SpaceX IPO is coming soon! Will space stocks get a boost?

Amid multiple positive catalysts, the commercial aerospace sector is heating up—what investment opportunities should investors focus on? | In-Depth Analysis | Research Report | Aerospace Sector

Recently, the global commercial aerospace sector has seen surging interest, driven by multiple favorable factors. Last week, U.S. commercial aerospace stocks rallied collectively, with many individual stocks posting gains exceeding... $AST SpaceMobile (ASTS.US)$ ...a single-month gain of over 50%, nearing a historical high, and $Rocket Lab (RKLB.US)$ ...a monthly gain exceeding 70%, reaching a record high. The sector is currently experiencing a triple catalyst convergence: SpaceX is reportedly targeting a Nasdaq listing as early as June 12, with a valuation range of $1.75 trillion to $2 trillion; NASA has unveiled a roadmap for establishing a sustained human presence at the lunar south pole; and domestic policies supporting the low-altitude economy continue to intensify, with China’s Civil Aviation Administration establishing a Low-Altitude Safety Division and expanding pilot programs to 23 provinces. The industry is poised to enter a golden development phase, and we recommend focusing on high-barrier leading companies in three key areas: satellite internet, commercial launch vehicles, and the low-altitude economy.

Amid multiple positive catalysts, the commercial aerospace sector is heating up—what investment opportunities should investors focus on?

Recently, bolstered by multiple supportive policies for the commercial aerospace sector, U.S. commercial aerospace stocks have been on a strong rally. On May 26, 2026, space-related stocks surged first, $Momentus (MNTS.US)$ ...jumping more than 109% in a single day, $Redwire (RDW.US)$ closing up 26%. Market enthusiasm continued to build the next day, on May 27, as the commercial aerospace sector extended its explosive rally: $Momentus (MNTS.US)$ rising another 25.97% following the previous day's 109% surge, $Redwire (RDW.US)$ gaining over 9%, $AST SpaceMobile (ASTS.US)$ Gains exceeded 8%. Although the aforementioned aerospace stocks experienced a pullback on May 28–29, most stocks in this sector still posted monthly gains above 10%. On the news front, SpaceX is expected to list on Nasdaq as early as June 12, with a target valuation exceeding $2 trillion, setting a new benchmark for the global commercial aerospace industry; NASA has released a three-phase roadmap for establishing a long-term presence at the lunar south pole, clarifying its long-term plan for returning humans to the Moon; domestically, policy support and legislation for the low-altitude economy continue to intensify, with the Civil Aviation Administration establishing a 'Low-Altitude Safety Division' and expanding low-altitude pilot zones to 23 provinces, accelerating industry development. Domestically, after the prior adjustment,Valuations of China’s commercial aerospace sector have retreated to historically low levels, offering a relatively high margin of safety. Meanwhile, with ongoing policy implementation and continuous technological breakthroughs, sector earnings are expected to gradually materialize, making the current timing favorable for positioning.

