What to Watch in US Stocks | NVIDIA's Annual Shareholder Meeting Is Here—Why Even Beginners Should T

[Weekly Market Insights] Persistent high inflation delays rate cuts; seek structural opportunities amid sector rotation

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780279393656-Ho1xXq3jFr.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Guide to this week's strategies for the US and Hong Kong markets:

With high inflation pushing rate cuts to 2027, how should investors navigate the elevated volatility in U.S. equities?

Amid Hong Kong equities’ triple constraints and a generally weak outlook, where can structural opportunities break through?

[Live Stream Reservation] Join Futu’s Chief Investment Research Expert today at 16:30 to preview this week’s market and explore quantum investment opportunities!

[I. Macroeconomic Observations]

1.1 International Macroeconomic:

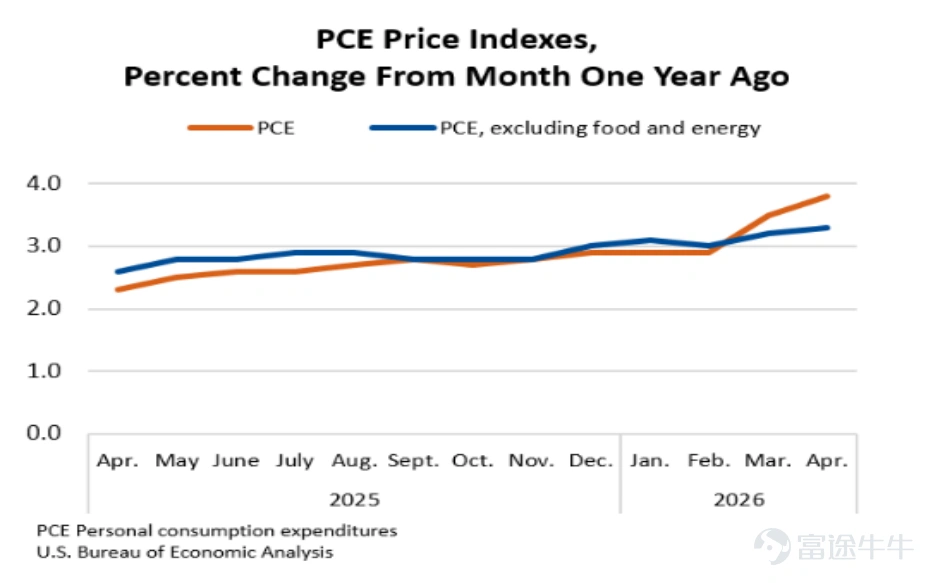

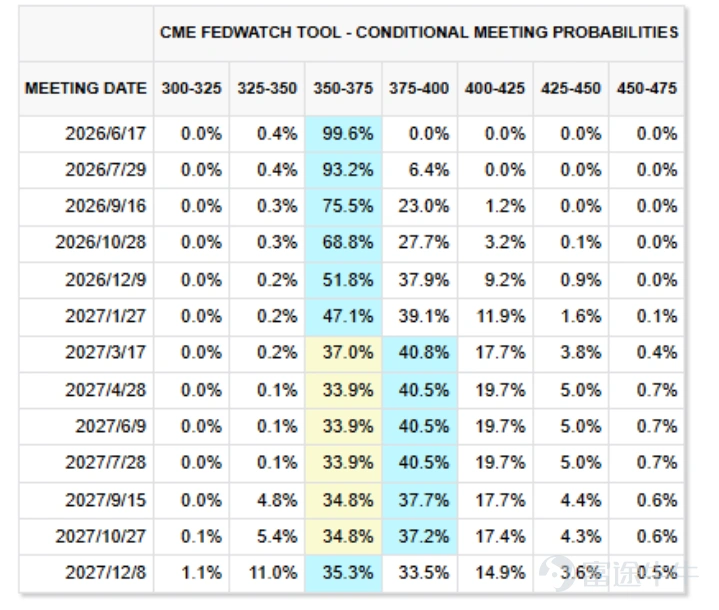

PCE inflation at 3.8% year-over-year hits a nearly three-year high—has the Fed’s rate-cut window been pushed to 2027?

