Waller's new policy measures are in the works! How should investors respond?

Options Sir on Macro | U.S. Treasury yields interrupt AI momentum—how long will this correction last?

First, index declines were limited, with selling pressure concentrated in high-momentum sectors.

U.S. equities showed clear divergence last night. $Dow Jones Industrial Average (.DJI.US)$ rose 0.32%, $S&P 500 Index (.SPX.US)$ edged down 0.07%, $Nasdaq Composite Index (.IXIC.US)$ fell 0.51%. In the final trading hour, Trump again signaled a conciliatory tone, helping narrow market losses. Subsequently, oil prices, Treasury yields, and the dollar retreated, allowing U.S. stocks to partially recover from their lows.

At the index level, markets did not experience a broad, disorderly sell-off; structurally, however, the Nasdaq led the decline, with pressure focused on previously strong-performing sectors such as tech stocks, AI hardware, semiconductors, optical modules, and memory chips. $Micron Technology (MU.US)$ fell nearly 6%, $SanDisk (SNDK.US)$ dropped more than 5%, $Lumentum (LITE.US)$ plunged over 8%; although tech stocks have been the strongest performers recently, they have also become the primary target of concentrated deleveraging.

II. Why did U.S. Treasury yields suddenly rise? The bond market is catching up on delayed repricing from the previous cycle.

After U.S. Treasury yields breached a key threshold, they once again pressured the valuations of growth stocks.The 10-year U.S. Treasury yield briefly rose to 4.631%, and the 30-year yield hit as high as 5.159%. Higher long-end rates increase discounting pressure on future cash flows, directly impacting tech stocks whose valuations rely heavily on distant growth prospects. Loss-making, high-valuation, high-beta fringe AI names face even more pronounced pressure.

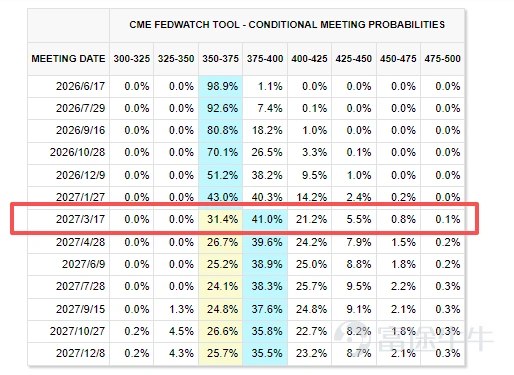

Markets have started revisiting discussions about 'delayed rate cuts, resurgent inflation, and even the return of rate hike risks to the table.'。Three months ago, markets were still betting the Fed would cut rates twice this year. But now,market consensus expects the Fed to hike rates by March next year, and the probability of a rate hike before December this year is nearly 50-50.The bond market’s current pricing path has abruptly shifted from anticipating rate cuts to guarding against rate hikes.

Then why did the bond market suddenly start reacting this time?

The bond market didn’t react sharply right away previously because it was still watching whether rising oil prices would first hurt growth or first push up inflation.If high oil prices first weigh on the economy, bonds could actually benefit, as markets would reprice in expectations of a recession-driven rate cut. However, data from the past two months has shown that the U.S. economy hasn’t significantly slowed down—corporate earnings and consumer spending remain resilient—while inflation expectations have started to rise again. As a result, the bond market has shifted its focus from 'waiting for growth to cool' to 're-guarding against inflation and higher-for-longer rates.' The rise in long-end yields essentially reflects this reassessment.

First, elevated oil prices and Middle East-related risks have pushed up inflation expectations—that’s widely understood. Second, the U.S. fiscal deficit and the resulting supply pressure from longer-dated Treasury issuance have lifted term premiums. Last week’s 30-year Treasury auction cleared at a yield close to 5%, yet demand was only mediocre, indicating that investors require a larger safety cushion.

Third, long-end rates globally are moving higher in tandem. The yield on the 30-year U.S. Treasury has risen to 5.159%, while long-end rates in Japan and Europe are also climbing.There is clear contagion in the long-end bond market: when yields rise in one major economy, it affects other markets through exchange rates, capital flows, and asset allocation decisions.

Fourth, Kevin Warsh’s imminent appointment as Fed Chair has prompted markets to conduct an early credibility test of future policy. He will inherit an environment marked by resurgent inflation pressures, oil price shocks, significant fiscal strain, and heightened market sensitivity to the policy path.

This is precisely the most delicate aspect of the current situation.Markets may have previously hoped Warsh would deliver faster rate cuts, but if long-end rates and inflation expectations have already moved higher, signaling dovishness too soon after taking office could undermine expectations of Fed independence and force the bond market to demand even higher inflation compensation.

Therefore, the rise in U.S. Treasury yields isn’t driven by any single event. Rather, it represents the bond market’s correction of excessive optimism in risk assets over recent months: oil prices haven’t fully retreated, inflation pressures haven’t vanished, fiscal challenges persist, and the path to rate cuts is far less straightforward than markets had previously assumed.

3. Has the momentum stock rally run its course? The main trend remains intact, but the phase has shifted.

For investors, the most critical question is: Have AI-related momentum stocks already peaked?

AI hardware, semiconductors, memory, and optical modules still have fundamental support. Semiconductor earnings per share (EPS) remain robust, and forward valuations haven’t fully decoupled from profitability. Memory prices show no signs of weakening and continue to validate the upcycle. Against the backdrop of AI server demand, HBM adoption, rising memory prices, and expanding compute infrastructure, some leading companies can still justify their share prices with strong earnings.

However, short-term positioning has become overheated—prices have risen too quickly and now need to shake out floating profits and consolidate positions.The market has already started hedging while prices rise; sentiment isn’t as stable as it appears on the surface. This suggests momentum stocks will likely transition from a 'broad-based rally phase' to a 'selection phase.'Leaders with strong earnings, verifiable orders, and valuations still digestible by fundamentals will likely regain strength after this adjustment.

In other words, the market hasn’t abandoned AI—it’s just becoming more selective about AI.

Rotation within the sector is also underway. Software stocks rose against the broader trend yesterday, $ServiceNow (NOW.US)$ rising over 8%, $Figma Inc (FIG.US)$ gaining over 6%, $Salesforce (CRM.US)$ and rising over 3%; semiconductor and AI hardware positions are extremely crowded, while software positions remain subdued;If semiconductor momentum weakens, unwinding of crowded trades could drive capital to rotate rapidly into software stocks in the short term, as investors unwind prior 'long hardware, short software' pairs trades.; Software and cybersecurity serve as near-term transitional destinations for capital during hardware corrections; energy acts more like a macro hedge, enhancing portfolio resilience while oil prices and inflation risks remain elevated.

IV. What to watch next: oil prices, Waller, NVIDIA earnings...

At this juncture, US equities have entered a phase of high volatility and consolidation. Evidence of a systemic bear market remains insufficient, but the one-way rally in momentum stocks has already been disrupted.

In the baseline scenario, the 10-year Treasury yield oscillates repeatedly between 4.5% and 4.7%, pressuring tech valuations, though corporate earnings continue to support the broader indices. AI hardware enters a consolidation phase, while software, cybersecurity, energy, and financials take turns providing temporary leadership. Index performance will hold up reasonably well, but individual stocks and sectors will experience significant volatility.

In an optimistic scenario, Middle East tensions continue to ease, oil prices retreat, and the 10-year Treasury yield falls back below 4.5%, prompting markets to reprice toward improved risk appetite. In that case, previously strong sectors—such as AI hardware, semiconductors, memory, and optical modules—could see a secondary recovery, with core large-cap leaders stabilizing earlier than marginal small-cap names.

In a risk scenario, oil prices remain elevated, pushing the 10-year Treasury yield toward 4.8% or even 5%, reigniting market discussions about potential rate hikes. Under such conditions, US equities could shift from sector rotation to broader deleveraging across risk assets, with high-valuation, unprofitable, high-Beta stocks facing deeper corrections.

On the options front,Investors already holding positions in AI hardware, semiconductors, memory, and optical modules who are concerned about drawdowns should focus on reducing naked risk exposure.For profitable positions, consider partially locking in gains or using options for protection. Investors unwilling to sell their underlying shares but worried about giving back profits might consider covered calls or collar option strategies to $Micron Technology (MU.US)$ For example:

A collar options strategy involves holding MU shares while buying an out-of-the-money put for downside protection and simultaneously selling an out-of-the-money call to partially offset the cost of the put with the premium received. Selling the out-of-the-money call adds an extra layer of cushion to the position. The strike price of the put should reflect your desired downside floor, while the strike price of the call indicates where you’re willing to cap your upside gains.

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

2. For investors looking to buy on dips, avoid rushing to scoop up all deeply declined momentum stocks at once.Consider building positions in stages instead. Better entry signals include: a decline in the 10-year U.S. Treasury yield, core market leaders showing strong volume and halting their downtrend, no further spread of selling pressure within the sector, and the market maintaining resilience following NVIDIA’s earnings release. AI hardware remains the dominant theme over the medium term, but short-term patience is needed as positions and valuations undergo digestion.

Alternatively, if a client is already inclined to buy the stock on a pullback and has a target entry price in mind, they could consider selling slightly out-of-the-money puts expiring in one to two months. If the stock stays above the strike price, the investor keeps the premium; if it falls below, they effectively acquire the shares at a lower net cost.

However, note that momentum stocks have recently seen substantial gains, so naked put selling carries significant risk. This strategy suits clients who believe in MU’s medium-term fundamentals but prefer not to chase the stock at current highs. The core sources of profit are the stock avoiding further steep declines and a drop in implied volatility. Clients unwilling to assume the risk of being assigned the shares should avoid this strategy.

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

Finally, Option Sir brings a small perk for fellow investors, welcome to claim it.Options Beginner Pack

*This event is exclusive to invited HK users. Click to learn more.Detailed event rules>>

Market conditions are complex and volatile,Options StrategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options Strategymaking investing simple and efficient!

Option Risk Warning:An option is a contract that grants the holder the right, but not the obligation, to buy or sell an asset at a fixed price on a specific date or at any time before that date. The price of an option is influenced by various factors, including the current price of the underlying asset, the strike price, time to expiration, and implied volatility. Implied volatility reflects the market’s expectations for the level of volatility in the option over a future period. It is a data point derived inversely from the Black-Scholes option pricing model and is generally regarded as an indicator of market sentiment. When investors anticipate greater volatility, they may be more willing to pay a higher price for options to hedge risks, resulting in higher implied volatility. Traders and investors use implied volatility to assess the attractiveness of option prices, identify potential mispricings, and manage risk exposure.

Disclaimer:This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in trading options can be substantial. In some cases, losses may exceed the initial margin deposited. Even if you set contingent orders such as 'stop-loss' or 'limit' orders, these may not prevent losses. Market conditions may make such orders unexecutable. You may be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any shortfall in your account. Therefore, before trading, you should study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures for exercising options and the rights and obligations upon exercise and expiration. Options trading carries extremely high risks and is not suitable for all investors. Investors should carefully readCharacteristics and Risks of Standardized Options。

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

34

72