AI Boom vs. Tight Liquidity: Will the US Stock Rally Continue?

Options Sir Macro View | CPI Release Looms: After a Sharp Rebound, the Market Still Needs an 'Inflation Answer'

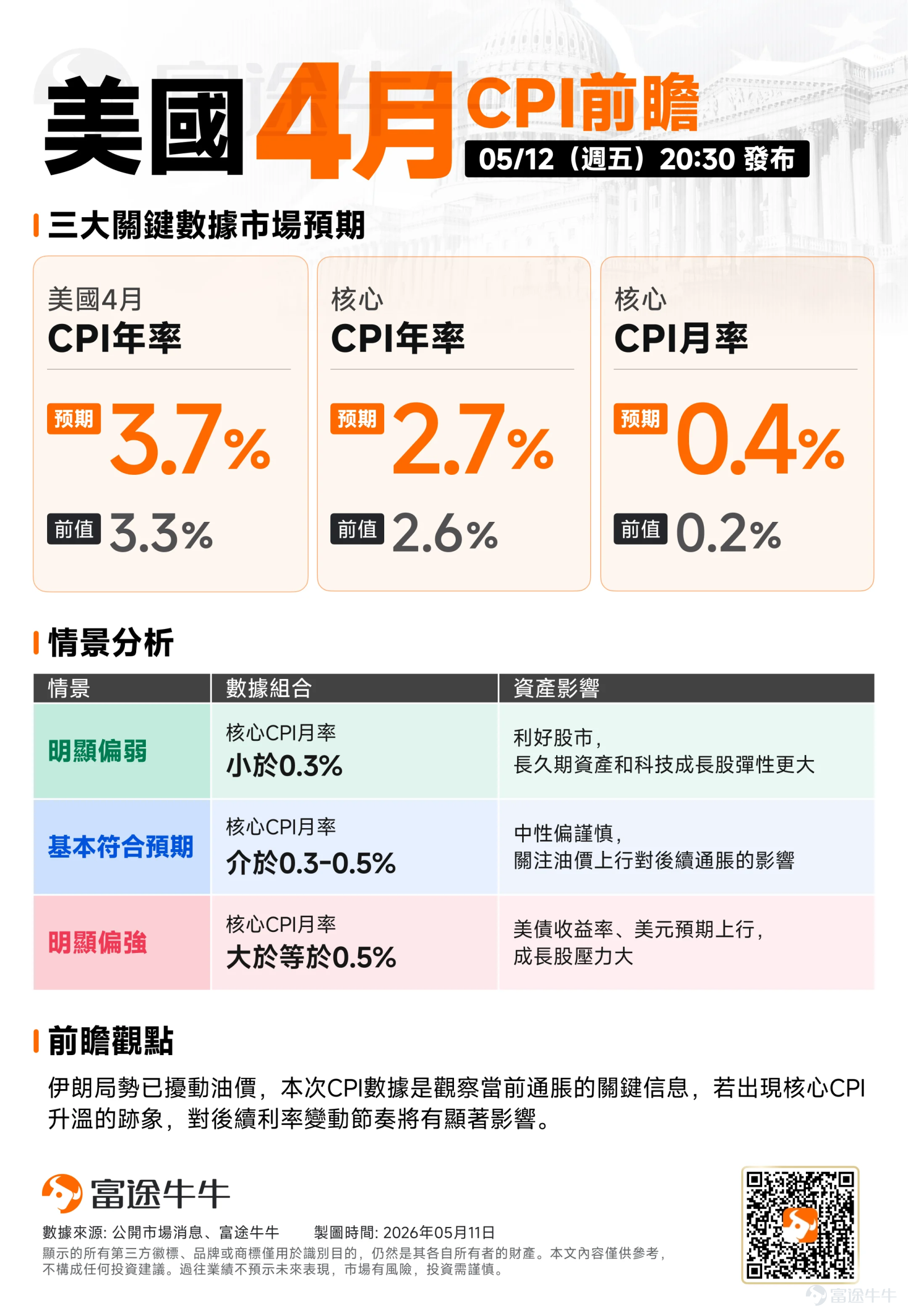

The US April CPI will be released at 8:30 PM tonight. Market expectations for this CPI release are not low, with the mainstream view being that 'overall inflation is showing a clear uptick, while core inflation is rising moderately.' Specifically, the consensus forecast expects the overall US CPI to rise by 0.6% month-over-month in April, with the annual growth rate potentially climbing to 3.7%; core CPI is expected to increase by 0.4% month-over-month, with the annual rate rising to 2.7%.

Currently, US stocks have rebounded to higher levels, with AI, semiconductors, and large-cap tech stocks still providing core support. However, the higher the market climbs, the more it needs macro data to support it. The upcoming CPI release will affect the market, but what truly matters isn't just a single data point—it's whether inflationary pressures spread, whether interest rates start to rise again, and whether the strongest technology-driven narrative can continue to justify valuations through earnings.

