The United States and Iran are sticking to their respective positions—can peace talks proceed smooth

Options Sir on Macro | Big Week Ahead! US-Iran Deal May Materialize + PCE Data Looms—How to Navigate Markets Next?

After months of a 'hope-disappointment' cycle, U.S.-Iran negotiations finally showed positive signs over the weekend—both sides have 'essentially agreed' on a memorandum aimed at reopening the Strait of Hormuz. The agreement includes extending the ceasefire, holding talks on Iran’s nuclear program within 60 days, reopening the strait, and the U.S. lifting its blockade on Iranian ports.This conflict, ongoing since February 28 and lasting nearly three months, is finally showing the first real signs of a breakthrough.

The volatility of geopolitical maneuvering has caused sharp swings in market sentiment between 'hope' and 'disappointment' over recent months. Nevertheless, oil prices have retreated from their highs, and the earlier 'rate-hike panic' triggered by elevated oil prices is now subsiding.

On the other hand, the upcoming release of the U.S. April PCE price index on Thursday will serve as the next test of market confidence.With both 'geopolitical de-escalation' and 'sticky inflation' now on the table, the macro narrative at the end of May is approaching a critical inflection point.

As oil prices fall, markets

Starting in the second week of May, both CPI and PPI data came in stronger than expected, and with Middle East tensions persistently unresolved, macro trading themes have been dominated by typical inflation concerns—anxiety that quickly spilled over into the Treasury market, which is most sensitive to Federal Reserve monetary policy.

The 10-year U.S. Treasury yield briefly approached 4.69% last week, while the 30-year yield surpassed 5.2%, hitting a new high since 2007, weighing on U.S. equity markets.

This forms a clear transmission chain:Geopolitical conflict → Surging oil prices → Rising inflation expectations → Strengthened rate-hike expectations → Soaring U.S. Treasury yields → Pressure on risk assets。

Now, with renewed prospects for U.S.-Iran negotiations, the oil price anchor has begun to shift lower. WTI crude has fallen more than 15% from its recent peak, and Brent crude has declined in tandem. For the market, this means the first link in the aforementioned transmission chain is starting to loosen.In fact, since Trump hinted last Wednesday that talks had entered their 'final stage,' U.S. Treasury yields and oil prices have been falling in sync, while risk assets have started to recover.

However, caution is warranted: a downward shift in the oil price anchor does not equate to 'problem solved.' Even if a deal is ultimately reached, full resumption of shipping through the Strait of Hormuz will take time—some Middle Eastern oil fields have already sustained damage due to wartime destruction and prolonged shutdowns, and crude reserves and inventories have been significantly depleted over the past several months.

More importantly, Trump’s erratic stance on Iran has left markets consistently skeptical about whether any agreement will actually materialize.This uncertainty implies that the path of declining oil prices will not be smooth; the market must still contend with a new normal of elevated but volatile oil prices.

Will Thursday's PCE data 'spook' the market?

At 20:30 Beijing time on Thursday (May 28), the U.S. April PCE data will be released. Compared to the more widely known CPI (Consumer Price Index), the PCE (Personal Consumption Expenditures) index is the Federal Reserve’s preferred inflation gauge.

The PCE covers a broader and more comprehensive range of expenditures; its component weights are adjusted quarterly based on actual consumer spending behavior, capturing substitution effects more promptly, whereas CPI weights are relatively fixed and updated only once every two years.

Since 2012, the Federal Reserve has explicitly set a 2% annual increase in the core PCE price index as its long-term inflation target. This official endorsement has elevated the PCE beyond a mere economic indicator—it now serves as the statutory benchmark for assessing whether monetary policy has fulfilled its mandate of 'price stability.'Federal Reserve officials almost invariably cite core PCE as their inflation reference in speeches and meeting minutes.

According to market consensus expectations, the year-over-year increase in the April PCE price index could jump to 3.9% from the prior reading of 3.5%, potentially marking the largest two-month cumulative gain since late 2021.

The sources of inflationary pressure are multifaceted: energy prices are undoubtedly the biggest driver—gasoline prices continued rising in April, and airfares climbed for a second consecutive month as airlines kept passing on higher fuel costs; food prices saw broader gains as upstream costs like fertilizer fed through to agricultural production; even surging demand linked to AI has tightened supply of memory chips, pushing up prices for personal computers and related hardware components.

But there’s a key point Sir needs to clarify for fellow investors:The market impact of the April PCE data may not be as significant as you might think.。

First, there’s the data lag.。April CPI and PPI data were already released on May 12 and May 13, respectively, and markets had already fully priced in the renewed inflation concerns at that time, reacting sharply (with U.S. Treasury yields spiking and equities adjusting).Although PCE differs from CPI in methodology, the two measures are highly correlated in trend. The April CPI surprise has already partially 'previewed' the April PCE outcome. In other words, markets have already priced in the 'bad news.' Unless the final release shows a much sharper-than-expected jump—such as core PCE year-over-year rising above 3.5%—the marginal market reaction is likely to be limited.

Second, there’s the policy transmission lag.Even if PCE data does come in hot, the Federal Reserve is unlikely to swiftly initiate rate hikes in June or July.Newly appointed Fed Chair Waller previously stated clearly during his confirmation hearing that the Fed would henceforth favor using the 'trimmed mean' measure to assess inflation.— This method can filter out the impact of extreme volatility, such as oil price swings.

What is this, exactly? In simple terms, it’s the scoring method commonly used in diving competitions: discard the highest and lowest scores, then take the average of the remaining judges’ scores as the athlete’s final score.

Wasserman believes that traditional metrics like core PCE are imperfect. Although they exclude food and energy, other components within the core basket still exhibit high volatility. He advocates using a trimmed mean that dynamically excludes extreme fluctuations, arguing that this better reflects the true underlying inflation trend.If the Federal Reserve shifts its policy anchor from core PCE to trimmed PCE, current inflation would appear significantly more benign, thereby creating room for his advocated interest rate cuts.

Therefore, the market reaction following Thursday’s PCE data release is likely to show a pattern of 'short-term disruption followed by medium-term digestion': if the data surprises to the upside, it may trigger a brief bout of volatility (a temporary spike in U.S. Treasury yields and short-term pressure on tech stocks). However, if oil prices continue trending lower and no major geopolitical shocks emerge, market sentiment should stabilize quickly.

Key focus ahead: Geopolitical developments and the AI investment theme

Beyond the short-term noise from PCE data, the key variable for markets over the coming weeks remains Middle East geopolitical tensions. Although a deal appears 'largely agreed upon,' uncertainties persist due to Trump’s habitual unpredictability, divisions within the Republican Party (with some senators criticizing the perceived leniency toward Iran), and Iran’s insistence on maintaining its stance regarding the scope of nuclear negotiations.

If the agreement is successfully signed and the Strait reopens, oil prices could fall further into the $80–90 per barrel range, substantially easing inflationary pressures and diminishing expectations for Fed rate hikes—paving the way for another leg up in U.S. equities, particularly tech stocks. Conversely, if negotiations collapse and conflict escalates, oil prices could rebound, reigniting stagflation concerns that would once again dominate market sentiment.

Aside from geopolitical turbulence, AI remains the strongest market-driving theme. Within AI-related investments, market focus is currently concentrated oncritical bottleneck segments of the AI supply chain—such as CPUs, memory chips, and optical communications.

Although positioning has become relatively crowded, the current rally in tech stocks is driven by earnings rather than sentiment—the S&P 500 Information Technology sector reported earnings growth of over 40% in Q1. This suggests that any near-term pullback is more likely to be structural and temporary rather than a trend reversal.

The core narrative going forward follows a clear logical chain:Geopolitical developments determine short-term shifts in risk appetite and capital flows, while the depth and breadth of the AI theme dictate the resilience of economic growth and the market’s upside potential.。

Options Strategy

The market currently exhibits a 'tale of two extremes' structure: on one hand, $SPDR S&P 500 ETF (SPY.US)$ market-wide volatility remains low amid easing geopolitical tensions but unclear directional conviction; on the other hand, implied volatility (IV) for popular AI-related stocks remains elevated, reflecting both overbought risks and persistent long-term momentum. Below are several targeted options strategies for consideration:

(1) Broad-market ETFs: hedge against 'black swan' events in a low-volatility environment

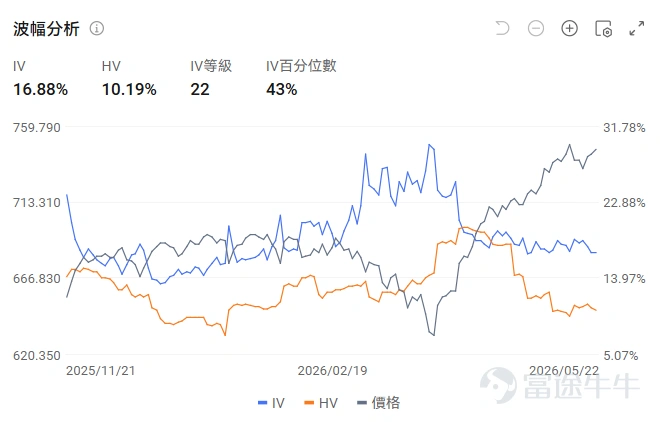

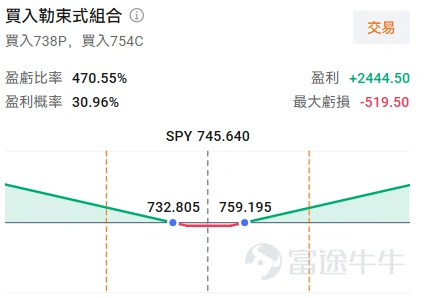

Futubull’s options analytics tool shows that SPY’s IV Rank is 22 and its IV Percentile is 43%, indicating overall neutral-to-low implied volatility. Considera long strangle strategy—simultaneously buying out-of-the-money call and put options with the same expiration date but different strike prices. The core rationale of this strategy is to go long volatility: it profits when the underlying asset experiences a significant price move, regardless of direction.

(The design images displayed on the screen are for demonstration purposes only and do not constitute any investment advice or guarantee; market movements are frequent, and the illustrated option prices do not represent actual conditions)

Note, however, that if the PCE data aligns with expectations and market volatility remains subdued, this strategy will incur a loss.

(2) Hot AI Stocks: An 'Enhanced Income' Strategy Under High Concentration

The AI sector is currently the market's strongest theme, with implied volatility (IV) of popular AI stocks at elevated levels. Taking $Micron Technology (MU.US)$ as an example, its IV has been steadily rising over the past month and, despite a slight pullback in recent trading sessions, remains high—significantly above the broader market’s volatility. In such a high-volatility environment, option sellers can collect higher premium income, giving the Covered Call strategy a natural advantage.

The core of the Covered Call strategy lies in selecting the strike price—a trade-off between 'retaining upside potential' and 'earning premium income':

Sell deep out-of-the-money (OTM) calls (strike price far above current price): Generates lower premium income but preserves most of the upside potential. Suitable for investors strongly bullish on the stock price.

Sell at-the-money (ATM) calls: Offers the highest premium income but caps upside potential. Ideal for investors expecting the stock to trade sideways or rise modestly in the short term.

Sell slightly out-of-the-money (OTM) calls: This is the most commonly used balanced approach, striking a compromise between earning reasonable premium income and preserving upside potential.

A covered call is a strategy that allows you to maintain your position and capture some upside gains while enhancing cash flow by selling call options. However, be aware that if the stock price surges significantly, your shares may be called away at the strike price.

Finally, here's a small perk for fellow Futubull investors, welcome to claim it.Options Beginner Pack

*This event is exclusive to invited HK users. Click to learn more.Detailed event rules>>

Market conditions are complex and volatile,Options StrategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options Strategymaking investing simple and efficient!

Option Risk Warning:An option is a contract that grants the holder the right, but not the obligation, to buy or sell an asset at a fixed price on a specific date or at any time before that date. The price of an option is influenced by various factors, including the current price of the underlying asset, the strike price, time to expiration, and implied volatility. Implied volatility reflects the market’s expectations for the level of volatility in the option over a future period. It is a data point derived inversely from the Black-Scholes option pricing model and is generally regarded as an indicator of market sentiment. When investors anticipate greater volatility, they may be more willing to pay a higher price for options to hedge risks, resulting in higher implied volatility. Traders and investors use implied volatility to assess the attractiveness of option prices, identify potential mispricings, and manage risk exposure.

Disclaimer:This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in trading options can be substantial. In some cases, losses may exceed the initial margin deposited. Even if you set contingent orders such as 'stop-loss' or 'limit' orders, these may not prevent losses. Market conditions may make such orders unexecutable. You may be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any shortfall in your account. Therefore, before trading, you should study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures for exercising options and the rights and obligations upon exercise and expiration. Options trading carries extremely high risks and is not suitable for all investors. Investors should carefully readCharacteristics and Risks of Standardized Options。

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (3)

to post a comment

29

28