Hong Kong Market Barometer: CPO, PCB, and memory stocks rally in rotation! Are you on the right trai

Market Weekly Report | May 11–17, 2026

Trump's visit to China sent positive signals, but stronger-than-expected US inflation pushed up Treasury yields and the dollar, leading global risk assets to fluctuate near highs, with Hong Kong and A-shares pulling back after an initial rally

The image was generated by AI.

1. Overview of the Global Macroeconomy

This week, global macro trading revolved around two main themes. First,US President Trump visited China from May 13 to 15, marking the first visit by a US president to China in nine years. Both sides established a new framework of 'constructive strategic stability' in US-China relations and reached multiple agreements on trade, technology, and people-to-people exchanges, significantly improving near-term expectations for bilateral ties.

Secondly,US April CPI rose more than expected, reaching a YoY increase of 3.8%, forthe highest level since June 2023, higher than the previous reading3.3%;Core CPI rose 2.8% year-over-year, higher than the previous reading2.6%, indicating that inflationary pressures are spreading from energy items to core components. Following the data release, market expectations for U.S. monetary policy turned hawkish again, with CME futures implyinga 39.1% probability of a rate hike by December 2026, and some sources indicate that the market is pricing in a greater than 50% chance of a rate hike before January next year. Against this backdrop,U.S. Treasury yields rose significantly and the dollar index strengthened, weighing on global equity valuations.

Domestically, fundamentals and the policy environment remain generally stable. China'sCPI rose 1.2% year-over-year in April、PPI rose 2.8% year-on-year, with the PPI increase widening compared to the previous readingby 2.3 percentage points; during the same period,M2 grew 8.6% year-on-year, slightly higher than the prior value.8.5%On May 15, the State Council’s executive meeting approved documents including the '15th Five-Year Plan for Urban Renewal,' reinforcing the signal of ongoing policy support. However, under the influence of rising external interest rates and declining risk appetite, both A-shares and Hong Kong stocks exhibited a pattern of rallying early in the week followed by a pullback mid-to-late week.

II. Performance of Global Asset Classes

Key theme this week: inflation reemerged as the dominant driver of global asset pricing, equities traded in a high-range consolidation, crude oil rebounded, bonds came under pressure, and the U.S. dollar strengthened.

On the equity side,, with major global equity indices showing divergent performance. U.S. stocks generally remained range-bound at elevated levels,with the S&P 500 index nearly flat for the week, closing at 7,408.49 points, down 0.06%, but during Thursday’s intraday and closing sessionsReached 7,501.25 points, marking the first time in history it closed above the 7,500-point level;The Nasdaq ended the week essentially flat at 26,225.1 points, down 0.19% for the week, hitting a record high of26,635.22 pointson Thursday;The Dow Jones Industrial Average historically breached the 50,000-point mark on Thursday, closing at 50,063.46 points. In Chinese markets,the Shanghai Composite Index fell 1.07% for the week to close at 4,135.39 points,the Shenzhen Component Index declined 0.02% for the week to 15,561.37 pointsbutwhile the ChiNext Price Index rose 3.50% for the week to 3,929.06 points, bucking the broader market trend,The STAR 50 Index rose by +3.40%, with growth-style stocks continuing to outperform. Hong Kong equities, however, faced broad pressure,as the Hang Seng Index declined by -1.63% for the week to 25,962.73 points,and the Hang Seng Tech Index dropped by -3.17% for the week to 4,941.14 points。

In commodities, while energy prices rebounded significantly.Brent crude rose from around USD 104.21 to USD 109.26, marking a weekly gain of approximately +4.8%, and WTI crude climbed from aboutUSD 99.75 to USD 105.42, posting a weekly increase of roughly +5.7%. During the week, Brent crude briefly surpassedUSD 107 per barrel, indicating that crude oil risk premium has risen again amid converging geopolitical tensions and supply-demand expectations.

In bonds, the U.S. Treasury market came under significant pressure.The yield on the 10-year U.S. Treasury note rose from 4.42% to 4.59%, climbing 17 basis points over the week.;The yield on the 20-year U.S. Treasury bond increased from 4.97% to 5.14%, also rising by 17 basis points.. In contrast, Chinese interest rate bonds remained stable,with the yield on China’s 10-year government bond easing slightly from 1.767% to around 1.766%, essentially flat., and the Sino-U.S. yield spread remains at a relatively low level.

