AI infrastructure is heating up! Hardware stocks rally across the board

Trump and Jensen Huang both express strong optimism! Legacy hardware giant sees post-earnings 'soaring rally'—how to seize the investment opportunity?

Recently, a “surge myth” led by the traditional hardware sector is unfolding in the U.S. stock market. Once seen as legacy hardware manufacturers with limited growth elasticity, these giants are now undergoing a dramatic revaluation amid the AI wave:

$LENOVO GROUP (00992.HK)$ : After reporting strong earnings on May 22, its share price surged throughout the following trading week,with cumulative gains exceeding 101% (hitting multiple all-time highs intraday).

$HP Inc (HPQ.US)$ : Following its earnings release on May 27, driven by recovering PC demand and AI-endpoint concepts,its stock rose more than 20%.

$Dell Technologies (DELL.US)$ : Reported earnings after U.S. market close on May 28; boosted by strong AI orders and upbeat profit guidance,the stock soared over 30% intraday, continuing its rally to gains of over 50%.

$Hewlett Packard Enterprise (HPE.US)$ In the Q2 earnings released on June 1, revenue increased by 40% year-over-year,After-hours share price surged strongly by over 28%.

Why have these former traditional hardware giants been able to unleash such remarkable upward momentum in such a short time? This is no coincidence—it is the inevitable result of earnings realization, cyclical recovery, and surging AI demand working in tandem.

The recent concentrated surge in share prices owes much to two key influential figures:

Dual support from policy and major contracts:On May 8, Trump publicly urged during a White House event: 'Go out and buy Dell computers! They’re great!' Shortly afterward, on May 29, the U.S. Department of Defense announced a five-year, approximately $9.7 billion contract with Dell for Microsoft software supply and services. This substantial, tangible order significantly bolstered market confidence in the hardware giant's supply chain.

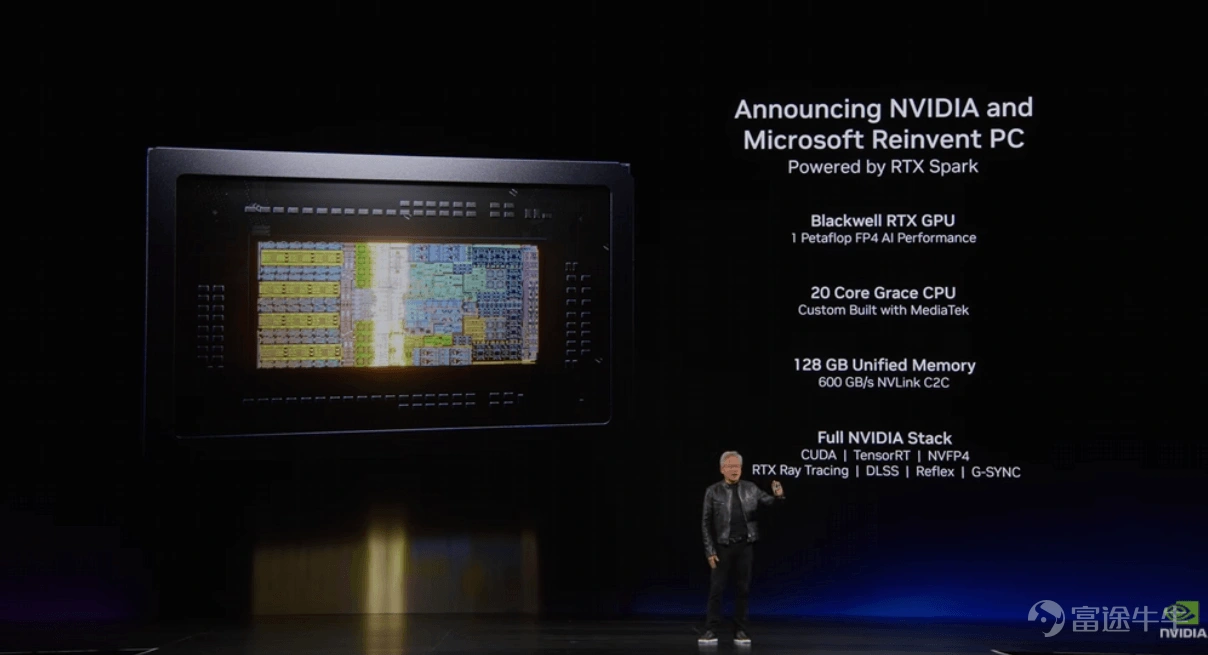

NVIDIA reshapes the PC industry landscapeAt the 2026 Taipei Computer Show, NVIDIA CEO Jensen Huang made a major announcement entering the consumer PC chip market, partnering with Microsoft to launch the 'RTX Spark Super Chip,' specifically designed to run local AI agents. This move not only has the potential to break Intel and AMD’s decades-long duopoly in the Windows PC market but also triggers the most profound value restructuring in the PC supply chain since its inception. $Dell Technologies (DELL.US)$ 、 $LENOVO GROUP (00992.HK)$ 、 $HP Inc (HPQ.US)$ are all among the first batch of partners to integrate RTX Spark, immediately positioning themselves at the forefront of this new trend.

Celebrity endorsements, large orders, and AI technology iterations serve as powerful 'catalysts,' while the company's recent robust financial results and the cyclical upturn in its industry have injected a strong 'shot in the arm' into the market.

1. Earnings Surpassing Expectations: Revenue Soars, Profits Double

In the AI infrastructure space, the irreplaceable value of hardware giants in system integration and delivery has been strongly validated by the market, with each company delivering exceptionally impressive results:

$Dell Technologies (DELL.US)$ : Q1 revenue surged 88% year-over-year, and net profit skyrocketed by 256%. In its core AI server segment, quarterly revenue exploded by 757% year-over-year to $16.1 billion, with AI-related backlog orders already piling up to $51.3 billion, demonstrating exceptional order visibility.

$Hewlett Packard Enterprise (HPE.US)$ : Quarterly revenue hit $10.7 billion, up 40% year-over-year—the largest earnings beat since 2018. Its core server business revenue jumped 32.7% year-over-year to $5.45 billion, with traditional server orders surging by triple-digit percentages.

$LENOVO GROUP (00992.HK)$ : The company’s transformation has reached a qualitative inflection point, with full-year revenue hitting $83.1 billion, up 20% year-over-year, and Q4 revenue reaching $21.6 billion, up 27% year-over-year. The standout development is that its Infrastructure Solutions Group (ISG) achieved profitability for the first time ever, and AI-related revenue now accounts for 38% of total company revenue. AI server order backlog at quarter-end soared to $21 billion.

$HP Inc (HPQ.US)$ : Q2 revenue reached $14.4 billion, up 6.9% year-over-year, exceeding analyst expectations, prompting an upward revision to its full-year earnings guidance. Driven by both the Windows 11 upgrade cycle and growth in AI PCs, its core Personal Systems business saw strong growth, with PC segment revenue rising 13% year-over-year to $10.25 billion.

2. Industry Cycle Recovery: A Compulsory Refresh Wave in Core Traditional Businesses

Beyond the explosive order growth driven by AI-related businesses, the upturn in the traditional hardware industry cycle is another key factor pushing stock prices higher.

In recent years, impacted by macroeconomic headwinds and slowing enterprise IT spending, traditional PCs and general-purpose servers underwent a prolonged inventory drawdown and downturn cycle. However, the situation is now reversing:

1. Recovery in Traditional Servers: After sustained inventory drawdown across the global PC industry, cyclical recovery is underway, driven by strong, inflexible demand from both enterprises and consumers to replace and upgrade aging servers.

2. AI PC Replacement Cycle: With the explosive emergence of on-device large AI models, high-compute AI capabilities have become essential, triggering a new wave of PC replacements centered around AI-capable devices.

This dual dynamic—bottoming out and recovery in core legacy businesses combined with explosive growth from AI-driven new demand—has significantly boosted market expectations for hardware companies’ growth prospects. Institutions have collectively raised target prices, further fueling share price appreciation.

III. Core Catalyst: The AI Compute Revolution Reshapes Industry Fundamentals

If earnings and cyclical recovery explain 'today’s surge,' then the ongoing evolution of AI demand outlines 'the future opportunity.'

Looking further ahead, global hardware giants are leveraging this inflection point to undergo a transformative shift—from 'cyclical hardware stocks' to 'high-growth technology stocks.'

Infrastructure (AI Servers) Enters Its Golden EraThe iterative advancement of trillion-parameter large AI models and deep enterprise-level AI transformation have spurred explosive growth in computing clusters. AI servers and high-speed storage devices have become essential core infrastructure for enterprises. Vendors such as Dell and Lenovo, leveraging their system-level integration capabilities, robust engineering delivery, and strong customer stickiness, have gained an early advantage in both concentrated procurement by cloud giants and on-premises enterprise deployments.

Terminal devices (AI PCs) are undergoing a profit re-ratingAI technology is comprehensively advancing into terminal devices. AI PCs, powered by on-device large models, ultra-fast response times, and strong privacy protection, are injecting new momentum into the sluggish PC market. Market forecasts predict that by 2027, global AI PC penetration will exceed 50%, driving a surge in premium device shipments and potentially triggering a significant boost in profitability and gross margins for PC manufacturers.

The 'Matthew Effect' in the supply chain is becoming increasingly pronouncedAI hardware imposes stringent requirements on high-end chips, memory, advanced cooling solutions, and other components, significantly raising supply chain barriers for market leaders who possess strong resource integration capabilities and production capacity advantages.

As the new era of AI PCs enters its phase of broad industry adoption, the cyclical principle of 'hardcore infrastructure first' remains firmly applicable.

Dell's management emphasized that current AI demand shows no signs of slowing down, with a backlog of $51.3 billion in orders already laying a solid foundation for high growth over the next 1–2 years.As global enterprises accelerate their AI transformation strategies, demand for AI servers and storage equipment will remain robust. Investors should pay close attention to the following areas:

In computing infrastructure, server giants with fully loaded order backlogs, exceptional mass-production capabilities, and deep strategic alliances with leading chipmakers will undoubtedly be the first beneficiaries;

In the end-user market, top-tier suppliers spearheading next-generation AI PC development—alongside the processor and high-frequency memory supply ecosystems—will jointly dominate market influence.

Moreover, as AI hardware specifications continue to advance and achieve scale production, key segments in the supply chain—particularly those specializing in advanced manufacturing processes, precision metal structural components, and liquid cooling thermal solutions—are poised for substantial earnings growth.

Niuniu has previously compiled a list of relevant concept stocks under the new AI PC 2.0 landscape for investors’ reference:

Despite the vast potential of AI hardware, investors should still objectively assess how market share shifts among leading players in each sub-sector amid technological iterations, as well as their long-term core competitive advantages.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

65

102