15:9, the Senate Banking Committee passed the CLARITY Act!

CLARITY Act faces implementation delays, raising risks of postponement and impacting crypto assets

Author: Freya Sun | SFC Central Reference Number: BWS708

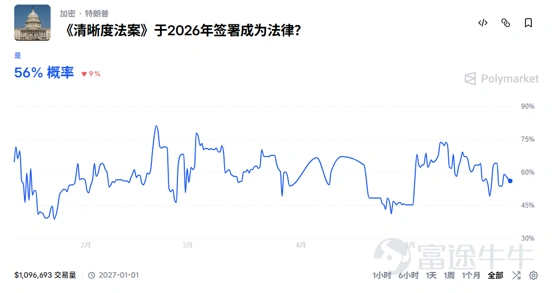

The U.S. Digital Asset Market Clarity Act (CLARITY Act) is indeed facing a clear risk of delayed implementation. Although the bill just passed a vote in the Senate Banking Committee on May 14, 2026,data from Wall Street analytical firms and prediction markets show that the probability of it ultimately passing and becoming law within 2026 has dropped significantly to around 50%.。

In the early hours of May 12, three senators jointly released a new version—the May text—which will serve as the basis for the final vote. The core changes focus on the stablecoin yield issue that had stalled progress for six months (prohibiting passive deposit interest while preserving rewards for trading activity).

I. Core Provisions of the Bill

📌 1. Three-tier Classification Framework for Digital Assets

This framework forms the foundational structure of the entire bill, addressing the question of 'who regulates what':

Digital Securities:Tokens exhibiting characteristics of investment contracts → fall under SEC jurisdiction

Digital Commodities:Decentralized assets not controlled by any issuer (e.g., BTC, Ethereum) → fall under CFTC jurisdiction

Licensed payment stablecoins:Stablecoins pegged 1:1 to fiat currencies (such as USDC, USDT, etc.) → fall under the jurisdiction of banking regulators

1.1 The specific significance of the three-tier classification

① Clarifies the nature of financial products and the regulatory authority’s jurisdiction

$Coinbase (COIN.US)$ , Ripple, and Kraken have been sued by the SEC in recent years—not essentially because they engaged in wrongdoing, but becausethe law never clearly defined what category these assets belong to.Under the SEC’s previous criteria, most tokens met the Howey Test (investment contracts). The core definition of a security is that investors contribute money with the expectation of profits derived from the efforts of others, and most early ICO tokens and governance tokens issued during project launches fell into this category.

This move now draws a clear boundary for the SEC—it should regulate only genuine securities and cannot expand its jurisdiction indefinitely. For example:

In 2012, Ripple issued XRP tokens and sold large quantities to investors and institutions to fund its operations.

In 2020, the SEC sued Ripple,The core allegation is that XRP is an unregistered security. The main argument hinges on the Howey Test: investors spent real U.S. dollars to buy XRP, and all XRP holders clearly expected to profit based on Ripple’s efforts.

However, following the Clarity Act, re-examining this case reveals that in its early days, XRP was under significant control by Ripple and thus qualified as a security;but XRP now has thousands of validator nodes, Ripple’s control has diminished, and it may seek classification as a digital commodity, shifting oversight to the CFTC.

② The Ethereum ecosystem has gained legal legitimacy

Previously, the SEC had suggested ETH might be a security, casting a long legal shadow over the entire Ethereum ecosystem (DeFi, NFTs, Layer 2). However, since ETH is sufficiently decentralized and not controlled by a single issuer, legislative confirmation that ETH is a commodity would grant legitimacy to an ecosystem worth hundreds of billions of dollars.

③ Stablecoins have become regulated payment instruments

Stablecoins pegged to fiat currencies, such as USDC and USDT, are now subject to the GENIUS Act, which imposes comprehensive requirements for issuance, reserves, and audits; stablecoins have evolved from 'unregulated gray-market products' into 'regulated payment instruments,' allowing institutions to hold and use them with confidence.

④ Institutional entry barriers related to compliance have been resolved

Compliance departments at pension funds, insurance companies, and banks follow a strict rule: they avoid assets lacking clear regulatory status. Once the three-tier classification is enacted into law, these compliance teams will finally have clear legal grounds.

📌 2. Yield Allocation for Stablecoins

The current bill still faces significant disagreement over provisions concerning whether stablecoins may offer passive yields or rewards to users through exchanges or intermediaries.Traditional banking lobbying groups strongly oppose this (fearing deposit outflows), causing repeated revisions to the amendment text amid intense stakeholder negotiations.

According to the May version, the bill explicitly **prohibits** interest or yield payments made solely for holding stablecoins, or any arrangements economically equivalent to bank deposit interest. However,activity-based rewards are exempt, allowing the following activities:

Under this legislative framework, Section 404 was passed on May 14 with a compromise text:Banks avoided direct substitution of deposits, and stablecoin firms retained their core reserve interest income, though their pace of subsequent commercial expansion has slowed.

📌 3. Statutory Capital Formation Pathways for Crypto Projects

For the first time, blockchain projects are provided with a legal framework for token offerings (ICO/ITO), moving them out of legal gray areas. Projects can file disclosure documents with the SEC and, upon meeting specified conditions, legally issue tokens to U.S. users.

📌 4. Regulatory Guidance on Tokenized Assets

Provides a framework for tokenization of real-world assets (such as real estate, bonds, and equities on-chain). Traditional Wall Street financial institutions like JPMorgan and BlackRock are already positioning themselves in this space.

📌 5. Developer Protections for DeFi

The bill currently stipulates that developers will not be held liable for platform activities as long as they do not exercise actual control over the protocol.

Take Uniswap as an example: Uniswap is the largest decentralized exchange, with daily trading volumes in the billions of dollars. Uniswap Labs (the development team) wrote the initial smart contract code, but the code is open-source and can be copied and deployed by anyone. The protocol operates automatically via smart contracts without human intervention. Uniswap Labs cannot freeze accounts, issue refunds, or censor transactions; governance authority rests with the community of UNI token holders.

Without this bill, the SEC would have the authority to sue Uniswap, but under the bill’s framework, Uniswap would not be held liable.

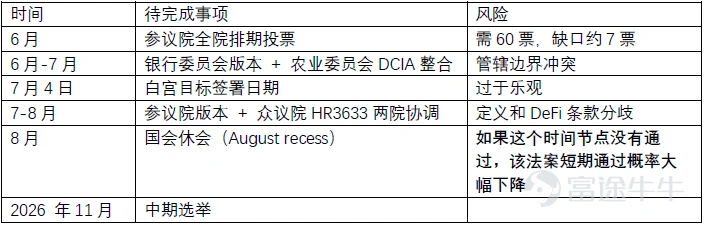

II. Current Obstacles

🚧 1. 60-Vote Threshold in the Senate

A full Senate vote requires overcoming a filibuster, which demands 60 votes. The current composition is as follows:All 53 Republican senators largely support the bill, while only 2 out of 47 Democratic senators on the committee crossed party lines to vote in favor. Approximately 5–7 additional Democratic senators’ support is still needed.. The nine Democratic members of the current committee, who voted against the bill, hold firm positions, making it extremely difficult to secure additional votes during the full chamber stage—this is the key variable determining whether the bill passes.

Polymarket’s current forecast shows the probability of the bill passing has dropped to 56%, with the window of opportunity steadily narrowing.—Congress is currently prioritizing budget and debt ceiling issues, and both parties must prepare for the midterm elections in September.

Senator Moreno has clearly stated: if the bill is not scheduled for a full-chamber vote by the end of May, it will have virtually no chance before the midterms. If efforts resume only after the midterms with the new Congress in 2027, the entire legislative process would need to restart under uncertain political conditions, making passage even less likely.The White House aims to sign the bill by July 4; most observers consider August more realistic, but the risk rises sharply if it extends beyond August.

Data source: Polymarket

🚧 2. Trump Family Conflict of Interest

The Democrats’ core demand is to include a provision prohibiting current government officials from holding or benefiting from crypto assets—a clause directly targeting the Trump family’s World Liberty Financial project—Trump’s sons hold substantial amounts of tokens from this project, whose value is directly affected by cryptocurrency regulation policies.

During the committee vote, the ethics amendment led by Warren was unanimously rejected. Democrats are using this as grounds to withhold support for the full-chamber version. There is little room for compromise on this issue—Republicans will not accept provisions specifically targeting Trump, while Democrats insist on them as a precondition for negotiations.This provision, at the sensitive time ahead of the midterm elections, has become a bargaining chip and weapon to attack Trump, and the Democratic Party will not easily compromise.

🚧 3. Reconciling the two Senate versions will take time

There are currently two parallel Senate versions advancing simultaneously:

🚧 4. Reconciliation with the House version

After passage in the Senate, reconciliation will still be required with HR 3633, which the House passed in July 2025. Key disagreements center on three areas: the regulatory scope for DeFi, the boundary definition between stablecoins and securities, and the treatment of tokenized equities.

III. Impact of the bill’s progress on cryptocurrency-related sectors

📈 Scenario 1: Full passage in June–July (optimistic)

BTC: Confirmed as a digital commodity, enabling institutional compliance and entry

ETH: The biggest beneficiary—SEC jurisdiction eliminated, unlocking the DeFi ecosystem

XRP: The SEC’s litigation rationale completely collapses, resolving all legacy issues

SOL: Benefiting from improved overall institutional sentiment

DeFi tokens: Developer safe harbor enacted, pricing in DeFi legalization premium

$Circle (CRCL.US)$ USDC granted legal status as a 'permitted payment stablecoin,' accelerating institutional adoption. Core driver: increased USDC circulation amplifies reserve interest income

$Coinbase (COIN.US)$ Dual drivers—legal barriers to Base network expansion fully removed + USDC revenue share scales directly with circulation growth

➡️ Scenario 2: Partial passage (most likely, neutral)

The most probable outcome currently is the introduction of a minimum viable version that first passes provisions with bipartisan consensus (e.g., a classification framework for digital assets), while deferring contentious elements such as ethical clauses and protections for DeFi developers.

CryptocurrencyBTC and ETH remain relatively optimistic; XRP still carries uncertainty-driven discount; DeFi performance hinges more on whether developer protection provisions are fully retained

$Circle (CRCL.US)$ Core reserve interest model remains unaffected

$Coinbase (COIN.US)$ Revenue sharing from interest remains unaffected, but Base network expansion still faces uncertainty

📉 Scenario 3: No passage before August (bearish)

The premium tied to optimistic regulatory expectations for 2025 has been erased, and the market is now pricing in legislative gridlock extending through 2030.

IV. Key upcoming milestones 🗓️

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (2)

to post a comment

4

2