In terms of exchange rates,, the U.S. dollar regained strength.The dollar index climbed from 97.92 to 99.27, posting a weekly gain of approximately 1.4%., reflecting renewed market pricing of higher real rates and stronger appeal of U.S. dollar-denominated assets following the upside surprise in U.S. inflation data.

III. Weekly Review of the Hong Kong Market

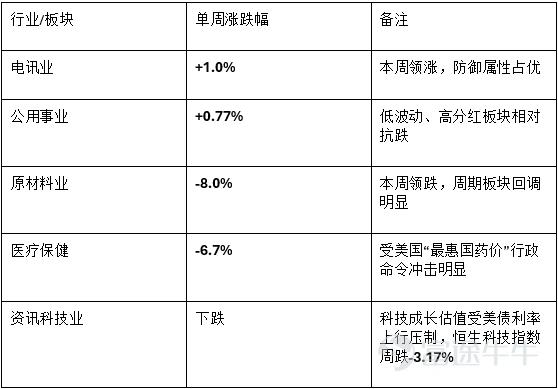

Hong Kong equities overall exhibiteda pattern of pullback from recent highs and heightened structural divergencethis week. On one hand, expectations of improved U.S.-China relations following Trump’s visit to China provided initial support to the market; on the other, stronger-than-expected U.S. April CPI data, a firmer dollar, and rising Treasury yields weighed on valuations in Hong Kong’s growth-oriented sectors. In terms of style performance, defensive high-dividend sectors held up relatively well, while technology, healthcare, and materials stocks experienced deeper corrections.

Index Performance

The Hang Seng Index fell 1.63% for the week, closing at 25,962.73 points;The Hang Seng Tech Index declined 3.17%, ending the week at 4,941.14 points;The Hang Seng China Enterprises Index dropped 2.23%. By sub-index,the Hang Seng Mainland Connect High Dividend Yield Index fell just 0.3%, marking the narrowest decline, andwhile the Hang Seng Composite SmallCap Index slumped 4.6%, the steepest loss, reflecting a defensive market bias this week and investor aversion toward highly volatile small-cap growth stocks.

In terms of valuation,The Hang Seng Index trades at approximately 11.83x P/E and 1.22x P/B, still generally near the lower end of its historical range; meanwhile,the Hang Seng AH Premium Index rose to 128.09, up 0.45% from last week, indicating that the relative valuation gap between A and H shares widened again during this week's Hong Kong market correction.

Industry sector gains and losses

On the liquidity front,southbound capital recorded a net inflow of approximately HK$9.3 billion for the week, continuing to provide marginal support amid the market pullback. In terms of timing, southbound flows were highly volatile during the week:net purchases amounted to about HK$800 million on Monday,net sales reached approximately HK$6.8 billion on Tuesday,combined net sales on Wednesday and Thursday totaled around HK$14.2 billionbutOn Friday, it significantly increased positions against the market trend by over HK$24.9 billion, marking a new two-month high for single-day net purchases.

Trading activity has picked up somewhat.The average daily turnover in the Hong Kong stock market was approximately HK$222.1 billion, up 19.20% week-over-week., indicating that despite index corrections, the intensity of capital positioning has not noticeably cooled. Structurally, in the past seven days, southbound funds have primarily added exposure tothree popular stocks within the information technology sector, totaling HK$4.925 billion;As of now,Southbound funds have recorded cumulative net inflows of approximately RMB 254.2 billion year-to-date, underscoring that mainland capital remains one of the most important sources of incremental funding for the Hong Kong market.

IV. Outlook for the future market

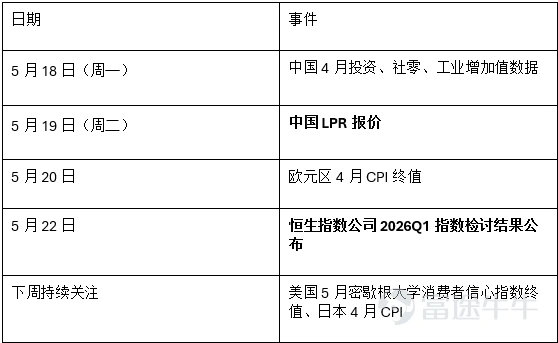

Next week, the market entersA critical window where macroeconomic data releases, policy repricing, and earnings verification converge.On one hand, China’s April economic data will be released on May 18, and the market will continue assessing the recovery in domestic demand and performance across the property chain; on the other hand,LPR quote on May 19、Announcement of Hang Seng Indexes Company’s Q1 2026 index review results on May 22will all influence Hong Kong equity market risk appetite and style dynamics.

Key calendar

Core Assessment

In the near term, the market will shift from 'event-driven' to 'data- and earnings-driven'. Expectations of improved U.S.-China relations following Trump's visit to China may help lower the geopolitical risk premium and potentially boost foreign investor sentiment toward Chinese assets, though this positive catalyst has already been partially priced in this week; relatively speaking,resurgent U.S. inflation, rising U.S. Treasury yields, and a stronger dollarremain more immediate constraints on global risk assets.

For Hong Kong equities, after the recent rebound, the index has entered a phase of consolidation, requiring fresh fundamental catalysts in the short term to offset overseas interest rate pressures. If the U.S. inflation trade continues to intensify, high-valuation growth sectors could remain under pressure.

Allocation strategy

1. Continue focusing on defensive and high-dividend themes. This weekThe Hang Seng China Connect High Dividend Yield Index declined by only -0.3%Telecommunications and utilities rose against the broader market trend, indicating that dividend-paying assets still offer allocation value during periods of rising interest rates and market volatility.

2. Growth-oriented tech stocks await a re-entry opportunity after earnings verification. The Hang Seng Tech Index underwent adjustments this week-3.17%, yet southbound capital continues to increase its allocationsThree popular stocks within the information technology sector, showing that capital has not systematically exited the tech sector. If earnings from leading companies like Tencent and Alibaba materialize as expected and marginal easing in U.S.-China tech tensions becomes reality, the tech sector could still emerge as a key driver of the next market rebound.

3. Within the A-share market, continue emphasizing the relative strength of growth-style stocks. This weekthe ChiNext Index gained +3.50%、SSE STAR Market 50 Index +3.40%It significantly outperformed the Shanghai Composite and CSI 300, indicating that high-growth sectors with strong fundamentals still offer relative return potential.

Risk Warning

⚠️ US inflation continued to exceed expectations, pushing Treasury yields higher. | Follow-up outcomes from China-US talks fell short of market expectations. | Earnings from leading companies such as Tencent and Alibaba missed expectations. | Weak domestic economic data for April dampened risk appetite.

Disclaimer: This report is for internal discussion purposes only and does not constitute investment advice.

Data sources: AlphaPai database and publicly available market information, as of May 19, 2026.

$CMS Hang Seng Tech Index ETF (03423.HK)$ $BABA-W (09988.HK)$ $TENCENT (00700.HK)$ $XIAOMI-W (01810.HK)$ $NTES-S (09999.HK)$ $MEITUAN-W (03690.HK)$ $KUAISHOU-W (01024.HK)$ $SMIC (00981.HK)$ $BYD COMPANY (01211.HK)$ $JD-SW (09618.HK)$ $LI AUTO-W (02015.HK)$ $TRIP.COM-S (09961.HK)$ $XPENG-W (09868.HK)$ $BIDU-SW (09888.HK)$ $LENOVO GROUP (00992.HK)$ $HAIER SMARTHOME (06690.HK)$ $JD HEALTH (06618.HK)$ $KINGDEE INT'L (00268.HK)$ $SUNNY OPTICAL (02382.HK)$ $BILIBILI-W (09626.HK)$ $MIDEA GROUP (00300.HK)$ $SENSETIME-W (00020.HK)$ $KINGSOFT (03888.HK)$ $ALI HEALTH (00241.HK)$ $HUA HONG GRACE (01347.HK)$ $TONGCHENGTRAVEL (00780.HK)$ $BYD ELECTRONIC (00285.HK)$ $ASMPT (00522.HK)$ $NIO-SW (09866.HK)$ $HORIZONROBOT-W (09660.HK)$ $TME-SW (01698.HK)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2