Nearly RMB 30 billion in losses over 90 days, the food delivery battle cools down

Source | Tech Planet

Text| Lin Jing

Major Chinese internet companies are stepping back from the subsidy-fueled food delivery battle.

On June 1, Meituan released its Q1 2026 financial results, reporting RMB 64.1 billion in revenue from its core local commerce segment and an operating loss of RMB 2 billion, a significant improvement compared to the RMB 10 billion loss in Q4 2025.

In the same reporting period, JD.com’s new business segment—which includes food delivery—reported a loss of RMB 10.4 billion, down from RMB 14.8 billion in Q4 2025. Taobao Flash Delivery narrowed its losses from RMB 22–23 billion last quarter to RMB 17–18 billion, cutting its losses by over RMB 10 billion.

Roughly calculated, in just one quarter, the combined losses of these three tech giants amounted to at least RMB 29.4 billion. Although their losses have significantly narrowed, the food delivery war remains a key factor impacting the financial performance of these major internet companies. After a year of aggressive subsidy-driven competition, merchants, riders, and consumers are now experiencing noticeable changes.

Higher commissions for merchants, declining order volumes for riders

Since the beginning of this year, merchants in provinces such as Anhui, Jiangsu, and Guangdong have started reporting increases in commission rates and delivery fees charged by food delivery platforms.

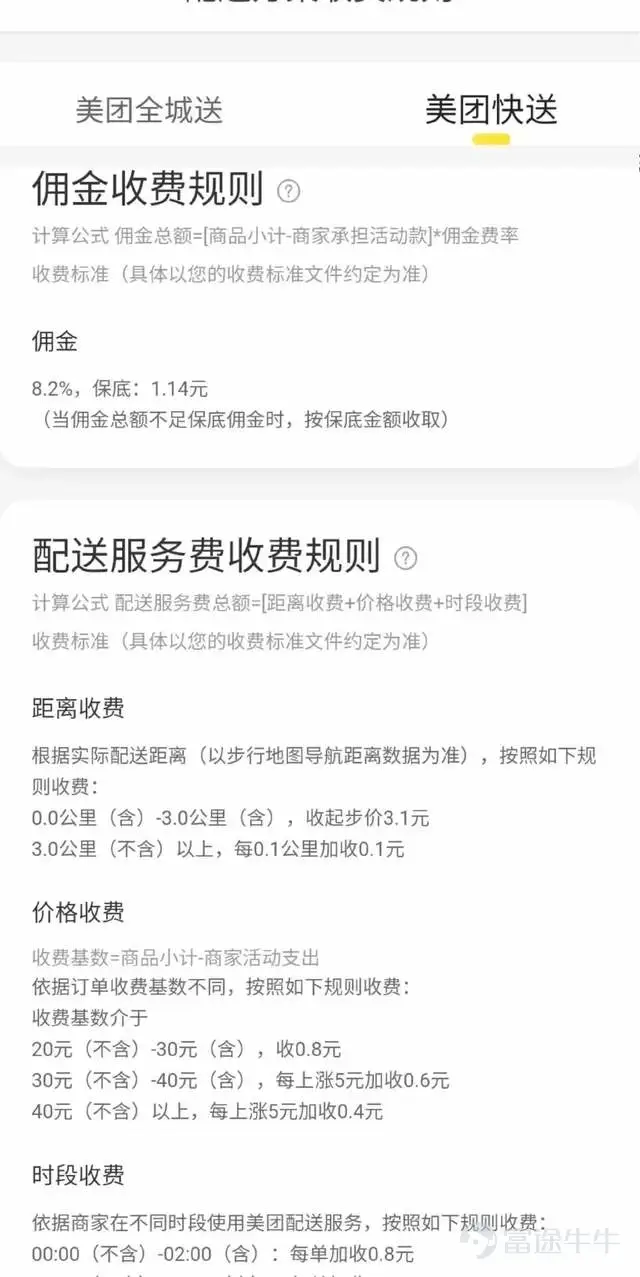

Lao Zhang, a merchant who operates a noodle and rice noodle shop, told Tech Planet that in his new contract received in April this year, both the 'time-based fee' and 'distance-based fee' under 'delivery service charges' had increased. For example, the per-order fee for deliveries between 21:00 and 23:59 rose from RMB 0.5 to RMB 1, and the distance-based fee for deliveries within 3 kilometers also increased by RMB 0.1 per order.

