Market cap nears $3 trillion! Can SpaceX's listing rally continue?

SpaceX reveals a massive compute contract, Nebius announces GPU price hikes… Has the 'turning point' arrived for the US-listed compute leasing sector?

Today, SpaceX’s disclosed IPO prospectus has sent shockwaves through the AI and computing infrastructure market.

This document not only provides a comprehensive view of SpaceX’s ambitious roadmap across space exploration, satellite internet, and AI infrastructure, but also reveals a blockbuster over-$40 billion data center deal with AI unicorn Anthropic.

When viewed alongside SpaceX’s massive order, NEBIUS’s recent GPU price hike announcement, and Applied Digital’s signing of a large-scale AI factory leasing agreement, a clear industry trend appears to be emerging:Contrary to some pessimistic expectations of oversupply, the global computing power leasing market is instead undergoing a complete repricing and rapidly accelerating toward a new wave of infrastructure investment centered on 'power availability' and 'massive-scale clusters.'

This article will provide fellow investors with an in-depth analysis:What are the latest developments in the computing power leasing sector? Which companies in the U.S. stock market stand to benefit the most?

What are the latest developments in the computing power leasing sector?

I. Record-Breaking Long-Term Contracts Set a New Benchmark—Computing Power Pricing Enters a 'Revaluation Moment'

The deal details between SpaceX and Anthropic have directly shattered the market's prior assumptions about the ceiling price for compute capacity leasing.

According to the prospectus, Anthropic signed a three-year long-term compute leasing agreement (from May 2026 to May 2029), under which it will pay SpaceX up to $1.25 billion per month, amounting to a total contract value of approximately $45 billion. This indicates that leading AI companies are willing to pay a significant premium to secure long-term compute capacity and ensure future compute availability.

– Disruptive doubling of per-GPU revenue: According to TF International Securities' overseas research estimates, the implied per-GPU lease rate under this contract reaches$7.8 per GPU-hour, significantly higher than current spot market prices (approximately $3 for H100, and around $6–$7 for H200/B200).

– Reshaping Neocloud’s revenue model: This premium will fundamentally reshape valuation models for compute infrastructure. Under the previously common market assumption of $3.5 per GPU-hour, annual revenue per 10,000 GPUs would be approximately $307 million; with the new benchmark pricing of $7.8, per-GPU revenue intensity jumps directly to2.2 timesthe original expectation. This will substantially expand profit margins for compute leasing providers, potentially driving incremental gross margins to remarkable levels.

2. Persistent supply-demand tightness creates 'resonance' between spot price increases and long-term contract lock-ins

SpaceX's long-term contracts are not an isolated case; the entire compute capacity market is experiencing an upward shift in pricing.

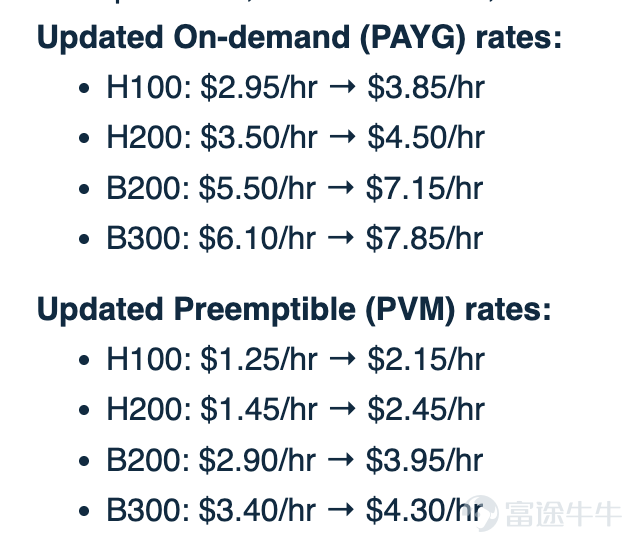

Recently, Cloud service providers $NEBIUS (NBIS.US)$have officially issued GPU price increase notifications.This move strongly resonates with Anthropic’s high-premium long-term contracts, sending a clear signal that the supply-demand imbalance for high-end compute capacity remains acute.

Amid exponentially growing model training scales, AI companies are no longer grappling with 'how expensive compute capacity is,' but rather with the existential anxiety of 'whether they can secure enough compute capacity.' Rising spot market prices and high-premium lock-ins in the forward market (long-term contracts) jointly confirm that the compute leasing sector remains a strong seller’s market, granting service providers significant pricing power.

3. Underlying infrastructure anxiety: Those who secure 'power' and 'scale' will dominate

Competition in compute leasing has long evolved beyond merely 'racing to buy GPUs' to 'competing for foundational infrastructure,' with the core issue being—Electric power。

Two recent mega-deals perfectly illustrate this point:

$Applied Digital (APLD.US)$ has recently signed an agreement with a U.S.-based, high-investment-grade hyperscaler to provide its fourth AI factory campus, Polaris Forge 3, located in a northern state. The campus is designed to deliver 300 MW of critical IT load, supported by approximately 430 MW of grid-connected utility power.

$NEBIUS (NBIS.US)$The subsidiary signed a master fuel cell capacity agreement and related system orders with Bloom Energy on May 14.During the term of the agreement, NEBIUS will pay monthly service fees totaling up to $2.6 billion for the capacity and power from the power supply systems. The provided power capacity is expected to come online in three phases, with a guaranteed capacity of approximately 250 MW and a total installed system capacity of approximately 328 MW. Bloom Energy will be responsible for installing, operating, and maintaining the power supply systems.

These two deals—each involving hundreds of megawatts and costing billions of dollars—fully reveal the core logic driving the next phase of AI infrastructure development:

1. 'Power' has become the absolute bottleneck for scaling compute capacity: AI training is no longer about individual GPUs but involves massive clusters of hundreds of thousands of GPUs working in tandem. Power demands routinely reaching hundreds of megawatts have made data centers with stable, large-scale power supply an extremely scarce strategic resource. Without power, even the most advanced GPUs cannot operate.

2. Diversification of energy sources and the trend toward 'off-grid' power generation: NEBIUS’s $2.6 billion commitment to Bloom Energy illustrates how, against the backdrop of slow grid approval processes and constrained grid capacity, major compute players are turning to off-grid independent power solutions—such as nuclear energy and natural gas fuel cells—to break through the physical limits on expansion.

3. Forward-looking land-grabbing by industry giants: Whether hyperscalers directly securing AI facilities with 400 MW of capacity or new AI powerhouses locking in the entire output of power plants, top players are bypassing traditional hardware procurement and moving straight to the foundational layer of 'power + real estate' to secure the physical foundation of their AI empires.

Which companies will emerge as the biggest beneficiaries?

Amid the current 'computing power revaluation frenzy' triggered by SpaceX's sky-high contracts and power supply anxieties, and aligned with the two core industry dynamics—'revaluation of computing power pricing' and 'those who secure power and scale will dominate'—the following three segments stand to benefit most from this AI infrastructure boom:

1. New Cloud Service Providers: The 'Pure Water Sellers' of the AI Era

These companies are a new breed born alongside the demand for large model training, focusing exclusively on offering high-end GPU computing power leasing services. They are typically deeply integrated with hardware giants like NVIDIA.

$CoreWeave (CRWV.US)$:Currently, the purest and most aggressively expanding AI-dedicated cloud service provider in the market—and NVIDIA’s 'favorite child,' having received direct investment and priority hardware allocation from NVIDIA. Thanks to extremely high GPU density and network architectures optimized specifically for AI workloads, it delivers more efficient and cost-effective per-unit computing power than traditional cloud providers. The market is closely watching its capacity expansion pace and NVIDIA’s future stakeholding moves.

$NEBIUS (NBIS.US)$:A rising computing power player with European technical roots, which has also recently secured investment from NVIDIA. It has drawn significant attention for announcing GPU price hikes and making massive investments to lock in Bloom Energy fuel cells—in other words, it was the first to break through the 'power shortage' bottleneck by building its own independent power generation network to secure computing capacity. Such Neoclouds with forward-looking energy strategies hold the strongest pricing power in this seller’s market marked by supply-demand imbalances.

$IREN Ltd (IREN.US)$: Successfully transitioned from Bitcoin mining to a 100% renewable-energy-powered AI computing center.Its advantage lies in readily available green power reserves and existing data center infrastructure, enabling it to rapidly deploy NVIDIA’s latest architectures.

$WhiteFiber (WYFI.US)$:An emerging infrastructure provider specializing in high-bandwidth fiber networks and interconnectivity between computing nodes. In hyperscale clusters (on the order of 100,000 GPUs), data transmission latency directly impacts computing efficiency. These companies solve critical pain points in intra- and inter-data-center connectivity.

2. High-Performance Computing (HPC): The 'Energy Landlords' Controlling the Foundational Lifelines

This segment includes numerous former cryptocurrency miners. In today’s AI computing crunch, their 'compliant grid capacity' and 'cooling infrastructure' have become invaluable assets coveted by tech giants.

$Applied Digital (APLD.US)$:is a next-generation data center developer specifically designed for high-performance computing (HPC). It has just signed a massive-scale AI factory lease agreement, upgrading its business model from 'buying GPUs and renting them out' to 'directly collecting super rents from tech giants.' Its core moat lies in its ability to secure land and power supply, as well as its engineering and delivery capabilities for building liquid-cooled data centers.

$TeraWulf (WULF.US)$& $Core Scientific (CORZ.US)$ :are HPC transformation pioneers with substantial power reserves. WULF focuses on zero-carbon/nuclear-powered electricity, while CORZ leverages its extensive infrastructure footprint to frequently secure long-term AI hosting contracts. Specifically, hyperscalers are rushing to purchase power allocations—often at a premium—from these HPC companies that offer clean energy and ready-to-use facilities, reflecting a pure 'monetizing power' logic.

$MARA Holdings (MARA.US)$, $Riot Platforms (RIOT.US)$, $CleanSpark (CLSK.US)$, $Hut 8 (HUT.US)$Wait for:is among North America’s leading cryptocurrency mining giants, gradually diversifying part of its high-energy-consuming assets into AI-focused high-performance computing (HPC) businesses. As traditional 'energy arbitrageurs,' the market is now revaluing the real option value embedded in their hundreds of megawatts of available power capacity.

III. Hyperscalers: The 'Top-Tier Harvesters' of the AI Ecosystem

They initiated this compute arms race and represent the group with the largest capital expenditures (CapEx).

$Microsoft (MSFT.US)$、 $Alphabet-A (GOOGL.US)$ 、 $Amazon (AMZN.US)$、 $Meta Platforms (META.US)$:These companies are not only NVIDIA GPU’s biggest buyers but also the primary funders of Neocloud and HPC infrastructure. Their core objective is to integrate AI capabilities into their own SaaS, search, or advertising businesses through massive, cost-insensitive infrastructure investments, thereby monopolizing both enterprise and consumer end markets.

$Oracle (ORCL.US)$ : A fast-rising challenger with extremely rapid cloud market share growth. With its highly flexible OCI (Oracle Cloud Infrastructure) architecture and aggressive small modular reactor (SMR)-powered data center plans, it is capturing significant AI training workloads from the three legacy cloud giants.

$Alibaba (BABA.US)$ : Facing a unique hardware supply chain environment, Alibaba Cloud has developed a strong moat in 'heterogeneous compute orchestration and optimization.' Its core strategy is to convert front-end AI traffic into long-term, inelastic consumption of underlying compute leasing and cloud storage services.

Summary

In summary, the decisive factor in AI infrastructure has fully evolved from the first half’s 'GPU rush' to the second half’s 'power showdown.' Amid this wave of compute pricing repricing—sparked by SpaceX’s record-breaking long-term contracts—the winners will be: 'new cloud providers' with the highest near-term profit elasticity; 'energy landlords' who collect super rents thanks to compliant power access in the medium term; and 'top-tier giants' who build unassailable ecosystem moats through capital strength and heterogeneous compute orchestration over the long run—all harvesting the inelastic红利 driven by power and hyperscale clusters.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (11)

to post a comment

178

717