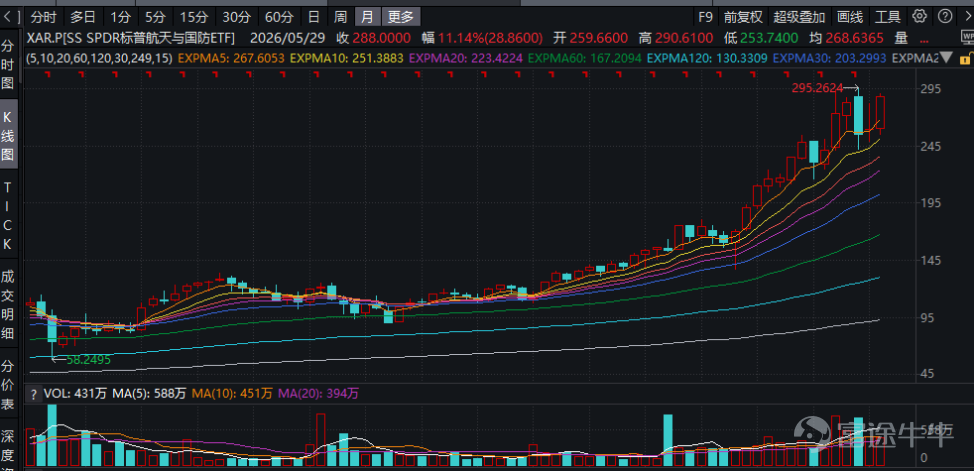

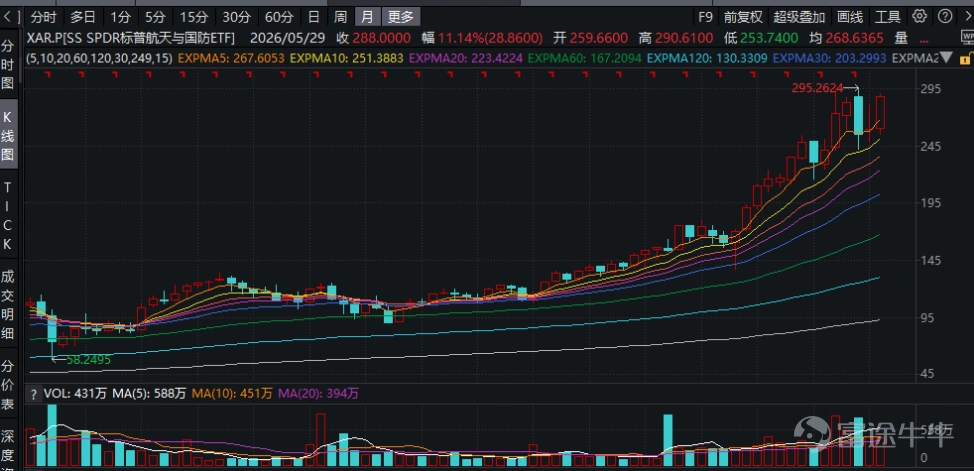

Figure 1: Performance of the S&P Aerospace & Defense Select Industry Index

Data source: Wind

– Key Catalysts for the Sector: Global Milestone Events and Accelerated Domestic Policy Implementation

* Anticipated SpaceX IPO Ignites Global Aerospace Enthusiasm

Market expectations for SpaceX’s upcoming IPO are extremely high. According to recent reports, SpaceX filed its S-1 registration statement with the U.S. Securities and Exchange Commission (SEC) on May 20, initiating what could become the largest IPO in history. The company plans to list on Nasdaq as early as June 12 under the ticker symbol 'SPCX,' with a target valuation between $1.75 trillion and $2 trillion. The market widely believes that SpaceX’s listing will establish a new valuation benchmark for the global commercial aerospace industry and attract significant capital toward space-sector companies with first-mover advantages.

Additionally, citing multiple insider sources, CNBC reported that discussions about a potential merger between SpaceX and Tesla have intensified as SpaceX’s IPO approaches. Elon Musk has already discussed the possibility of integrating the two trillion-dollar companies with key colleagues—a topic that has been openly debated within Tesla for years. Currently, the two companies share deep overlaps in board members, senior executives, and engineering teams, and have established routine operational collaboration: SpaceX is procuring Tesla Megapack energy storage systems to power AI data centers, while Tesla has commissioned SpaceX to develop specialized alloy materials. Both companies face common challenges related to power supply and computing resources, providing a practical foundation for further integration.

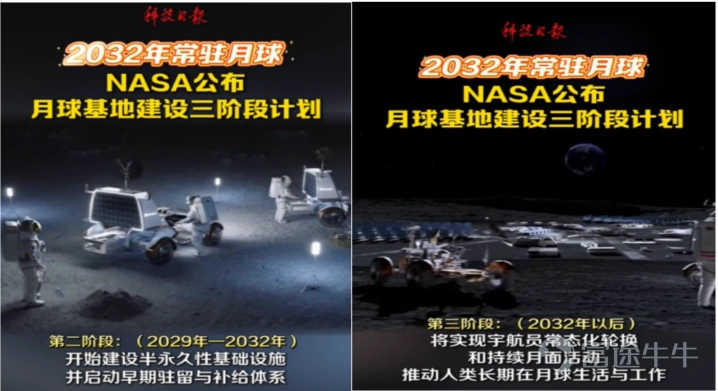

* NASA Unveils Three-Phase Roadmap for Lunar Base Construction

On May 26, NASA officially released a detailed three-phase roadmap for building a long-term human presence facility at the lunar south pole, further clarifying its long-term strategy for returning humans to the Moon. According to this roadmap, the U.S. will advance lunar base construction in three phases: Phase 1 (2026–2029): Focus on robotic missions to prepare for human return; Phase 2 (2030–2034): Achieve short-term human habitation on the lunar surface and construct basic infrastructure; Phase 3 (post-2035): Establish a sustainable, long-term lunar base to lay the groundwork for future Mars exploration.Lunar base construction will drive growth across multiple domains—including rocket launches, satellite communications, lunar exploration, and space resource utilization—creating vast market opportunities for the global commercial aerospace industry.

Figure 2: NASA's Published Phased Plan for Lunar Base Construction

Source: NASA

*Domestic legislation and policies supporting the low-altitude economy continue to intensify

China is accelerating the establishment of a legal and regulatory framework for emerging sectors such as artificial intelligence and the low-altitude economy. On May 13, the Civil Aviation Administration of China (CAAC) officially established the 'Low-Altitude Safety Department,' marking the full implementation of a national two-tier management system combining top-level strategic planning with specialized industry oversight. On May 27, Song Zhiyong, Party Secretary and Director of the CAAC, published a signed article titled 'Promoting Healthy and Orderly Development of the Low-Altitude Economy' on the front page of Study Times. The article revealed that core technologies—such as unmanned aerial systems and electric vertical takeoff and landing (eVTOL) aircraft—have achieved rapid breakthroughs in China. To date, type certifications have been completed for 19 unmanned aerial vehicle models, with over 70 new aircraft types currently under certification review.

The significant enhancement of domestic innovation capabilities in low-altitude equipment has laid a solid foundation for China’s participation in global low-altitude industry competition. The article explicitly stated that the civil aviation sector must align with technological trends, seize this strategic window of opportunity, and promote deep integration between the low-altitude economy and cutting-edge technologies like artificial intelligence and new energy. It emphasized accelerating the internationalization of Chinese technical solutions and industry standards to strengthen China’s voice and rule-shaping influence in the global low-altitude domain. This will enable China to gain an early-mover advantage and cultivate competitive strengths amid the new wave of scientific and industrial transformation, thereby comprehensively enhancing national competitiveness. At the policy level, the low-altitude economy has been included in the Government Work Report for three consecutive years and is officially designated as a national 'emerging pillar industry' starting in 2026. With continued policy support, pilot low-altitude flight zones have expanded to 23 provinces nationwide, with more than 110 short-haul transport routes now operational.As the policy framework continues to mature, infrastructure gradually takes shape, and technological innovation achieves sustained breakthroughs, the low-altitude economy is poised to become a new engine driving China’s economic growth, catalyzing explosive development across the entire industrial chain—including drones, general aviation, aerospace manufacturing, and low-altitude services.

Figure 3: Overview of Low-Altitude Economy Airspace

Source: National Low-Altitude Economy Integrated Innovation Industry Center

– Which investment opportunities within the sector should investors pay attention to?

Commercial aerospace is experiencing multiple concurrent growth curves, with low Earth orbit (LEO) satellite internet representing the most certain first growth curve at present. Major countries and companies worldwide are accelerating LEO constellation deployments. As of the end of 2025, over one million LEO satellites have already been registered with the International Telecommunication Union (ITU). The global satellite internet market is projected to exceed $108 billion by 2035, with China accounting for approximately 30% of this total. The maturation of reusable rocket technology serves as the core driver of this industry boom, having reduced launch costs by over 90%. For example, SpaceX’s Falcon 9 now costs less than $60 million per launch.China's Long March 10B, Zhuque-3, and several other reusable rockets are scheduled for their maiden flights in 2026, potentially reducing launch costs from the current RMB 75,000/kg to below RMB 20,000/kg, removing a major cost barrier to large-scale satellite constellation deployment.

Beyond near-term growth, the commercial aerospace sector is also nurturing two future trillion-dollar markets. On one hand, NASA’s release of its lunar base development roadmap marks humanity’s official entry into the 'lunar economy era.' Encompassing lunar exploration, resource exploitation, tourism, scientific research, and more, the global lunar economy is projected to exceed USD 1 trillion in scale by 2040. On the other hand,The low-altitude economy—a ground- and low-altitude extension of commercial aerospace technologies—is now benefiting from dual tailwinds of policy support and technological advancement. As China deepens reforms in low-altitude airspace management, industries such as drones, general aviation, and air taxis are poised for accelerated growth, with China’s low-altitude economy expected to surpass RMB 5 trillion in market size by 2030.

In terms of investment opportunities, key domestic commercial aerospace targets are categorized by industry segment as follows:

Satellite Internet:

$China Satellite Communications (601698.SH)$ : The only domestic satellite operator with access to communications and broadcasting satellite resources, employing a synergistic high-orbit + low-orbit operational model, and positioned to significantly benefit from the commercial rollout of direct-to-cellphone satellite connectivity.

$China Spacesat (600118.SH)$ : The sole listed platform of the China Academy of Space Technology (CAST, part of CASC), holding over 60% of China’s small satellite market share and responsible for manufacturing 60% of the satellites under the national Starlink-equivalent project (‘Xingwang’). It currently has a backlog of orders exceeding RMB 30 billion.

Aerospace Technology and Industrial Chain Support:

$CHINA AEROSPACE (00031.HK)$ : A core platform under China Aerospace Science and Technology Corporation (CASC), with businesses spanning aerospace technology applications and satellite operations services.

$AVICHINA (02357.HK)$ : A flagship platform for China’s aerospace high-tech industry, with operations covering core aerospace components and satellite application system integration.

$GOLDWIND (02208.HK)$ An early investor in LandSpace, China's leading commercial rocket company, holding a 4.14% stake.

Low-altitude economy:

$Avic Chengdu Aircraft (302132.SZ)$ A leading domestic manufacturer of unmanned aerial vehicle (UAV) systems, with products covering multiple core military and civilian sectors.

$Aerospace CH UAV (002389.SZ)$ A leading enterprise in military drones, actively expanding into the civilian drone market and developing low-altitude application scenarios.

Disclaimer: The information provided in this report, or any investment or potential transaction related thereto, is subject to the applicable laws and regulatory requirements of your jurisdiction, and you are solely responsible for compliance with such laws and regulations. The content of this report is for reference only and does not constitute any investment advice. Our company has made every effort to ensure the accuracy of the financial information provided, but assumes no responsibility or provides any form of guarantee for the accuracy, completeness, or effectiveness of all or part of the content. We will not be liable for any errors or omissions. Please also note that securities and virtual asset prices can fluctuate, especially given the extremely high risks associated with virtual assets, and investors should exercise caution and assume investment risks on their own.

———————————————————————

About the author:

Victory Securities – Hong Kong’s Leading Virtual Asset Broker

Victory Securities (HKEX: 08540), rooted in Hong Kong for over 50 years, is a fully licensed, integrated brokerage offering comprehensive financial services. It provides four core business lines—wealth management, asset management, virtual assets, and capital markets—to individual investors, institutional clients, high-net-worth individuals, and corporations, earning numerous awards and essential operating licenses across the Asia-Pacific region. In 2023, Victory Securities became the first Hong Kong broker to hold SFC licenses for virtual asset trading, advisory, and asset management services, and received SFC approval to offer virtual asset trading and advisory services to retail investors, providing a one-stop compliant platform for Bitcoin and Ethereum trading, conversion, and fiat on/off-ramps.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

5

2