What to Watch in US Stocks | NVIDIA's Annual Shareholder Meeting Is Here—Why Even Beginners Should T

Global Weekly Insights | U.S. Q1 economic growth revised downward; China’s new growth drivers lead efficiency gains

United States: First-quarter economic growth was revised downward, inflation remains persistently high, and stagflationary features have become more pronounced.

Last week, U.S. macroeconomic data continued to reflect a stagflationary pattern characterized by weakening economic momentum alongside persistently high inflation, further narrowing the Federal Reserve's policy maneuvering room. On the data front, annualized GDP growth for the first quarter was revised down to 1.6%, below both the initial estimate and market expectations,mainly weighed down by a slowdown in business inventory accumulation and weaker-than-expected consumer spending on services. Growth improved only marginally from the fourth quarter of last year, while corporate profit expansion cooled significantly, reflecting weak underlying economic momentum.Inflationary pressures continued to intensify, with April’s PCE and core PCE price indices posting their highest year-over-year increases in three years and nearly two years, respectively. Rising energy prices driven by Middle East geopolitical tensions have continued to transmit across the entire industrial chain, becoming a key driver behind persistently elevated inflation. Consumer spending showed clear divergence, with nominal consumption rising modestly but real consumption—adjusted for inflation—nearly flatlining,as stagnant household income growth and a sharp decline in the savings rate to multi-year lows left current consumption resilience largely dependent on drawing down savings, raising concerns about its sustainability.The combination of slowing growth and high inflation has complicated the Federal Reserve’s policy decisions, pushing market expectations for rate cuts further into the future. The new Fed chair faces significant challenges in establishing policy credibility and managing inflation expectations.

China: Industrial enterprise profits continue to accelerate, driven by emerging sectors, with pronounced structural divergence across industries

In China, the macro focus centered on industrial enterprise profitability data, which overall showed steady revenue growth, accelerating profit gains, and improving earnings quality—highlighting clear signs of industrial upgrading. From January to April, profits at nationwide industrial enterprises above designated size rose 18.2% year-on-year, with April alone seeing a further acceleration to 24.7%. The pace of profit recovery has continued to pick up, while unit revenue costs have declined for four consecutive months, and the revenue profit margin reached its highest level for the same period since 2023, indicating steadily improving overall profitability.Structurally, industrial profitability exhibited notable sectoral bright spots, with high-tech manufacturing and equipment manufacturing serving as the primary engines of growth,as emerging sectors such as semiconductors, optoelectronics, and industrial automation posted explosive profit growth, with the electronics industry accounting for nearly half of the total profit increase. Raw materials manufacturing also benefited from rising global commodity prices and strong demand from emerging industries, driving substantial profit gains in non-ferrous metals, chemicals, and petroleum processing. Profitability improved broadly across all types of market participants, with large, medium, small, and micro enterprises—as well as enterprises under various ownership structures—all recording steady growth.However, the economy still faces structural pressures, with a pronounced imbalance between strong domestic supply and weak demand. Profitability in the property sector and some traditional manufacturing industries continues to decline,Corporate accounts receivable and inventory turnover efficiency have somewhat weakened, and going forward, reinforcing the recovery of industrial activity will still rely on expanding domestic demand and improving supply quality.

In the equity market,

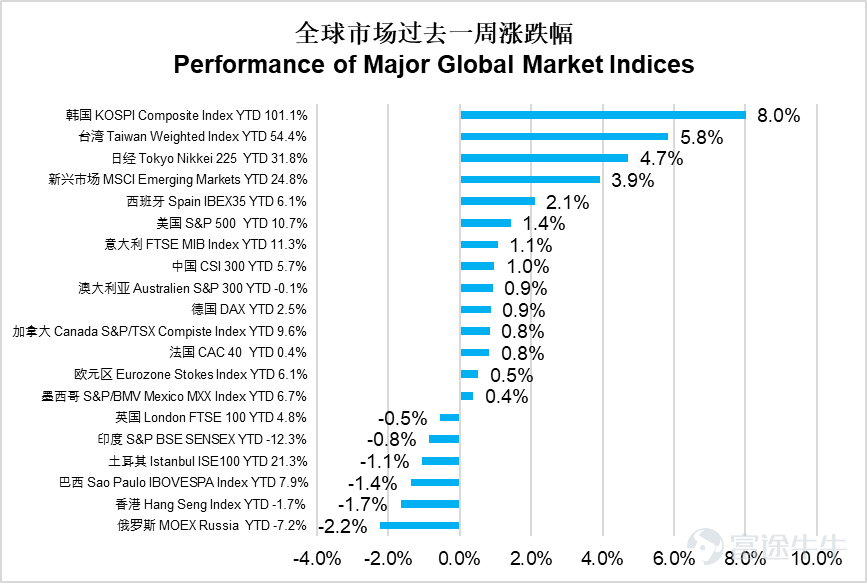

Global markets showed divergent performance last week,with the KOSPI surging 8.0% to lead global markets, and the Taiwan Weighted Index rising 5.8%,while the Nikkei 225 gained 4.7%. Emerging markets as a whole jumped 3.9%, the Hang Seng Index fell 1.7%, and the CSI 300 rose 1.0%. The MOEX Russia Index declined 2.2%, Brazil's IBOVESPA dropped 1.4%, and Turkey's ISE 100 fell 1.1%, underperforming notably. U.S. equities $S&P 500 Index (.SPX.US)$ rose 1.4%.Overall, Asian emerging markets stood out particularly strongly.

