Countdown to NVIDIA's conference: AI computing power and storage sectors may benefit—what to invest

Short-term on-chain turnover cools, regulatory policy博弈 heats up, and use cases continue to expand—Observing Bitcoin’s structural signals

Summary of Key Insights

Recently, the Bitcoin market has exhibited several noteworthy structural signals. On-chain data shows that the proportion of short-term coins in on-chain turnover activity remains low, indicating a cooling of speculative short-term trading and potential selling pressure. On the policy front, crypto industry political action committees demonstrated significant financial and mobilization capabilities during U.S. congressional primaries, potentially heightening market attention to upcoming crypto regulatory legislation. Regarding use cases, Mastercard obtained a New York State BitLicense, Italy’s Banca Sella received approval to offer crypto-asset-related services, and Abu Dhabi’s IHC completed an institutional-grade stablecoin transaction—all reflecting ongoing efforts by traditional finance and institutional infrastructure to explore digital asset applications. This article will analyze these developments across four dimensions: on-chain structure, policy environment, use cases, and institutional capital.

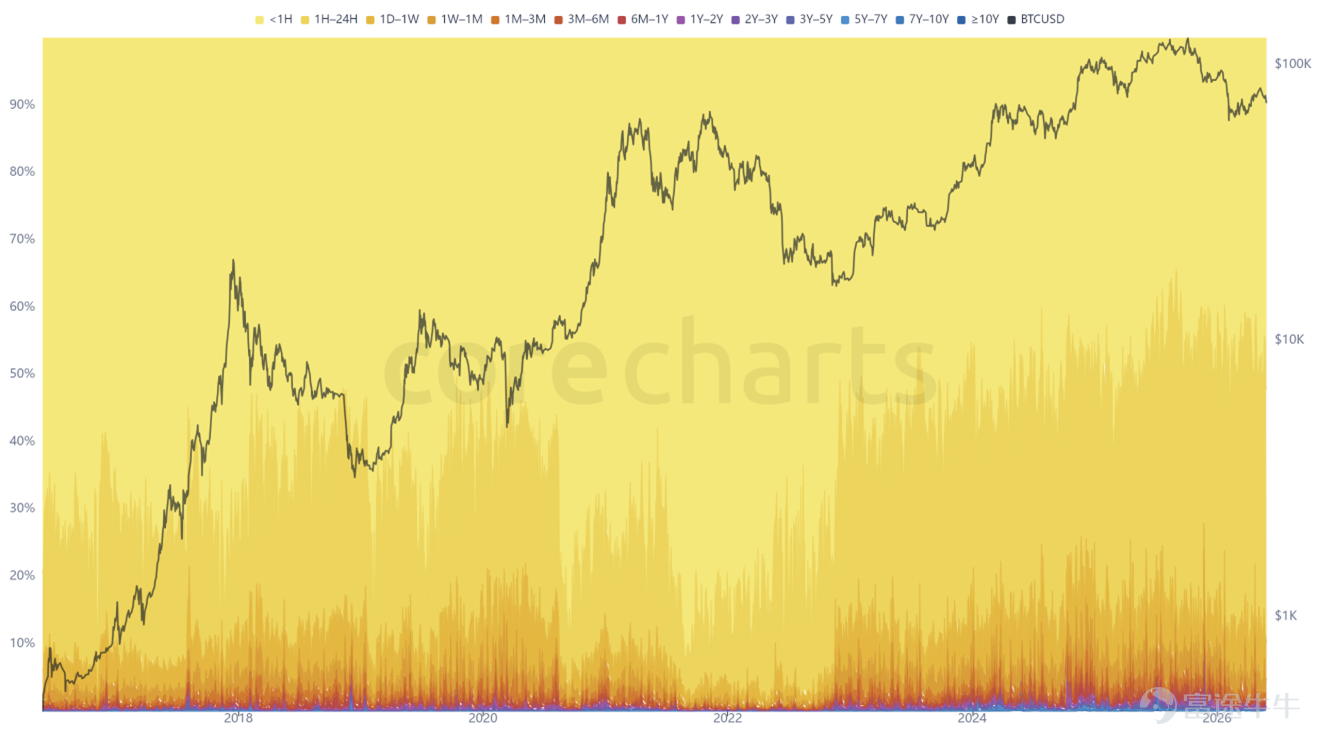

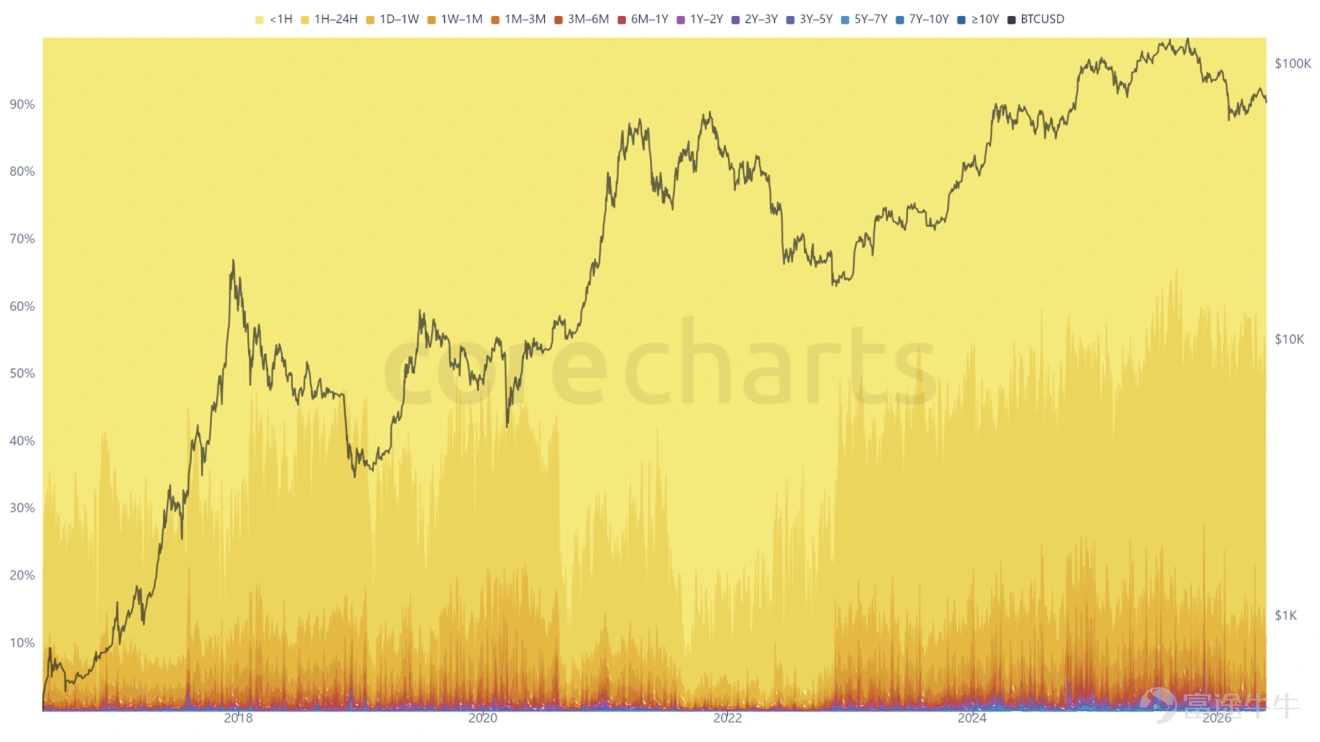

1. Short-term on-chain turnover cools, coin age distribution shows low activity

This article uses CoreCharts’ Bitcoin Spent Volume Age Bands metric to observe the share of coins with different coin ages in on-chain spent volume. This metric helps determine whether current on-chain turnover is primarily driven by recently moved short-term coins or by coins that have remained dormant for longer periods.

Recent data shows that the turnover weight in the short-term coin age bands is at a relatively low level, indicating a decline in on-chain activity among short-term capital. This typically suggests reduced dominance of short-term behaviors—such as speculative trading, arbitrage, profit-taking, or panic selling—in on-chain activity. Meanwhile, the supply share held by short-term holders is also at a阶段性 low, further signaling an easing of short-term selling pressure.

Source: CoreCharts, May 28, 2026

It should be noted that on-chain metrics only reflect changes in token distribution and trading behavior and should not be used alone to determine market bottoms or predict price trends. Going forward, these indicators should be considered alongside macro liquidity conditions, ETF fund flows, regulatory developments, and shifts in market risk appetite.

II. Rising Political Influence of Crypto: CLARITY Act’s Passage Odds Draw Attention

In the Democratic runoff primary for Texas’s 18th Congressional District, newly elected Representative Christian Menefee defeated long-serving Representative Al Green. The district had undergone recent redistricting, resulting in a rare intra-party contest between two incumbent Democratic representatives.

During this election, candidates’ stances on crypto policy became a key focus for markets. According to public reports, crypto-related political action committees (PACs) heavily funded support for Menefee while opposing Green. Green had previously voted against crypto-related legislation such as the GENIUS Act and the CLARITY Act and received a low rating from crypto advocacy group Stand With Crypto. Crypto industry groups like Fairshake interpreted Green’s defeat as evidence that anti-crypto positions may carry electoral costs. However, it should be noted that this outcome was also influenced by multiple factors, including redistricting, generational turnover among candidates, and shifts in local political dynamics.

From a market perspective, this event highlights the growing financial investment and political mobilization capacity of the crypto industry in U.S. elections. As Congress continues advancing a regulatory framework for digital assets, the influence of industry groups on lawmakers’ positions and election outcomes could become a critical variable in tracking future crypto legislation.

The CLARITY Act passed the Senate Banking Committee on May 14 by a vote of 15 to 9 and will now proceed to a full Senate floor vote. The current U.S. Senate composition includes 53 Republicans, 45 Democrats, and 2 independents. Since most major Senate legislation typically requires at least 60 votes to invoke cloture and end debate, securing sufficient bipartisan support remains crucial for its advancement.

III. Accelerating Real-World Adoption: Payments, Custody, and Institutional-Grade Stablecoin Trading

Several recent cross-regional developments collectively point to the ongoing maturation of crypto infrastructure.

Mastercard Obtains New York BitLicense. On May 27, Mastercard's U.S. transaction services unit received a BitLicense from the New York State Department of Financial Services. This is the third license issued by New York in 2026. The license supports Mastercard’s long-term strategy involving payment and settlement infrastructure for digital currencies such as stablecoins and tokenized deposits. Since the program’s launch in 2015, New York has issued only about 40 BitLicenses in total. With this license, Mastercard can now launch blockchain-based settlement services within a regulated framework.

Italy’s Banca Sella Approved for Crypto Custody Services. Banca Sella, an Italian bank with €34 billion in assets, has become the country’s first commercial bank authorized to directly offer cryptocurrency custody and transfer services to clients, following a legal notification procedure submitted to the Bank of Italy. This move marks European traditional banks expanding crypto services under the MiCA framework.

Abu Dhabi-Based Institution Completes $30 Million Stablecoin Transaction. International Holding Company (IHC), headquartered in Abu Dhabi, announced it has completed a $30 million transaction using DDSC, a UAE dirham-backed stablecoin—marking the first institutional use of this stablecoin. The transaction was executed on ADI Chain, an institutional-grade Layer-2 blockchain developed by the ADI Foundation. Officials stated that this transaction demonstrates the digital currency ecosystem’s capacity to handle institutional-scale transaction volumes. DDSC was co-created by IHC, First Abu Dhabi Bank, and Sirius International Holding.

IV. Institutional Funding Channels Remain Open: SATA Can Buy Nearly 800 Bitcoins in a Single Week

SATA, a subsidiary of Strive, has demonstrated sustained institutional interest in Bitcoin-related assets through its recent financing activities.

