Barings: U.S. High Yield Bonds – Navigating the Maturity Wall

U.S. high yield bond issuers face a substantial maturity wall. However, given the current market structure, this maturity pressure appears less daunting for issuers and may present potential opportunities for investors.

In the U.S. high-yield bond market, issuers are facing a significant peak in the 'maturity wall'—a term referring to the aggregate maturity schedule of the bond market—with approximately 20% of bonds set to mature within the next three years and an additional 22% maturing over the subsequent three to four years [1]. With U.S. interest rates remaining elevated, higher financing costs could make it more challenging for issuers to refinance this large volume of maturing debt, particularly if their financial condition or fundamentals are under pressure. This could lead to an increase in distressed debt in the market and, in extreme scenarios, a rise in default risk.

However, while these concerns are valid, they may be somewhat exaggerated and could obscure potential investment opportunities in the market. We believe several factors still help reduce the likelihood of worst-case scenarios materializing.

1. Higher credit quality

Overall, U.S. high-yieldcorporate fundamentals remain solid,particularly as many issuers have consistently strengthened their financial positions in recent years. For example, leverage levels among most U.S. issuers have generally remained moderate, with current net leverage at around 3.6x [2].

This improvement is also reflected inthe credit quality of the U.S. high-yield market, which currently stands near historically high levels.The share of BB-rated issuers has risen to 58%, a notable increase from 49% a decade ago [3]; meanwhile, the proportion of CCC-rated issuers has declined from 13% a decade ago to 9% today. In addition, themarket structure of the U.S. high-yield bond market has also become more resilient., secured bonds currently account for approximately 37% of outstanding debt, a significant increase from 20% a decade ago [4].

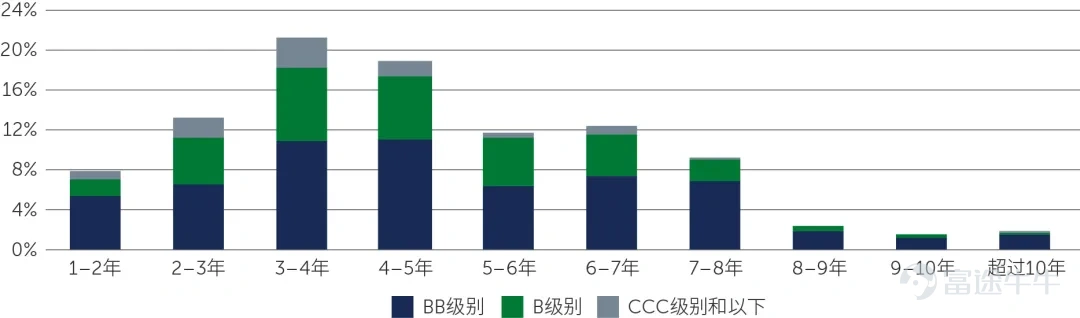

CCC-rated bonds represent a limited share of bonds maturing soon.

Refinancing and default risks are typically concentrated among CCC-rated and lower issuers, as these companies generally have lower interest coverage ratios and higher balance sheet leverage compared to higher-rated firms, resulting in greater debt repayment risk. However,in the upcoming maturities of the U.S. high-yield market, CCC-rated and lower bonds constitute only a small portion.. Among the roughly 20% of issuers facing maturities over the next three years, only about 3% of bonds are rated CCC.(Figure 1)。

Figure 1: CCC-rated bonds represent a relatively small share of U.S. high-yield bonds maturing soon

![U.S. high yield bond issuers face a substantial maturity wall. However, given the current market structure, this maturity pressure appears less daunting for issuers and may present potential opportunities for investors. In the U.S. high yield bond market, issuers are encountering a significant 'maturity wall peak'—referring to the aggregate maturity schedule of the bond market—with approximately 20% of bonds maturing within the next three years and another roughly 22% maturing between years three and six[1]. With U.S. interest rates remaining elevated, higher financing costs could make refinancing this large volume of maturing debt more challenging for issuers, particularly those under financial or fundamental stress. This could lead to an increase in distressed debt in the market and, in extreme scenarios, a rise in default risk. Nevertheless, while these concerns are valid, they may be somewhat overstated and could obscure potential investment opportunities in the market. We believe several factors continue to mitigate the likelihood of worst-case scenarios. 1. Higher Credit Quality Overall, U.S. high yieldcorporate fundamentals remain solid. In particular, many issuers have continued strengthening their balance sheets in recent years—for example, most U.S. issuers have maintained relatively moderate leverage levels, with net leverage currently around 3x...](https://nnqimage.futunn.com/sns_client_feed/26085956/20260527/web-1779846780313-qwuHVcRaei.webp/big?area=2&is_public=true&imageMogr2/ignore-error/1/format/webp)

Source: ICE BofA US Non-Financial High Yield Constrained Index and Bloomberg, as of March 31, 2026.

2. Limited exposure to the software sector

One of the market’s focal points this year has been the potential disruption posed by artificial intelligence. As concerns grew that AI could erode software companies’ business models and profit margins, the sector experienced a notable correction earlier this year, leading to heightened default expectations in related markets.

In this environment,compared to other asset classes, the US high-yield bond market has been relatively less affected by such default risk, primarily because the software sector accounts for only about 3.8% of this market(Figure 2).

Figure 2: The US high-yield bond market is relatively less exposed to default risk from the software sector

![U.S. high yield bond issuers face a substantial maturity wall. However, given the current market structure, this maturity pressure appears less daunting for issuers and may present potential opportunities for investors. In the U.S. high yield bond market, issuers are encountering a significant 'maturity wall peak'—referring to the aggregate maturity schedule of the bond market—with approximately 20% of bonds maturing within the next three years and another roughly 22% maturing between years three and six[1]. With U.S. interest rates remaining elevated, higher financing costs could make refinancing this large volume of maturing debt more challenging for issuers, particularly those under financial or fundamental stress. This could lead to an increase in distressed debt in the market and, in extreme scenarios, a rise in default risk. Nevertheless, while these concerns are valid, they may be somewhat overstated and could obscure potential investment opportunities in the market. We believe several factors continue to mitigate the likelihood of worst-case scenarios. 1. Higher Credit Quality Overall, U.S. high yieldcorporate fundamentals remain solid. In particular, many issuers have continued strengthening their balance sheets in recent years—for example, most U.S. issuers have maintained relatively moderate leverage levels, with net leverage currently around 3x...](https://nnqimage.futunn.com/sns_client_feed/26085956/20260527/web-1779846780368-kkw7Ojx3Uv.webp/big?area=2&is_public=true&imageMogr2/ignore-error/1/format/webp)

Source: Morgan Stanley and Bloomberg, as of March 31, 2026.

3. Issuers have proactively positioned themselves for refinancing

Moreover, many issuers have actively accessed the market ahead of schedule to refinance debt maturing in the near term, thereby alleviating future maturity pressures. Overall,global high-yield bond issuers typically arrange refinancing approximately 12 to 24 months before maturity, as their balance sheets become significantly more sensitive to liquidity once debt shifts from long-term to short-term liabilities.

In 2025, approximately 64% of total US high-yield bond issuance was used to repay existing debt[5]. Refinancing activity is expected to continue dominating new bond issuance this year. Since 2026, more than 50% of transactions have been used for refinancing [6].

Meanwhile, market technicals continue to provide support. Demand from yield-seeking investors remains robust, offering a steady base of buyers for this asset class. Additionally, portfolio managers typically reinvest coupon income back into the market, creating a relatively stable foundation for buybacks. These factors together support new bond issuance and refinancing activity, keeping overall market technicals positive.

‘Early refinancing’ may help enhance returns

This dynamic could significantly impact investments. In the six to twelve months leading up to a refinancing event, total bond returns are more likely to be driven by the refinancing itself rather than movements in government bond yields or spreads. As issuers progressively refinance debt maturing in 2027, 2028, and even 2029, a ‘pull-to-par’ effect will emerge—bonds trading at a discount will be redeemed at par, potentially allowing investors to realize gains from price discounts sooner than implied by standard yield calculations.

This phenomenon implies that investment outcomes could exceed yield expectations. As shown in Figure 3, if a bond maturing in 2029 is refinanced in 2028, it could generate an additional 130 basis points of yield (assuming no default occurs).

Figure 3: Illustration of the pull-to-par mechanism

![U.S. high yield bond issuers face a substantial maturity wall. However, given the current market structure, this maturity pressure appears less daunting for issuers and may present potential opportunities for investors. In the U.S. high yield bond market, issuers are encountering a significant 'maturity wall peak'—referring to the aggregate maturity schedule of the bond market—with approximately 20% of bonds maturing within the next three years and another roughly 22% maturing between years three and six[1]. With U.S. interest rates remaining elevated, higher financing costs could make refinancing this large volume of maturing debt more challenging for issuers, particularly those under financial or fundamental stress. This could lead to an increase in distressed debt in the market and, in extreme scenarios, a rise in default risk. Nevertheless, while these concerns are valid, they may be somewhat overstated and could obscure potential investment opportunities in the market. We believe several factors continue to mitigate the likelihood of worst-case scenarios. 1. Higher Credit Quality Overall, U.S. high yieldcorporate fundamentals remain solid. In particular, many issuers have continued strengthening their balance sheets in recent years—for example, most U.S. issuers have maintained relatively moderate leverage levels, with net leverage currently around 3x...](https://nnqimage.futunn.com/sns_client_feed/26085956/20260527/web-1779846780374-n1cAOcKkrK.webp/big?area=2&is_public=true&imageMogr2/ignore-error/1/format/webp)

Source: Morgan Stanley and Bloomberg, as of March 31, 2026.

Investment Insights

Despite the large and concerning wall of maturities, the U.S. high-yield bond market appears relatively well-positioned to manage this challenge, primarily benefiting froma higher-quality credit profile, relatively low exposure to the software sector, and proactive refinancing strategies by issuers。

In addition,The U.S. high-yield bond market currently has a relatively short duration of approximately three years., which is below the historical market average of 4.15 years [7]. Meanwhile,yield levels remain attractive, currently at approximately 6.9%[8]. These characteristics suggest that this asset class may offer a degree of defensive strength compared to other fixed-income markets. In particular,the U.S. high-yield bond market exhibits relatively favorable breakeven characteristics: assuming a 12-month holding period, U.S. Treasury yields would need to rise by approximately 229 basis points for U.S. high-yield bonds to generate negative returns; by comparison, U.S. investment-grade corporate bonds would require only about 75 basis points, and emerging market sovereign bonds around 107 basis points (Figure 4).

In the current environment of heightened market volatility, this feature is particularly noteworthy: for investors concerned about potential losses from widening credit spreads or interest rate fluctuations,historically, changes in U.S. Treasury yields have had a relatively limited impact on the U.S. high-yield bond market, which provides a degree of confidence.

Figure 4: Breakeven characteristics of U.S. high-yield bonds, highlighting the asset class’s currently attractive yields and relatively low duration

![U.S. high yield bond issuers face a substantial maturity wall. However, given the current market structure, this maturity pressure appears less daunting for issuers and may present potential opportunities for investors. In the U.S. high yield bond market, issuers are encountering a significant 'maturity wall peak'—referring to the aggregate maturity schedule of the bond market—with approximately 20% of bonds maturing within the next three years and another roughly 22% maturing between years three and six[1]. With U.S. interest rates remaining elevated, higher financing costs could make refinancing this large volume of maturing debt more challenging for issuers, particularly those under financial or fundamental stress. This could lead to an increase in distressed debt in the market and, in extreme scenarios, a rise in default risk. Nevertheless, while these concerns are valid, they may be somewhat overstated and could obscure potential investment opportunities in the market. We believe several factors continue to mitigate the likelihood of worst-case scenarios. 1. Higher Credit Quality Overall, U.S. high yieldcorporate fundamentals remain solid. In particular, many issuers have continued strengthening their balance sheets in recent years—for example, most U.S. issuers have maintained relatively moderate leverage levels, with net leverage currently around 3x...](https://nnqimage.futunn.com/sns_client_feed/26085956/20260527/web-1779846780443-mzmXos4xpB.webp/big?area=2&is_public=true&imageMogr2/ignore-error/1/format/webp)

Source: Intercontinental Exchange BofA, JPMorgan, and Barings internal analysis as of March 31, 2026. U.S. high-yield bonds are represented by the Intercontinental Exchange BofA U.S. Non-Financial High Yield Constrained Index; U.S. investment-grade bonds by the Intercontinental Exchange BofA U.S. Corporate Index; developed market sovereign bonds by the Intercontinental Exchange BofA Global Government Index; and emerging market sovereign bonds by the JPMorgan EMBI Global Diversified Index. This analysis is calculated by dividing the 'Yield-to-Worst' by the 'Modified Duration.' Yield-to-Worst refers to the lowest potential yield that can be received on a bond without the issuer actually defaulting. Investment returns are not guaranteed. This analysis is for illustrative purposes only and addresses only the specific factors discussed; it does not encompass all elements and variables that could affect outcomes.

Overall, U.S. high-yield bonds not only offer the potential to outperform what simple yield metrics might suggest, but also provide advantages in downside risk management and portfolio diversification, along with relatively low sensitivity to interest rate volatility. However, risks remain. The U.S. high-yield bond market comprises numerous issuers, and their refinancing risks vary significantly across entities, making security selection critically important. We believe that through an active investment approach, combined with deep market research capabilities and extensive experience, investors can more effectively navigate upcoming challenges and capture potential opportunities.

For the purposes of this document, high-yield bonds refer to those rated below investment grade. Sub-investment grade refers to ratings of 'BB+' or lower by Standard & Poor’s or Fitch Ratings, 'Ba1' or lower by Moody's Investors Service, or equivalent ratings by other internationally recognized rating agencies.

[1] Source: Intercontinental Exchange, Bank of America, and UBS Group, as of February 28, 2026.

[2] Source: CreditSights, as of December 31, 2025.

[3] Source: Intercontinental Exchange, Bank of America, as of April 21, 2026.

[4] Source: Intercontinental Exchange, Bank of America, as of April 21, 2026.

[5] Source: CreditSights, as of March 31, 2026.

[6] Source: CreditSights, as of March 31, 2026.

[7] Source: Intercontinental Exchange, Bank of America, and Bloomberg, as of April 21, 2026.

[8] Source: Intercontinental Exchange, Bank of America, as of April 21, 2026.

Important Information

This document is for reference only and does not constitute an offer or solicitation to buy or sell any financial instrument or provide financial services. The information contained in this document was prepared without considering the investment objectives, financial situation, or specific needs of potential recipients. This document is not, nor should it be considered as, investment advice, recommendation, research, or a commitment. Prospective investors must assess the merits and risks of the investment target independently before making investment decisions. Prior to making an investment decision, prospective investors should seek appropriate investment, legal, tax, accounting, or other independent professional advice.

Unless otherwise stated, the opinions expressed in this document are those of Barings. These views are based on information available as of the date of preparation of this document and may change due to various factors after the publication date; Barings will not provide further notice when updating them. Parts of this document are based on data believed to be from reliable sources. Barings has made every effort to ensure the accuracy of the data contained herein, but makes no express or implied representation or warranty regarding the accuracy, completeness, or adequacy of the data. Any forecasts contained in this document are based on Barings' opinion of the market at the time of preparation, subject to many factors, and may change without further notice.

Investing involves risks. Past performance is not indicative of future results. Investors should not make investment decisions based solely on this material. This document is issued by Barings Asset Management (Asia) Limited and has not been reviewed by the Hong Kong Securities and Futures Commission.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3

1