The U.S. April PCE price index rose 3.8% year-over-year, matching expectations and reaching its highest level since May 2023. Core PCE inflation also climbed 3.3% year-over-year, the highest since November 2023, primarily driven by rising energy prices amid the Iran conflict. Personal income was flat month-over-month (0.0%), while the savings rate dropped to a precarious low of 2.6%.Consumers are being forced to 'draw down savings to sustain spending,' with real (inflation-adjusted) personal consumption expenditures increasing by just 0.1% month-over-month—a clear sign of cooling demand.

U.S. April PCE

A hold on rates at the Fed’s June meeting is now widely expected, with some institutions projecting the first rate cut could be delayed until Q1 2027 (25 bps cuts each in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2.0%, butAmid a backdrop of 'slowing growth, resilient earnings, and sustained AI-related investment,' the foundation for elevated risk asset valuations remains intact.

FEDWATCH

1.2 Domestic Macroeconomics:

May PMI fell to the 50.0 breakeven mark, weighed down by both domestic and external demand; industrial profit structures show growing divergence.

The May manufacturing PMI stood at 50.0%, down 0.3 percentage points from last month—declining more than seasonal patterns would suggest. New orders dipped below the 50.0 mark, and new export orders dropped sharply, highlighting weak domestic demand and softening external demand. Finished goods inventory unexpectedly rose to 49.3%, indicating firms face involuntary inventory accumulation pressure. The construction sector (48.8%) remains in contraction territory, with physical project execution progressing slower than expected.

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280219423-k8GQiWZLsf.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

The non-manufacturing business activity index stood at 50.1%, up 0.7 percentage points from last month,indicating a recovery in non-manufacturing sector sentiment. By sub-sector, the construction business activity index rose by 0.8 percentage points from last month, while the services business activity index increased by 0.7 percentage points. Within the services sector,railway transportation, telecommunications, radio and television broadcasting, satellite transmission services, and insurance all reported business activity indices above the 55.0% mark, reflecting strong expansion;while sectors such as air transportation and real estate recorded business activity indices below the 50.0% threshold.

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280205103-mQ7GVOVPgQ.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

A key highlight lies inthe resilience and structural divergence in industrial profits: From January to April, profits of designated-size industrial enterprises rose 18.2% year-on-year. Profits in the computer, communication, and electronic equipment manufacturing sector surged by 108%, driven by both the global AI-related capital expenditure boom and the semiconductor cycle recovery, contributing 43.8% to the overall growth in industrial profits. However, downstream consumer goods manufacturers remain under pressure, with sectors like agricultural and sideline food processing and furniture experiencing deteriorating profitability,as domestic demand remains weak。

[Section Two: Market Views]

2.1 US Stock Market

With the index hitting new highs and AI earnings validating the profit cycle, how should investors position themselves amid this high-level sector rotation?

$S&P 500 Index (.SPX.US)$ Up 1.43% for the full week, $NASDAQ 100 Index (.NDX.US)$ Gained 2.39%, supported by a marginal pullback in U.S. Treasury yields and rising expectations of geopolitical de-escalation, with both technology and consumer sectors underpinning the market. The Russell 2000 outperformed the broader market last week, with airlines up 9.0%, housing up 6.4%, and retail up 7.7%,Market breadth is broadening from a handful of mega-cap leaders to a wider range of risk assets。

Sentiment remains cautiously optimistic; indices are holding strong in a high-level trading range. Attention should be paid to whether the market has entered the latter stage of a primary uptrend, characterized by intensified sector rotation at elevated levels. With both volatility and positioning crowding increasing, high-beta sectors may undergo short-term consolidation. Focus is recommended on three structural themes:Hard tech driven by AI earnings realization and capital expenditure validation, consumer and airline/retail sectors benefiting from declining oil prices, and small-cap breadth expansion。

The S&P 500’s forward 12-month P/E ratio stands at 21.4 (as of May 28), near the upper end of its historical range; however, as long as employment, consumer spending, and corporate capital expenditures do not simultaneously deteriorate, the foundation for current elevated valuations remains intact.

The S&P 500’s forward 12-month P/E ratio stands at 21.4 (May 28)

Stock Spotlight – $Marvell Technology (MRVL.US)$ : A multi-year high-growth platform driven by AI interconnects and custom chips

Comprehensively raised medium-term guidance confirms high growth visibility: FY27 revenue guidance lifted to $11.5 billion (+40% YoY), FY28 raised to $16.5 billion (+45% YoY); data center business projected to grow 50% in FY27 and 55% in FY28; custom chip revenue targeted to exceed $10 billion in FY29;Even though current valuations are at historical highs, the significantly improved visibility into growth trajectory and industry duration supports the view that 'pullbacks are buying opportunities.'。

Interconnect business is the strongest real-world driver behind this round of upward revision.FY27 interconnect revenue growth guidance has been raised to over 70%, significantly above the prior expectation of 50%. As large-model cluster scale expands, both interconnect usage and value density continue to rise, ensuring future growth will outpace cloud CapEx growth.

The key catalyst for FY28 custom chip revenue doubling is inference workloads—rising KV cache demand is driving sustained upside surprises in NIC and CXL-attached memory requirements.Management has clearly outlined a long-term target of over $10 billion in custom chip revenue by FY29, signaling a clear upgrade in the profitability model.。

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280306666-kZF9nbDqlF.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

2.2 Hong Kong Stock Market

The Hang Seng Index fell 1.65% for the week, constrained by triple headwinds; tactical portfolio rebalancing is preferred over broad index allocation.

The Hang Seng Index declined 1.65% over the full week, with average daily turnover of HK$374.8 billion, up approximately HK$93.3 billion from last week. Southbound Connect recorded net inflows of HK$8 billion overall—but saw a single-day net outflow of HK$7.7 billion on May 27, followed immediately by a net inflow of HK$7.6 billion the next day.Capital flows are reversing rapidly, reflecting pronounced short-term speculative behavior, with southbound funds yet to establish sustained positive feedback.。

The underlying weakness in Hong Kong equities stems from three key constraints:

① Elevated 10-year U.S. Treasury yields (4.49%–4.50%) are suppressing growth valuations;

② Hong Kong’s internet-heavy index tilts toward soft tech, creating a structural mismatch with the global AI capex theme focused on hard tech (semiconductors/high-end manufacturing).

③ External variables (U.S.-Iran negotiations, pace of rate cuts) continue to cause repeated market disruptions.

Need to wait"U.S. Treasury yields decline + substantive progress in U.S.-Iran talks + stable southbound capital inflows"At least two of these conditions must materialize before betting on a broad market rally; currently, tactical portfolio rotation is more suitable, with hardware-related plays, high-dividend stocks, and event-driven sectors relatively favored.

The Hang Seng Index’s forward 12-month P/E ratio stands at 11.44 (as of May 29), indicating continued valuation appeal, though the July lock-up expiration of large LLM-related IPOs could exert short-term pressure on the index. Patience is advised while monitoring for right-side confirmation signals.

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280324747-awEr86mjNo.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

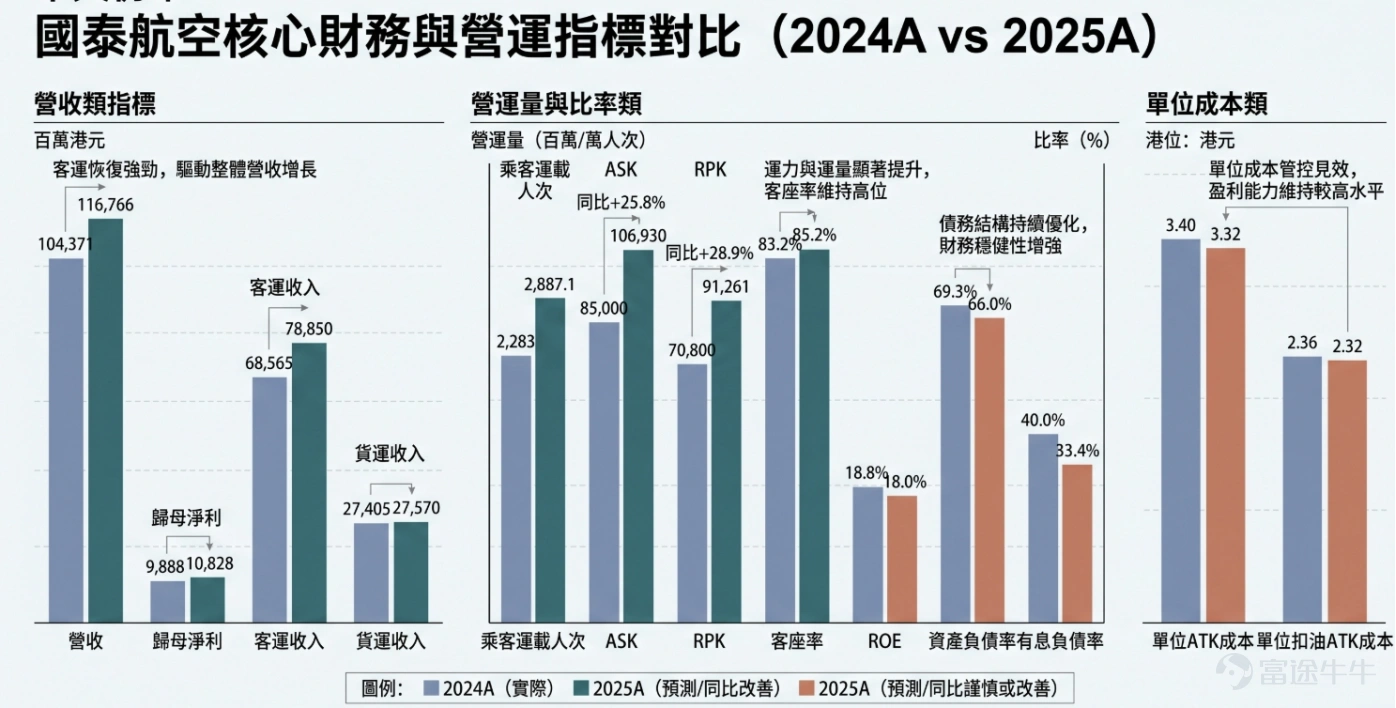

Stock Spotlight – $CATHAY PAC AIR (00293.HK)$ : Middle East tensions are catalyzing demand for direct Asia-Europe flights, with route structure optimization driving profitability.

Benefiting from disruptions to Middle Eastern hub transits caused by Iran-related conflicts, passengers are shifting to direct Asia-Europe routes, which Cathay Pacific is directly capturing—particularly high-end and long-haul travelers. Load factor reached 92.2% in March, nearing peak-season capacity limits. The impact of route optimization far exceeds simple frequency increases; during periods of weak Middle East demand, capacity has already been redeployed to strong-demand European destinations such as Manchester and Rome.The target of approximately 10% year-over-year growth in passenger capacity for full-year 2026 remains unchanged.

Direct Asia-Europe flights are boosting long-haul RPKs and yields, while stronger front-cabin premium demand is improving cabin mix. Synergies between belly-hold and dedicated cargo networks are further enhancing overall flight economics. Cargo tonnage in April 2026 rose 8.2% year-over-year, with a cumulative increase of around 8% for January–April. In May, the company added two A350F freighters to its order book, expanding the total A350F fleet commitment to eight aircraft, continuously strengthening intercontinental cargo capabilities.

Near-term focus: further developments in the Middle East situation and whether peak-season demand on Europe routes can be sustained.

Cathay Pacific Airways (0293.HK) Key Financial and Operational Metrics Comparison

[III. Focus for This Week]

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780279366143-ENLSN8CfbO.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

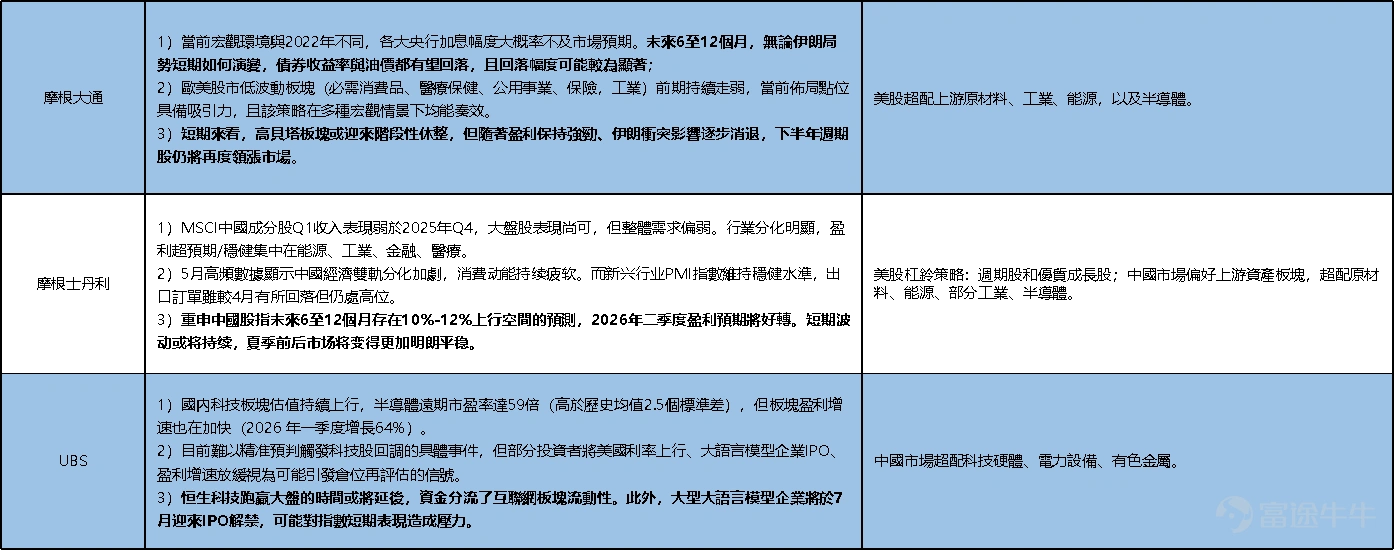

[4. Major bank views]

US Stock Summary:Institutions generally remain cautiously bullish. Market gains are driven by AI earnings realization and the likelihood of geopolitical tensions easing, pushing indices to new highs. High-beta sectors may experience a short-term consolidation phase, but cyclical stocks are expected to lead the market again in the second half of the year as earnings remain robust and the impact of the Iran conflict gradually fades. Over the next 6–12 months, regardless of short-term developments in Iran, both bond yields and oil prices are likely to see a notable decline.

Hong Kong Stock Summary:Hong Kong equities face headwinds from elevated U.S. Treasury yields, structural imbalances in the tech sector, and recurring external uncertainties. At the monthly allocation level, hardware-linked names, high-dividend stocks, and event-driven plays appear relatively favorable. The Hang Seng Tech Index may lag further before outperforming; large-scale LLM company IPO lock-up expirations in July could exert short-term pressure on the index. However, earnings expectations for Q2 are poised to improve, and Chinese assets remain underweight in institutional portfolios. The market is expected to stabilize around summer, and investors are advised to wait patiently for clear right-side signals before adding positions.

Featured Views

[5. Simulated Portfolio]

5.1 Weekly Thesis

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280458222-ttdDI4vmVE.jpeg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

5.2 NAV

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280467941-eivyoFOno8.jpeg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

5.3 Performance Attribution

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280477835-Guovxt7lnK.jpeg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280477836-FG0jQQsUEU.jpeg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Portfolio updated as of May 4

![Guide to this week's strategies for the US and Hong Kong markets: With inflation remaining elevated and rate cuts pushed back to 2027, how should investors navigate the heightened volatility in U.S. equities? Hong Kong stocks remain constrained by three headwinds—where can structural opportunities break through? [Live Stream Reservation] Today at 16:30, Futu’s Chief Investment Research Expert will join you to preview this week’s market outlook and unpack quantum investment opportunities! [Share Link: Two billion dollars poured into the quantum computing race—how to position yourself in the ecosystem?] [I. Macroeconomic Observations] 1.1 International Macroeconomic: PCE inflation hits 3.8% year-over-year, the highest in nearly three years—will the Fed’s rate cut window shift to 2027? U.S. April PCE rose 3.8% year-over-year, matching expectations and marking the highest level since May 2023. Core PCE climbed 3.3% year-over-year, its highest since November 2023. Rising energy prices driven by the Iran conflict were the primary contributor. Personal income stagnated month-over-month (0.0%), and the savings rate fell to a dangerously low 2.6%.Consumers are being forced to 'spend down savings to sustain consumption.' Real consumer spending, adjusted for inflation, rose only 0.1% month-over-month, signaling a clear cooling trend. A hold on rates at the Fed’s June meeting is now widely expected. Some institutions project the first rate cut could be delayed until Q1 2027 (with two 25-basis-point cuts expected in March and June 2027). Additionally, Q1 GDP was revised down to 1.6%, below the initial estimate of 2%, butUnder the scenario of 'slowing growth, resilient earnings, and sustained AI investment,' the foundation for risk assets to remain elevated still exists. 1.2 Domestic Macroeconomics: May PMI fell to the breakeven level, both domestically and externally...](https://nnqimage.futunn.com/sns_client_feed/988889/20260601/web-1780280491632-rzSYhGM78s.jpeg/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Disclaimer

This report has been prepared by Futu Securities International (Hong Kong) Limited (“Futu Securities”). Without the prior written consent of Futu Securities, this report and the information contained herein may not be (i) reproduced, copied, or stored in any form, or (ii) distributed or transmitted directly or indirectly to any other person for any purpose. The information contained in this report is derived from sources that Futu Securities believes to be accurate and reliable as of the date of publication. However, this report is not intended to contain all information necessary for investor decision-making and may be affected by factors such as delivery delays, disruptions, or interception. Futu Securities makes no express or implied representation or warranty regarding the adequacy, accuracy, completeness, reliability, or fairness of any such information or opinions. Accordingly, neither Futu Securities nor its affiliates (collectively, the “Futu Group”) shall bear any liability for any losses of any kind (including, without limitation, direct, indirect, or consequential losses) arising from actions taken by any third party relying on the contents of this report. The views, recommendations, suggestions, and opinions expressed in this report do not necessarily reflect the positions of Futu Securities or its affiliates and are subject to change without notice. Futu Securities undertakes no obligation to update any information or opinions contained herein. This report is provided for general informational purposes only and is intended solely for general reading by clients of Futu Securities, without regard to the specific investment objectives, financial situation, or particular needs of any individual recipient. Nothing contained herein constitutes or should be construed as an offer, recommendation, or solicitation by any member of the Futu Group to buy or sell any securities, investments, or other financial instruments. It should not be interpreted as an offer or invitation to purchase or sell securities. Any decision to purchase securities mentioned in this report should take into account publicly available information, including any applicable prospectuses relating to such securities. The products referenced in this report may not be suitable for all investors. Readers should fully consider relevant factors and seek professional advice before making any investment decisions. This report is provided to each recipient on the basis that such recipient is deemed capable of independently evaluating investment risks and exercising independent judgment in making investment decisions. In certain jurisdictions or countries, the distribution, issuance, or use of this report may contravene local laws, regulations, rules, or other registration or licensing requirements. This report is not intended for distribution to, or use by, any person or entity in such jurisdictions or countries. Hong Kong investors with any questions regarding Futu Securities’ research reports should contact Futu Securities directly. The Central Entity Number of the author’s license issued by the Hong Kong Securities and Futures Commission is disclosed next to the author’s name on the front page of this report. The analyst primarily responsible for preparing this report confirms that: (i) the views expressed herein accurately reflect his or her personal views about the listed corporation(s) covered in this report; and (ii) none of the compensation he or she has received, is receiving, or will receive—directly or indirectly—is linked to any specific recommendations or views expressed in this report. The analyst further confirms that neither the analyst nor any of his or her associates have traded in the securities of the listed corporation(s) covered in this report or related securities during the 30-day period preceding the publication of this report or within three business days following its publication. Neither the analyst nor any of his or her associates serve as senior management of the listed corporation(s) covered in this report, nor do they hold any financial interest in such corporation(s). In this report, Futu Securities holds no financial interest amounting to 1% or more of the market capitalization of the issuer, and has had no investment banking relationship with the company in the past 12 months. None of the employees of Futu Securities are employees of the issuer.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

3