ASCO 2026 Academic Conference Data Disclosure: Chinese Biopharma Assets Recently Attract Market Attention

Summary of Key Insights

With the Q1 earnings season now concluded, market focus is swiftly shifting toward clinical data and individual stock fundamentals. The 2026 American Society of Clinical Oncology (ASCO) Annual Meeting (May 29–June 2) will be held in Chicago and stands as one of the key catalysts for the biopharma sector this year. Notably, Chinese assets feature prominently in several pivotal Phase III datasets—particularly in first-line treatment for non-small cell lung cancer (NSCLC)—including Innovent Bio, Kelun-Biotech, and Akeso.Against a backdrop of mild macroeconomic volatility triggering sector-wide adjustments, we believe Hong Kong-listed biopharma assets supported by solid fundamentals deserve attention.

I. Market Context: Post-Earnings Focus Shifts to Fundamentals-Driven Catalysts

Following the conclusion of the Q1 earnings season across Mainland China, the U.S., and Hong Kong, investor attention is shifting from financial results to academic conference data disclosures and company-specific business progress. In the current macro environment, long-end rates in the U.S., Japan, and the U.K. have all risen, compounded by heightened global macroeconomic uncertainty, creating valuation pressure on certain unprofitable biotech firms. The Hong Kong biopharma sector has underperformed the broader market for two consecutive weeks, partially reflecting these macro headwinds.

However, our ongoing observations indicate that the fundamentals of China’s biopharmaceutical and innovative drug sector are on a positive upward trajectory. Recent industry developments have been largely favorable: BeiGene’s Beozyta® (sotorasib, BEQALZI™️) received accelerated approval from the U.S. Food and Drug Administration (FDA); Hengrui Pharma announced a significant licensing agreement with a multinational pharmaceutical company; and Hutchmed raised its U.S. sales guidance for one of its drugs. These events collectively underscore tangible progress made by Chinese pharmaceutical companies in global expansion and commercialization.

Against this backdrop, if macro-driven volatility triggers temporary capital outflows or market pullbacks, fundamentally sound, high-quality Hong Kong-listed biopharma assets could attract attention.

II. ASCO 2026: Chinese assets prominently featured, with key focus on first-line lung cancer

Overall landscape

Titles of abstracts released for this year’s ASCO meeting indicate that results from multiple highly anticipated pivotal Phase III trials will be unveiled, including several head-to-head trials directly comparing investigational therapies against current standard-of-care regimens with the potential to reshape treatment paradigms. Notably, Chinese-related assets represent a significant share of the prestigious Late-Breaking Abstract (LBA) session—a segment subject to extremely high selection thresholds and rigorous screening—highlighting the rising global competitiveness of China’s biotech R&D and underscoring its role as an indispensable component of this year’s conference.

We believe ASCO data readouts will serve as a key catalyst this year for business development (BD) collaboration opportunities and individual stock valuations, with data visibility being a focal point for the market.

Akeso’s partner will present overall survival (OS) data from the HARMONi-6 study during the ASCO Plenary Session (May 30). This China-based Phase III trial evaluates ivonescimab (a PD-1/VEGF bispecific antibody) plus chemotherapy versus another PD-1 inhibitor plus chemotherapy as first-line treatment for advanced squamous non-small cell lung cancer (NSCLC).

This OS data represents the first-ever overall survival readout for the ivonescimab-plus-chemotherapy regimen in first-line lung cancer. The market is closely watching whether the data demonstrate statistically significant OS benefit, which would provide critical cross-trial reference for the upcoming readout from Akeso’s global Phase III study (HARMONi-3).

Selection into the Plenary Session is generally viewed as a positive signal. This data release is expected to be one of the most closely watched moments of this year’s ASCO meeting.

Key Highlight #2: Kelun-Biotech ( $SKB BIO (06990.HK)$ ) — Phase III data for Sac-TMT in combination with Keytruda

Kelun-Biotech will disclose detailed results from the OptiTROP-Lung05 study (May 30), a China-based Phase III trial evaluating the TROP2 ADC (antibody-drug conjugate) sacituzumab tirumotecan (Sac-TMT) combined with pembrolizumab versus pembrolizumab monotherapy in first-line PD-L1-positive advanced non-small cell lung cancer (NSCLC). Topline results from this trial previously showed positive signals.

This readout also carries significant strategic implications for Kelun-Biotech’s partner Merck & Co (MRK): detailed data from the China trial will provide critical cross-trial insights to inform Merck’s ongoing global Phase III programs across multiple tumor types.

Innovent Bio will present updated data for its PD-1/IL-2α bispecific antibody IBI363 across several lung cancer indications, including IO-resistant NSCLC, first-line NSCLC in combination with chemotherapy, and squamous NSCLC following chemotherapy/IO therapy. These three datasets span different lines of treatment, helping the market comprehensively assess IBI363’s clinical potential and differentiated positioning.

Other Chinese biotech companies worth watching

III. Investment Implications: Fundamental Allocation Opportunities Amid Macro Volatility

Near-term Catalyst Pathway

The timeline of ASCO-related catalyst events is clear:

● May 21: Full ASCO abstracts officially released (5:00 PM ET)

● May 29 – June 2: Main conference held, with Late-Breaking Abstracts disclosed sequentially

● May 30: Innovent Bio’s HARMONi-6 OS data (Plenary Session); Kelun-Biotech’s sac-TMT Phase III data

● June 1: Innovent Bio’s IBI363 data update

This timeline implies that the Hong Kong-listed biopharma sector will face continuous data-driven catalysts starting May 21, extending through early June.

Medium- to Long-Term Outlook

The globalization of China’s innovative drug industry is entering an accelerated realization phase. This year’s ASCO serves as a concentrated validation window: pivotal Phase III data from Chinese pharmaceutical companies will not only impact their own valuations but also serve as key benchmarks for emerging therapeutic modalities globally—such as PD-1/VEGF bispecific antibodies and ADCs—attracting significant attention from international institutions.

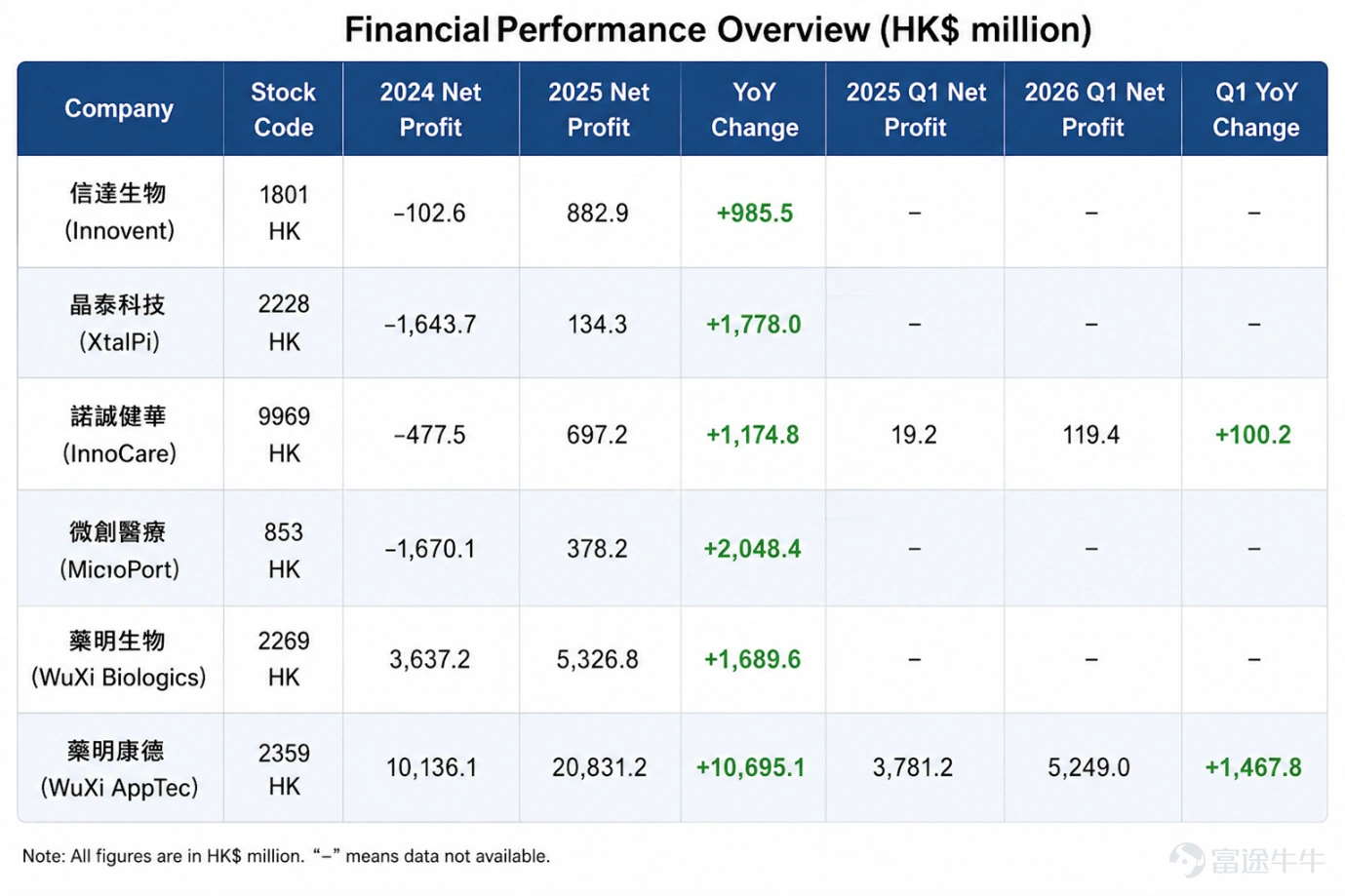

Meanwhile, fundamentals for the Hong Kong biopharma sector continue to improve, as evidenced by recent earnings reports.According to the latest financial data, several Hong Kong-listed biopharma companies turned profitable in 2025, including Innovent Bio (1801.HK), XtalPi (2228.HK), InnoCare Pharma (9969.HK), and MicroPort (0853.HK). InnoCare Pharma, in particular, reported significant year-over-year growth in net profit for Q1 2026. Additionally, Wuxi Biologics (2269.HK) and Wuxi AppTec (2359.HK) maintained profitability and delivered full-year growth, reflecting a steady improvement in overall sector earnings quality.

Source: Bloomberg, as of May 19, 2026

We believe that Hong Kong-listed biopharma assets with the following characteristics warrant close attention in the current environment:

• Possessing pivotal Phase III clinical data即将公布 (imminently to be released)

• Have already secured, or clearly demonstrate the potential to secure, cross-border business development (BD) licensing deals

• Large-cap names with solid commercialization progress and high earnings visibility

Maintaining discipline amid mild macroeconomic fluctuations and focusing on high-quality assets with solid fundamentals represents our recommended strategy in the current market environment.

________________________________________

One-click exposure to leading Hong Kong-listed biotech companies

China AMC Hang Seng Biotech ETF tracks the Hang Seng Biotech Index, whose constituents include globally competitive Chinese biotech firms such as Innovent Bio and Akeso Pharma, offering investors a convenient, efficient, and diversified tool to capture potential growth opportunities in the biotech sector.

$ChinaAMC Hang Seng Biotech ETF (03069.HK)$ It is currently the largest by assets under management (AUM) and most liquid biotech ETF in the Hong Kong market, providing investors with a convenient, efficient, and diversified allocation tool to capture long-term growth opportunities in the biotech industry. 【1】

$SSE Composite Index (000001.SH)$$CSI 300 Index (000300.SH)$$NVIDIA (NVDA.US)$$Amazon (AMZN.US)$$Alphabet-C (GOOG.US)$$Meta Platforms (META.US)$$Tesla (TSLA.US)$$HSTECH (LIST91332.HK)$$Hang Seng Index (800000.HK)$$SSE 50 Index (000016.SH)$$CSI 300 Index (000300.SH)$$CSI 1000 Index (000852.SH)$$SSE Science and Technology Innovation Board 50 Index (000688.SH)$$ChinaAMC CSI 300 Index ETF (03188.HK)$$SSE Composite Index (000001.SH)$$XIAOMI-W (01810.HK)$$JD.com (JD.US)$$TENCENT (00700.HK)$$Shenzhen Component Index (399001.SZ)$$Kweichow Moutai (600519.SH)$$Contemporary Amperex Technology (300750.SZ)$$PING AN (02318.HK)$$Alibaba (BABA.US)$$ICBC (01398.HK)$$CHINA MOBILE (00941.HK)$

Data source

• Goldman Sachs, "China Healthcare: ASCO 2026 China datapoints: focus on potential reshaping of front-line treatment landscape", April 27, 2026

• Goldman Sachs, "Global Healthcare: Pharmaceuticals: What to watch at ASCO", April 21, 2026

• AASTocks: BeiGene – Brukinsa (zanubrutinib) approved by the U.S. FDA for treatment of relapsed/refractory mantle cell lymphoma, May 14, 2026, https://www.aastocks.com/tc/stocks/news/infocast-news/IC4901288/1

• cnyes.com: Hengrui Pharma and BMS form a $15.2 billion strategic alliance, pioneering a 'China-based early R&D + global translation' approach, May 13, 2026, https://news.cnyes.com/news/id/6456767

• Zhitong Finance: Hutchmed (00013.HK) surges over 11% as fruquintinib’s overseas sales growth exceeds guidance, April 1, 2025, https://hk.investing.com/news/stock-market-news/article-867540

【1】Data sourced from China AMC (HK) and Bloomberg, as of May 19, 2026.

Investing involves risks, including the potential loss of principal. Past performance is not indicative of future results. Investors should review the offering documents, including risk factors, before investing in the China AMC Hang Seng Biotech ETF (the “Fund”). You should not rely solely on this information to make investment decisions. Please note:

• The Fund seeks to provide investment returns that closely correspond to the performance of the Hang Seng Biotech Index (the “Index”), before fees and expenses.

• This fund is passively managed. An expected decline in the index will likely lead to a corresponding decrease in the value of this fund.

• Investing in equity securities exposes the Fund to general market risks. Its value may fluctuate due to various factors.

• Since the index is newly established, this fund may face higher risks compared to other ETFs tracking indices with longer operational histories.

• This fund tracks the performance of biotech companies and a specific region (i.e., mainland China and Hong Kong), thus facing concentration risk, and its volatility is likely to exceed that of broadly diversified funds.

• This fund is exposed to risks associated with characteristics of biotech companies, such as lack of revenue, net liquidity liabilities, lower liquidity, higher volatility, reliance on intellectual property or patents, technological changes, increased regulation, and intense competition.

• This fund involves securities lending transaction risks, including the possibility that borrowers may not return the securities on time or even at all.

• This fund involves tracking error risk.

• If cross-counter transfers of fund units between the two counters are suspended, and/or due to any restrictions on services provided by securities brokers and Central Clearing System participants, unit holders will only be able to trade their fund units at one counter. The market price of fund units traded at each counter may deviate significantly.

• Fund unit holders will only receive distributions in Hong Kong dollars. Non-HKD based fund unit holders may incur fees and expenses related to foreign exchange conversion.

• The base currency of this fund is Hong Kong dollars, but there are also fund units traded in US dollars. Investors may incur additional costs or losses associated with foreign currency fluctuations.

• Generally, retail investors can only buy and sell the fund units of this fund on the Hong Kong Stock Exchange, where the trading price of fund units is influenced by market factors such as supply and demand for the fund units. Therefore, the trading price of fund units may trade at a significant premium or discount to the fund’s net asset value.

Market data, case studies, and industry observations mentioned herein are for illustrative purposes only, sourced from public media reports and industry research, and do not constitute investment advice.

Investing involves risks, including the possible loss of principal. Any forecasts, outlooks, or opinions contained herein are provided for your reference only and are not guaranteed to materialize. The information in this document reflects market conditions and our views as of the date of publication and is subject to change without notice. This material is issued by China AMC (HK) Limited. It has not been reviewed by the Securities and Futures Commission of Hong Kong. For full details and risk disclosures regarding the referenced funds, please refer to our official website and prospectus.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

4

5