According to Odaily Planet Daily, SATA raised enough capital within two trading days to purchase 396 Bitcoins, surpassing its previous weekly record. As of this week, its cumulative fundraising amount is sufficient to buy 798 Bitcoins—and continues to grow. Cash flows generated from SATA’s preferred stock offerings are directly converted into ongoing Bitcoin purchases, creating a closed-loop cycle of 'fundraising → accumulation.'

This data indicates that channels for allocating capital to Bitcoin via compliant structured products remain open.

Conclusion:

Synthesizing the above observations, the Bitcoin market has recently exhibited multiple structural signals:

• On-chain structure: The proportion of short-term holdings involved in on-chain turnover activity remains at a relatively low level, indicating a cooling off in short-term speculative trading and potential selling pressure. However, on-chain metrics alone should not be used as the sole basis for identifying market bottoms or forecasting price trends;

• Political influence: Crypto industry Political Action Committees (PACs) have demonstrated significant financial resources and mobilization capabilities in recent U.S. congressional primaries, potentially heightening market attention to upcoming cryptocurrency regulatory legislation;

• Use cases: Three cross-regional developments—Mastercard, Banca Sella of Italy, and Abu Dhabi’s IHC—collectively signal the maturation of crypto infrastructure;

• Funding momentum: SATA raised enough capital in a single week to purchase nearly 800 Bitcoin, reflecting robust institutional funding channels.

China AMC Cryptocurrency ETF Series — A compliant, convenient, and diversified allocation tool

No need to manage private keys or bear exchange credit risk; you can compliantly and conveniently allocate crypto assets through a Hong Kong stock account:

China AMC Bitcoin ETF (3042.HK / 83042.HK / 9042.HK), China AMC Ethereum ETF (3046.HK / 83046.HK / 9046.HK)

🎖️ The most traded ETF of its kind in Hong Kong [1]

🎖️ The most liquid ETF of its kind in Hong Kong, and the only product in Hong Kong with trading counters in HKD, USD, and RMB [1]

China AMC Solana ETF (3460.HK / 83460.HK / 9460.HK)

🎖️ Asia's first and only Solana ETF [1]

🎖️ Equipped with three trading counters: HKD, USD, and RMB

$ChinaAMC Bitcoin ETF (03042.HK)$$ChinaAMC Bitcoin ETF-U (09042.HK)$$ChinaAMC Bitcoin ETF-R (83042.HK)$$ChinaAMC Ether ETF (03046.HK)$$ChinaAMC Ether ETF-U (09046.HK)$$ChinaAMC Ether ETF-R (83046.HK)$$ChinaAMC Bitcoin ETF (Unlisted Class) (HK0001012720.MF)$$SSE Composite Index (000001.SH)$$CSI 300 Index (000300.SH)$$NVIDIA (NVDA.US)$$Amazon (AMZN.US)$$Alphabet-C (GOOG.US)$$Meta Platforms (META.US)$$Tesla (TSLA.US)$$HSTECH (LIST91332.HK)$$Hang Seng Index (800000.HK)$$SSE 50 Index (000016.SH)$$CSI 300 Index (000300.SH)$$CSI 1000 Index (000852.SH)$$SSE Science and Technology Innovation Board 50 Index (000688.SH)$$ChinaAMC CSI 300 Index ETF (03188.HK)$$SSE Composite Index (000001.SH)$$XIAOMI-W (01810.HK)$$JD.com (JD.US)$$TENCENT (00700.HK)$$Shenzhen Component Index (399001.SZ)$$Kweichow Moutai (600519.SH)$$Contemporary Amperex Technology (300750.SZ)$$PING AN (02318.HK)$$Alibaba (BABA.US)$$ICBC (01398.HK)$$CHINA MOBILE (00941.HK)$

Important Information about China AMC Bitcoin ETF

Investing involves risks, including the loss of principal. Past performance is not indicative of future results. Before investing in the China AMC Bitcoin ETF (the "Fund"), investors should refer to the fund's prospectus, paying particular attention to the risk factors. You should not rely solely on this material to make investment decisions. Please note:

• The Fund’s investment objective is to provide investment results that closely track the performance of Bitcoin (as measured by the CME CF Bitcoin Index (APAC Close Price) ("Index")) before fees and expenses.

