Waller's new policy measures are in the works! How should investors respond?

With Waller taking office alongside a US-Iran ceasefire, can markets really breathe a sigh of relief?

Key Points

Waller’s election as the 17th Chair of the Federal Reserve marks a shift from Powell’s data-dependent approach toward a reform-oriented framework. However, his policy philosophy fundamentally conflicts with Trump’s push for rate cuts to support midterm elections—a tension that likely ensures their 'honeymoon period' will be short-lived. Waller will seek a balance acceptable to both sides while safeguarding the central bank’s independence. Meanwhile, global bond markets are undergoing a storm far exceeding typical cyclical adjustments. At its core, this turmoil stems from a negative feedback loop: geopolitical conflicts have fueled inflationary pressures and heightened concerns over fiscal sustainability, triggering a concentrated market reaction. Compounding this, long-standing structural supply-demand imbalances in global debt markets continue to deteriorate, significantly weakening the traditional rationale for buying so-called risk-free assets. More alarmingly, the true driver of global economic activity and asset prices may not be the federal funds rate—as widely assumed—but rather the MOVE Index (a gauge of U.S. Treasury market volatility). In the current adjustment, the MOVE Index has surged abnormally, highlighting acute liquidity stress in bond markets. Should it climb further into the high-volatility zone above 120, a systemic liquidity crisis could ensue. Against this backdrop, although a U.S.-Iran ceasefire agreement appears close to realization, the phased verification mechanism—based on reciprocal actions—coupled with stark misalignments in each side’s core demands and Israel’s strong opposition, suggests that geopolitical risks may merely be postponed rather than eliminated. Even if an agreement is reached, the oil price anchor is unlikely to quickly revert to pre-conflict levels, meaning inflationary pressures will persist.

Under the triple pressures of the Fed’s policy pivot, mounting bond market risks, and反复 geopolitical maneuvering, global markets now rest in a fragile equilibrium dominated by geopolitical expectations: near-term risk sentiment remains supported by optimistic hopes of a deal, yet persistent concerns over high inflation, elevated interest rates, and fiscal sustainability remain unresolved. In the short term, market focus centers on three key issues: first, the finalization and implementation of the U.S.-Iran memorandum of understanding; second, how the Fed under Waller calibrates its policy stance between inflation control and economic growth; and third, whether extreme volatility in global bond markets could trigger a systemic liquidity crisis. From a trading perspective, there may be little need to fixate on Monday’s opening price—instead, observe the true market pricing once Eastern U.S. liquidity returns.

Risk warnings: Geopolitical conflict escalates beyond expectations; extreme volatility risk in Japanese government bond markets; uncertainty surrounding internal Fed reforms

Weekly Market Reflections

Global Bond Market Turmoil: The Convergence of Geopolitical Shocks and Fiscal Negative Feedback

On May 22 local time, Waller was elected the 17th Chair of the Federal Reserve by a narrow margin and sworn in at the White House East Room—the first Fed Chair since Greenspan in 1987 to take the oath at the White House rather than at the Fed’s headquarters. At the ceremony, Trump stated he hoped Waller would serve as a fully independent Fed Chair, acting without regard to his or anyone else’s preferences and simply doing what he believes is right. In his remarks, Waller clearly stated his intention to lead a reform-oriented Federal Reserve, moving away from rigid frameworks and models while upholding integrity and sound governance standards. Historical precedent shows that a Fed Chair’s policy choices result from the interplay of personal ideology, institutional constraints, and political pressure—from Burns yielding to political cycles and igniting the Great Inflation, to Volcker using monetary targets as a shield against politics to rebuild anti-inflation credibility, to the distinct independence strategies of Greenspan and Powell. Overall, Trump nominated Waller to push for rate cuts ahead of the midterm elections, but this goal clashes with both the reality of high inflation and Waller’s advocacy for balance sheet reduction. This contradiction suggests their 'honeymoon period' may be brief. Nevertheless, Waller is unlikely to engage in open confrontation; instead, he will seek a compromise that preserves Fed independence while accommodating political realities.

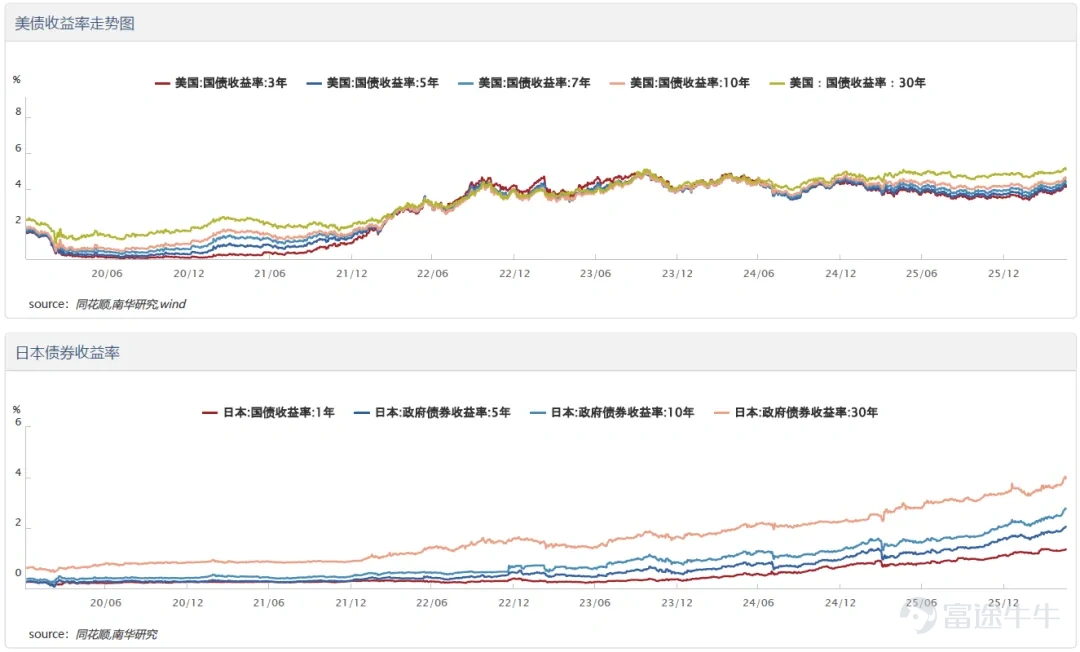

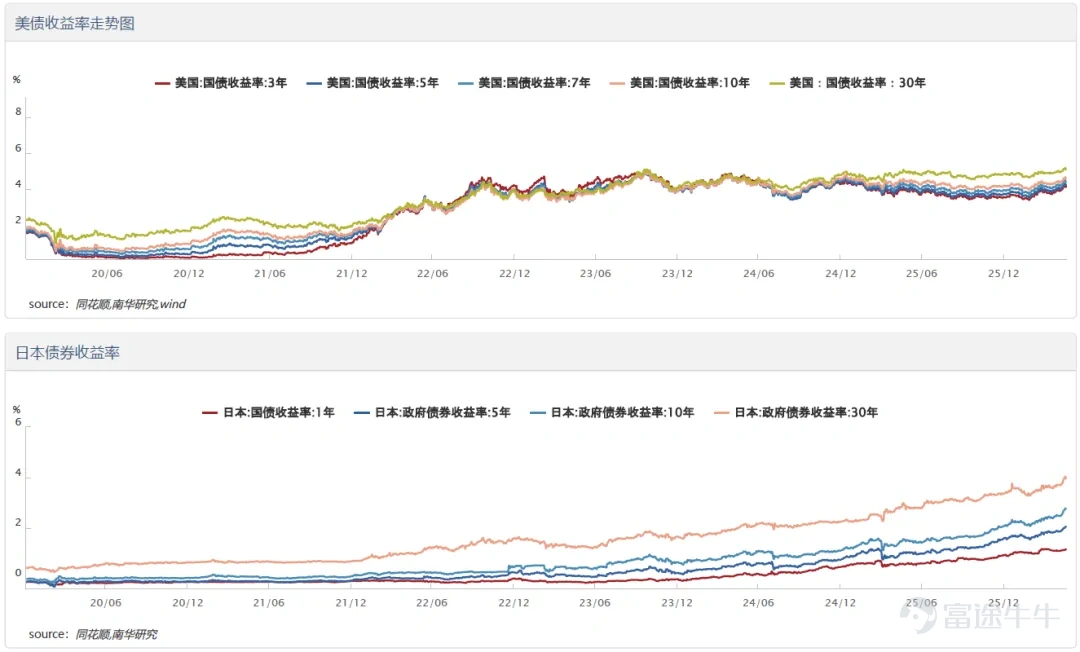

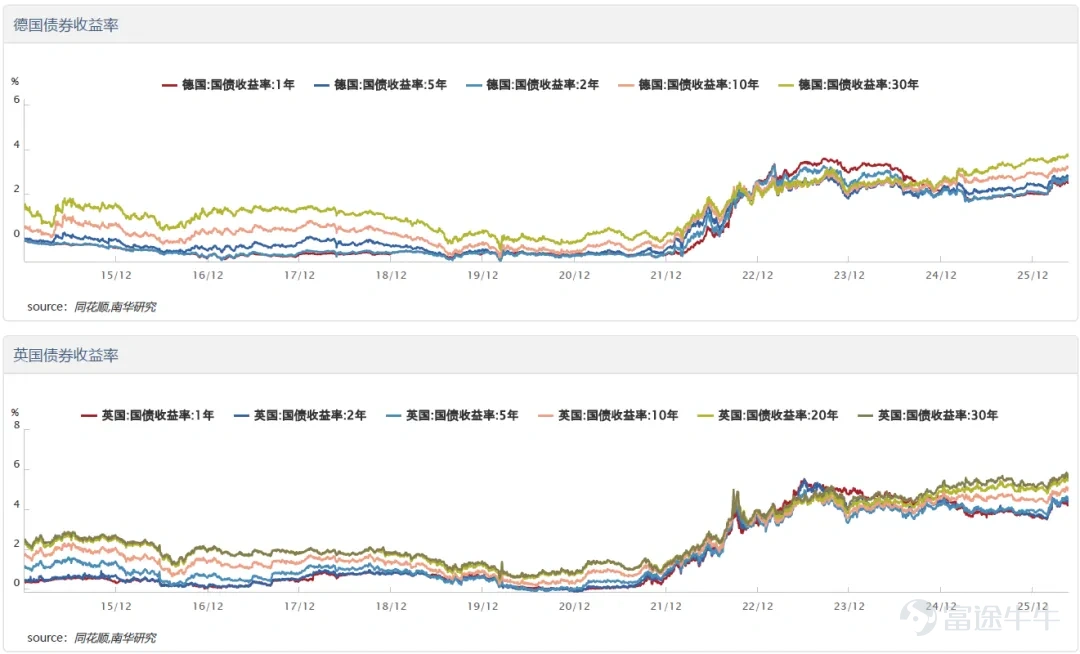

Meanwhile, the global bond market turmoil that began with the U.S.-Iran conflict in February is entering an even more dangerous new phase. As of the close on May 22, long-term sovereign bond yields across major economies have collectively surged to multi-year or even record highs. We believe the current global bond market is facing not only cyclical pressures but also a concentrated eruption of negative feedback loops driven by geopolitical conflicts—heightening inflation concerns and doubts over fiscal sustainability. Beyond these two core drivers, the long-standing structural supply-demand imbalances in global bond markets continue to deteriorate. On the supply side, fiscal expansion in advanced economies has become an irreversible norm: the U.S. will see approximately $10 trillion in Treasury securities mature or require refinancing this year; Europe is significantly increasing spending on defense, energy transition, and industrial policy; and Japan faces triple pressures from social security expenditures, interest payments, and energy subsidies. On the demand side, the traditional rationale for buying risk-free assets is fundamentally weakening. Post-pandemic inflation’s higher baseline, persistently widening fiscal deficits, and rising equity-bond correlation mean investors no longer automatically view long-dated U.S., European, or Japanese government bonds as natural portfolio hedges. Structurally, the share of non-price-sensitive buyers—such as central banks, insurance companies, pension funds, and foreign investors—has fallen markedly below pre-pandemic levels, while more trading-oriented, price- and volatility-sensitive capital now accounts for a significantly larger portion of demand. Although easing Supplementary Leverage Ratio (SLR) requirements may somewhat improve banks’ balance sheet capacity, their allocation preference leans toward short- and medium-term Treasuries, making it difficult to fundamentally address the chronic lack of demand for long-end duration instruments like 30-year bonds.

Going further, conventional wisdom holds that the federal funds rate is the key variable influencing the global economy and asset prices. However, Michael J. Howell, founder of CrossBorder Capital, offers a contrarian view: what truly drives the economy and equities is not the federal funds rate but the MOVE Index (a measure of U.S. Treasury market volatility). The core logic is that when the MOVE Index spikes sharply, it signals a significant increase in price uncertainty for Treasuries—the cornerstone collateral of the global financial system. A decline in collateral value directly impairs financial institutions’ ability to secure repo financing, triggering a contraction in the collateral multiplier and a broader global liquidity squeeze. During this bond market correction, we have indeed observed an anomalous surge in the MOVE Index, which contrasts with other liquidity indicators. This suggests that current liquidity stress is largely confined to the bond market itself and has not yet fully spilled over into the broader financial system. Nevertheless, this does not mean the risk can be ignored. Should the MOVE Index continue climbing into the high-volatility zone above 120, a sharp erosion in collateral value could easily spark a systemic liquidity crisis.

Geopolitical博弈: The TACO vs. NACHO Trade Standoff

Recent macro asset trends can be summarized by two popular market terms: the TACO trade bets that tensions will eventually ease, while the NACHO trade assumes the conflict will drag on longer. News of progress in U.S.-Iran negotiations released intensively between May 23 and 24 has given the short-term TACO trade the upper hand, though the NACHO trade thesis has not entirely disappeared.

On May 23, Trump stated via social media that a deal between the U.S. and Iran was essentially finalized and awaiting only final confirmation, explicitly adding that the Strait of Hormuz would be reopened as part of the agreement. On the same day, Iranian Foreign Ministry spokesperson Baghaei said that the positions of Iran and the U.S. are moving closer together and that both sides are currently in the final stages of drafting a memorandum of understanding.

According to Xinhua News Agency citing U.S. sources, the U.S. and Iran are close to reaching a temporary 60-day memorandum of understanding. Core provisions include extending the ceasefire, guaranteeing navigation through the Strait of Hormuz, partial U.S. lifting of sanctions on Iranian oil and ports, and Iran’s commitment not to pursue nuclear weapons and to engage in nuclear talks. It should be noted that Iranian officials have offered differing characterizations on certain clauses, such as the nuclear issue, and the agreement has not yet been finalized. Markets widely believe that even if a deal is reached, it would merely defer geopolitical risks by 60 days, leaving Middle East uncertainties intact.

Although a deal appears imminent, the specific terms of the memorandum simultaneously reveal two issues often overlooked by markets—indicating that geopolitical risks have only been postponed, not eliminated.

First, the U.S. has designed a phased verification mechanism tied to concrete actions in exchange for sanctions relief. The current draft memorandum already includes 14 articles, but the complexity of the bargaining goes far beyond the written text. Iran’s core demands—immediate unfreezing of seized assets and permanent sanctions removal—are explicitly included in the draft, yet the U.S. has only committed to temporary, 60-day relief subject to clear preconditions: Iran must first make substantive concessions, including clearing naval mines from the Strait of Hormuz, halting uranium enrichment activities, and transferring its stockpile of highly enriched uranium out of the country. This means the agreement is not a one-time settlement but a rolling verification process with 60-day cycles—any failure by either party to fulfill commitments could halt renewal. Notably, Iranian Parliament Speaker Qalibaf publicly criticized the U.S. as utterly untrustworthy during a meeting with Pakistani mediators and revealed that Iran’s armed forces had used the ceasefire period to complete reorganization and rearmament—a signal both as leverage against potential breakdown and as preparation for worst-case scenarios.

Second, Iran’s most critical demands remain unmet. Tehran has clearly stated through Foreign Ministry spokesperson Baghaei that the nuclear issue will not be included in the initial agreement and belongs to subsequent negotiation phases; key topics such as control over the Strait of Hormuz and permanent sanctions removal have likewise been deferred. On the issue of transit fees for the Strait of Hormuz, Trump explicitly opposes Iran imposing long-term tolls, with U.S. officials even stating such a move would render the deal unworkable—making this divergence a potential trigger for collapse. In essence, the two sides remain misaligned on the fundamental question of what should be negotiated now versus later. Adding external pressure, Israel strongly opposes the deal: Netanyahu has urgently convened his security cabinet, and the Israeli military has declared its highest alert status, further undermining an already fragile agreement.

Third, public statements from both sides not only differ in tone but also show directional divergence. Trump has claimed a deal will be announced soon and even issued an ultimatum—suggesting a 50-50 chance between securing a good agreement or resuming bombing—so much so that he canceled attending his eldest son’s wedding to remain at the White House handling the matter. Meanwhile, Iran has cautiously indicated it needs to wait and observe developments over the next three to four days, with its Foreign Ministry spokesperson having earlier emphasized that diplomacy is time-consuming and that it is premature to declare a deal near completion. U.S. officials have also candidly admitted that the draft is being revised daily with minimal progress, and several wording-level disagreements remain unresolved, with no final decision yet made. This dynamic—one side rushing to send signals and even threatening war as leverage, the other deliberately dampening expectations while using military reorganization as a fallback—reveals that the agreement remains in a precarious state, vulnerable to disruption by any unexpected variable.

In summary, based on the latest developments in U.S.-Iran negotiations, both sides have entered a high-pressure standoff phase within the current negotiation window. Although significant differences remain, both parties have a pragmatic need to avoid full-scale conflict. However, even if a ceasefire agreement is reached, oil prices are unlikely to quickly revert to pre-conflict levels, and inflationary pressures will persist for some time.

Outlook and Recommendations

Global markets currently rest on a fragile equilibrium driven by geopolitical expectations: near-term risk sentiment remains positive, supported by optimistic expectations of an imminent deal, yet concerns over elevated inflation, high interest rates, and fiscal sustainability have not abated. In the short term, market focus will center on three key areas: first, the final signing and implementation of the U.S.-Iran memorandum of understanding; second, how the Federal Reserve, under Kevin Warsh’s leadership, calibrates its policy stance between inflation pressures and growth risks; and third, whether heightened volatility in global bond markets could trigger a systemic liquidity crisis. From a trading perspective, it is advisable not to fixate on Monday’s opening price but instead observe true price discovery once liquidity returns during U.S. East Coast trading hours.

Author: Zhou Ji, Assistant Dean, Nanhua Research Institute (Registration No. Z0017101)

Important Disclaimer: The content and opinions in this article are for learning and reference purposes only and do not constitute any investment advice. The market carries risks, and investments should be made with caution.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment