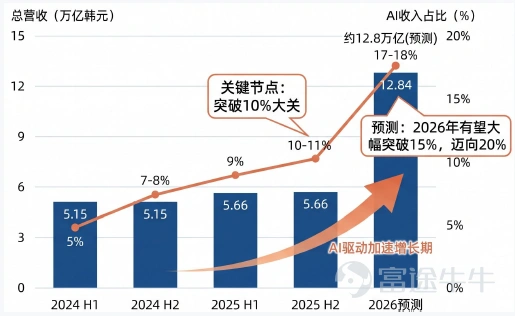

AI revenue contribution: 7–8% in 2024 → over 10% in H2 2025 → projected to reach 17–18% in 2026

High-end MLCC market share increased from 20% to 30%; Q1 2026 capacity utilization above 90%

Core thesis: Dual drivers of MLCC and FC-BGA, rapidly rising AI revenue contribution, and silicon capacitor technology poised to upgrade the product portfolio.

MLCC accounts for approximately 70% of revenue—the highest concentration globally, ranking third worldwide (with roughly 10% market share)

FY26 AI server MLCC sales expected to grow ~30% YoY, potentially accelerating to 80–85% growth in FY27–FY28

Core thesis: Highest earnings elasticity during price-up cycles or AI/automotive demand surges. Conservative capex, tight supply-demand balance, and high utilization rates will more readily translate into profit upside.

US-listed ADR: $Taiyo Yuden (ADR) (TYOYY.US)$

Its core asset is YuYang Technology, a wholly owned subsidiary and China's fourth-largest MLCC manufacturer, ranking among the top ten globally

Focuses on high-end, miniaturized mid-to-high capacitance MLCCs; its AI-related products have already entered Huawei’s server supply chain

Core thesis: A rare play in the Hong Kong market with strong inherent elasticity, though accompanied by higher risk and volatility.

Overall positioning: Murata and Samsung Electro-Mechanics offer stronger certainty; Taiyo Yuden and Tainet Holdings provide greater upside potential but also higher volatility.

V. Selected Q&A

Q: Are Japanese MLCC companies significantly impacted by China Rareearth export restrictions?

A: The impact exists but is practically limited. Rare earth elements account for only about 1% of MLCC formulations, representing a low cost component that can be absorbed; leading Japanese and Korean firms maintain safety inventories of over six months; and they are accelerating sourcing from alternative channels such as Australia, the U.S., and Vietnam. More importantly, China still relies on Japan for key high-end manufacturing equipment, creating a mutual check between the two sides.

Q: How long is this current wave of price increases expected to last?

A: It will take at least 1.5–2 years to ramp up new high-end capacity. Market demand for high-end MLCCs is expected to remain robust through the end of 2027. Driven by three overlapping demand factors—server rack upgrades, rising MLCC content per electric vehicle, and scaling robotics supply chains starting in the second half of this year—and underpinned by the duopoly of Japanese and Korean suppliers, the sector's favorable conditions are conservatively projected to span 2026–2027. Expectations for Q3 and Q4 of this year may see upward revisions, potentially extending the tailwind beyond 2028.

The above content is for reference only and does not constitute investment advice. Feel free to share your views in the comments section!

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (6)

to post a comment

13

21