• The Fund is passively managed. A decline in the index may lead to a corresponding decline in the value of the Fund. The Fund is subject to new product risk, new index risk, tracking error risk, and the risk of trading at a discount or premium.

• Since the Fund invests directly only in Bitcoin, it is exposed to concentration risk and risks associated with Bitcoin, such as risks related to Bitcoin and the Bitcoin industry, speculative risk, unforeseen risks, extreme price volatility risk, ownership concentration risk, regulatory risk, fraud, market manipulation and security breach risk, cybersecurity risk, potential manipulation of the Bitcoin network risk, fork risk, illegal usage risk, and transaction timing difference risk.

• The Fund is exposed to risks associated with Virtual Asset Trading Platforms ("VATP"), custody risk, and the risk of differences between the enforceable price of Bitcoin on the SFC-licensed virtual asset trading platform and the index price for cash subscriptions and redemptions.

• Listed and unlisted classes follow different pricing and trading arrangements. Due to differing fees and costs, the net asset value per unit of each class may vary. The trading cutoff times for listed and unlisted classes differ. The cutoff times for transactions in each class also vary.

• Listed class fund units are traded on the secondary market at the current market price, while non-listed class fund units are sold through intermediaries based on the net asset value at the end of the trading day. Investors in the non-listed class can redeem their units at net asset value, whereas investors in the listed class on the secondary market can only sell at the prevailing market price and may have to exit the fund at a significant discount. Investors in the non-listed class may have an advantage or disadvantage compared to those in the listed class.

• This fund involves multiple counterparty risks.

Please note that the above list of risks is not exhaustive; for details, please refer to the fund's prospectus.

Important Information about China AMC Ether ETF

Investing involves risks, including the loss of principal. Past performance is not indicative of future results. Before investing in the China AMC Ether ETF (the "Fund"), investors should refer to the fund's prospectus, paying particular attention to the risk factors. You should not rely solely on this material to make investment decisions. Please note:

• The Fund’s investment objective is to provide investment results that closely track the performance of Ether (as measured by the CME CF Ether Index (APAC Close) (the "Index")) before fees and expenses.

• The Fund is passively managed. A decline in the index may lead to a corresponding decline in the value of the Fund. The Fund is subject to new product risk, new index risk, tracking error risk, and the risk of trading at a discount or premium.

• Since the Fund invests directly in Ether, it is subject to concentration risk and risks associated with Ether, such as risks related to Ether and the Ether industry, speculative risks, unforeseen risks, extreme price volatility risk, ownership concentration risk, regulatory risk, fraud, market manipulation and security breach risk, cybersecurity risk, fork risk, illegal usage risk, risks associated with Ether staking, and transaction timing risk.

• The Fund is exposed to risks associated with Virtual Asset Trading Platforms ("VATP"), custody risks, and risks related to the difference between the executable price of Ether on the SFC-licensed virtual asset trading platform and the index price for cash subscription and redemption.

• Listed and unlisted classes follow different pricing and trading arrangements. Due to differing fees and costs, the net asset value per unit of each class may vary. The trading cutoff times for listed and unlisted classes differ. The cutoff times for transactions in each class also vary.

• Listed class fund units are traded on the secondary market at the current market price, while non-listed class fund units are sold through intermediaries based on the net asset value at the end of the trading day. Investors in the non-listed class can redeem their units at net asset value, whereas investors in the listed class on the secondary market can only sell at the prevailing market price and may have to exit the fund at a significant discount. Investors in the non-listed class may have an advantage or disadvantage compared to those in the listed class.

• This fund involves multiple counterparty risks.

Please note that the above list of risks is not exhaustive; for details, please refer to the fund's prospectus.