The key lies in whether inflation spreads again.

This time, the overall CPI is expected to be relatively high, and the market is mentally prepared. Gasoline prices may be one of the main contributors to the increase in this month’s CPI, and food prices may also rebound from an unusually stable March, both of which will push up headline CPI.

What truly impacts asset prices is core CPI. If core CPI comes in around 0.3%, the market may see inflation as sticky but not out of control for now. If core CPI approaches 0.4%, concerns over spreading service-sector inflation will resurface. If it hits 0.5%, it would significantly reinforce the trading narrative of 'higher rates for longer,' which would be unfriendly for the Nasdaq, semiconductors, AI software, and high-valuation growth stocks.

Goldman Sachs' interest rate team has postponed expectations for the Federal Reserve's next 25-basis-point rate cut to December, with the subsequent adjustment anticipated in March next year. This means that the current rally in U.S. stocks can no longer be simply based on the premise of 'an imminent rate cut,' but must rely more on the realization of corporate earnings.

First scenario: CPI is slightly higher, but structurally manageable.If the overall higher CPI mainly stems from disruptions in energy and housing, without spreading into core services, U.S. stocks are likely to remain strong. Semiconductors and memory may continue to be the main focus for capital, but gains will be more concentrated in leading companies with the clearest upward revisions in earnings.

Second scenario: CPI comes in lower than expected.This is the most favorable combination for tech stocks. If U.S. Treasury yields fall simultaneously, sectors like AI, semiconductors, cloud computing, and memory could continue to benefit. However, considering the significant short-term rise in semiconductors, the strategy would be better suited to holding dominant leaders or waiting for intraday pullbacks rather than chasing second- and third-tier stocks with already excessive short-term gains.

Third scenario: Core CPI significantly exceeds expectations.This is the risk the market needs to guard against most right now. If interest rates rise again, high-valuation tech stocks and crowded trades will come under pressure first. Semiconductors won't be completely immune to interest rate impacts just because of strong earnings—especially in areas with large gains like memory, CPUs, and thematic AI chains, where rapid pullbacks may occur.

What do major institutions think: Is there still room for storage? Are semiconductors currently in a bubble?

The aspect of the current semiconductor rally that invites the most controversy is the magnitude of the gains. $PHLX Semiconductor Index (.SOX.US)$ Having risen approximately 66% year-to-date, it has clearly outperformed. $S&P 500 Index (.SPX.US)$ and $Nasdaq Composite Index (.IXIC.US)$ The trend over the past few weeks has been closer to a vertical climb. Based solely on price, it's easy to conclude that the market is 'overheated'.

However, this semiconductor rally differs from a typical bubble. Bernstein's core view is that the current rise in the semiconductor sector is mainly driven by upward revisions in earnings, rather than purely by an expansion in valuation multiples. The SOX index currently trades at about 28 times forward earnings, which is not cheap but still below historical peaks. More importantly, the forward earnings per share (EPS) of SOX have risen approximately 69% since the beginning of the year, while the sector’s forward price-to-earnings ratio has slightly declined by about 2%. This indicates that there is real earnings support behind the index's rise.

Bernstein believes that the entire semiconductor sector cannot be simply defined as a bubble because the upward revision in earnings is genuine, and valuation multiples have not completely spiraled out of control. Valuation expansion has been more pronounced for CPUs and analog chips this year, whereas the growth in valuations for GPUs/ASICs and semiconductor equipment has been relatively moderate, potentially leaving room for catch-up gains.

Looking at the details, the memory sector is more representative. The average stock price increase for memory stocks this year is approximately 264%, but the upward revision in forward earnings expectations reached about 386%, with the corresponding valuation multiple actually declining by about 21%. This means that although the short-term surge in memory stocks is impressive, it is not purely driven by sentiment. What the market is truly concerned about is not whether the current valuation is expensive, but whether this round of earnings growth can be sustained.

Therefore, whether there is still room for memory stocks depends on a more nuanced analysis.There is still room for memory stocks driven by earnings, but as the rally enters its latter stages, trading congestion has significantly increased. Stock selection and timing are now more important than just direction.

The potential for memory stocks comes from three main factors. First, AI servers and HBM continue to squeeze traditional DRAM capacity, keeping prices strong for both standard DRAM and server memory. Second, cloud providers' capital expenditures are still expanding. Bank of America expects the combined capital expenditures of Amazon, Microsoft, Alphabet, Meta, and Oracle—the five major tech companies—to grow by more than 60% year-over-year by 2026, reaching approximately $600 billion, and possibly exceeding $750 billion by 2027. Third, leading memory companies still appear undervalued; even after the stock price increase, the speed of earnings revisions has not lagged significantly.

However, short-term risks are also increasing. Although spot prices remain far above normal levels, they have shown a slight decline over the quarter. This indicates that the memory market has entered a phase where high prosperity coexists with high volatility. If price increases slow down or the market begins to worry about supply expansion post-2027, stock prices will adjust ahead of fundamentals.

Options Strategy

AI and semiconductor earnings remain the most critical support for US stocks, and no clear reversal in the memory cycle has been observed yet. CPI will determine short-term interest rate pressures, interest rates will dictate the volatility range of high-valuation assets, and semiconductor earnings will decide whether this rally has fundamental support.

At present, semiconductors cannot be simply categorized as a bubble, and the logic for memory stocks has not yet come to an end. However, from a trading perspective, the easiest stage of widespread gains has passed. Going forward, the focus will be on whose earnings can continue to improve and whose valuations have already been priced in advance.

1. If core CPI is lower than expected, investors are optimistic about a sustained rebound.

If the data release shows that only energy pushed up the overall CPI but core inflation remains relatively controlled, growth stocks may not face sustained pressure, especially if the broader US equity market continues to stabilize. For investors who are either not fully invested, lightly positioned, or wish to participate in the tech stock rally following a favorable CPI report, they can consider implementing a Bull Call Spread strategy. After the data release, implied volatility (IV) will likely decline, and simply buying Calls could lead to a situation where the direction of the trade is correct but the premium doesn't increase. Using spreads can reduce costs and focus potential gains within the range of continued index recovery. For example: $Intel (INTC.US)$ For example:

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

2. If core CPI is significantly higher than expected, investors worry about a pullback from high positions.

If the data is significantly higher than expected, particularly with core CPI also surpassing market expectations, alongside an increase in the 10-year Treasury yield, a stronger dollar, and weakening Nasdaq futures, the market's trading logic might shift towards 'delayed rate cuts or even more hawkish pricing.' In this scenario, growth stocks and highly valued tech stocks would come under pressure.

For investors holding significant tech stock positions and concerned about further pullbacks after the CPI release, if they prefer not to sell the underlying shares, they can buy protective Puts for 1-2 weeks. If they want to reduce the cost of protection, they can sell out-of-the-money Calls to offset the Put costs, forming a Collar structure. The advantage of this approach is twofold: first, using Puts provides downside protection; second, selling Calls recovers some premium, lowering hedging costs. The trade-off is sacrificing some upside potential, which aligns with the objectives of defensive clients. However, caution should be exercised if the market opens sharply lower beyond what the data itself can explain, while the 10-year Treasury yield does not continue rising. In such cases, purchasing Puts late could result in losses due to a potential reversal. Taking INTC as an example:

(The figure below illustrates the simulated profit and loss scenario of this strategy on the expiration date. The design image displayed on the screen is for demonstration purposes only and does not constitute any investment advice or guarantee; market conditions fluctuate frequently, and the prices shown do not represent actual values.)

Finally, Option Sir brings a small perk for fellow investors, welcome to claim it.Options Beginner Pack

*This event is exclusive to invited HK users. Click to learn more.Detailed event rules>>

Market conditions are complex and volatile,Options StrategyOverwhelmed by choices? Futubull helps you build a portfolio in three steps.Options Strategymaking investing simple and efficient!

Option Risk Warning:An option is a contract that grants the holder the right, but not the obligation, to buy or sell an asset at a fixed price on a specific date or at any time before that date. The price of an option is influenced by various factors, including the current price of the underlying asset, the strike price, time to expiration, and implied volatility. Implied volatility reflects the market’s expectations for the level of volatility in the option over a future period. It is a data point derived inversely from the Black-Scholes option pricing model and is generally regarded as an indicator of market sentiment. When investors anticipate greater volatility, they may be more willing to pay a higher price for options to hedge risks, resulting in higher implied volatility. Traders and investors use implied volatility to assess the attractiveness of option prices, identify potential mispricings, and manage risk exposure.

Disclaimer:This content does not constitute any offer, solicitation, recommendation, opinion, or guarantee of any securities, financial products, or tools. The risk of loss in trading options can be substantial. In some cases, losses may exceed the initial margin deposited. Even if you set contingent orders such as 'stop-loss' or 'limit' orders, these may not prevent losses. Market conditions may make such orders unexecutable. You may be required to deposit additional margin within a short period. If you fail to provide the required amount within the specified time, your open positions may be liquidated. However, you will still be responsible for any shortfall in your account. Therefore, before trading, you should study and understand options and carefully consider whether such trading is suitable for you based on your financial situation and investment objectives. If you trade options, you should be familiar with the procedures for exercising options and the rights and obligations upon exercise and expiration. Options trading carries extremely high risks and is not suitable for all investors. Investors should carefully readCharacteristics and Risks of Standardized Options。

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (7)

to post a comment

16

25