Unitree IPO plus Jensen Huang's endorsement—will robotics stocks undergo a revaluation?

Unitree's first-quarter profits halved, as the Spring Festival Gala proved too costly! Its former biggest rival is also going public.

Source | Deep Blue Finance

According to the latest reports, the highly anticipated Unitree Technology will appear before the listing review committee on June 1, seeking to raise RMB 4.202 billion.Its humanoid robot shipments exceeded 5,500 units, capturing a global market share of 32.4%.Revenue surpassed RMB 1.708 billion, with non-GAAP net profit exceeding RMB 600 million, representing growth of over 335%.

However, in 2026, the company’s growth has significantly slowed. According to its latest prospectus, year-over-year revenue growth in the first quarter plummeted from 332.64% in the prior year to just 68.49%, while non-GAAP net profit declined by 52.55%. The company attributes this to cooling industry enthusiasm, intensified market competition, and a surge in expenses driven by brand promotion activities—including preparations for the Spring Festival Gala—and increased R&D investment.

This spring-summer transition period has seen two Hangzhou-based robotics companies step up to the threshold of capital markets, painting the most vivid—and contrasting—picture of China’s embodied AI industry.

DeepRobotics, once dubbed 'Unitree’s biggest rival,' has had its STAR Market IPO application accepted and is one of the so-called 'Hangzhou Six Dragons.' Yet its prospectus reveals a surprising figure: in all of 2025,it sold only one humanoid robotgenerating approximately RMB 820,000 in revenue, which accounted for less than 0.3% of total income.

The two companies started from similar positions—both entered the market through quadrupedal robots and are based in Hangzhou. However, their diverging paths thereafter have led to strikingly different IPO stories today.

01 Unitree’s Q1 profit halved: The Spring Festival Gala was too costly!

From 2023 to 2025, Unitree Technology delivered explosive growth, with a compound annual revenue growth rate of 226.78%, increasing from RMB 159 million in 2023 to RMB 16.99 billion in 2025. In 2025, its net profit attributable to shareholders of the parent company, after deducting non-recurring gains and losses, reached RMB 5.91 billion, and the gross margin on core operations rose to 60.13%, reflecting continuous financial improvement.

However, in the first quarter of this year, the company’s performance hit a clear inflection point. It reported Q1 revenue of RMB 4.23 billion, with net profit after deducting non-recurring items falling to RMB 402.536 million from RMB 848.365 million in the same period last year—a year-over-year decline of 52.55%.

The company explicitly noted that the sharp drop in net profit after deducting non-recurring items was primarily due to a significant increase in period expenses, including R&D and sales expenses. R&D expenses rose by RMB 383.28 million year-over-year, while sales expenses surged as the company leveraged high-visibility platforms such as the 2026 CCTV Spring Festival Gala for brand promotion to solidify its market influence.

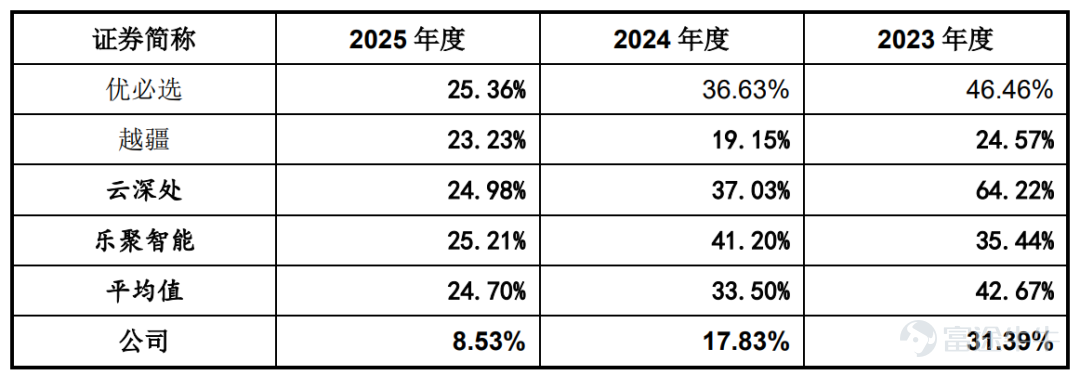

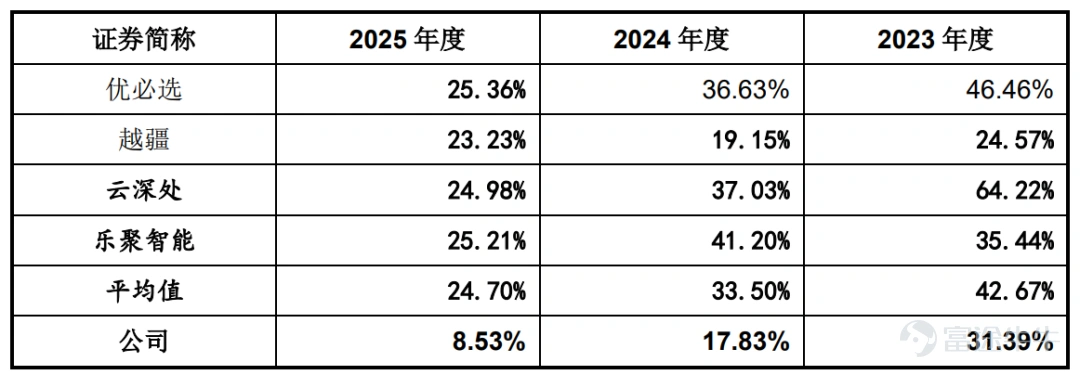

Industry R&D expense ratio comparison, source: Unitree Technology's prospectus

The company expects that as its revenue base continues to expand and industry hype gradually cools, future growth rates will be difficult to sustain at the high levels seen during the reporting period. It forecasts H1 2026 revenue of approximately RMB 10.52 billion to RMB 11.28 billion, representing a year-over-year increase of about 35.62% to 45.41%. Net profit after deducting non-recurring items is expected to decline by approximately 6.43% to 21.97% year-over-year, though this represents a significant narrowing compared to the Q1 decline.

From a product mix perspective, humanoid robots have become Unitree Technology’s largest revenue driver. In 2025, humanoid robot revenue reached RMB 8.68 billion, accounting for 51.78% of core business revenue—up significantly from 27.68% in 2024—while quadrupedal robot revenue totaled RMB 6.98 billion, or 41.62% of core business revenue. During the reporting period, the company sold over 33,000 quadrupedal robots cumulatively, maintaining the global market share leadership for multiple consecutive years; it also sold 5,632 humanoid robots cumulatively, with over 5,500 units shipped in 2025 alone, ranking first globally.

In terms of product portfolio, the company has established a comprehensive lineup covering full-size (H1, H2) and mid-to-small-sized (G1, R1) humanoid robots, as well as industrial-grade (B-series, A-series) and consumer-grade (Go-series) quadrupedal robots. The G1 mid-size humanoid robot starts at RMB 85,000, while the R1 Air model starts at RMB 29,900, continuously lowering the barrier to market entry. Overseas revenue consistently accounted for over 40% across all periods of the reporting timeframe, reaching RMB 7.32 billion in overseas core business revenue in 2025.

The proceeds from this fundraising are intended for four projects, totaling approximately RMB 4.2 billion: the Intelligent Robot Model R&D Project (RMB 2.022 billion), the Robot Body R&D Project (RMB 1.11 billion), the New Intelligent Robot Product Development Project (RMB 445 million), and the Intelligent Robot Manufacturing Base Construction Project (RMB 624 million). Among these, the model R&D project is the largest in scale and will focus on developing embodied large models (the 'brain') and body-intelligent models (the 'cerebellum'). The manufacturing base construction project will acquire approximately 78,700 square meters of self-owned production facilities and introduce automated assembly lines and intelligent warehousing systems to address capacity constraints at current leased factories.

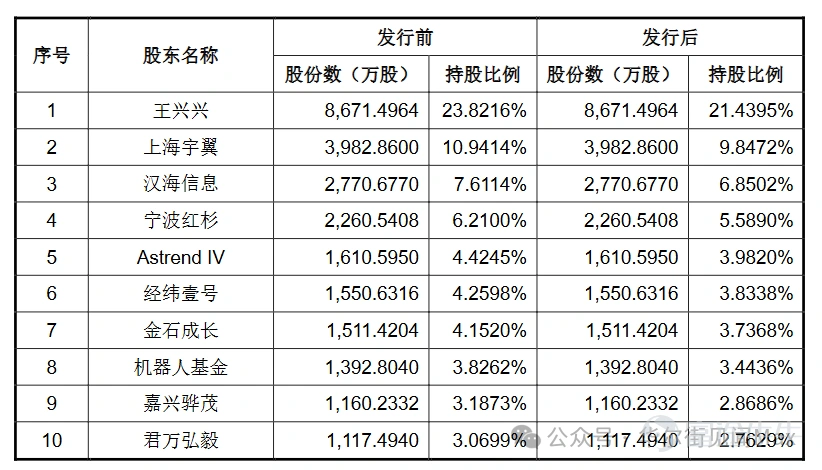

Unitree Robotics boasts an impressive shareholder lineup, bringing together numerous top-tier investors. According to its prospectus, over 30 renowned institutions—including Tencent, Meituan, Sequoia China, Matrix Partners China, China Mobile Hecuang, and Shenzhen Capital Group—are shareholders of the company. Founder Wang Xingxing directly holds 23.82% of shares and, through a special voting rights structure, controls 68.78% of the voting rights, firmly maintaining strategic control over the company. Meituan is Unitree’s second-largest shareholder, with its affiliated entities collectively holding 9.6488% of shares.

Unitree Robotics is facing intensifying competitive pressure. Tesla’s Optimus Gen-3 has announced the start of small-scale trial production, and multiple domestic automotive and consumer electronics manufacturers have officially entered the humanoid robotics space. Additionally, as of January 31, 2026, the company held only 20 domestic invention patents. The prospectus explicitly warns that this limited patent portfolio may be insufficient to effectively mitigate risks of technology infringement. The company has also recently faced a series of patent lawsuits filed by Hangzhou Luwei Meiri Chemical Co., Ltd.; however, it has won both the first and second instance rulings, and the China National Intellectual Property Administration has declared all patents involved in the litigation invalid.

02 "Unitree's biggest rival," DeepRobotics, generated RMB 300 million in revenue solely from robotic dogs

Founded in 2017, DeepRobotics has not only been included among the 'Hangzhou Six Unicorns,' but is frequently compared side-by-side with Unitree in public discourse, often dubbed 'Unitree’s biggest rival.' Its founding team originated from Zhejiang University’s robotics laboratory. From the outset, it avoided chasing mass-market appeal and instead deployed robots in complex, demanding, and stability-focused scenarios such as power grid inspection, industrial operations, and emergency rescue. Its clients include State Grid Corporation of China, China Southern Power Grid, Baosteel, and Singapore’s SP Group.

This pragmatic strategy has delivered tangible financial returns. Between 2023 and 2025, DeepRobotics’ revenue grew from RMB 50.11 million to RMB 337 million, achieving a two-year compound annual growth rate of nearly 160%. In 2025, it reported its first-ever net profit of RMB 28.68 million, and operating cash flow also turned positive at approximately RMB 63.75 million. The company has cumulatively produced over 5,500 robots, with quadruped and wheeled-legged robots contributing more than 95% of its core revenue.

By industry application revenue in 2025, DeepRobotics ranked first globally in the quadruped robot market, followed by Unitree in second place and Boston Dynamics in third. In other words,DeepRobotics achieved RMB 300 million in revenue—and turned profitable—without relying on humanoid robots, selling only robotic dogs.

However, it is not avoiding humanoid robots entirely. In 2024, it launched the DR01, followed by the DR02 in 2025, positioning it as the 'world’s first industrial-grade all-weather humanoid robot' with an IP66 rating, capable of operating in environments ranging from -20°C to 55°C. This continues its consistent strategy: entering B2B scenarios first to solve practical operational challenges in power, emergency response, and industrial settings—rather than promoting a vision of 'robots in every household.'

The challenge lies in the rapidly heating-up humanoid robotics sector. If growth in its quadruped business slows while humanoid robots fail to scale in time, DeepRobotics risks a gap in its 'second growth curve.' Its IPO was backed by profitable robotic dogs, but post-listing, it must prove it can extend this capability to larger robot product lines.

Although the two companies have taken different paths, both have demonstrated strong profitability. Unitree Robotics achieved a gross margin of 60.13% in its core business in 2025, driven by its dual focus on humanoid and quadruped robots along with scaled shipments—a figure that has risen steadily year-over-year (44.22% in 2023). DeepRobotics reported a consolidated gross margin of 52.83% in 2025 (up from 38.76% in 2024). While slightly lower than Unitree’s, its core products in the industrial-grade quadruped robot segment consistently maintain a high gross margin range of 54% to 57%.

03 Conclusion

DeepRobotics quietly profits from robotic dogs and, despite selling only one humanoid robot, dares to pursue an IPO; Unitree leads global humanoid robot sales and sees explosive revenue growth but faces questions over insufficient R&D investment. Both paths are reasonable in their own right—and each carries its own risks.

DeepRobotics’ challenge lies in whether it can successfully transfer its B2B application expertise from quadrupeds to humanoids, avoiding becoming forever known as just a 'robotic dog company.' Unitree’s challenge is whether it can move beyond sales volume and market buzz to truly master embodied large models, enabling its robots to evolve from merely 'running and jumping' to genuinely 'understanding and making decisions.'

An IPO is not the finish line—it’s the starting point of a new race.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment