NVIDIA is pushing hard on 800V—so who’s selling the shovels in power semiconductor?

Breakthrough in AI Power Consumption! NVIDIA Anchors 800V DC Architecture; Under High Consensus from Morgan Stanley and Citrini, Which Companies Are Worth Investing In?

With the explosive growth of AI computing power, electricity has become the key determinant of success for data centers. A technological race revolving around 'reducing power loss and increasing power density' is now fully underway.

Recently, this silent competition has quietly affected pricing: major domestic and overseas power semiconductor companies have issued price hike notices one after another, with increases generally as high as 10% to 25%. The core driver behind this wave of price hikes is none other than AI data centers with an insatiable demand for energy.

In terms of technological evolution, industry giants and institutions have reached a high consensus. At NVIDIA's 2025 Technology Conference,the 800V High-Voltage Direct Current (HVDC) architecture was officially established as the core power supply solution for the next generation of AI factories.

The latest research report from Citrini Research also points out that the transition of AI data centers to 800V HVDC is an inevitable trend.In this architectural revolution, 'power semiconductors,' which handle power conversion and transmission, are undoubtedly the heart of the entire system.

By now, many fellow investors likely have a question:So, what exactly is the 800V high-voltage direct current (HVDC) architecture? What investment opportunities in the industrial chain, triggered by this AI-led power revolution, are worth paying close attention to?This article will explain each aspect for fellow investors.

1. What is 800V High-Voltage Direct Current (HVDC)? Why do AI data centers urgently need to transform?

Traditional data center racks mainly use a 54V DC power distribution standard. However, with the significant leap in AI computing power, chip power consumption has sharply increased. It is expected that by the next-generation Rubin Ultra system, the power consumption of a single GPU will exceed 2500W. If the low voltage of 54V continues to be used, it will generate massive currents, which would not only require extremely bulky copper wire infrastructure but also lead to substantial heat losses and reduced transmission efficiency.

Therefore,Doubling or even significantly increasing the voltage to 800V is the only way to physically construct 600kW or even 1MW megawatt-level high-density racks.。

Two core advantages of the 800V HVDC architecture:

1. Simplifying conversion stages, improving efficiency:Traditional architectures within data centers undergo multiple cumbersome conversions such as AC-AC (alternating current to alternating current) and AC-DC (alternating current to direct current). The 800V architecture, on the other hand, directly converts AC to 800V DC at the source and performs DC-DC step-down closer to the load terminal, greatly reducing the number of conversion stages and lowering power losses.

2. Significantly reducing copper usage:At the same power level, the higher the voltage, the lower the current,

The smaller the flow, the more this significantly reduces reliance on expensive thick copper wires, simplifying infrastructure.

Notably, in late April,Media reports indicated that NVIDIA has approached major Korean power equipment companies, proposing to design data center infrastructure based on an approximately 800V DC system,Currently, it is privately advancing discussions with Korean companies regarding specific cooperation plans for data centers.

In this power revolution sparked by AI, what are the key investment opportunities worth focusing on?

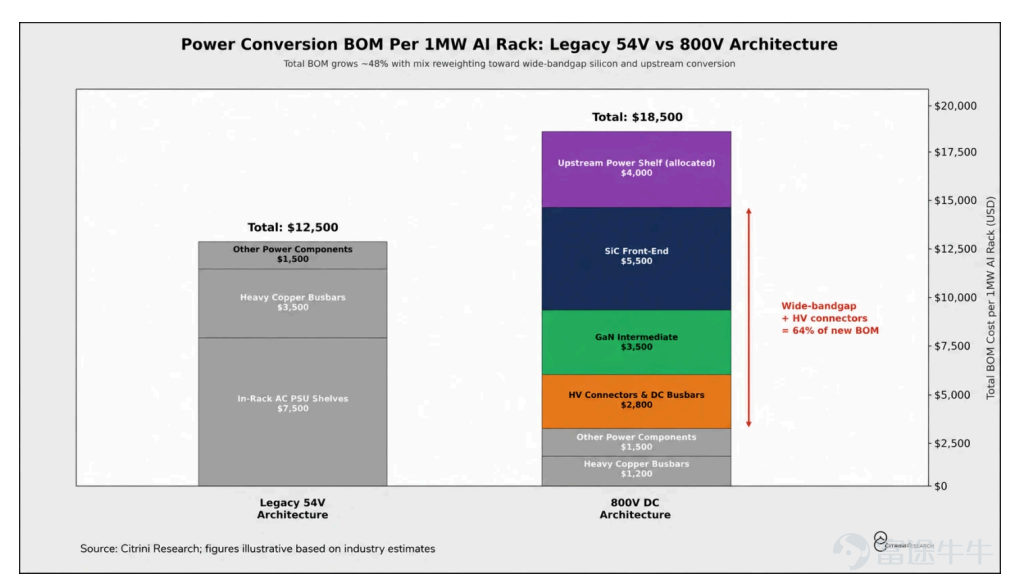

Driven by the 800V architecture, the Bill of Materials (BOM) for rack power supplies is undergoing structural reorganization. The proportion of wide bandgap semiconductors and high-voltage connectors in the power BOM has surged from nearly zero to about 64%.

Based on publicly available data such as Citrini Research, the following areas are expected to become the most direct beneficiaries:

First layer: Wide bandgap semiconductors (SiC/GaN core devices and equipment)

Every step-down conversion from the public power grid to the chip requires wide bandgap materials: the front-end step-down to 800V DC heavily relies on silicon carbide (SiC), while the back-end high-frequency step-down to GPU operating voltage depends on gallium nitride (GaN).

Notably, Citrini Research highlighted in its report a highly compelling investment logic with significant 'expectation differential':Supply chain inheritance。

Over the past few years, the global silicon carbide market has largely been driven by electric vehicles alone. However, with weakening demand for EVs in Europe and strong competition from Chinese production capacity, the industry’s growth rate has quietly hit a bottleneck. Nevertheless,What the market has yet to fully recognize is that AI infrastructure is aggressively taking over.—Citrini estimates that by 2030, AI will consume half of the world’s silicon carbide production capacity. The most fascinating part is that the wafers used in AI data centers and electric vehiclesare exactly the same specifications.。

This creates an extremely asymmetric valuation opportunity: In most institutional pricing models, these SiC leaders are still being labeled as 'auto cycle stocks.' What they fail to realize is that AI has effectively 'inherited' this capacity originally prepared for automakers. This means the more pessimistic the EV market becomes, the greater the potential returns on this trade—as these severely undervalued hardcore assets, shackled by their automotive stock label, are quietly standing on the eve of an AI boom.

Companies worth watching: $INFINEON TECHNOLOG (IFNNY.US)$ are expected to benefit from their extensive SiC/GaN portfolio. $Wolfspeed (WOLF.US)$ is considered one of the top picks by institutions due to owning the world's only commercially operational 200mm SiC wafer fab; $Navitas Semiconductor (NVTS.US)$ is an emerging giant whose GaNFast and GeneSiC products have already been selected for use in 800V HVDC architectures. Others like $STMicroelectronics (STM.US)$ 、 $ON Semiconductor (ON.US)$ 、 $Power Integrations (POWI.US)$ 、 $Axcelis Technologies (ACLS.US)$ 、 $Rohm (6963.JP)$ 、 $Fuji Electric (6504.JP)$ is also worth paying close attention to.

Additionally, in the Hong Kong stock market, $INNOSCIENCE (02577.HK)$、 $SICC (02631.HK)$is equally worth noting.Previously, Innoscience announced on the Hong Kong Stock Exchange that the company provides a full GaN power solution for 800 VDC power architecture, enabling a new generation of AI Factories. NVIDIA will support the 800 VDC power architecture. The 800 VDC rack power architecture brings breakthrough progress to artificial intelligence data centers, achieving higher efficiency and higher power density while reducing energy consumption and carbon dioxide emissions.

On the SICC Advanced side, its market share of conductive silicon carbide substrates reached 27.6% in 2025, surpassing Wolfspeed to become the world's largest. In particular, the company’s market share of 8-inch silicon carbide substrates leads by a wide margin with a 51.3% market share. Huayuan Securities believes that given the company’s ability to mass-produce 8-inch SiC substrates, it is expected to benefit from the recovery of the SiC substrate industry and see increased demand.

The second layer: Power management, gate drivers, and protection (the 'capillaries' near the chip)

This section covers voltage regulation (VRM), gate driving, mixed-signal power supply, and high-current protection. These devices are responsible for high-density, high-precision power conversion and control near the GPU.

Companies worth noting: $Monolithic Power Systems (MPWR.US)$ is an undisputed leader, almost monopolizing the module market next to GPUs that handle extreme currents of 'thousands of amperes.' Providing foundational hardware support for it are the two giants of analog chips, $Texas Instruments (TXN.US)$ And, $Analog Devices (ADI.US)$ who ensure the utmost precision in every voltage conversion.

Moreover, the highly modular AI racks are heavily reliant on $Vicor (VICR.US)$ patented step-down technology, while $Alpha & Omega Semiconductor (AOSL.US)$ 、 $Renesas Electronics (6723.JP)$ and $Microchip Technology (MCHP.US)$ plays its respective role in controllers and drivers.

Third Layer: Busbars, Connectors, and Power Modules (Rack-Level Basic Components)

This stage primarily involves rack-level copper architecture, interconnections, and assembly, encompassing infrastructure provision such as high-current connectors, power harnesses, rack power supplies, and cooling systems.

Companies to Watch: The global leader in server power suppliesDelta Electronics plays a pivotal role here, providing top-tier power supply and cooling systems. Following the power lines, $Amphenol (APH.US)$ And, $TE Connectivity (TEL.US)$ these two giants dominate the high-voltage, high-current connectors used for power distribution; andBizLink、 $Methode Electronics (MEI.US)$ , as well as cable expertPrysmian, are responsible for connecting these nodes with the highest specification harnesses. During implementation, $Flex Ltd (FLEX.US)$ provides a full set of solutions from design to manufacturing, $Shenzhen Megmeet Electrical (002851.SZ)$ steadily manages the power supply system, $nVent Electric (NVT.US)$ while providing these expensive devices with physical protection and liquid cooling 'coats'.

Layer Four: Industrial Power Infrastructure (Macro Grid and Factory Infrastructure)

This stage mainly involves grid edge, switchgear, transformers, and data center electrification, with responsibilities including providing support for high-voltage direct current (HVDC) applications such as UPS, grid equipment, and automation systems.

Companies worth watching: In this sector, $Vertiv Holdings (VRT.US)$ is undoubtedly the purest AI play, with its provision of uninterruptible power supply and thermal management being the lifeline for data centers. At the same time, a group of century-old electrical giants are experiencing a boom — Schneider Electric、 $Eaton (ETN.US)$ 、ABBand $SIEMENS AG (SIEGY.US)$ 、 $GE Vernova (GEV.US)$ 、 $Mitsubishi Electric (6503.JP)$ and $Hitachi (6501.JP)$ . They are responsible for channeling energy from the macro power grid into these mega AI factories in a continuous and stable manner.

Notably, Morgan Stanley recently introduced an 'AI 800V Concept' investment portfolio, as follows:

Morgan Stanley noted that developments in AI data center racks have surpassed today's 480V AC (VAC)/54V DC architecture; next-generation systems like NVDA Rubin Ultra/Kyber require higher voltage designs (including 800V side power cabinets), which will significantly increase the value content of power semiconductors.

They emphasized that due to higher voltage and heat dissipation requirements, wide bandgap semiconductors (SiC/GaN) will be key beneficiaries, and they are optimistic about $INFINEON TECHNOLOG (IFNNY.US)$ a broad portfolio of SiC/GaN/silicon products, as well as $ON Semiconductor (ON.US)$ the growing proportion of SiC business.

Morgan Stanley pointed out that Infineon sees an addressable market opportunity of about $175,000 per kilowatt (kW) currently, with potential for further upside. On the other hand, ON Semiconductor expects the power semiconductor content value per rack to expand from approximately $15,000 for today’s 120kW racks to around $115,000 for future 600kW-1MW systems by 2030.

Summary

All things considered, this revolution in the 800V HVDC architecture ignited by AI data centers is fundamentally a "forced" breakthrough in the face of physical limitations. As the growth of computing power inevitably hits the "energy consumption wall," a comprehensive leap in power infrastructure has become the only solution to support the advancement of the AI era.

This also offers the market a fresh perspective: the红利 of the AI industrial chain is rapidly spreading from单一 computing terminals to the underlying "basic ecosystem." Following the logic of this technological evolution, we can clearly observe a structural reshaping of the rack power material list—from the micro level where wide-bandgap semiconductors (SiC/GaN) and power management chips see soaring value, to the macro level involving a complete upgrade of grid-edge infrastructure and high-voltage components, all quietly absorbing this massive wave of incremental demand.

For fellow investors, stepping outside the单纯的 chip narrative and re-examining the entire hardware supply chain along the highly predictable暗线 of "reducing losses and improving energy efficiency" may help us filter out short-term market noise. With clearer underlying logic, we can identify those truly high-quality stocks with long-term growth potential.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

218

858