According to Lao Zhang, his previous contract applied a flat commission rate of 23%. The new contract shifted to an 8% commission plus separate 'time-based' and 'distance-based' fees. Although the headline rate appears lower, the fixed base charge for orders starting at 2.5 kilometers alone amounts to RMB 2.8 per order. Taking a typical RMB 15 meal delivered within 3 kilometers as an example, the total commission and delivery service fee under the new contract is approximately RMB 0.6 higher per order. Overall, despite the structural change, the effective cost to merchants remains around the original 23% rate.

The commission calculation rules for food delivery platforms are relatively complex and vary across cities. Commissions also fluctuate due to factors such as pricing, distance, weather, and whether orders are self-delivered, delivered by the platform, or handled by third-party logistics providers. In some non-direct-operated cities managed by agents, there have been instances where agents unilaterally raised commission rates for merchants.

Mr. Zhang’s store is listed on three platforms—Meituan, Taobao Flash Delivery, and JD.com. According to him, the combined commission and delivery fees on the first two platforms generally hover around 23%, while JD.com’s food delivery service has shifted from its initial zero-commission model to charging approximately 5.6% plus a fixed RMB 3 delivery service fee.

He explained that although JD.com’s commission rate is lower, order volume is relatively small. Some merchants choose to ‘keep their listings active and accept orders if they come in,’ while others, constrained by limited capacity and aiming to reduce labor and other operational costs, opt to deactivate their listings. He and other merchants also share the perception that JD.com’s food delivery team experiences more frequent personnel changes—for instance, the city manager assigned to his area was replaced three times within a single month.

In recent earnings calls, Meituan, Alibaba, and JD.com have shifted their focus for their food delivery businesses from emphasizing market share to highlighting improvements in unit economics (UE). UE is a core metric that measures whether the platform makes or loses money on each delivered order, and profitability recovery has become the central theme for the food delivery industry heading into 2026.

Caption: Meituan Direct Delivery commission and delivery service fees, provided by interviewees

Beyond raising commissions and delivery fees, food delivery platforms have also adjusted their promotional strategies, including discount thresholds, red envelope multipliers, exclusive coupons, and ‘hundreds-of-billions’ subsidy campaigns. Some merchants report that many small and medium-sized restaurants lack sufficient online operational capabilities—due to unfamiliarity with cancellation procedures or backend system limitations—which enables regional managers to enroll merchants in promotions without consent or add high-value red envelope offers.

A bakery owner told Tech Planet that compared to the early days of the food delivery wars—when platforms and merchants each covered roughly 50% of promotional costs—merchants now bear a significantly larger share.

The food delivery wars have also left lasting repercussions on the industry. A large number of merchants who previously did not offer delivery services were involuntarily drawn into the competition and now must confront new challenges stemming from strategic shifts by platforms. The number of delivery riders has surged dramatically, rapidly transitioning the sector from a state of 'delivery capacity shortage' to one of 'delivery capacity saturation.'

A UBS Group research report published on March 12, 2026, indicated that as of February 2026, the combined daily order volume across JD.com, Taobao Flash Delivery, and Meituan totaled approximately 110 million orders. Currently, China has nearly 20 million instant delivery riders, yet only about 4 million skilled riders are needed to support the current daily order volume of 110 million. This implies that over 16 million riders represent excess capacity generated by the delivery wars.

A Meituan Direct Delivery rider in Beijing told Tech Planet that his average daily order volume has dropped from 60 last year to 50. This decline stems not only from the cooling of the food delivery wars and an overall dip in demand but also from continued growth in rider numbers, which further fragments order allocation. Despite this, the rider revealed that his station has not halted recruitment and will not downsize. Stations must maintain ample delivery capacity to handle potential order surges during extreme weather events such as heatwaves or heavy rainstorms.

Reduced losses and stemmed the bleeding, but food delivery continues to drag down profitability

The food delivery battle began in February 2025 and intensified during the summer peak season in July, as platforms like JD.com and Taobao Flash Delivery entered the market with commission reductions and large cash subsidies. Meituan responded throughout the summer with defensive promotions such as 'Free Drinks' and 'Super Coupon Boosts.'

Meituan, Taobao Flash Delivery, and JD.com collectively burned through hundreds of billions of yuan in subsidies, directly impacting their financial results: Meituan reported a full-year net loss of RMB 23.4 billion in 2025, JD.com’s new businesses posted a loss of RMB 46.6 billion, and Alibaba’s instant retail segment suffered an even steeper loss of RMB 87 billion.

By Q1 2026, although losses from new businesses—including food delivery—narrowed sequentially, food delivery remained a key profit drainer. Moreover, the erosion of revenue by subsidies was evident, with Meituan’s Core Local Commerce segment reporting only a marginal 0.1% year-over-year increase in revenue, reaching RMB 64.1 billion this quarter.

In terms of total revenue, Meituan generated RMB 91 billion this quarter, up 5.6% year-over-year, but reported an adjusted net loss of RMB 4.97 billion. In contrast, the company had posted a net profit of RMB 10.95 billion in the same period last year, marking a shift from profit to loss on a year-over-year basis.

During the earnings call, Meituan Chairman and CEO Wang Xing stated that the company is gradually reducing subsidy spending while reinforcing its leadership position in the medium-to-high average order value (AOV) segment. If industry competition remains at its current, more rational level, he expects unit economics to improve significantly in Q2, supported by seasonal tailwinds.

Wang Xing also emphasized during the earnings call that Meituan is continuously widening its unit economic model advantage over competitors. However, the extent of improvement in unit economics (UE) in the second half of the year will still depend, to some degree, on how the competitive landscape evolves.

Meituan’s sales and marketing expenses surged 51.1% year-over-year this quarter to RMB 23 billion, increasing as a share of revenue from 17.6% to 25.2%.

Despite persistently high marketing costs, all three internet giants have seen some pullback this quarter compared to the peak of the food delivery war. For example, JD.com’s marketing expenses in Q1 2026 were RMB 15.37 billion, down nearly 50% from the RMB 27.01 billion spent during the height of the food delivery battle in Q2 2025.

Moreover, as early as Q3 2025—while Alibaba and Meituan were still ramping up subsidies—JD.com had already begun proactively scaling back its investment in food delivery, becoming the first to exit the subsidy war. Its marketing expenses had already declined 22% quarter-over-quarter to RMB 21.1 billion.

Multiple third-party research reports have disclosed market share data for the three players. According to JPMorgan’s November 2025 survey data, calculated by order volume, Meituan holds 50%, Taobao Flash Delivery 42%, and JD.com 8%—a ratio closely aligned with UBS Group’s order-volume-based figures, maintaining an approximate '5:4:1' market structure.

During earnings conference calls over the past few quarters, both Wang Xing, Chairman and CEO of Meituan, and Jiang Fan, CEO of Alibaba’s e-commerce business group, have repeatedly referenced market share, stating their aim to 'achieve a leading market position.'

Currently, JD.com is gradually shifting its narrative focus in food delivery toward its Seven Fresh Kitchen initiative. Meanwhile, Alibaba, due to its continued heavy investment in AI, has had its resource allocation to food delivery somewhat constrained. As a result, all three platforms have now entered an operational phase centered on unit economics (UE) recovery.

From the consumer perspective, chain brands offering new-style tea drinks, fried chicken, and similar items priced around RMB 15—once frequent participants in the food delivery wars—have significantly raised their takeout prices. Looking at user discount coupons across the three platforms, although JD Daojia still offers promotions like 'RMB 5 off orders over RMB 6,' these require minimum order values ranging from RMB 20 to RMB 25, and many high-value coupons are restricted to new users only.

Compared to heavily subsidized low-priced delivery, merchants are now more frequently encouraged to participate in various low-price meal programs. Meituan has launched products like 'Pin Hao Fan' and 'Shen Qiang Shou' targeting budget orders, while Taobao Flash Delivery has introduced comparable offerings such as 'Bao Pin Tuan' and 'Chao Qiang Shou.' Merchants offer low-priced meal sets to secure fixed revenue, adopting a high-volume, low-margin strategy.

One key challenge for these special-offer food delivery channels is attracting more chain brands to enrich their supply side and enhance user appeal and trust.

However, a franchisee of a chain brand told Tech Planet that participation in such campaigns is centrally managed by headquarters, leaving franchisees without authority to modify terms. The franchisee added that while revenue per low-priced order is fixed, they are often reluctant to join: 'For example, if a customer orders a drink—whether they pay RMB 13 or RMB 15—we receive a fixed amount of just RMB 7–8. But our material costs are too high. Each delivery order requires a separate receipt, a sealed sticker, and designated packaging bags and cups. These costs more than double compared to in-store purchases; packaging that used to cost just over RMB 1 now costs RMB 2–3. For stores, chasing volume alone makes no sense—it’s actually losing money. But for headquarters, they can continuously procure raw materials at scale.'

The smoke of the food delivery battle is clearing, but the market landscape remains unsettled. Platforms are stepping back from aggressive subsidy-driven growth and shifting toward reducing losses and improving efficiency. While scaling back subsidies, they are also carefully managing to prevent any decline in consumer-side experience. Caught in the middle, merchants continue to face ongoing turbulence amid evolving platform rules and product iterations.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment