In-Depth Research: China Dividend ETFs — How Much Do You Know?

The dividend strategy has long been one of the most favored factor allocations in China's equity ETF market. Between 2024 and 2025, this segment continued to expand, with incremental capital increasingly flowing into onshore dividend ETFs tracking H-shares. A deeper analysis reveals that A-share and H-share dividend ETFs are beginning to diverge in terms of performance and fund flows.

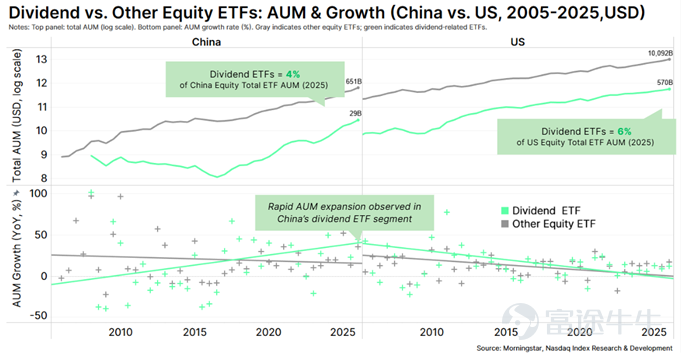

Market Landscape and Scale Evolution

01

As of the end of 2025, Chinese dividend ETFs accounted for approximately the following share of total equity ETF AUM:

A. 1%

B. 4%

C. 6%

D. 10%

(Answer: B)

China's dividend ETFs continue to accelerate in growthMeasured by assets under management (AUM), dividend ETFs have consistently represented the largest factor-based strategy segment within China's equity ETF market. As of the end of 2025, China’s dividend ETFs had approximately USD 29 billion in AUM, accounting for about4%(Figure 1)。

In comparison, U.S. dividend ETFs accounted for a slightly higher share of6%, representing roughly USD 570 billion of the over USD 10 trillion equity ETF market. Although the growth rate of U.S. dividend ETFs has largely kept pace with the overall equity ETF market, China’s dividend ETFs have exhibited a notably more pronounced acceleration in both scale expansion and growth rate since 2015(Figure 1)。

Chart 1: Comparison of AUM Growth Trends Between Dividend ETFs and Other Equity ETFs in China and the U.S.

From A-shares to Hong Kong stocks: China's dividend ETFs achieve a significant leap in scale

Chart 2 further breaks down the AUM composition of China’s dividend ETFs by underlying assets.

2006-2017

In the decade following the launch of the first dividend ETF in 2006, its assets under management remained negligible for over ten years.

2018-2022

However, after 2018, assets began to accumulate steadily, driven by A-share dividend ETFs, reaching approximately USD 4 billion by early 2022.

2023-2025

Starting in 2023, assets under management expanded significantly. Although A-share products still constitute the majority of existing assets, Hong Kong Stock Connect dividend ETFs have become a major source of incremental capital, particularly evident since 2024. As of December 31, 2025, total assets under management of China dividend ETFs exceeded USD 29 billion, with exposure to Hong Kong equities amounting to roughly USD 12 billion, representing over 40% of the total.

Chart 2: Breakdown of AUM between A-Share and Hong Kong-Listed China Dividend ETFs

Performance Divergence and Factor Attribution

02

Compared to A-share dividend ETFs, what is a more pronounced characteristic of Hong Kong-listed dividend ETFs?

A. Higher market risk exposure (Beta)

B. Greater sensitivity to the value factor

C. More pronounced positive exposure to the quality factor

D. More concentrated sector allocation

(Answer: C)

Hong Kong-listed dividend ETFs have delivered leading performance

This expansion in allocation scale has coincided with a significant divergence in performance between Hong Kong and A-share dividend ETFs over the past year. As of December 31, 2025, the median one-year total return for Hong Kong dividend ETFs stood at 20%, compared to just 3% for their A-share counterparts.

Among leading products, the two largest Hong Kong dividend ETFs—513630.SH (+26%) and 159691.SZ (+18%)—posted strong returns. In contrast, the largest A-share dividend ETF, 512890.SH, rose only 5%, while the second-largest, 510880.SH, was essentially flat.(Figure 3)During the same period, capital continued flowing into Hong Kong dividend ETFs, while demand for A-share dividend strategies became more cautious.

Exhibit 3: One-Year Performance and Fund Flows of Dividend ETFs

Quality and Value Factors: Core Differences Across Dividend ETFs with Varying Factor Exposures

To explain the performance gap between A-share and Hong Kong dividend ETFs, we applied the widely used Fama-French factor model framework, which helps decompose returns into several common investment dimensions, including:Market risk exposure (Beta)、Size factor、Value versus growth orientation factorandQuality factorand others.

