NVIDIA is pushing hard on 800V—so who’s selling the shovels in power semiconductor?

NVIDIA leads the upgrade to 800V DC architecture, ushering in an accelerated penetration phase for silicon carbide power devices

The explosion of AI computing power has made electricity a core bottleneck in data center development. NVIDIA has established 800V HVDC as the standard power supply solution for the next generation of AI factories, which will drive explosive growth in demand for silicon carbide power devices. Specifically, AI power systems and AI infrastructure construction are deeply coupled and co-evolve, together forming the core underlying support for high-quality development of the artificial intelligence industry. As a key representative of third-generation semiconductors, silicon carbide power devices represent the most certain technological upgrade direction and core growth driver in the current AI power field. From energy conversion efficiency, high-voltage and high-current adaptability to the maturity of the entire industry chain, silicon carbide demonstrates comprehensive advantages in AI high-voltage power applications that traditional silicon-based devices cannot match. Data shows that by 2030, AI power supplies will account for 50% of the SiC power market, driving nearly a 10-fold increase in demand for SiC substrates and equipment. The power semiconductor industry has now entered a structural price increase cycle, with price hikes generally reaching 10%-25%, presenting a historic investment opportunity for the silicon carbide industry chain.

NVIDIA leads the upgrade to 800V DC architecture, ushering in an accelerated penetration phase for silicon carbide power devices

Electricity has become the decisive factor in determining the competitive landscape of AI computing power. Global data center electricity consumption is expected to soar to 1,264 TWh by 2030. The power of single AI training cluster cabinets has already exceeded 200kW and is rapidly evolving toward megawatt levels. Traditional 54V power architectures suffer from severe line losses under high current conditions and can no longer support the continued expansion demands of AI computing power. In this context, the 800V high-voltage direct current (HVDC) architecture has become an industry consensus. NVIDIA has officially established it as the core power supply solution for the next generation of AI factories and plans to fully deploy it starting in 2027. This architecture can increase end-to-end power supply efficiency to over 98.5% and reduce energy losses by more than 60%, supporting cabinet power to jump from 200kW to 1MW. Silicon carbide, with its core material properties of high voltage resistance, low loss, and high-temperature tolerance, has irreplaceable advantages in 800V high-voltage power scenarios and has been listed by Citrini Research as the most undervalued core theme in the AI field.

The current price hike in the power semiconductor industry is continuing to gain momentum. Leading international manufacturers such as Infineon, Texas Instruments, and STMicroelectronics, along with domestic leaders like Silan Microelectronics and New Clean Energy, have issued dense price increase notices. Product price increases generally range from 10%-25%. The extreme energy demands of AI data centers are the core driver behind this round of price hikes. From an investment perspective, it is recommended to focus on leading companies in the silicon carbide industry chain that have high technical barriers, fast capacity expansion, and have entered NVIDIA's supply chain, prioritizing investments in the four core segments of substrates, epitaxy, devices, and modules.

Figure 1: Trend of the third-generation semiconductor index

Source: Wind

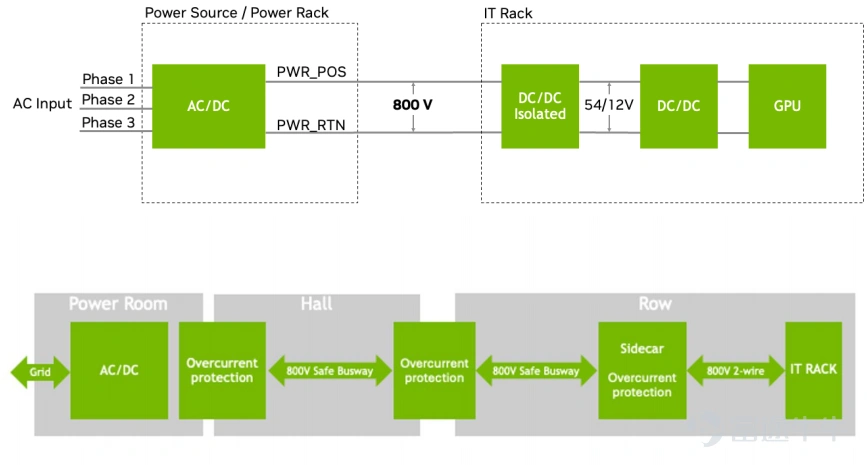

800V HVDC: Power architecture upgrade for AI data centers

*What is the 800V high-voltage direct current architecture? What are its core advantages?

In October 2025, NVIDIA released the white paper '800V DC Architecture for Next-Generation AI Infrastructure' at the OCP Global Summit, officially defining 800V high-voltage direct current (HVDC) as the standard power architecture for next-generation AI factories.

The 800V HVDC architecture simplifies the traditional multi-stage conversion into a two-stage conversion process: "13.8kV AC → 800V DC → GPU voltage":

The first stage involves converting 13.8kV alternating current directly to 800V direct current through medium-voltage rectifiers or solid-state transformers (SST) located at the periphery of the data center. The second stage involves reducing the 800V direct current to the 1.8V-12V voltage required by GPUs through DC/DC converters inside the racks.

According to official NVIDIA data, the 800V HVDC architecture offers comprehensive revolutionary advantages over traditional 48V/54V power architectures: its end-to-end efficiency can reach up to 90.3%, which is more than 5% higher than traditional architectures. For example, in a 100MW data center, this 5% efficiency improvement alone can save over 40 million yuan in electricity costs annually. At the same transmission power, the 800V architecture reduces current to about 1/15th of the 54V architecture, reduces copper usage by 45%, and allows the same cross-sectional conductor to transmit 85% more power. It also supports rack power densities of 1MW and above, leaving ample room for the continued expansion of future AI computing power. Additionally, this architecture reduces 3-4 power conversion stages, decreasing system failure points by 70% and maintenance costs by 70% simultaneously. More importantly, the perfect synergy between the 800V HVDC architecture and liquid cooling systems has become the standard configuration for AI data center construction in 2026.

Figure 2: NVIDIA's 800V architecture

Source: Company official website

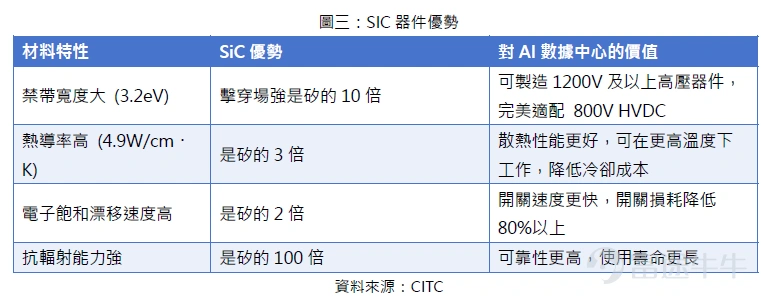

*Why Silicon Carbide?

In an 800V HVDC architecture, power semiconductors responsible for energy conversion and transmission are at the core of the entire system. As a third-generation semiconductor material, silicon carbide (SiC) offers unparalleled advantages over silicon-based devices in high-voltage, high-frequency, and high-temperature scenarios: its breakdown electric field strength is 10 times that of silicon, naturally fitting 800V and future higher voltage architectures without requiring multiple silicon-based devices to achieve high voltage resistance, significantly simplifying circuit design and reducing series losses; on-state resistance and switching losses decrease by more than 50% and 80%, respectively, directly contributing to achieving over 98.5% end-to-end efficiency in 800V HVDC systems, substantially lowering data center electricity costs; operating temperatures can reach above 200°C, far surpassing the 125°C limit of silicon-based devices, allowing better endurance against heat dissipation pressures brought by the high power density of AI data centers while reducing the size and energy consumption of cooling systems; supporting higher switching frequencies allows significant reductions in the dimensions of passive components such as transformers and inductors, increasing power module density by over three times, perfectly matching power needs for single cabinets of 1MW or more; additionally, SiC devices have higher radiation resistance and longer lifespans, effectively reducing system failure points and maintenance costs over their lifecycle, becoming irreplaceable core components of 800V HVDC architecture.

Global renowned AI supply chain research institution Citrini Research noted in its latest report: "Whether it's efficiency requirements, technical compatibility, or industry chain maturity, silicon carbide holds irreplaceable advantages in AI high-voltage power scenarios. AI power supplies and AI infrastructure complement each other, forming the core support for AI industrial development, with silicon carbide being the key incremental component in AI power supplies." SiC devices play an indispensable role in every power conversion stage of 800V HVDC systems: in medium-voltage rectifiers and solid-state transformers (SST), they handle the core task of directly converting 13.8kV AC to 800V DC, requiring large quantities of 1200V-1700V SiC MOSFETs and diodes; SSTs using SiC devices can reduce volume and weight by 60%-90% and increase power density fivefold; in cabinet-level DC/DC converters, they convert 800V DC to 48V or 12V, improving conversion efficiency by 2%-3% and increasing power density by over 40%; in server power supplies (PSU), PSUs above 3kW have fully adopted SiC devices, achieving efficiencies of over 98%, a 1.5%-2% improvement over traditional silicon-based PSUs; furthermore, SiC devices' excellent high-temperature characteristics allow them to integrate seamlessly with liquid cooling systems, further boosting the power density of liquid-cooled power modules, fully meeting the high-power, high-density power demands of AI data centers.

Figure 3: Advantages of SiC Devices

Analysis and Investment Opportunities in the Silicon Carbide Industry Chain

The silicon carbide industry chain can be divided into three major segments: upstream substrates and equipment, midstream epitaxy and device manufacturing, and downstream packaging and testing. Among these, substrates and epitaxy represent the highest technological barriers and most concentrated profit margins, accounting for approximately 50% and 20% of device costs, respectively.

*Upstream: Substrates and Equipment

Substrates are the most critical segment of the silicon carbide industry chain, presenting the highest technological barrier. Currently, the global SiC substrate market is mainly dominated by companies like$Wolfspeed (WOLF.US)$ 、$SICC Co.,Ltd. (688234.SH)$ , Tianke Heda, etc.

Sky Advanced (688234.SH): The absolute leader in domestic silicon carbide substrates, with a global market share of 16.7%. The company masters both semi-insulating and conductive substrate technology routes; its semi-insulating products hold over 30% of the global market share, while its conductive substrates rank second globally. It has achieved mass production of 8-inch substrates, and made substantial progress in 12-inch substrate R&D. Clients include international giants like Infineon, Bosch, and NVIDIA’s data center power supply chain. Equipment is the core guarantee for capacity expansion. In silicon carbide manufacturing equipment, PVT furnaces (used for substrates) are the most critical. Previously reliant on Germany’s PVA TePla, domestic manufacturer Northern Huachuang now holds a 61% market share, with most domestic companies using their equipment.

$NAURA Technology Group (002371.SZ)$ : Leading domestic semiconductor equipment provider, holding a 61% market share in silicon carbide PVT furnaces, with breakthroughs also achieved in epitaxial equipment. As a key target for domestic substitution, it accounts for over 50% of equipment used in local wafer fabs such as Yangtze Storage's production expansions. It ranks first in domestic market share for etching and thin-film deposition equipment. Short-term benefits come from the global semiconductor price surge and a new round of fab expansions, while long-term growth will be driven by the acquisition of Core Micro to enhance photoresist coating layout advantages. Key risks stem from U.S. export controls and advanced process technology breakthrough timelines.

*Midstream: Epitaxy and Device Manufacturing

Epitaxial wafers are a layer of silicon carbide film grown on a substrate, directly impacting device performance. Major domestic epitaxy companies include Sanan Optoelectronics (600703.SH), Hanteck, and Dongguan Tianyu.

$Sanan Optoelectronics (600703.SH)$ : Leader in domestic compound semiconductors, having built China’s first 8-inch silicon carbide wafer production line with an annual capacity of 720,000 wafers. Products have been validated by automakers such as Li Auto and BYD, and entered the AI data center power supply market. Device manufacturing involves processing epitaxial wafers into silicon carbide diodes, MOSFETs, etc. Global giants Infineon, STMicroelectronics, and ON Semiconductor dominate 83% of the market share, but domestic companies are catching up quickly.

$StarPower Semiconductor (603290.SH)$ : Domestic IGBT leader, with silicon carbide modules already in mass application for new energy vehicles, and expanding into the AI data center power sector.

$Hangzhou Silan Microelectronics (600460.SH)$ : Domestic power semiconductor leader, achieving mass production of silicon carbide diodes and MOSFETs, with prices for some device products increasing by 10% starting March 1, 2026.

*Downstream: Packaging, Testing, and Modules

Packaging and testing is the final stage of the silicon carbide industry chain, directly affecting device reliability and heat dissipation performance. Major domestic packaging and testing enterprises include...$JCET Group Co., Ltd. (600584.SH)$ 、$TongFu Microelectronics (002156.SZ)$ 、$Tianshui Huatian Technology (002185.SZ)$Wait.

Disclaimer: The information provided in this report, or any investment or potential transaction related thereto, is subject to the applicable laws and regulatory requirements of your jurisdiction, and you are solely responsible for compliance with such laws and regulations. The content of this report is for reference only and does not constitute any investment advice. Our company has made every effort to ensure the accuracy of the financial information provided, but assumes no responsibility or provides any form of guarantee for the accuracy, completeness, or effectiveness of all or part of the content. We will not be liable for any errors or omissions. Please also note that securities and virtual asset prices can fluctuate, especially given the extremely high risks associated with virtual assets, and investors should exercise caution and assume investment risks on their own.

———————————————————————

About the author:

Victory Securities - Hong Kong's Leading Virtual Asset BrokerVictory Securities (08540.HK), with over 50 years of history in Hong Kong, is a comprehensive full-service licensed brokerage offering four main business services to retail investors, institutional investors, high-net-worth clients, and enterprises: wealth management, asset management, virtual assets, and capital markets. It has received numerous accolades and essential qualifications in the Asia-Pacific region. In 2023, Victory Securities became the first licensed brokerage in Hong Kong to hold licenses issued by the Securities and Futures Commission for virtual asset trading, advisory, and asset management services. It was also approved by the SFC to provide virtual asset trading and advisory services to retail investors, offering one-stop compliant and legal Bitcoin and Ethereum trading, exchange, and deposit/withdrawal services.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

5