The Big Four's performance diverges after results! Who is the real winner in AI?

AI Capex enters the cash flow test phase

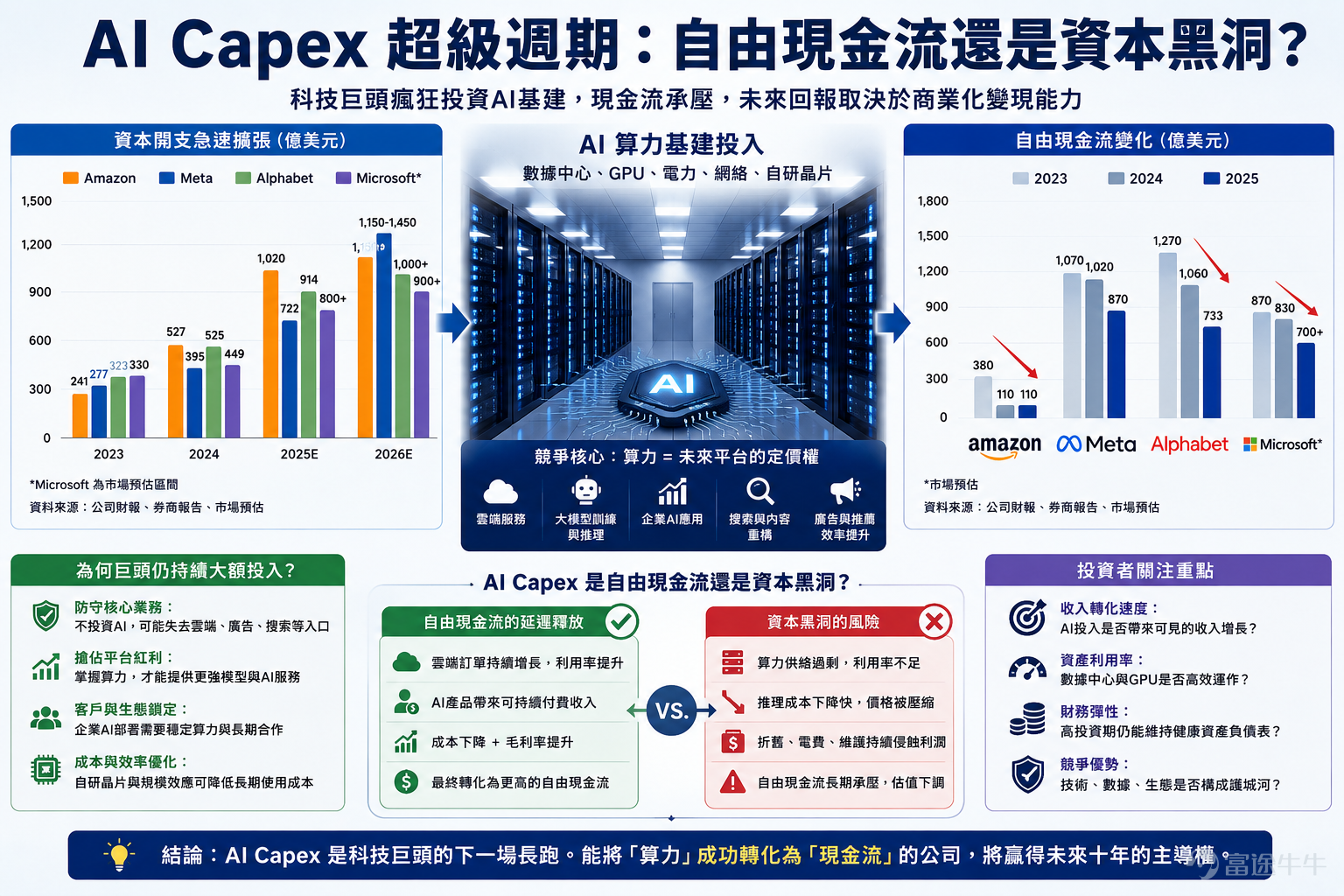

![Artificial intelligence is no longer just a growth story for tech companies—it has become a supercycle of capital expenditure. In the past, investors evaluated large-cap tech stocks primarily by revenue growth, gross margins, cloud market share, and free cash flow. However, in the generative AI era, a sharper question has emerged: Are mega-cap companies investing hundreds of billions—even over a trillion—dollars annually into data centers, GPUs, custom AI chips, and power infrastructure to secure early advantages in the next-generation platform, or are they dragging what was once stable free cash flow into a capital expenditure black hole? The scale of this race is extraordinary. Amazon disclosed in its 2025 annual report that free cash flow dropped from $38 billion to $11 billion, primarily due to a $50.7 billion increase in property and equipment purchases. The company explicitly stated that this shift in free cash flow largely reflects AI-related capital expenditures. Meta has also significantly ramped up AI infrastructure investments, with 2025 capital expenditures already exceeding $70 billion. Market reports indicate its 2026 capex guidance has been further raised to as high as approximately $145 billion, reflecting management’s willingness to trade short-term cash flow for dominance in AI computing power.([Share Link: Fortune]) Alphabet is expanding rapidly as well; analysts estimate its capital expenditures rose from $32.3 billion in 2023 to $91.4 billion in 2025—nearly tripling in two years. Supporters argue this isn’t wasteful spending but rather a ticket to the new platform. AI model training, inference services, enterprise Copilots, search engine re-architecting, ad recommendations...](https://nnqimage.futunn.com/sns_client_feed/40001501/20260520/web-1779271618749-NFYN0J08Jc.png/big?area=1&is_public=true&imageMogr2/ignore-error/1/format/webp)

Artificial intelligence is no longer just a growth story for tech companies—it has become a supercycle of capital expenditure. In the past, investors evaluated large-cap tech stocks primarily by revenue growth, gross margins, cloud market share, and free cash flow. However, in the generative AI era, a sharper question has emerged: Are mega-cap companies investing hundreds of billions—even over a trillion—dollars annually into data centers, GPUs, custom AI chips, and power infrastructure to secure early advantages in the next-generation platform, or are they dragging what was once stable free cash flow into a capital expenditure black hole?

The scale of this race is extraordinary. Amazon disclosed in its 2025 annual report that free cash flow dropped from $38 billion to $11 billion, primarily due to a $50.7 billion increase in property and equipment purchases. The company explicitly stated that this shift in free cash flow largely reflects AI-related capital expenditures. Meta has also significantly ramped up AI infrastructure investments, with 2025 capital expenditures already exceeding $70 billion. Market reports indicate its 2026 capex guidance has been further raised to as high as approximately $145 billion, reflecting management’s willingness to trade short-term cash flow for dominance in AI computing power.(Fortune) Alphabet is expanding rapidly as well; analysts estimate its capital expenditures rose from $32.3 billion in 2023 to $91.4 billion in 2025—nearly tripling in two years.

Supporters argue this isn’t wasteful spending but rather a ticket to the new platform. AI model training, inference services, enterprise Copilots, search re-architecting, ad recommendations, and cloud compute leasing all require massive hardware infrastructure. Whoever secures sufficient computing power, electricity, and data center capacity first will gain pricing power in enterprise AI deployment. For Microsoft, Amazon, Alphabet, and Meta, AI capex is not merely a cost item—it’s insurance for defending their core businesses. Cloud providers without enough GPUs cannot meet demand from AI startups and enterprise clients; ad platforms lacking proprietary models may fall behind in recommendation efficiency and content generation; and search engines that fail to rebuild their user experience around AI answers risk losing their position as primary traffic gateways.

However, what capital markets truly worry about is the timing mismatch. Capex occurs today, but revenue may not materialize tomorrow. Once data centers are completed, depreciation, electricity costs, maintenance, and chip refresh cycles will continuously weigh on the income statement. If AI products fail to generate sufficient willingness to pay, or if enterprise clients are merely in trial phases, these massive investments will first erode free cash flow and subsequently drag down valuation multiples. Recent reports have also indicated that large tech firms are increasingly turning to overseas bond markets to finance AI infrastructure—partly because the scale of AI spending is putting significant pressure on free cash flow. As a business model once characterized by 'light assets and high cash flow' in software and internet services gradually shifts toward a 'capital-intensive, high-depreciation' structure, investors naturally reassess the valuation premium.

Therefore, whether AI capex acts as a source of free cash flow or becomes a capital black hole hinges not on the size of expenditures, but on return on invested capital. If spending drives growth in cloud orders, AI subscription revenue, higher ad conversion rates, or expansion of developer ecosystems, today’s decline in free cash flow is merely deferred realization. Conversely, if companies simply race to expand capacity out of fear of falling behind, leading eventually to oversupply of compute power, falling prices, and underutilization, this arms race will become a classic case of capital misallocation.

More subtly, the market does not view all AI capex equally. If Amazon’s AI spending directly translates into AWS demand, investors may see it as capacity expansion with high revenue visibility. If Alphabet uses its in-house TPUs to lower costs, it could improve long-term inference economics. Meta, meanwhile, must demonstrate that its AI infrastructure can consistently enhance ad efficiency and user engagement—or else its massive outlays risk being labeled as 'faith-based investing.' In other words, while everyone may be spending on GPUs, some are building toll roads, while others might just be stockpiling expensive hardware.

At its core, this AI capex supercycle reflects how tech giants are front-loading their competitive bets for the next decade onto their capital expenditure statements. It could either usher in the next peak of free cash flow—or expose cracks in the pace of AI commercialization. For investors, the key question is no longer who spends the most, but who can convert compute power into revenue fastest, turn revenue into profit, and ultimately transform profit back into free cash flow. Only by closing this loop does AI capex become a moat; otherwise, it will inevitably become a black hole that devours valuation.

(Chips and Compute Power Series #59)

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3