Important Information about China AMC Solana ETF

Investing involves risks, including the loss of principal. Past performance is not indicative of future results. Before investing in the China AMC Solana ETF (the "Fund"), investors should refer to the fund prospectus, paying close attention to risk factors. You should not rely solely on this material to make investment decisions. Please note:

• The Fund’s investment objective is to provide investment results that closely track the performance of SOL (measured by the CME CF Solana-USD Index (APAC Close) (the "Index")) before fees and expenses.

• The Fund is passively managed. A decline in the Index may result in a corresponding decline in the value of the Fund. The Fund involves new product risk, new index risk, tracking error risk, and discount or premium trading risk.

• Since the Fund invests directly only in SOL, it is subject to concentration risk and risks associated with Solana and SOL, such as SOL and Solana industry risk, speculative risk, unforeseen risks, limited history risk, hybrid PoH and PoS mechanism risk, inflation risk, extreme price volatility risk, ownership concentration risk, regulatory risk, fraud, market manipulation and security breach risk, cybersecurity risk, network disruption risk, forking risk, illegal usage risk, and time lag risk.

• The Fund involves risks related to virtual asset trading platforms ("VATP"), custody risk, and risks associated with the difference between the enforceable price of SOL on SFC-licensed virtual asset trading platforms and the index price for cash subscriptions and redemptions.

• Listed and unlisted classes follow different pricing and trading arrangements. Due to varying fees and costs, the net asset value per unit of each class may differ. The trading cutoff times for listed and unlisted classes are different. The transaction deadlines for each class may vary.

• Listed class fund units are traded on the secondary market at the current market price, while non-listed class fund units are sold through intermediaries based on the net asset value at the end of the trading day. Investors in the non-listed class can redeem their units at net asset value, whereas investors in the listed class on the secondary market can only sell at the prevailing market price and may have to exit the fund at a significant discount. Investors in the non-listed class may have an advantage or disadvantage compared to those in the listed class.

• This fund involves multiple counterparty risks.

Please note that the above list of risks is not exhaustive; for details, please refer to the fund's prospectus.

Data source:

• Binance Square, On-chain Activity Weight Analysis, May 28, 2026, https://www.binance.com/zh-CN/square/post/327256298430417

• The Block Beats, Crypto PAC Spends Tens of Millions to Defeat Anti-Crypto Lawmaker, May 2026, https://www.theblockbeats.info/flash/347905

• Binance Square, Mastercard Obtains New York State BitLicense, May 27, 2026, https://www.binance.com/zh-CN/square/post/05-27-2026-mastercard-obtains-new-york-state-bitlicense-327683677539153

• Bitget News, Italy’s Banca Sella Approved for Crypto Custody Services, May 2026, https://www.bitget.com/zh-TC/news/detail/12560605431023

• Binance Square, Abu Dhabi Company Completes $30 Million Stablecoin Transaction, May 26, 2026, https://www.binance.com/zh-CN/square/post/05-26-2026-abu-dhabi-company-completes-30-million-stablecoin-transaction-327198433695857

• Binance Square, Strive's subsidiary SATA is raising funds to purchase 798 Bitcoin, May 27, 2026, https://www.binance.com/zh-CN/square/post/05-27-2026-strive-s-sata-subsidiary-is-raising-funds-to-purchase-798-bitcoins-327743950799938

[1] Data sourced from China AMC (Hong Kong) and Bloomberg, as of May 28, 2026.

The market data, case studies, and industry observations mentioned in this article are for illustrative purposes only, sourced from public media reports and industry research, and do not constitute investment advice.

Investment involves risks, including the loss of principal. The price of fund units can go up as well as down, and past performance of the fund is not indicative of future returns. This fund invests directly in virtual assets ("VA"), thus there are concentration risks as well as inherent risks associated with each virtual asset and its ecosystem, along with risks from virtual asset trading platforms. You should read the fund’s offering documents and product key facts statement for details. Investors should not make investment decisions based solely on this promotional material.

This document is for your reference only and does not constitute an offer or solicitation for the purchase or sale of any securities or funds or any trading thereof, nor is it intended as investment advice. This material is issued by China AMC (HK) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment