OpenAI's growth slowdown reported, is the pullback in AI stocks a risk or an opportunity?

Carriers Enter the Token Era: Understanding China Telecom's Token Plan

The real significance of China Telecom's Token plan lies not in the revenue scale of a single package, but in bridging the 'last mile' of 'computing power as a utility'—lowering the consumption threshold for AI capabilities from enterprise-level to individual-level and flattening the API technical barriers down to phone bill charges. This is a critical turning point event in China's AI industrialization process, transitioning 'from quantitative change to qualitative change.' Carriers may not be the biggest beneficiaries of the Token economy, but they will be the most important catalysts and infrastructure providers. The true Alpha lies within the industry chain, not the carriers themselves.

I. Event Overview: A Comprehensive View of China Telecom's Token Package Solution

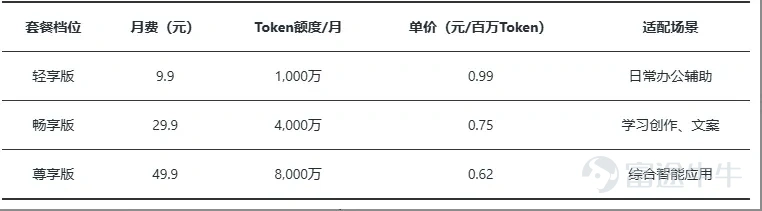

1.1 Package Structure and Pricing

On May 17, 2026, China Telecom officially launched its trial commercial Token package, becoming the first domestic basic telecom operator to systematically productize Token services (Note: Shanghai Telecom had earlier introduced a pay-per-use version; this launch marks the debut of a standardized nationwide tiered package). Developer and SME version (StarCloud large model + mainstream models like GLM5, suitable for AI programming/code debugging/agent building):

Personal and Home version (StarCloud large model + ecosystem models like DeepSeek V3.2, suitable for daily office work/learning creation):

Additional services: Broadband upstream speed-up package + security protection package (optional); supports ordering via the Tianyi Cloud official website and China Telecom app; delivery methods include local hardware or cloud computers; introduces Tianyi Token coins and Token benefits for point redemption.

1.2 The System Engineering Behind It

This package is supported by a complete infrastructure system: Tianyi Cloud TeleCloudOS 5.0 (reducing Token inference latency by 35% and improving efficiency by 300%) + StarCloud TokenHub Operation Service Platform 1.0 (multi-model aggregation + intelligent routing) + a brand-new Token security protection system. In April 2026, China Telecom's Ningxia branch initiated a massive procurement project worth 17.438 billion yuan (including tax), named the 'Token Factory,' divided into 11 bidding packages located in the Ningxia core hub of the national East Data West Compute initiative, setting a historical record for AI service procurement by domestic operators.

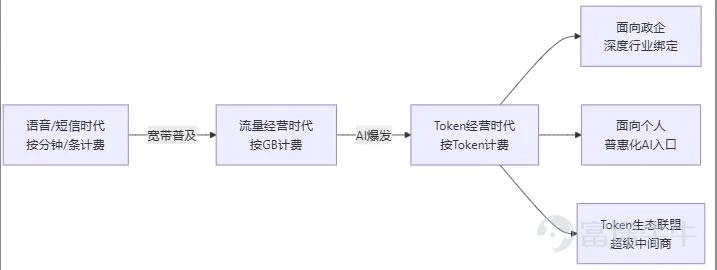

II. Strategic Significance Analysis: Operators Transitioning from 'Selling Traffic' to 'Selling Computing Power'

2.1 Strategic Value for the Operators Themselves

The fundamental driver is background pressure: in 2025, national mobile internet access traffic grew by 17.3%, but revenue from mobile data traffic fell by 3.1%; user base has peaked, and the unit price of traffic has plummeted 90% over the past decade. The traditional scale-for-revenue model has reached its limit. In Q1 2026, the three major operators collectively saw a decline in net profits, making the urgency of transformation self-evident. The essence of Token operation represents the third leap in 'infrastructure as a service':

China Telecom's 2025 foundational base (providing ammunition for this transformation): Tianyi Cloud revenue: 120.7 billion yuan; AIDC revenue: 34.5 billion yuan; Smart revenue: 12.3 billion yuan; over 400 million mobile users + over 200 million broadband users (direct-to-consumer channel capabilities). Chairman Ke Ruiwen of China Telecom has set a clear strategic position: not to become another ByteDance (traffic-driven), not to become another Alibaba (full-stack internet cloud), but to be a 'super AI intermediary'—using government-enterprise channels, industry expertise, and localized delivery capabilities as core weapons to embed Token capabilities seamlessly into government clouds, industry-specific lines, and digital solutions, converting existing customers into AI users without them noticing.

2.2 Implications for China's AI Infrastructure Landscape

A milestone institutional breakthrough: This Token package marks the first time that large model invocation fees can be directly paid through mobile phone bills, signaling the evolution of AI computing power from an "enterprise-level high-threshold resource" to a "standardized public utility akin to water and electricity." Deputy Director Yu Ying of the National Data Bureau confirmed this trend: "The growth in Token invocation volumes is driving a shift in the business models of computing power service providers, with the supply of computing power transitioning from selling raw computing capacity to providing services and capabilities." Macro significance: China's daily average Token invocation volume has exceeded 140 trillion. The three major telecom operators are collectively focusing on Token operations, and public data shows that by 2025, China's public cloud large model invocation volume will grow 16-fold year-on-year. Systematic intervention by telecom operators is expected to further increase overall invocation scale by one to two orders of magnitude. This holds strategic value for the democratization of China's AI application layer and the integrity of domestic AI infrastructure.

Three, Feasibility Assessment: Operators' Resource Endowments and Core Challenges

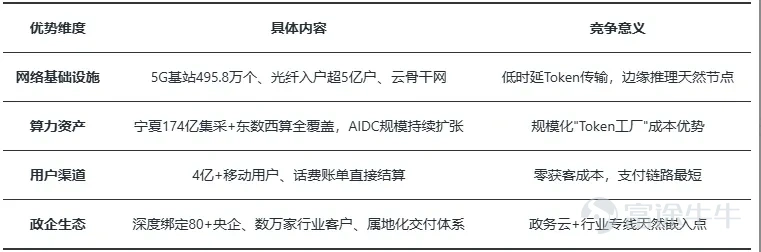

3.1 Resource Endowments: Four Natural Advantages

The trustworthy foundation of central state-owned enterprises serves as a differentiated barrier: In government and enterprise scenarios with stringent requirements for data security, compliance audits, and identity verification, the state-owned background of telecom operators forms an invisible threshold that internet cloud vendors find difficult to replicate.

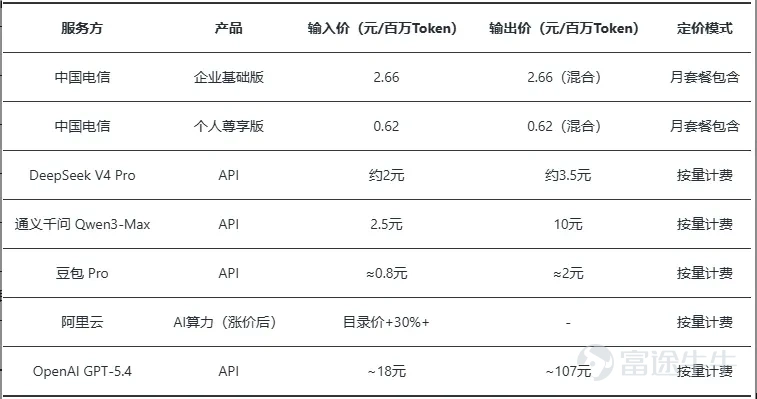

3.2 Analysis of Pricing Competitiveness

Key Pricing Comparison Table (As of May 2026):

Core assessment: The pricing of operator enterprise packages (2-2.66 yuan per million Tokens) matches leading domestic model APIs, slightly higher than ByteDance's DouBao, but the experience advantages of the package model—monthly inclusive consumption, no additional settlement complexity, and direct payment via phone bills—are substantially attractive to small and medium-sized enterprises and long-tail developers. For individual users, the rate of 9.9 yuan per 10 million Tokens equates to 0.99 yuan per million Tokens, lower than most competing products, indicating strong pricing competitiveness.

Risk Warning: Ultra-low promotional prices offered by some internet cloud vendors (e.g., DeepSeek V4 Pro at only 0.025 yuan per million Tokens after deep caching) may still pose price undercutting threats in specific scenarios.

3.3 Core Challenges: Three Unavoidable Weaknesses

Challenge One: Weak technical autonomy. China Telecom's proprietary Xingchen large model capabilities still lag behind DouBao/Qwen/Baidu Wenxin. Currently, the package relies on third-party models (DeepSeek V3.2, GLM5, etc.), meaning profit margins are constrained by upstream model providers. The gross margin structure resembles a 'Token operator' (OpenRouter charges about a 5.5% platform fee) rather than a 'Token factory' (Fireworks AI has around a 50% gross margin).

Challenge Two: Ecosystem construction is still in its infancy. ByteDance DouBao’s daily token consumption rose from 60 trillion tokens per day at the end of 2025 to 120 trillion tokens per day by April 2026, driven by numerous consumer-end proprietary application scenarios. Operators lack similarly powerful 'killer AI applications' to drive token usage, and their AI STORE agent marketplace is just getting started, with developer stickiness yet to be proven.

Challenge Three: Brand perception mismatch. In the minds of consumers and developers, operators are labeled as 'telecommunication service providers' rather than 'AI service providers.' Building a brand image as a 'trusted AI platform' will take time and puts them at a disadvantage compared to technology brands like Alibaba Cloud and Tencent Cloud.

4. Industry Impact Analysis

4.1 Impact on cloud vendors – Controllable effects, mainly differentiated competition

Core assessment: The impact of operator token packages on cloud vendors should not be overstated for the following reasons: Clearly stratified markets – cloud vendors excel in technical ecosystems (self-developed chips/full-stack models/developer tools), while operators have strengths in government-enterprise channels and localized services; they target different customer groups, avoiding head-to-head competition.

Cloud vendors have raised prices for self-protection: Alibaba Cloud increased AI computing power pricing by up to 34%, Tencent Cloud’s HunYuan series rose by 463%, and Baidu Cloud increased by 5-30%. Cloud vendors are leveraging strong demand to reshape pricing dynamics and are not immediately threatened by low-cost competition.

Alibaba Cloud accelerates AI monetization: In Q4 2026 (FY26Q4), Alibaba Cloud's external commercial revenue grew by 40% year-over-year, with AI-related products accounting for over 30% (approximately 35.8 billion annualized), aiming for AI to contribute more than 50% within a year, targeting 100 billion USD in cloud and AI-related business revenue by 2031. Alibaba’s full-stack AI capabilities remain difficult for operators to challenge in the short term.

The real impact falls on smaller cloud service providers in the intermediate layer: General cloud providers lacking core model capabilities face the most challenging situation under the large-scale token package strategies employed by operators.

4.2 Boost to the AI application ecosystem – Most certain positive impact

The multiplier effect of lowering usage barriers: Shanghai Telecom's pay-as-you-go version: 1 yuan = 250,000 Token quota, settled via mobile phone bills, with API access to over 30 mainstream models. Developers no longer need corporate cloud accounts or credit card binding, eliminating the entry barrier for long-tail developers. Jiangsu Mobile's "Crayfish AI Token Package" saw daily Token sales exceed 800 million within a month of its launch, validating the market demand for inclusive pathways. During the 2026 Spring Festival, Tianyi Zhiling surpassed 4 million AI-generated users, with average daily Token consumption increasing 14-fold—indicating initial validation for C-end scenarios.

Three directions driving new use cases: 1. Explosion in long-tail Agent development: Low-cost API calls enable individual developers to scale up the creation of vertical intelligent agents, accelerating the prosperity of AI STORE-like app stores; 2. Increased ARPU for AI office/content tools: SaaS providers' AI membership penetration will significantly rise due to reduced Token costs; 3. Seamless integration of government-enterprise Tokens: Operators will invisibly embed Token capabilities into government clouds and industry-dedicated lines, converting existing government-enterprise customers without their awareness, addressing the "last mile" of AI commercialization.

4.3 Investment Judgment

Core viewpoint: Operator Token packages mark a milestone in the public infrastructure transformation of AI computing power. In the short term, they act as sentiment catalysts, while in the medium term, they serve as triggers reshaping the industry landscape. The profit logic lies in the incremental growth from "Token democratization → consumption scale × N times," rather than improvements in operators' own profitability. The essence of operators' Token business leans more towards being an "operator" than a "factory," with limited gross margin ceilings, but the traffic it generates will nourish the entire industrial chain. Risks upfront: Weak proprietary model capabilities of operators, profits constrained by upstream model vendors, potentially persistently low gross margins for Token businesses; under the trend of cloud vendor price hikes, operators’ mid-to-low-priced packages may trigger price war rebounds; lengthy validation cycles for government-enterprise use cases, with Token business scale contributing limitedly to operators' total revenue within 1-2 years; the "Operator Version OpenRouter" model of Token economics faces risks of insufficient platform stickiness and user attrition.

4.4 Investment Directions

Direction One: Operators themselves (low risk, low volatility, allocation attribute) Direction Two: Beneficiaries of Token factories (high volatility, key focus) Direction Three: Token operators/intermediaries (high volatility, high uncertainty) Direction Four: AI applications/SaaS (benefiting from Token price cuts, ARPU growth logic) Direction Five: Computing power industrial chain (continued high prosperity, watch for acceleration in domestic substitution).

All analyses in this article are based on publicly disclosed information and open-source research as of May 17, 2026, and do not involve undisclosed material information. This article is for informational reference only and does not constitute any investment advice. Readers bear full responsibility for risks associated with any actions taken based on this content.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

3