Empirical analysis based on this methodology shows thatHang Seng Dividend ETFit exhibits relatively low market risk exposure overall, and the regression coefficient for the quality factor is significantly positive, thereby demonstrating stronger defensive characteristics(see Figure 4)。

Figure 4: Hang Seng Dividend ETF – Low Beta and Quality Tilt

In contrast,A-share Dividend ETFalso shows relatively low market risk exposure and a significantly positive quality factor coefficient, while its value factor regression coefficient is also statistically significantly positive(see Figure 5)。

Chart 5: A-share Dividend ETFs Exhibit Higher Sensitivity to the Value Factor

Fund Flows and Investor Composition

03

Between 2024 and 2025, which type of investor showed a more pronounced preference for allocating to Hong Kong dividend ETFs?

A. Mutual Funds

B. Private Equity Funds

C. Pension and Insurance Funds

D. Foreign Hedge Funds

(Answer: C)

Insurance demand is supporting fund inflows into Hong Kong dividend ETFs

Fund flow and position data clearly confirm that the sources of incremental capital for A-share and Hong Kong dividend ETFs are diverging(Exhibit 6)As of the end of December 2025, dividend ETFs tracking A-share stocks still held a dominant position in terms of total assets under management (AUM), amounting to approximately USD 17 billion, followed closely by Hong Kong-listed dividend ETFs with around USD 12 billion.

Notably, despite the gap in overall scale, net inflows into both categories were very close during the same period: A-share dividend ETFs recorded net inflows of about USD 4 billion, while their Hong Kong counterparts attracted USD 5 billion. Given their smaller initial base, Hong Kong dividend ETFs have significantly outpaced A-share peers in terms of growth rate.

Exhibit 6: AUM and One-Year Fund Flows of Dividend ETFs by Underlying Asset Class

Exhibit 7Combining AUM and holdings data, this exhibit illustrates how the expansion of dividend ETFs between 2024 and 2025 maps specifically at the product level. Apart from 510880.SH showing notable divergence, most ETFs experienced significant AUM growth, visually represented by the widening of the bars.

At the same time inIn terms of portfolio composition, concentration has shown a gradual declining trend.The combined weight of the top ten holdings in most dividend ETFs has generally decreased, confirming that as AUM expands, these funds are increasingly adopting more diversified investment strategies. Furthermore, portfolio composition varies by investor type: pension and insurance investors (indicated in blue) show a clear preference for Hong Kong dividend ETFs, whereas mutual funds (orangeare predominantly positioned in A-share dividend ETFs.

Exhibit 7: Portfolio Allocation by Investment Characteristics (%)

The rapid rise of China dividend ETFs has been accompanied by notable differences across multiple dimensions between products linked to A-shares and those linked to Hong Kong stocks. Recent data shows distinctions in assets under management growth trajectories, performance, factor exposure characteristics, and investor composition. These differences reflect current market observations, and continuous monitoring is essential to assess how the features of dividend ETFs and investor behavior evolve as markets develop further.

The information contained in this communication document includes forward-looking statements involving various risks and uncertainties. Nasdaq hereby advises readers that any forward-looking information does not constitute a guarantee of future performance, and actual results may differ materially from the contents of the forward-looking information. Forward-looking statements can be identified by terms such as "will" and "believe," along with similar expressions. Such statements involve numerous risks, uncertainties, or other factors beyond Nasdaq's control. These risks and uncertainties are detailed in Nasdaq's filings with the U.S. Securities and Exchange Commission (SEC), including its annual reports on Form 10-K and quarterly reports on Form 10-Q, published on Nasdaq's investor relations website (http://ir.nasdaq.com) and the SEC's official website (www.sec.gov). Nasdaq has no obligation to publicly update any forward-looking statements, whether due to new information, future events, or otherwise.

Nasdaq® is a registered trademark of Nasdaq, Inc. The information provided above is for reference and educational purposes only, and none of the content in this article should be considered as investment advice representing a specific security or overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates provides recommendations on buying or selling any securities, nor do they make any statements regarding the financial condition of any company. Statements about Nasdaq-listed companies or Nasdaq proprietary indices are not guarantees of future performance. Actual results may differ significantly from those expressed or implied. Past performance is not indicative of future results. Investors should conduct their own due diligence and carefully evaluate companies before investing. It is strongly recommended to seek advice from securities professionals. Any discrepancies or divergences caused by translation are non-binding and have no legal effect on compliance or enforcement. If there are any questions about the information provided in this translation, please refer to the English version.

Yinan Xiao

CFA

Nasdaq Index Research and Development Department

Senior Analyst

Phoebe Wang

CFA

Nasdaq Index Research and Development Department

Senior Director

Click to view related articles

Click "Read More" below to view the full analysis report

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment