AMD and Meta have joined forces to secure a major chip order

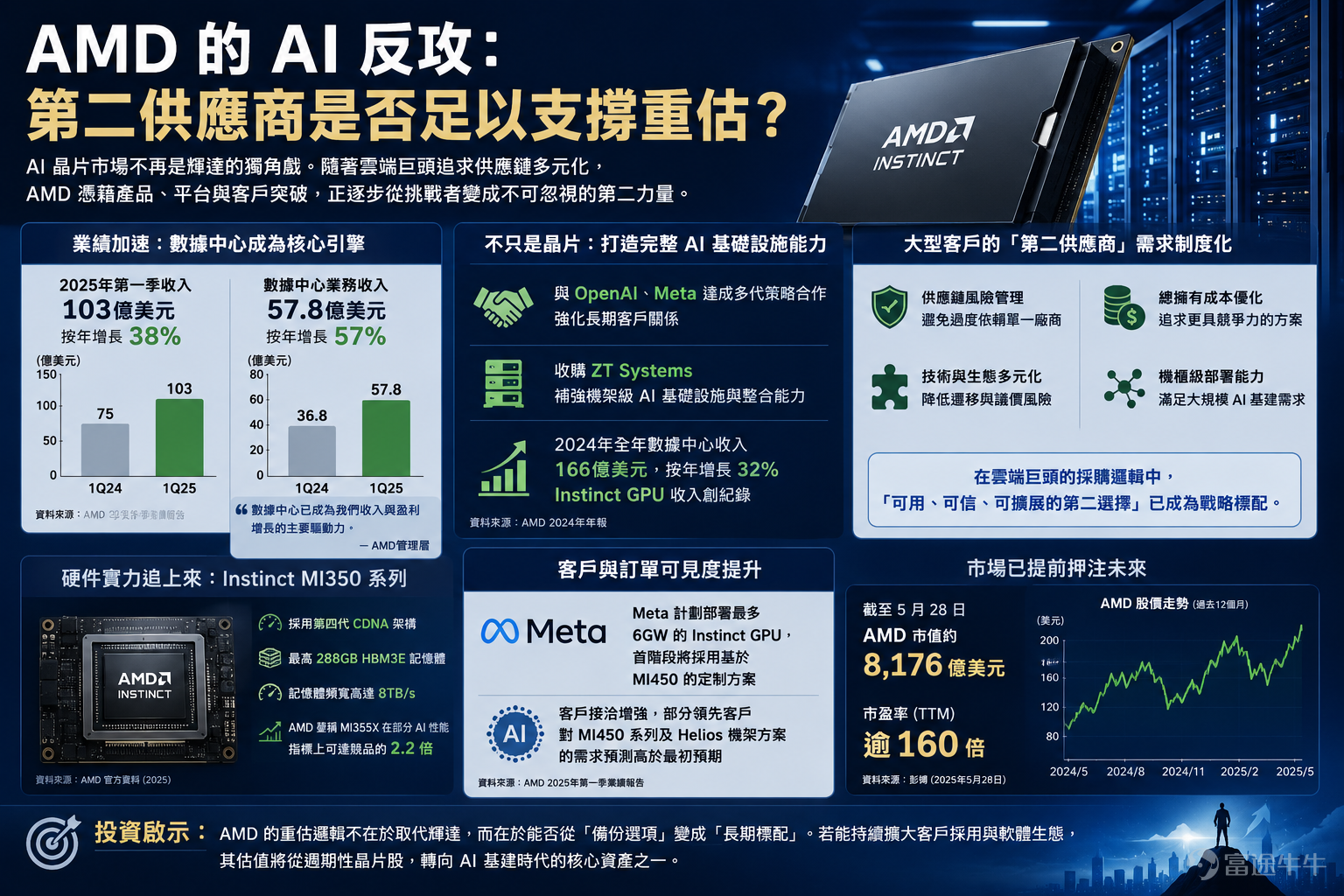

AMD's AI Counteroffensive: Is Being the Second Supplier Enough to Justify a Re-Rating?

Over the past two years, the AI chip market has largely been seen as NVIDIA’s one-man show, with AMD often relegated to the role of a 'promising challenger.' But today, the market is beginning to ask anew: as large cloud service providers and model companies grow increasingly reluctant to place their entire supply chain bets on a single vendor, has AMD’s strategic value as a second supplier become sufficient to support a new round of valuation re-rating? Judging from its latest results, this question is no longer abstract. AMD reported Q1 revenue of $10.3 billion, up 38% year-over-year; data center revenue reached $5.78 billion, a 57% year-over-year increase. Management explicitly stated that the data center segment has now become the primary driver of both revenue and profit growth. This signals that AMD’s narrative is shifting from traditional PC and server chips toward an AI infrastructure platform. The market is re-rating the stock precisely because AMD is no longer merely 'playing catch-up'—it is now securing a more substantial foothold within the AI capex cycle.

What truly gives AMD a chance to turn things around isn’t the market’s belief that it can comprehensively defeat NVIDIA, but rather the fact that hyperscale customers are institutionalizing their demand for a 'second supplier.' In the AI era, procurement logic goes beyond raw per-card performance—it now encompasses supply reliability, total cost of ownership, software migration complexity, rack-level deployment capabilities, and bargaining leverage. For large customers, maintaining a viable, credible, and scalable second option in itself carries strategic value. AMD’s role is becoming critical in this gap. According to the company’s 2025 annual report, data center revenue grew 32% year-over-year to $16.6 billion, with record-breaking Instinct GPU sales. AMD also announced multi-generational strategic collaborations with OpenAI and Meta, and completed its acquisition of ZT Systems to strengthen its rack-scale AI infrastructure capabilities. These moves signify that AMD is no longer just selling chips—it is now building out full-stack AI system delivery capabilities.

Can It Transition from Backup to Standard?

From a product specification standpoint, AMD has already delivered hardware that substantiates market expectations. The Instinct MI350 series, based on the fourth-generation CDNA architecture, offers up to 288GB of HBM3E memory and 8TB/s bandwidth. AMD claims the MI355X achieves up to 2.2x the performance of competing products on certain AI benchmarks. Even if such comparisons carry vendor bias, they at least demonstrate that AMD’s hardware capabilities are no longer out of reach. More importantly, Lisa Su noted in the earnings call that customer engagements for the upcoming MI450 series and Helios rack solutions are intensifying, with demand forecasts from leading clients exceeding initial expectations. AMD also disclosed that Meta plans to deploy up to 6GW of Instinct GPUs, with the initial phase using a custom solution based on the MI450. For capital markets, what truly drives re-rating isn’t one or two product launches, but the order certainty created by a clear roadmap, firm customer commitments, and deployment visibility.

However, being the second supplier does not automatically translate into a high valuation. The core moat in the AI chip market has never been solely about hardware—it lies in software, ecosystem, and developer habits. NVIDIA’s hardest-to-replicate advantage isn’t peak product performance, but rather the CUDA ecosystem, system integration capabilities, and the stickiness of customers’ existing workflows. AMD has recently emphasized its open, royalty-free enterprise AI software stack, hoping to attract enterprise and cloud customers with lower costs and a more open architecture—but this path remains long. The market will assign AMD a higher valuation only if it proves it is not merely a temporary beneficiary of 'backup orders,' but a structural player capable of sustainably capturing a meaningful share of the AI accelerator market over the long term.

In other words, whether AMD deserves a re-rating hinges not on 'whether there is a second-supplier rationale,' but on whether this rationale can be translated into a sustainable profit model. If AMD only captures overflow demand during supply shortages, its valuation ceiling will remain limited. But if large customers begin incorporating AMD into long-term procurement frameworks and consistently expand its usage across training, inference, and rack-level deployments, the market will gradually reclassify AMD from a 'cyclical semiconductor stock' to a 'core AI infrastructure asset.' As of May 28, AMD’s market cap stood at approximately $817.6 billion, with a price-to-earnings ratio exceeding 160x—indicating that capital markets have already priced in a degree of optimistic expectations.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment