SpaceX has perfectly achieved a flywheel closed loop integrating rockets, satellites, AI, and computing power. We are bullish on Musk's execution capability and vision.

SpaceX (Space Exploration Technologies Corp.) officially filed its S-1 registration statement with the U.S. Securities and Exchange Commission (SEC) on May 20, 2026, planning to list on Nasdaq on June 12, 2026 (ticker symbol: SPCX). This IPO aims to raise approximately USD 75–80 billion, targeting a valuation of USD 1.75–2 trillion, which is expected to become the largest IPO in human history.

The company had previously submitted its S-1 confidentially on April 1. The consolidation of xAI into SpaceX’s financials in early 2026 and its recent computing capacity contract with Anthropic can both be seen as strategic moves to maximize valuation ahead of the peak in AI-related capital expenditures.

Below is an in-depth analysis of SpaceX’s landmark S-1 filing:

1. Company Positioning and Industry Outlook

1.1 Company Overview and Market Positioning

SpaceX was founded by Elon Musk in 2002. SpaceX defines its ultimate mission as: 'To build the systems and technologies required to make life multiplanetary, understand the true nature of the universe, and extend the light of consciousness to the stars.'

Our mission is to build the systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars.

However, in commercial reality, the company’s positioning has leapfrogged from being a pure 'aerospace rocket manufacturer and launch provider' to becoming a 'global integrated space-ground satellite internet network operator + orbital AI computing and frontier technology giant.'

1.2 Industry Outlook

In its prospectus, SpaceX outlined to investors what it describes as the largest potential total addressable market (TAM) in human history—$28.5 trillion. The composition of this vast market is highly aggressive:

Traditional and next-generation commercial space launches and lunar/Mars economies: approximately $2 trillion.

Global satellite broadband connectivity: approximately $100–200 billion.

Orbital AI compute and artificial intelligence (Orbital AI Compute & AI): accounts for the overwhelming majority of TAM, amounting to $26.5 trillion. SpaceX firmly believes that future AI compute power will not be limited to Earth, and orbital data centers will become the ultimate infrastructure of the AI era.

1.3 Company's Industry Position and Competitive Landscape

Launch and satellite segment: SpaceX holds an absolute dominant position. It accounts for the vast majority of satellites launched and commercial payload launches globally. Traditional aerospace giants (such as Boeing, Lockheed Martin, and Northrop Grumman) have been left far behind due to high costs and lack of reusable technology.

AI segment: Following SpaceX’s full acquisition of Musk’s AI company xAI in February 2026 and its joint launch with Tesla of the 'Terafab' AI chip manufacturing project, SpaceX unusually named OpenAI and Anthropic in its prospectus as its direct core competitors in the AI field.

SpaceX’s Estimated TAM

Source: S-1

2. Core Competitiveness and Business Model

2.1 Technological Barriers

Advanced launch vehicle recovery technology: Commercially mature reuse of Falcon 9 and Falcon Heavy rockets, along with the intensively tested fully reusable Starship system.

Vertical integration capability: All core components—from Raptor engines and miniaturized phased-array satellite antennas to in-house AI chips—are independently developed and manufactured under a highly vertically integrated model, reducing supply chain costs to a fraction of industry averages.

Massive-scale satellite constellation deployment: Over 9,600 Starlink satellites are already in orbit, supported by highly sophisticated inter-satellite laser communication and networking technologies.

2.2 Business Model

SpaceX employs a unique business model that leverages cash-generative legacy operations to fund capital-intensive new ventures, primarily structured around three segments:

1. Space Launch (Space Segment): Providing high-frequency, low-cost launch services to government agencies (NASA, U.S. military) and commercial customers.

2. Satellite Connectivity (Connectivity Segment): The Starlink business, which charges subscription fees from global B2B (aviation, maritime, enterprise, government) and consumer users. This segment currently serves as the company's cash cow and profit engine.

3. Artificial Intelligence and Orbital Computing (AI Segment): Offers large model API services, enterprise-grade AI solutions, and orbital computing capacity leasing based on xAI (Grok models) and newly deployed orbital AI data centers.

2.3 Company's Core Advantages

Unmatched cost efficiency: Cost per kilogram of payload per launch is an order of magnitude lower than competitors.

Relentless execution capability: Silicon Valley-style rapid hardware-software iteration cycle (Build-Test-Fail-Fix), combined with Musk’s proven business execution prowess.

Extreme vertical integration: Fully in-house development and manufacturing across rockets, satellites, user terminals, AI clusters, and chips (Terafab).

Monopolistic ecosystem positioning: Owns its own 'vessel' (Starship), granting absolute priority and lowest internal pricing for transporting its own 'cargo' (Starlink satellites and orbital AI servers).

Deep alignment with Musk. The board approved the grant of 1 billion shares of Class B restricted common stock to Musk. The vesting of these restricted shares is contingent upon (i) achieving 15 milestone stages tied to a market capitalization of up to $7.5 trillion; and (ii) establishing a permanent human colony on Mars with at least 1 million inhabitants.

3. Research and Development and Innovation Capability

3.1 R&D Expenditure and Investment

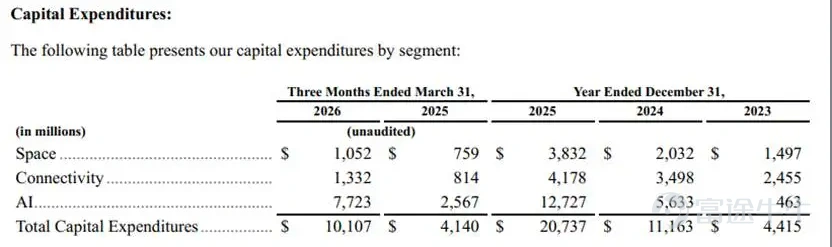

SpaceX is an extremely asset-intensive and technology-driven company. In 2025, the company’s capital expenditures (CapEx) will exceed $20 billion. Of this,

Starship development: Cumulative investment of USD 15 billion from 2020 to 2025.

AI infrastructure investment: The AI division’s capital expenditure reached USD 12.7 billion in 2025. Of the total USD 10 billion in capital expenditures in Q1 2026, USD 7.7 billion was allocated to AI (GPU clusters, infrastructure, and data center construction), while only USD 1 billion and USD 1.3 billion were dedicated to aerospace launches and Starlink, respectively.

AI strategy for space-based computing by 2028: Plans to deploy a constellation of orbital AI computing satellites by 2028, providing 100 GW of AI computing capacity annually to xAI, large models, autonomous driving, and scientific computing. Currently, SpaceX’s AI computing facilities COLOSSUS and COLOSSUS II together deliver 1.0 GW of computing power, already ranking among the largest AI training data center clusters on Earth.

Source: S-1

3.2 R&D Team Background

The team is a cross-disciplinary fusion of top-tier talent, comprising traditional aerospace engineers, cutting-edge semiconductor chip design experts, leading AI scientists (formerly core members of xAI), and seasoned software architects.

3.3 Talent Pipeline and Incentives

The company implements a highly competitive and flat management structure, with over 22,000 full-time employees. Its incentive mechanism relies heavily on a broad employee stock ownership plan (ESOP) to maintain strong alignment of interests across the entire workforce—this has been the key reason for exceptionally high employee loyalty despite the company remaining private for many years.

4. Product Portfolio, Growth Drivers, and Target Customers

The company’s strategy is to build a technological foundation through satellite launch services, generate consistent and stable cash flow via the Starlink network connectivity business, and then channel these resources into constructing AI computing infrastructure—thereby creating a closed-loop flywheel connecting rockets, satellites, AI, and space-based computing satellites.

Source: Author

5. Financial Analysis

5.1 Revenue and Growth

Total revenue in 2025: Reached USD 18.7 billion (up 30% year-over-year).

Q1 2026: Revenue reached USD 4.7 billion, up 15.4% year-over-year.

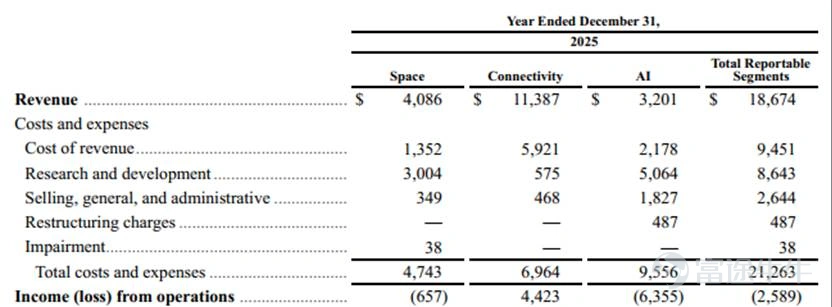

Starlink (Connectivity segment) has become the absolute pillar. Starlink generated USD 11.4 billion in revenue in 2025, accounting for nearly 60% of total revenue; in Q1 2026, it generated USD 3.3 billion (70% of quarterly revenue). From 2023 to 2025, EBITDA doubled annually.

The traditional aerospace launch segment (Space) reported USD 4.1 billion in revenue in 2025, benefiting from cost reductions due to Falcon 9 rocket reusability, yet still incurred a loss of RMB 6 billion.

AI is burning cash to sell computing power. In 2025, it generated USD 3.2 billion in revenue, with an operating loss of USD 6.3 billion and capital expenditures of USD 12.7 billion spent on chips from suppliers such as NVIDIA.

Source: S-1

5.2 Profitability and Cash Flow

Cash cow Starlink delivered strong performance: In 2025, Starlink generated $4.4 billion in operating profit, up 120% year-over-year, with adjusted EBITDA rising 86%. Subscribers grew from 2.3 million to 8.9 million last year, though ARPU declined from $99 to $66.

Overall net loss: Despite Starlink's profitability, SpaceX as a whole remains in the red due to massive spending on its AI business and Starship development. The company reported an operating net loss of $2.6 billion in 2025; driven by enormous AI-related capital expenditures in Q1, operating losses reached $1.9 billion in Q1 2026, resulting in a total net loss exceeding $4.2 billion.

Source: S-1

5.3 Costs and R&D

The AI segment is a major source of losses: In 2025, the AI segment generated $3.2 billion in revenue but incurred an operating loss of $6.35 billion. AI R&D expenses totaled $5 billion, primarily driven by the construction of computing clusters and development of the Grok large language model, with significant costs stemming from GPU hardware depreciation and AI data center construction.

In essence, SpaceX’s current financial profile features an extremely profitable Starlink satellite network that is fully funding and subsidizing the high-investment phases of xAI and Starship development.

5.4 Financial Position and Capital Structure

This IPO aims to raise approximately $75–80 billion, with proceeds primarily allocated to further expand AI computing infrastructure, accelerate mass production of Terafab chips, and achieve final commercialization of Starship.

Dual-class share structure: The prospectus discloses that Class A shares carry one vote per share and will be offered to the public, while Class B shares carry ten votes per share and will be held by insiders. Following the listing, Musk alone will control 85.1% of the voting power, granting him unassailable control over the company.

Musk may serve indefinitely as CEO, CTO, and Chairman of the Board.

6. Risk Factors

1. AI and massive capital expenditure monetization risk: The company has invested tens of billions of dollars in AI infrastructure (GPU data centers, computing power). Although it has locked in a portion of revenue through contracts with entities like Anthropic, if the AI industry experiences a broad bubble burst or if its orbital AI computing technology roadmap fails, these massive investments could face significant impairment.

2. Space safety and collision risk (space debris): With the total number of Starlink satellites approaching 10,000 and continuing to grow rapidly, the probability of collisions with space debris or other spacecraft has risen substantially, potentially triggering chain reactions or resulting in massive liability claims and regulatory penalties.

3. Key personnel and conflict of interest risk: The company is highly dependent on Elon Musk. However, Musk simultaneously leads multiple companies including Tesla, xAI (now merged), and X (formerly Twitter). Potential conflicts of interest may arise from Musk’s allocation of time, related-party transactions across companies, or the distribution of business opportunities.

7. Valuation and Key Highlights

7.1 Valuation Level

SpaceX’s target valuation is USD 1.75 trillion.

Compared to its projected 2026 revenue of USD 22–24 billion, this implies a price-to-sales (P/S) ratio of 72–80x.

This valuation far exceeds that of Tesla (approximately 8–12x P/S) and traditional tech giants such as Microsoft and Apple. Clearly, the market is not valuing it as a conventional aerospace or communications company, but rather as the 'ultimate monopolist of AI and infrastructure in the coming interstellar era,' with the premium reflecting substantial optionality value.

7.2 Key Highlights

A super high-conviction cash flow engine: Starlink has crossed the breakeven point, surpassed 10 million users, and now enjoys powerful network effects and pricing power.

A new space-based computing narrative for the AI era: By acquiring xAI and partnering with Anthropic, SpaceX has successfully positioned itself at the core of the AI race, with unique upside potential in space-based energy and orbital heat dissipation.

Once Starship succeeds, it will deliver a dimensionality-reducing competitive blow: Full-scale adoption of Starship will drive launch costs per ton to negligible levels, thereby fully unlocking the 'lunar economy' and the era of 'space manufacturing.'

8. Conclusion (Company Strengths and Weaknesses)

Strengths (Pros):

Unmatched, category-defining leadership in commercial aerospace and low-Earth-orbit satellite communications.

A perfectly vertically integrated supply chain, delivering exceptional cost control and high gross margins.

Starlink has already established a virtuous commercial loop with strong self-sustaining cash generation capabilities.

Weaknesses (Cons):

The company as a whole has yet to achieve net profitability, with AI and Starship acting like two massive 'cash-burning beasts.'

Valuation is extremely aggressive (70x+ P/S), pricing in high growth for many years ahead and leaving very little room for error.

Corporate governance risks are prominent, as the dual-class share structure grants Musk unilateral control.

9. Formulate six key questions for management

Based on information disclosed in the prospectus, we propose the following six core questions for SpaceX management during the roadshow:

I. Future Development Strategy and Concrete Implementation

1. [Implementation strategy for orbital AI computing] The prospectus states that $26.5 trillion of the company’s total addressable market (TAM) comes from AI, and it is actively developing 'orbital AI computing centers.' Please elaborate concretely on the technical implementation steps for deploying large-scale computing clusters in orbit—specifically regarding thermal management, radiation hardening, power supply, and data latency—compared to terrestrial data centers. When is the first batch of commercially operational orbital computing nodes expected to be fully deployed?

2. [Resource allocation for Starship commercialization] Starship has already consumed $15 billion between 2020 and 2025. Of the $75–80 billion raised in this IPO, what specific percentage will be directly allocated to Starship’s continued development and high-frequency launches? What are the critical policy, technological, or supply chain enablers required for Starship to achieve the 'daily launch cadence' envisioned in the prospectus?

II. Clarification of Core Competitive Advantages, Bottlenecks, and Mitigation Strategies

3. [AI competitive advantage and customer concentration] The company lists OpenAI and Anthropic as competitors, yet the prospectus reveals that its AI segment relies heavily on a $1.25 billion-per-month computing capacity lease agreement with Anthropic. Does this pose a significant customer concentration risk? Compared to purely ground-based AI giants like OpenAI, what exactly is the core strategic advantage of the combined SpaceX and xAI ecosystem?

4. [Physical bottlenecks of spectrum and orbital capacity] With over 9,600 Starlink satellites already in orbit and plans for further expansion, challenges are mounting—including congested frequency bands, tightening approvals from the International Telecommunication Union (ITU), and heightened risks of collisions with space debris. How does the company intend to address these physical and geopolitical constraints on growth? Are there specific insurance mechanisms or technical solutions—such as active collision avoidance or laser-based seamless inter-satellite links—to mitigate financial risks arising from satellite failures or destruction?

III. Clarification of Anomalous Data in the Prospectus

5. [Clarification on Massive AI Segment Losses and Unusual Margins] The prospectus shows that the AI segment generated $3.2 billion in revenue in 2025 but incurred an operating loss of as much as $6.35 billion, with AI accounting for nearly 80% of capital expenditures in Q1 alone. Please clarify: Of this massive AI segment loss, how much is attributable to depreciation and GPU hardware procurement? Given that the Grok large model has not yet achieved broad-scale monetization among enterprise (B2B) clients, for how many more quarters is such intense capital investment expected to continue? When overall can breakeven be achieved?

6. [Clarification on Related-Party Transactions and Financial Independence] The prospectus notes that SpaceX integrated Musk’s personal xAI entity in February this year and is jointly developing the 'Terafab' chip project with Tesla, while also highlighting the risk of 'conflicts of interest' involving Musk. Please provide detailed explanations regarding the pricing basis for R&D asset transfers, intellectual property ownership of chips, and allocation of personnel compensation among SpaceX, Tesla, and xAI. How will public shareholders be assured of the fairness of related-party transactions and the independence of fund usage?

10. Summary

SpaceX is a space infrastructure company leveraging Starship to deploy AI computing power into orbit. Its core business model exploits extreme engineering efficiency and vertical integration, breaking the boundaries between traditional aerospace and conventional internet industries. Starlink serves as its cash cow and money-printing engine; rocket launch services act as its moat; and AI computing power combined with Starship represents its grand vision—building a vertically integrated company spanning three layers of infrastructure: space, communications, and AI.

Investor Expectations for the Future:

In the near term, investors hope to see Starlink further monetize its user base among government, enterprise, and globally unconnected regions to stabilize its core fundamentals. In the medium term, they anticipate the full commercialization of Starship, driving per-launch costs down to the aggressively advertised low end. Over the long term, all capital is betting on one enormous possibility: whether Musk can successfully build the largest orbital AI distributed computing network in human history by leveraging his unique low-Earth-orbit satellite constellation and space-based energy resources. This century-defining IPO gamble is both a ticket to the future and the ultimate test of capital’s patience.

Risk Disclosure: The above content is for personal sharing purposes only and does not constitute any investment advice. Please assume all risks yourself.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comment (1)

to post a comment

8

1