SMIC and Hua Hong Semiconductor surge sharply as domestic chips receive multiple tailwinds

Are there risks in chasing high valuations in semiconductor investment opportunities?

Semiconductors are undoubtedly one of the biggest investment highlights of 2026, with AI demand far exceeding market expectations, especially in the US and China.Tech giants continue to increase capital expenditure to enhance computational power deployment,which is the core logic driving the entire semiconductor industry into a 'super cycle'.super cycle' at the core logic.

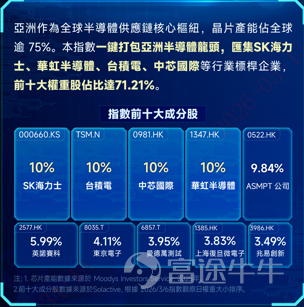

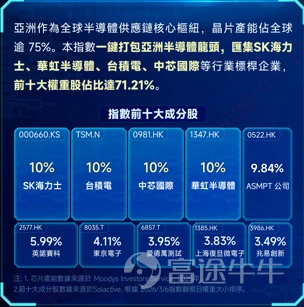

As the core hub of the global semiconductor supply chain, Asia, with over 75% of global chip production capacity, naturally benefits from this 'super cycle' in the semiconductor market.Solactive Asia Semiconductor Select Indexpacks leading Asian semiconductor companies, gatheringSK Hynix、 $HUA HONG SEMI (01347.HK)$ 、 $Taiwan Semiconductor (TSM.US)$ 、 $SMIC (00981.HK)$ Industry leaders such as.

**The index has achieved a cumulative return of up to 550% since its base date of March 20, 2020. It has also risen by over 53% year-to-date in 2026 and surged more than 80% in 2025.

*Chip production capacity data sourced from Moody's Investor Service, 2025.

**Data source: Bloomberg, data as of May 7, 2026. The above is an objective display of the historical performance of the benchmark index. Past performance of the index does not predict future fund returns, and should not be considered as investment advice. Investors are advised to be aware of the risks associated with index volatility. Actual fund returns will be affected by management fees and tracking errors, and may differ from index performance. Investors are advised to take note.

Investment Logic in the Semiconductor Sector

With the growing popularity of AI applications, the public is no longer unfamiliar with various large language models (LLMs), such as OpenAI's ChatGPT,$Alphabet-C (GOOG.US)$Gemini, xAI's Grok, Anthropic's Claude,$BABA-W (09988.HK)$Qwen,$TENCENT (00700.HK)$the ingots, as well as$BIDU-SW (09888.HK)$such as Wenxin Yiyan.

This year, AI has experienced explosive growth, mainly due to the rapid rise of AI Agents. For instance, OpenClaw, which became highly popular at the beginning of the year, heavily utilized the computational power of the Claude model. Meanwhile, in the Chinese market, there was a 'lobster farming' craze, leading to a shortage of computing power. Tech giants significantly increased their capital expenditures in the latest quarterly earnings reports. In April 2026, Anthropic adjusted its API policy to a pay-per-use model, further intensifying the demand for computing power. The explosive growth of AI Agents is driving companies to invest more in computing power, becoming the core driver of the semiconductor industry entering a super cycle.

In recent years, the market has increasingly focused on AI applications in two major areas: memory and CPUs. Over the past two years, these two types of products have received far less attention than logic chips in the AI sector, with relatively weaker demand. However, as large AI models mature, their operational mode gradually shifts from 'training' to 'inference,' significantly boosting the demand for memory and CPUs, with memory seeing particularly notable growth.

The current supply shortage of HBM (High Bandwidth Memory) is the most severe,$Micron Technology (MU.US)$with the latest production capacities of major manufacturers like Hynix and Samsung already booked until 2027. This phenomenon brings about two major chain effects:

1. The new generation HBM4 adopts advanced processes (such as Samsung's 4nm and Hynix's 3nm), driving a sharp increase in demand for advanced logic processes, prompting major wafer fabs to accelerate capacity expansion. Consequently, the demand for advanced semiconductor equipment improves significantly, resulting in a notable enhancement in profitability.

2. The severe shortage of HBM has led memory manufacturers to shift wafer capacity toward high-margin HBM, reducing the supply of traditional and mid-range memory (e.g., DDR, NAND). At the same time, the continuous expansion of AI data centers stimulates overall memory demand, creating a situation where both price and volume are rising. This drives the entire memory industry into a super cycle and significantly boosts demand for semiconductor equipment.

