PDD Holdings reported Q1 revenue of RMB 106.2 billion—has its share price already hit bottom?

In-depth Analysis of Alibaba's FY26Q4 Earnings Report: Confirmation of AI Commercialization Inflection Point and Valuation Restructuring

I. Core Perspectives

1.1 AI commercialization inflection point confirmed, exponential growth exceeds expectations

Alibaba Cloud's AI commercialization has entered a substantive harvest period. In FY26Q4, revenue from AI-related products reached approximately RMB 9 billion (annualized at RMB 36 billion), accounting for 30% of the cloud intelligence group’s external revenue. According to management, it is expected that in about a year, the proportion of revenue from AI-related products will exceed the 50% threshold, becoming the core engine driving cloud business revenue growth.

More noteworthy is the exponential growth of the MaaS (Model as a Service) business. According to management, the ARR of the BaiLian MaaS platform has exceeded RMB 8 billion, and it is expected to reach RMB 10 billion in June and surpass RMB 30 billion by the end of the year - implying a 3.75x growth within six months. This exponential growth rate far exceeds the linear extrapolation thinking accustomed to by the market, making it one of the most underestimated variables in the AI era.

On the other hand, management stated that "every chip is fully utilized," indicating current growth is constrained by chip supply rather than insufficient demand. With U.S. approval for selling H200 chips to Chinese companies (including Alibaba, ByteDance, Tencent, etc.), once supply bottlenecks ease, growth may further accelerate.

1.2 Clear path for profitability improvement in cloud business

Alibaba Cloud’s EBITA margin in FY26Q4 was 9%. According to management, the cloud business EBITA margin is expected to rise to the "teens" range over the next two quarters, with a long-term target of 20%. This improvement path is driven by three factors:

1. High-margin mix shift of MaaS: The gross margin of MaaS business could reach 50-70%, and as its share continues to increase, it will significantly drive overall profitability.

2. Improved computing power utilization: According to management, the data center payback period is "better than expected," suggesting a significant increase in factory capacity utilization.

3. Pingtouge chips achieve cost reduction: Self-developed chips cumulatively delivered 470,000 units, with 60% serving external customers, and economies of scale are beginning to show

1.3 Key expectation gap: The market prices based on retail metrics, overlooking the full-stack value of AI + cloud

The author believes that the current market pricing for Alibaba reflects a fundamental mismatch. The market remains focused on slowing GMV growth for Taobao/Tmall, as well as competition from PDD Holdings/ByteDance in the retail business, assigning an '8-10x PE' valuation typical for a 'retail company.' However, in reality, Alibaba is the only cloud computing company in China with full-stack AI capabilities:

Infrastructure layer: Pingtouge's self-developed chips have cumulatively delivered 470,000 units

Model Layer: The Qwen open-source model has exceeded 1 billion downloads, with Model Studio customer numbers increasing 8-fold

Platform layer: The Bailian MaaS platform’s ARR rapidly climbed to 30 billion

Application Layer: Qwen APP boasts 158 million monthly active users, integrated into DingTalk AI

1.4 Valuation restructuring timing: Investment logic over a 2-3 year horizon

The author believes that Alibaba's valuation increase is not a short-term trading opportunity but rather a 2-3 year valuation restructuring logic. If MaaS ARR reaches 30 billion as expected, and cloud profit margins enter the teens range, the main catalysts for valuation restructuring will emerge between FY27-FY28 (around 2027). This could be similar to the valuation paradigm shift triggered by Amazon AWS when it first disclosed its financials independently in 2015.

2. Management's Strategic Statement: The "AI Factory" Framework

2.1 Clear Statement on the Inflection Point of AI Commercialization

During the FY26 Q4 earnings call, management made a clear statement for the first time that the inflection point for AI commercialization has arrived:

"The inflection point for AI + cloud commercialization has now arrived… Revenue from AI-related products accounts for 30% of the external revenue of the Cloud Intelligence Group. It is expected that in about one year, the proportion of revenue from AI-related products will surpass the 50% threshold, becoming the core driver of cloud business revenue growth."

The key significance of this statement lies in:

1. Quantitative Anchor: Specific figures for AI revenue share (30%) and timeline (within 1 year → 50%) were provided for the first time

2. Strategic Positioning: Clarified that AI will become the 'core engine' rather than a supplementary business

3. Verifiability: Track the change in AI revenue contribution every quarter to verify management guidance

2.2 "AI Factory" Investment Framework: Manufacturing Logic

CEO Wu Yongming introduced the "AI Factory" investment framework during the earnings call, which is key to understanding Alibaba's AI strategy:

"AI is more like manufacturing. When we want to increase revenue, we must build two core factories — the AI training factory and the AI inference factory. Behind these two factories lies the construction of data centers, which will consume a significant portion of the group’s free cash flow. However, the commercialization path for these necessary data center investments is very clear... with an expected return on investment within the next 3-5 years."

The deeper meaning of the "manufacturing" narrative:

1. Predictable input-output: Unlike traditional internet models that focus on "spending to acquire customers," AI infrastructure investments show a linear relationship between input and revenue output

2. Significant economies of scale: Increased utilization of data centers reduces per-unit computing costs

3. Clear ROI timeline: A 3-5 year investment return cycle, providing reassurance to the capital markets

Two core factories:

AI training factory: Used for large model training, requiring large-scale GPU clusters, with concentrated investment but cyclical usage

AI inference factory: Used for model inference services, with continuous and stable demand, being the direct source of MaaS revenue

According to management, the current data center payback period is 'better than expected,' validating the effectiveness of this investment framework.

2.3 Three major funding guarantees

Management has clarified the three major sources of funding supporting AI investment:

1. Stable cash flow from consumer business: Taobao and Tmall continue to contribute; flash sales losses are expected to narrow significantly over the next two years, with international operations transitioning from loss to profit

2. Cloud business cash flow reinvestment: Investment in cloud infrastructure → Acceleration of AI cloud revenue → Gross margin improvement → Formation of a virtuous cycle

3. Strong balance sheet: Net cash as of March 31, 2026 is approximately USD 38 billion (including long-term debt maturing in over 5 years of approximately USD 58 billion)

2.4 Five-year goals for cloud business

Management reiterated the long-term goals for the cloud business:

"The revenue target for cloud + AI-related businesses from 2026-2031 is set to exceed USD 100 billion, implying a CAGR of over 40% over the next five years; the long-term EBITA margin target for the cloud business is 20%."

Goal breakdown:

Current cloud business revenue is approximately USD 22 billion (FY26 approximately RMB 158 billion)

Reaching USD 100 billion in five years will require an annual compound growth rate of 35-40%

An increase in profit margin from the current 9% to 20% implies that profits will grow at a faster pace.

III. In-Depth Analysis of Core Business Segments

3.1 Cloud/AI Business: Growth Engine

3.1.1 Quantitative Breakdown of AI Revenue

In FY26 Q4, revenue from Alibaba Cloud's AI-related products reached a key milestone:

Key Insights:

1. MaaS ARR shows exponential growth: Growing from 8 billion to 300 billion in just six months, representing a 3.75x increase, far exceeding linear expectations. According to management, this target will be achieved "earlier than the end of the year," likely being reached in September or October.

2. Higher quality B-end commercialization: B-end token consumption accounts for only 25% of total volume but contributes 50% of external cloud revenue, with ARPU being 8-10 times that of C-end.

3. Supply constraints rather than insufficient demandAccording to management, 'every card is fully utilized,' and the current growth rate is actually constrained by GPU supply.

3.1.2 Path to Cloud Margin Improvement

The improvement in Alibaba Cloud's profit margin is the most important earnings catalyst for FY27:

Current Status (FY26Q4):

EBITA margin: 9%

Main drag: Traditional IaaS price wars, peak depreciation of AI infrastructure

Near-term Guidance (FY27Q1-Q2):

According to management, the EBITA margin for the cloud business will significantly improve to the 'teens' range over the next two quarters. This is the first time management has provided specific guidance on the magnitude.

Long-term Target:

EBITA margin: 20%

MaaS Gross Margin: 50-70% (Source: Company CB Minutes)

Drivers of Margin Improvement:

1. Mix shift towards high-margin MaaS: As the proportion of MaaS revenue continues to increase, the rise in high-margin business share will significantly boost overall profitability

2. Increased utilization rate of inference factories: According to management, the data center payback period is "better than expected." With the surge in MaaS demand, the capacity utilization rate of inference factories has significantly increased, reducing per-unit computing costs

3. Enhanced pricing power: In March 2026, Alibaba Cloud announced a price increase for GPU computing power products, with T-Head computing cards rising by 25-34%, reflecting favorable supply and demand dynamics for sellers

4. Economies of scale for T-Head chips: Cumulative delivery of 470,000 units, with 60% serving external customers; self-developed chips will contribute to margin improvement

3.1.3 Full-stack AI Layout

Alibaba is the only cloud computing company in China with full-stack AI capabilities:

Infrastructure layer:

Pingtouge chips: cumulative shipments of 470,000 units, with over 100,000 units of Zhenwu PPU deployed at scale

Alibaba Cloud IaaS: 29 regions globally, with over 90 availability zones

36% market share of IaaS in China (Gartner), continuously increasing

Model and platform layer:

Tongyi Qianwen: open-source downloads exceeding 1 billion, one of the most widely used open-source models globally

Bailian MaaS Platform: ARR rapidly growing, supporting third-party models

Model Studio: customer count increased 8 times year-over-year

Application Layer:

Qianwen APP: 158 million monthly active users (peaked at 300 million during the Spring Festival)

Wukong Platform: Enterprise-level Agent, fully operational on DingTalk

ATH Business Group: Directly overseen by CEO Yongming Wu, integrating the entire AI commercialization chain

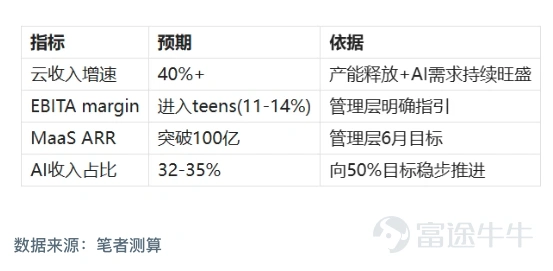

3.1.4 FY27Q1 Outlook (April-June 2026)

Based on management guidance and business trends, the author's expectations for cloud business in FY27Q1 are as follows:

Key monitoring points:

Whether the cloud EBITA margin enters the teens as expected, which is the primary indicator to verify the path of profitability improvement

Whether MaaS ARR reaches 10 billion, validating the sustainability of exponential growth

According to management, Capex may exceed the 380 billion guidance, requiring close attention to actual investment pacing

3.2 E-commerce Business (Taotian Group): Opportunities amid cognitive biases

FY26Q4 Taotian Group CMR (monetization rate) data shows a divergence of 'weak on paper, strong in substance'

Reported CMR: Year-over-year +1%

Like-for-Like CMR: Year-over-year +8%

Source of discrepancy: Impact of new marketing program -7 percentage points

According to management, the new marketing program has signed one-year contracts with merchants. This -7 percentage point impact will last for a year. This means that the full-year reported CMR for FY27 will remain under pressure, but the actual monetization capability is improving.

Cognitive bias opportunity:

Most investors only look at the reported CMR figures, which could lead them to mistakenly believe that e-commerce fundamentals are deteriorating. However, in reality:

1. The +8% Like-for-Like CMR demonstrates that monetization capability is improving.

2. When GMV growth accelerates, the gap between reported CMR and actual CMR will widen (due to the increase in contra revenue absolute amount)

3. Core commerce EBITA remains stable (excluding express purchases), with no damage to profit quality

This cognitive bias precisely provides an opportunity for expectation differential.

3.3 Instant retail (express purchases): Clear path to loss reduction

FY26 Q4 instant retail business shows positive signals:

AOV (average order value) growth

Losses narrowed quarter-over-quarter

According to management, UE (unit economic model) will turn positive in a certain month of FY27. However, it should be noted thatUE turning positive does not equal EBITA turning positive:

UE: Per-order delivery revenue - Per-order delivery cost - Per-order subsidy

EBITA: Depreciation, headquarters allocation, R&D expenses, and other items still need to be deducted

The path to reducing losses is expected to follow the timeline previously provided by management.

Factors driving loss reduction:

Increase in AOV (already observed)

Market share stability (management stated 'at least maintain stability,' but the author believes it may be challenging given the decrease in subsidies, requiring support from growth in non-food delivery order volumes)

Improvement in subsidy efficiency

3.4 All Others (AI investment): Short-term pressure and long-term value

3.4.1 Breakdown of FY26 Q4 losses

The All Others segment's loss for FY26 Q4 was 21.2 billion yuan, a significant increase from 9.8 billion in Q3, mainly consisting of two parts:

1. One-time items: Spring Festival Thousand Questions user subsidy marketing expenses (estimated at 5 to 8 billion USD, activities such as '3 billion USD free milk tea')

2. Ongoing projects: AI training operational costs, model iteration costs, Thousand Questions C-end customer acquisition (estimated at 13 to 16 billion USD/quarter baseline)

According to the author's research, Thousand Questions advertising spending figures have declined quarter-over-quarter, supporting the view that Q2 losses will approach the lower end of the range.

