The Endgame Debate in the 3D Printing Industry: Will It Be 'One Dominant Player with Several Strong Competitors' or 'One Dominant Player with Numerous Weak Ones'?

The consumer-grade 3D printing industry is entering a 'golden moment' marked by high prosperity and explosive growth.

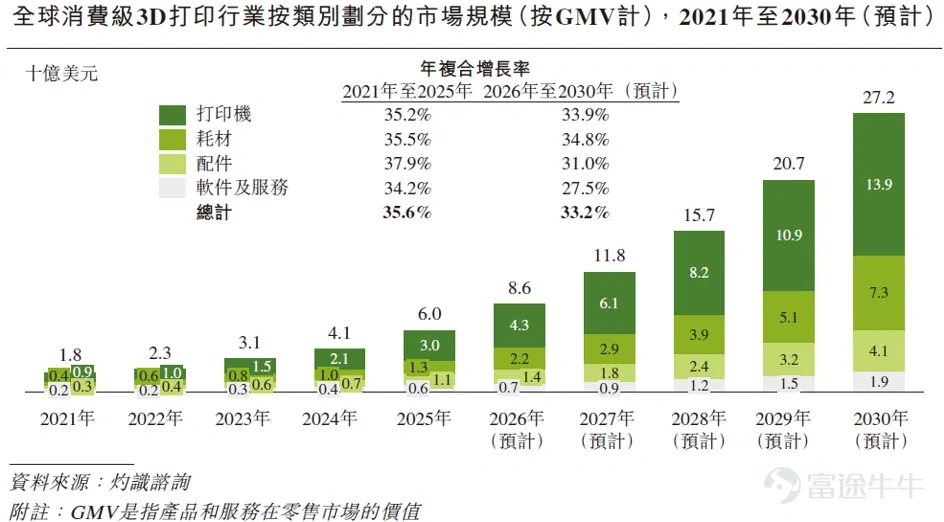

Data shows that the global market size for consumer-grade 3D printing reached $6 billion in 2025 and is projected to grow to $27.2 billion by 2030, representing a compound annual growth rate exceeding 35%. In the first four months of 2026, domestic production of 3D printing equipment increased by over 50% year-over-year, with exports totaling 2.46 million units—double the figure from the same period last year.

In capital markets, China’s primary market raised nearly RMB 10 billion in total funding in 2025, as venture capital firms and industrial investors raced to deploy capital. Once a niche topic among tech enthusiasts, 3D printing has now become a focal investment theme attracting intense interest across the investment community.

Amid this rapid industry expansion, a heated debate over the endgame is intensifying—

Will the endgame for the consumer-grade 3D printing industry resemble that of smartphones—where multiple manufacturers like Apple, Samsung, Huawei, and Xiaomi coexist in competitive balance—or that of consumer drones, where DJI dominates alone while other players struggle to survive?

In other words, will the endgame of consumer-grade 3D printing be characterized by 'one dominant leader with several strong contenders,' or 'one dominant leader with numerous weak players'?

The answer to this question will directly determine the return on the current billions of dollars in invested capital, as well as the allocation of an even larger pool of capital poised to enter the market.

A high-growth industry moving toward concentration: thriving on one side, eliminating on the other

In the first quarter of 2025, global shipments of consumer-grade 3D printers surpassed one million units in a single quarter. Of these, more than 90% came from Chinese companies—specifically, four Shenzhen-based firms: Bambu Lab, Creality, Zeeho, and Anycubic.

Measured by 2025 GMV, Bambu Lab held a market share exceeding 42%, Creality accounted for approximately 11%, and Zeeho and Anycubic each held between 8% and 9%.

In terms of revenue, Bambu Lab surpassed RMB 10 billion in 2025, nearly doubling from the previous year; Creality reported revenue of around RMB 3.1 billion, an increase of over 30% year-over-year; Zeeho generated roughly RMB 2.3 billion, up more than 40% year-over-year; and Anycubic also reached the RMB 1 billion scale.

The concentration among brands is equally evident in the realm of 3D printing farms—professional operations that treat printers as production assets. As of the first half of 2025, China had over 2,000 registered printing farms, with desktop-grade printer installations exceeding 100,000 units, over 70% of which were Bambu Lab devices.

However, even as the industry surges ahead, many manufacturers have quietly exited the market.

In 2025, AnkerMake, a subsidiary of Anker, announced the termination of all its FDM 3D printing operations, less than three years after launching its first product. Around the same time, Spain’s BCN3D filed for bankruptcy, U.S.-based Desktop Metal entered bankruptcy restructuring, Germany’s TRUMPF sold off its additive manufacturing business, and Arburg exited the 3D printing sector altogether.

In the overseas consumer-grade market, brands that once rivaled Chinese firms have been almost entirely cleared out, with only Czech Republic-based Prusa Research retaining a market share of approximately 5.8%.

With highly overlapping supply chains and a compound annual growth rate exceeding 35%, such a market should, in theory, accommodate more players.

Yet in reality, prosperity and attrition are occurring simultaneously, and industry consolidation is becoming increasingly pronounced.

The root cause can arguably be traced back to a single company: Bambu Lab.

System capabilities that cannot be sourced from the supply chain are becoming a watershed moment.

Founded less than six years ago, Bambu Lab has nearly redefined product standards for consumer-grade 3D printing—from print speed and intelligence to out-of-the-box user experience.

Before Bambu Lab emerged, the industry had already been simmering for four or five years in Shenzhen, fueled by supply chain advantages and talent dividends. However, it was only after Bambu Lab launched its X1 series in 2022 that the market truly entered a period of explosive growth.

How did a company founded just six years ago break through among a group of long-established players? This question has been repeatedly asked since the day the X1 launched—and remains as relevant as ever.

The answer may lie beyond hardware specifications.

Bambu Lab’s core team comes from DJI. Founder Tao Ye led development of DJI’s flagship Mavic Pro drone series, and key team members span motion control, machine vision, and systems engineering.

What they brought to 3D printing was something the consumer market hadn’t seen before: vibration compensation algorithms adapted from drone attitude control, enabling printers to self-correct resonance during high-speed operation; miniature LiDAR for first-layer detection, calibrating the very first stroke of each layer with micron-level precision; and a fully in-house motion control algorithm—redefining motion accuracy logic from the ground up.

In a media interview, SmartSpectrum CEO Chen Bo bluntly stated: “Bambu Lab’s software is truly a moat,” adding that his team “would find it extremely difficult to catch up in the short term.” He gave a concrete example: Bambu Lab’s machines maintain consistent precision even after more than a month of use, whereas competitors typically require monthly recalibration. “This is a generational gap at the algorithmic level—not a hardware issue.”

In this industry, software and hardware are completely integrated. Algorithms, sensors, slicing software, cloud-based workflows—if any component falters, the printed output suffers. Software isn’t merely an accessory to hardware; it is an intrinsic part of the product itself.

Moreover, Bambu Lab’s comprehensive ecosystem is another critical factor sustaining its leadership position.

In 2023, Bambu Lab launched its model community, MakerWorld, investing hundreds of millions of yuan annually to subsidize creators and build an incentive system akin to YouTube’s.

This investment has yielded impressive results: MakerWorld now boasts tens of millions of monthly active users, over 300,000 active creators, and a library of more than 2 million models—with nearly 100,000 new models added each month. In less than two years, its monthly traffic has surpassed that of Thingiverse, a veteran community operating for over a decade, and it maintains an 83% one-year user retention rate—a rarity in the hardware industry.

Ultimately, this ecosystem crystallizes into a seamless user experience: a user sees a model on MakerWorld, clicks “Print,” and the printer starts working—no need to download files, understand slicing parameters, or copy data onto an SD card. For someone entirely new to 3D printing, this means the barrier to entry is nearly as low as online shopping.

Such an experience is only possible when hardware, software, and platform layers are fully integrated—the printer natively recognizes model formats from the platform, the platform understands the performance specs of every printer, and the software automatically handles all necessary translation and orchestration tasks in between. Competitors may gradually catch up on hardware specs, but replicating this complete end-to-end workflow—from browsing to finished print—is extremely difficult in the short term.

Bambu Lab MakerWorld Homepage

Shadows Beneath the Prosperity: Global Competition Extends Beyond Products

With product leadership and a mature ecosystem, Bambu Lab and other Chinese companies hold advantages that are unlikely to be shaken in the near term within the industry. But winning the market is just the first hurdle—the real test of going global has only just begun.

Today, consumer-grade 3D printing may well be one of the most extreme examples of China’s hard-tech exports: over 90% of global shipments originate from Chinese companies. When an industry becomes so thoroughly dominated by one country, competition often spills beyond products themselves—politics, regulations, and discourse power all become new battlegrounds.

The open-source controversy in May 2026 was a telling example.

An overseas developer created a third-party tool based on the open-source code of Bambu Studio (Bambu Lab’s slicing and device connectivity software), using existing interfaces to bypass Bambu Lab’s security middleware and directly call its cloud services.

Since the tool was not officially authorized, Bambu Lab subsequently contacted the developer privately and requested the project be taken down. The developer complied, but the incident immediately sparked widespread controversy in overseas open-source communities, thrusting into the spotlight the boundaries between open-source licenses, user freedoms, and cloud security responsibilities.

The incident itself remains contentious, and the industry has yet to reach a consensus.

At the heart of the dispute is not merely whether a third-party tool should be removed. From Bambu Lab’s perspective, cloud connectivity involves user accounts, device control, and service security—areas for which the manufacturer must ensure platform stability. However, within overseas hacker and maker communities, users expect greater freedom to modify and control hardware they have purchased.

This divergence is almost inevitable—the more consumer-grade 3D printing resembles an integrated 'hardware + software + cloud service' ecosystem, the more manufacturers must draw lines between openness, user experience, and security. And once a company assumes the role of industry leader, every decision about where to draw that line will inevitably face intense external scrutiny.

Competition extends beyond products alone. In recent years, Prusa founder Josef Průša has consistently posted lengthy social media commentary urging European and North American users to beware of Chinese 3D printers over data security concerns, while actively advocating for sales restrictions on Chinese devices in the EU and North America. Although such measures remain highly unlikely, the possibility of a 'black swan' event cannot be entirely ruled out.

The open-source controversy may only be the prologue. As devices spread across millions of homes and factories worldwide, and cloud platforms host vast troves of design files and print data, scrutiny of Chinese companies’ data security practices and platform openness will only intensify.

Conclusion

Returning to the initial question: 'one dominant leader with multiple strong competitors,' or 'one dominant leader with numerous weak rivals'?

Industry data shows Bambu Lab’s revenue has surpassed RMB 10 billion, with a net profit margin exceeding 30%. MakerWorld boasts tens of millions of monthly active users and an 83% user retention rate. Competitors openly acknowledge a significant gap in software capabilities, and global rivals are exiting the market in rapid succession. The trend toward market concentration is becoming increasingly evident.

Meanwhile, 3D printing is accelerating its path toward mainstream adoption through multiple channels.

Online, e-commerce platforms and model-sharing communities continue lowering barriers to awareness and usage. Offline, industry players are also making concerted moves—Bambu Lab officially entered 64 Sam’s Club stores nationwide in May 2026 as the exclusive 3D printing brand partner, while rapidly expanding its own retail network in tier-one and tier-two cities; Creality and other companies are also establishing offline experience stores.

When Bambu Lab's 3D printers start appearing on Sam's Club shelves—displayed alongside major international consumer brands and exposed to over 10 million paying members and their households—the category will face genuine, more rigorous mass-market scrutiny.

Overall, both consolidation and mass adoption are accelerating.

The convergence of these two forces is propelling consumer-grade 3D printing into a new phase.

For this high-momentum, high-growth industry, the ultimate question may not merely be whether the landscape evolves into 'one dominant player with several strong contenders' or 'one dominant player with many weak ones.' Rather, it’s about how Chinese companies—having established comprehensive global leadership in technology, ecosystem, and distribution for this category—will continue to evolve and define the next decade of the industry.

*The above content does not constitute investment advice, does not represent the views of the publishing platform, the market carries risks, invest with caution, and make independent judgments and decisions.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1