Latest catalyst:

On May 6, 2026,Anthropic CEO Dario Amodei and his sister, co-founder Daniela Amodei, at the "Code with Claude 2026" developer conference revealed that the company’s Q1 2026 revenue andusage recorded an annualized 80x growth,,far exceeding the originally anticipated 10x growth,mainly driven by the explosive popularity of Claude Code. During the discussion, they also mentioned that they are no longer designing products solely for the current model capabilities but will aim for models six to eighteen months ahead, which is expected to lead to massive demand for AI infrastructure in the short term.

This explosive demand has caused a significant lag in the expansion speed of AI infrastructure, ensuring strong near-term demand for computing power and related infrastructure, making the investment outlook for the semiconductor supply chain (including HBM, advanced processes, equipment, etc.) clearer and more certain.

In the semiconductor investment boom, not only are chip manufacturers expected to achieve substantial profits, but semiconductor equipment manufacturers are also likely to benefit in tandem this year. Investors can capture $EFund A SEMICON ETF (03486.HK)$ , a one-stop solution to seize the growth opportunities of leading semiconductor producers and equipment makers in Asia.

(As of May 7, 2026, Hynix and Samsung’s stock prices have surged by approximately 154% and 127% year-to-date, respectively, while semiconductor equipment stocks $ASMPT (00522.HK)$ have risen 129% year-to-date.)

In terms of risks, investors can evaluate from a valuation perspective and appreciate the importance of diversification through ETFs. Even though individual stocks within an ETF may have seen large gains, it doesn't necessarily imply bubble risk. For instance, Hynix's stock price has surged about 154% year-to-date as of May 7, 2026, but according to Bloomberg data, its forecasted P/E ratios for 2026 and 2027 are just around 6.1x and 4.5x,indicating that valuations remain reasonable amid rapid growth, mainly driven by the super cycle in memory products, with HBM orders locked in until 2027, providing clear visibility on profitability.

Another example is $HUA HONG SEMI (01347.HK)$ , which has a TTM P/E ratio as high as 574x. However, supported by national policy and technological upgrades, the company's gross margin and capacity utilization rate continue to improve, resulting in explosive profit growth. In In the first quarter of 2026, the company's quarterly profit increased by 460% year-over-year.If measured by the PEG (Price/Earnings to Growth) ratio, its valuation has become reasonable.

(Data source: Bloomberg, Huahong Semiconductor 1347.HK as of the closing price on May 7, 2026)

In fact, different semiconductor companies and equipment manufacturers have varying investment rationales and circumstances. Individual stock risks, including financing for capacity expansion, must not be overlooked. Diversifying investments through ETFs can effectively reduce single-company risk.

Important Information

The E Fund (Hong Kong) Solactive Asia Semiconductor Select Index ETF (the "Sub-fund") is a sub-fund under the E Fund ETF Trust. The E Fund ETF Trust is an umbrella unit trust established under Hong Kong law. The Sub-fund is categorized as a passively managed ETF under Chapter 8.6 of the Code on Unit Trusts and Mutual Funds issued by the Securities and Futures Commission ("SFC"). Units of the Sub-fund ("Units") are traded on the Hong Kong Stock Exchange ("HKEX") like stocks. The investment objective is to provide investment returns that closely track the performance of the Solactive Asia Semiconductor Select Index ("Index") (before deduction of fees and expenses).

As the Sub-fund’s investments are concentrated in securities of companies primarily engaged in specific sectors within the Hong Kong and East Asian semiconductor industries, it may be particularly affected by certain factors, thus exposing the Sub-fund to industry and geographic concentration risks. Therefore, its net asset value may be more volatile compared to broadly diversified funds.

The issuer of this content is E Fund Asset Management (Hong Kong) Co., Ltd. This content is for reference only and does not constitute an invitation or recommendation to invest in fund units. This content is for display purposes only and should not be shown to any person for whom such display would be illegal. Investment involves risks, and you may lose a significant portion of your principal. Before investing, investors should carefully read the fund prospectus (including the "Risk Factors" section) to understand the investment risks associated with the fund. This content has not been reviewed by the SFC.

For more detailed important notices and disclaimers regarding the above fund, please visit the E Fund HK website at https://www.efunds.com.hk/tc/products/53/important/

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

9

3