3.4.2 FY27Q1 Outlook

According to management, FY27Q1 (the upcoming disclosed quarter) All Others loss will be "above 10 billion but below 20 billion USD." This wide range (spanning 10 billion USD) reflects internal uncertainty in forecasting incremental AI training costs:

Lower limit (10 billion): Complete withdrawal of Spring Festival subsidies, better control of AI training costs

Upper limit (20 billion): Release of new models (e.g., Qwen4.0 full-modal large model) brings substantial training costs

FY27 Full-Year Expectations:

High certainty of Spring Festival subsidy withdrawal (reducing losses by 3 to 5 billion USD)

However, AI training costs are ongoing. According to management, there are expenditures such as model and AI training computing power costs.

The author expects that the full-year loss will still be substantial.

How should investors view this?:

This is the inevitable cost of strategic AI investment. Management’s 'AI Factory' framework has outlined a 3-5 year return on investment; short-term losses are for long-term value creation. The key is to monitor whether AI revenue growth materializes as expected.

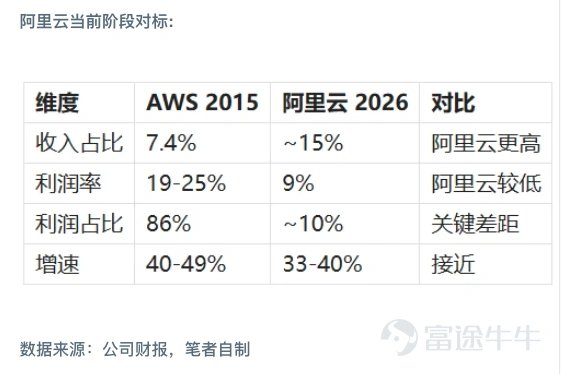

Fourth, AWS comparative insights: Historical experience in valuation restructuring.

As a thought experiment, we can refer to Amazon Web Services’ historical experience to understand the potential for Alibaba Cloud's valuation restructuring.

AWS's valuation turning point (2015):

In Q1 2015, Amazon first independently disclosed AWS financial data, triggering a shift in valuation paradigm:

AWS accounted for only 7.4% of revenue but contributed 86% of profits.

The market realized that Amazon was not merely a 'retailer,' but a 'technology company with a high-profit cloud engine.'

The stock price has risen 118% year-to-date, with the valuation multiple jumping from 1.6x PS to 4.3x PS.

Alibaba Cloud's current benchmarking phase:

Key differences:

Amazon represents 'low-margin retail + high-margin cloud' (value-unlocking type), while Alibaba represents 'high-margin e-commerce + low-margin cloud' (value-enhancing type). The 'unveiling' effect of AWS stems from a dramatic contrast in profit margins, whereas Alibaba Cloud needs to trigger a valuation re-rating through margin improvement.

Triggers for valuation re-rating:

Based on AWS experience, Alibaba Cloud's valuation re-rating requires:

1. Cloud profit margin surpassing 20%: currently at 9% → teens → 20%, this is the critical threshold.

2. AI revenue share exceeding 50%: proving AI has become the core driver.

3. MaaS ARR consistently materializing: achieving the path from $800 million to $3 billion as expected.

Timeline assessment:

If the above conditions are met as expected, the main catalysts for valuation re-rating will emerge in FY27-FY28 (around 2027). This represents a 2-3 year investment thesis rather than a short-term trading opportunity.

In my view, Alibaba Cloud is at the beginning of a valuation restructure: its revenue scale has met expectations, but profitability still needs improvement. As the proportion of high-margin MaaS business increases, the profit contribution from the cloud segment will grow rapidly, compelling the market to reassess its valuation.

Risk Warning:

The views expressed in this article represent my personal research and analysis and do not constitute any form of investment advice. The company, industry, and market analyses mentioned in the article are based on publicly available information and reasonable speculation, which may involve delayed information or interpretive bias. Investing carries risks; proceed with caution when entering the market.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

6