Data source: Wind

The U.S. information technology sector surged 4.6%, leading all sectors, followed by consumer discretionary up 1.5%, materials up 1.2%, and industrials up 0.8%.Communication services were flat. However, the energy sector plunged 5.4%, consumer staples fell 3.2%, utilities dropped 2.1%, real estate declined 1.4%, financials slipped 0.7%, and healthcare edged down 0.3%.The market exhibited an extreme divergence, with information technology leading gains and energy and consumer sectors leading losses.

Source: Wind

Hong Kong's industrial sector was flat, while the Hang Seng Tech Index edged up 0.3%, making it one of the few advancing sectors.The information technology sector fell 0.5%, consumer staples declined 0.6%, and the energy sector dropped 0.8%. Meanwhile, consumer discretionary plunged 3.3%, materials slid 2.8%, real estate and construction fell 2.6%, and healthcare declined 2.0%. Conglomerates dropped 1.9%, telecommunications fell 1.6%, financials declined 1.4%, and utilities slipped 1.3%.The market showed resilience in technology and industrial sectors, while consumer and materials sectors led the declines.

Source: Wind

Bond Market

Global bond markets continued to recover over the past week, with the Global Aggregate Index rising 1.00% and the U.S. Aggregate Index up 0.83%.U.S. investment-grade corporate bonds rose 0.97%, while U.S. high-yield corporate bonds gained 0.55%. The Emerging Markets USD Bond Aggregate Index increased 1.09%, and the China USD Credit Bond Index advanced 0.64%.

On the rates front, U.S. Treasury yields shifted lower across the curve.The yield on the 2-year U.S. Treasury note fell 12 basis points to 4.00%, and the 10-year Treasury yield declined 12 basis points to 4.44%.

Market outlook

– Early signs of weakening U.S. consumer spending are emerging, with oil price movements becoming a key variable.

The core tension in global markets currently lies in the tug-of-war between 'AI-driven earnings growth' and 'policy tightening risks amid a stagflationary environment.'On one hand, explosive growth in AI infrastructure investment has provided strong earnings support for the technology sector, driving the information technology sector up 37.5% year-to-date. This industry-revolution-driven earnings growth shows strong sustainability, allowing U.S. equities to continue hitting new highs despite macro headwinds. On the other hand, April's PCE inflation rose 3.8% year-over-year—the highest in three years—and Q1 GDP was revised downward from 2.0% to 1.6%, forming a classic stagflationary mix of 'slowing growth plus accelerating inflation.' Interest rate swaps now price in a roughly 55% probability of a Fed rate hike by year-end.If persistently high inflation forces the Federal Reserve to pivot toward rate hikes, an elevated interest rate environment would exert greater pressure across broad segments of the economy beyond AI, and early signs of weakening consumer spending are already visible.

Oil price trends will be the critical variable shaping how this core tension evolves. Brent crude fell 12% this week to $91 per barrel, primarily driven by expectations of easing U.S.-Iran negotiations.If the U.S. and Iran subsequently reach a formal agreement and shipping through the Strait of Hormuz resumes, oil prices could decline further, significantly alleviating inflationary pressures,giving the Federal Reserve room to hold rates steady and providing a tailwind for global risk assets. However, if talks collapse or Middle East tensions escalate again, oil prices rebounding above $100 would accelerate the realization of stagflation risks,substantially increasing the likelihood of a forced Fed rate hike and posing a material threat to U.S. equities, whose valuations are already at elevated levels.

Key economic data and events this week

On Monday, the U.S. will release May's ISM Manufacturing PMI;

On Wednesday, the U.S. will release the May ADP employment report, the May ISM Services PMI, and the Federal Reserve's Beige Book.

On Friday, the U.S. will release the May nonfarm payrolls report.

Disclaimer: The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions can only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may rise or fall, and past performance is not indicative of future results. Before investing, investors should carefully read the fund prospectus (including the 'Risk Factors' section) to understand the investment risks related to the fund. This report may only be distributed in certain jurisdictions. In any jurisdiction where distributing such information or making any invitation or recommendation is prohibited, or where distributing this report or making an invitation or recommendation to any person would be illegal, this report does not constitute such distribution or invitation or recommendation. This document has been exempted from prior review and approval by the Hong Kong Securities and Futures Commission, and has not been reviewed by the SFC. SFC approval does not imply promotion or endorsement of the plan, nor does it guarantee its commercial merits or performance, nor does it indicate suitability for all investors, or endorsement of suitability for any particular investor or category of investors. All rights reserved © 2026. E Fund Asset Management (Hong Kong) Co., Ltd.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

1