SpaceX stock on a rollercoaster ride—how to position in space-related equities?

Tengsi · IPO Analysis | Valuation Quadruples in 11 Months! SpaceX: The Valuation Paradox Behind the Biggest IPO in History—Is It a Value Opportunity or a Valuation Trap?

Image source: Publicly available data, compiled and reorganized by Gaoteng

An astronomical-number spectacle defying conventional wisdom

When a company that posted nearly $5 billion in losses last year is racing toward what could be the largest IPO in human history with a $1.75 trillion valuation, what does this figure really mean?

SpaceX Revenue by Segment

$1.75 trillion,roughly equivalent toOne company's $Tesla (TSLA.US)$ market capitalization equals one-third of the UK's annual GDPhalf、one-third of $NVIDIA (NVDA.US)$ , and that company is none other than SpaceX—the one building rockets to Mars.

For Hong Kong investors, when that stock with ticker symbol $SpaceX (SPCX.US)$ is listed on the Nasdaq exchange on the evening of June 12 Beijing time, a fundamental question naturally arises:

—in this IPO extravaganza valued atUSD 75 billion, are we standing at the starting point of a historic wealth distribution event, or merely the final buyers left holding the bag after more than a decade of private market euphoria?

First layer of analysis: sky-high valuations for loss-making companies—arithmetic or art?

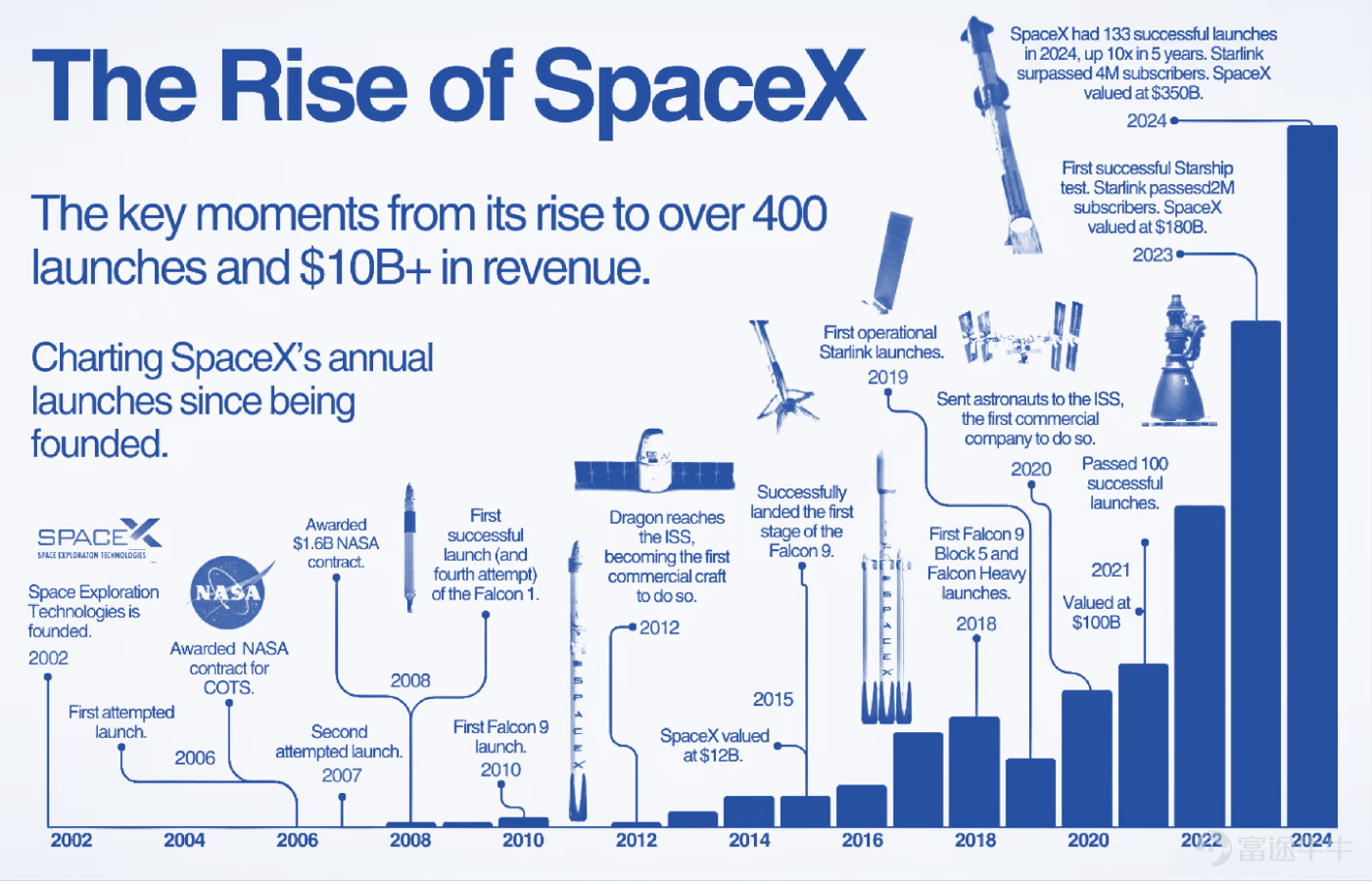

To understand why SpaceX has stunned the world with a $1.75 trillion valuation, one must first recognize how remarkably simple its original mission was when Elon Musk founded the company in 2002 with $100 million from the sale of PayPal—to reduce the cost of rocket launches and ultimately make humanity a multiplanetary species.

From the first three Falcon 1 launches all ending in explosions to the company teetering on the brink of bankruptcy in 2008, and then its dramatic turnaround with a $1.6 billion NASA resupply contract on the fourth attempt, this nearly defunct rocket startup forged a legendary path rising from the ashes.

However, it is the three pivotal moments that truly reshaped SpaceX’s destiny—and these are precisely the keys to deciphering its valuation framework.

First,In 2015, the Falcon 9 rocket's first stage was successfully recovered, reducing launch costs to 5%–10% of traditional methods and fundamentally reshaping the competitive landscape of the global commercial launch market. Today, SpaceX accounts for nearly half of all orbital launches worldwide.nearly half of all orbital launches worldwide;

Second,In 2019, the Starlink program began large-scale deployment. This global internet infrastructure, built with thousands—even tens of thousands—of low Earth orbit satellites, had surpassed 10 million users by February 2026, covering over 160 countries and regions, generating $11.4 billion in annual revenue, which accounts formore than 60%, meaning SpaceX’s most profitable business is no longer launching rockets, butcollecting network fees like a telecom operator;

Third,In February 2026, it acquired Musk’s AI company xAI through an all-stock transaction, causing the combined entity’s valuation to surge to$1.25 trillion, giving the company the imaginative wings of artificial intelligence.

Precisely for this reason, today’s analysts no longer view SpaceX as merely a rocket manufacturer, but as an integrated space infrastructure operator combining launch capabilities, satellite internet coverage, and AI computing power—investors are willing to pay 94 times its revenue for every dollar of income it generates.

In comparison, $Apple (AAPL.US)$ has a price-to-sales ratio of only about 9.5x, $Alphabet-A (GOOGL.US)$ 11.3x, Tesla 16.2x. This stark valuation gap reflects not current profits, but the market's expectation that Starlink will generate monopolistic cash flows in scenarios beyond terrestrial network reach—such as远洋 cargo ships and commercial aircraft—andorbital AI data centersa currently still-PPT-stage yet highly disruptive vision that commands a sci-fi premium.

Second-layer analysis: Why is Elon Musk, who took Twitter private for $44 billion, returning to the public markets?

Elon Musk’s relationship with public companies has always been describable as"Mutual annoyance"A precise four-character summary.

Although Tesla, which went public in 2010 at an IPO price of $17, has generated a staggering return of approximately 360x to date, Musk has repeatedly expressed his disdain for being a public company. The requirement to file quarterly reports every 90 days, Wall Street analysts scrutinizing profit margins, short-sellers waiting to pounce, and media magnifying every misstep—all these constraints are undoubtedlya suffocating braking system。

for the famous 2018"considering taking Tesla private at $420"tweet that triggered an SEC lawsuit, ultimately resulting in a settlement where Musk stepped down as chairman;

and in 2022, he took it private for$44 billionCompletedTwitterand drastically cut roughly 80% of staff, subsequently renaming itX, to some extent, is precisely a concrete manifestation of his attempt to escape public market regulation.

So here's the question:Why would someone so deeply averse to the public company system push his most prized asset, SpaceX, toward the public markets?

The answer has nothing to do with sentiment or personal preference—it’s purely driven by capital needs. Musk’s ambitions are simply too expensive to fund.

Starshiprequires tens of billions, if not hundreds of billions, of dollars to transition from testing to commercial operations,StarlinkMaintaining its current scale requires launching approximately 2,000 replacement satellites annually, and further expansion demands even greater launch investments.

And that grand vision ofbuilding AI data centers in orbit—using solar power to solve energy needs and the cold environment of space to handle coolingcould require funding on the order of hundreds of billions of dollars, far exceeding the cost of any terrestrial data center imaginable.

SpaceX has raised only about $12 billion in total private funding over its more than 20 years of existence, yet this IPO alone aims to raise $75 billion—a scale of capital that only public markets can supply in such a short time.

Thus, Musk doesn't just want to go public—he needs to go public.

This is precisely the fundamental internal contradiction at the heart of what could be the largest IPO in history.

Third-level deconstruction: Structural risks of low free float and the passive investor's prisoner's dilemma

This IPO features an extremely unusual structure: SpaceX plans to sell only about4.3%of its shares, meaning that based on a $1.75 trillion valuation, investors in the public marketwill have access to an extremely limited pool of freely tradable stock.。

Historically, such low free-float structures have repeatedly caused price distortions—for example, Saudi Aramco’s 2019 IPO sold only 1.5% of its shares; although its stock jumped 10% on the first day, it subsequently underperformed, trading around 27 Saudi riyals today versus its IPO price of 32 riyals, yielding an annualized return of only about 1.7% including dividends.

Even more concerning is that $NASDAQ (NASDAQ.US)$ has just revised $NASDAQ 100 Index (.NDX.US)$ rules, which eliminated the hard requirement that a stock must have a free-float of at least 10% to be included in the index, meaning SpaceX could soon be added. When that happens, over $600 billion in passive tracking funds will automatically buy it.

Many industry professionals have publicly questioned this move, arguing it forces passive investors to buy SpaceX at high prices without sufficient information—akin to a surreal scenario where one concert ticket is available but a million people are lining up to grab it.

Fourth Layer of Analysis: Finding Investment Benchmarks from the Joys and Sorrows of History’s Largest IPOs

Let’s turn our attention to those once highly anticipated mega-IPOs in financial history:

Saudi Aramco raised $29.4 billion in its IPO—the largest ever—and its share price remains below its offering price to this day;

Second, $BABA-W (09988.HK)$$Alibaba (BABA.US)$ Alibaba raised $21.8 billion in 2014 as the pride of China’s internet sector, drawing massive attention on its listing day, yet its share price today still trades below its IPO price;

Third, $SoftBank Group (ADR) (SFTBY.US)$$SoftBank Group (9984.JP)$ raised $21.3 billion in 2018 and has underperformed the broader market ever since...

— Among the eight largest IPOs in history, it seems only Facebook $Meta Platforms (META.US)$ achieved a remarkable outperformance against the market.

This story reveals that even strong companies can see their stock decline after a massive IPO—the real key lies in whether investors are speculating or investing.

Returning to SpaceX itself, perhaps the most intriguing card it holds for public market investors is precisely the one that sounds utterly implausible:Space-based AI data centers—in a sense, this represents the latest uncertainty and newest risk premium opportunity SpaceX offers to the public.

Just as the success of Falcon rockets didn’t guarantee Starlink’s success, and Starlink’s success doesn’t guarantee the success of space-based data centers, it is precisely this layered uncertainty that prevents SpaceX from resting on past achievements to collect predictable returns on growth. Instead, it continues to earn returns by taking existential risks.

For investors with deep research capabilities and patience for long-term holding, this may very well be the source of excess returns.

In conclusion

Viewed through the lens of Hong Kong investors’ familiar IPO subscription logic, SpaceX’s IPO presents an exceptionally rare contradiction:

a company that holds a dominant monopoly in the global commercial launch market, whose satellite internet user base is growing exponentially, and whose founder has a legendary track record of turning science fiction into reality.

—yet simultaneously carries an extremely high valuation premium, minimal free float, a founder deeply distrustful of public company governance, and an unproven narrative around space-based AI.

For short-term IPO investors accustomed to chasing first-day premiums, low float combined with frenzied market sentiment could trigger a sharp short-term price surge. However, such extreme valuations are often built on the fragile assumption that all of the following conditions hold true simultaneously: Starlink subscribers continue doubling, Starship achieves commercial success, orbital AI data centers in space are successfully deployed, and Elon Musk’s public statements and physical health remain problem-free. If just one of these assumptions fails, the valuation could collapse as rapidly as it rose.

In financial history, companies that have managed to sustain extreme valuations and still delivered long-term profits for investors are exceedingly rare—Facebook succeeded, and Tesla arguably did too, but these two names survived out of hundreds, if not thousands, of failed ventures.

In reality, that $1.75 trillion figure remains purely speculative at this point. What investors truly need to consider is this: when you finally hold SpaceX shares in your hands, are you buying the next Tesla or the next Alibaba? Only time will deliver the final verdict on this question.

Beyond IPO speculation, we’ll always be right here $GaoTeng WeInvest Money Market Fund (HK0000478930.MF)$$GaoTeng WeValue USD Money Market Fund (HK0000584752.MF)$Waiting for you here.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

17

18