Has the rebound opportunity arrived? Hong Kong stocks welcome a strong start in May

Global Weekly Review | Fed policy divergence hits multi-decade high, while Q1 profits of China's industrial firms accelerate

United States: Fed policy divergence hits multi-decade high; rising inflation and manufacturing sector divergence make policy path increasingly unclear

The core macroeconomic situation in the US shows an intensification of policy divergence, a bifurcation in inflation structure, and pressure on manufacturing expansion. The focus is on three key dimensions: Fed policy, inflation, and manufacturing.Regarding the Federal Reserve, the Senate Banking Committee voted to approve Wash's nomination as Fed Chair (with clear partisan divisions). On the same day, the Fed released its April interest rate decision.For the third time this year, the Fed kept rates unchanged. However, the 8-to-4 voting result marked the highest number of dissenting votes since 1992, highlighting growing internal hawk-dove divisions. Powell announced that he plans to remain as a Fed governor after his term ends.On the inflation front, the March PCE price index rose 3.5% year-over-year and 0.7% month-over-month, both representing the largest increases since 2022, primarily driven by a surge in energy prices. Meanwhile, core PCE showed moderate growth, indicating that inflation exhibits energy-led structural characteristics.Strong performance in consumption and income supported economic resilience, but high energy costs may pose downside risks to future consumption. In terms of manufacturing, the ISM Manufacturing PMI for April remained at an expansion level of 52.7. However, the input price index hit a four-year high, while the employment index fell to a four-month low. Coupled with supply chain disruptions due to Middle East conflicts, manufacturing expansion faces dual constraints from cost pressures and labor shortages.

China: Industrial enterprises' profit growth accelerated in Q1, and the April PMI continued to expand, maintaining overall economic stability.

Last week’s core macroeconomic focus in China was on industrial enterprise profits and PMI data, reflecting the resilience of economic recovery. Regarding industrial enterprises’ profits, total profits of large-scale industrial enterprises grew by 15.5% year-over-year in Q1.In March alone, there was a 15.8% increase, with growth continuing to accelerate. High-tech manufacturing, equipment manufacturing, and raw material manufacturing performed exceptionally well.Industries related to artificial intelligence and semiconductors played a significant driving role. Unit costs for industrial enterprises decreased, profitability continuously improved, and profits across enterprises of different ownership structures all grew. Regarding the PMI, the manufacturing PMI in April stood at 50.3%, remaining in the expansion zone for two consecutive months. Although it slightly declined by 0.1 percentage points compared to last month, production and demand continued to expand, with large, medium, and small enterprises all entering the expansion range.High-tech and equipment manufacturing maintained strong momentum, and business market expectations strengthened.The non-manufacturing business activity index stood at 49.4%, showing some decline, but the composite PMI output index was 50.1%, still above the critical point, indicating that overall enterprise production and operation activities in the country remain in an expansionary state.

In terms of the equity market

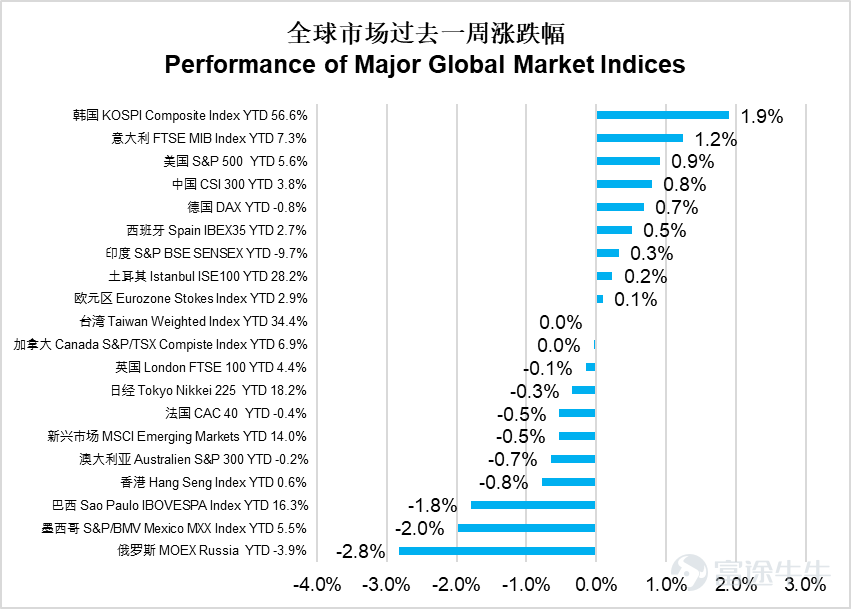

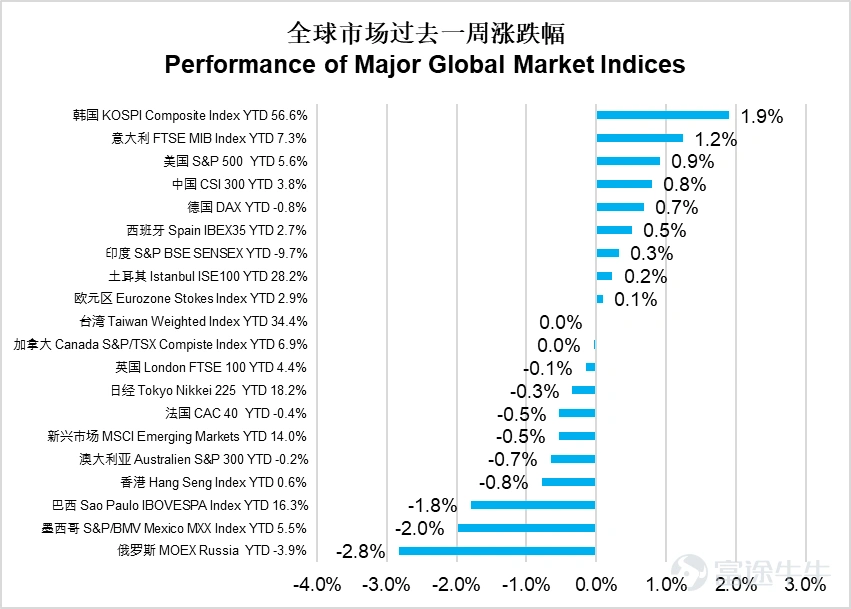

Last week, global markets showed divergent performances, with the KOSPI rising 1.9% to lead, followed by Italy's FTSE MIB with a 1.2% increase.The S&P 500 rose by 0.9%. Emerging markets fell by 0.5% overall, with the Hang Seng Index down 0.8%. Russia's MOEX dropped 2.8%, marking the worst performance; Mexico's MXX fell 2.0%, and Brazil's IBOVESPA declined by 1.8%.Overall, European and US markets saw slight gains, while Latin America and Russia faced significant pressure.

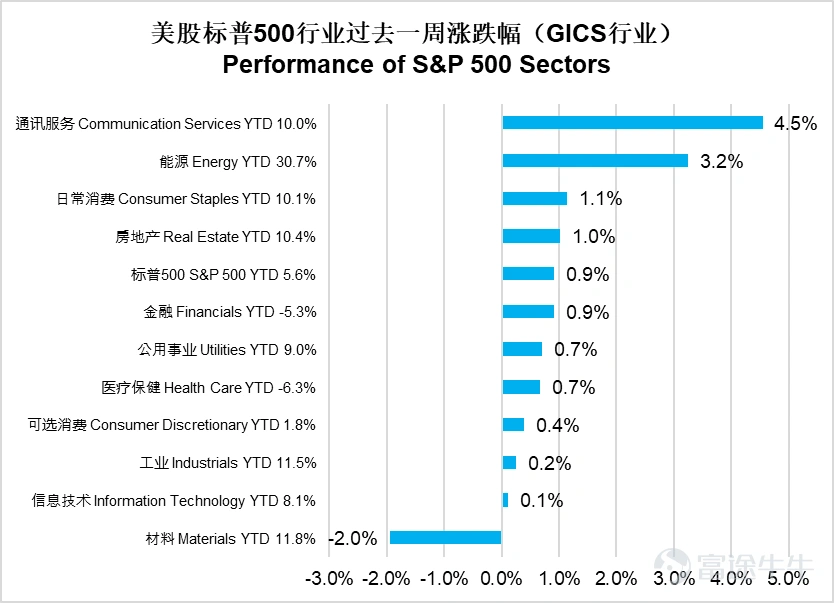

The US communication services sector surged 4.5%, leading all sectors, with energy up 3.2%, and consumer staples increasing by 1.1%.Real estate rose 1.0%, financials were up 0.9%, utilities and healthcare both gained 0.7%, consumer discretionary increased by 0.4%, and industrials edged up 0.2%. Information technology inched up 0.1%. However, materials fell 2.0%, becoming the only declining sector.The market exhibited a pattern of strong leadership from communications and energy sectors, with materials as the sole decliner.

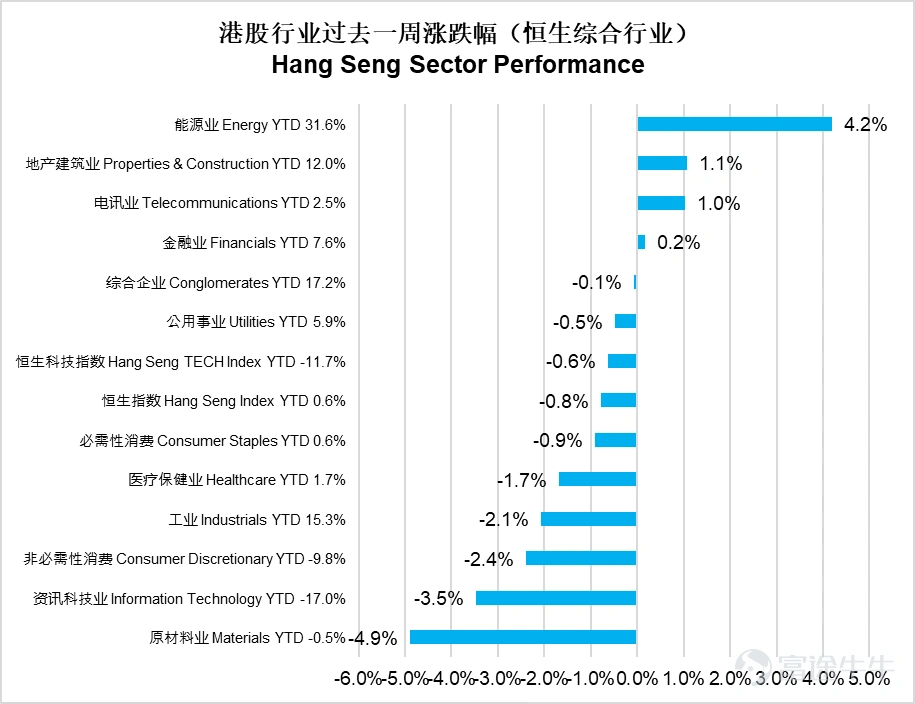

In Hong Kong stocks, the energy sector performed best with a 4.2% rise, real estate and construction climbed 1.1%, and telecommunications advanced 1.0%.Finance edged up 0.2%. However, raw materials plummeted 4.9%, information technology dropped 3.5%, and non-essential consumption fell 2.4%. Industrials declined 2.1%, healthcare dipped 1.7%, and essential consumption slipped 0.9%. The Hang Seng Tech Index fell 0.6%, utilities dropped 0.5%, and conglomerates slightly declined 0.1%.The market showed extreme divergence, led by energy and real estate on the upside, while raw materials and technology lagged significantly on the downside.

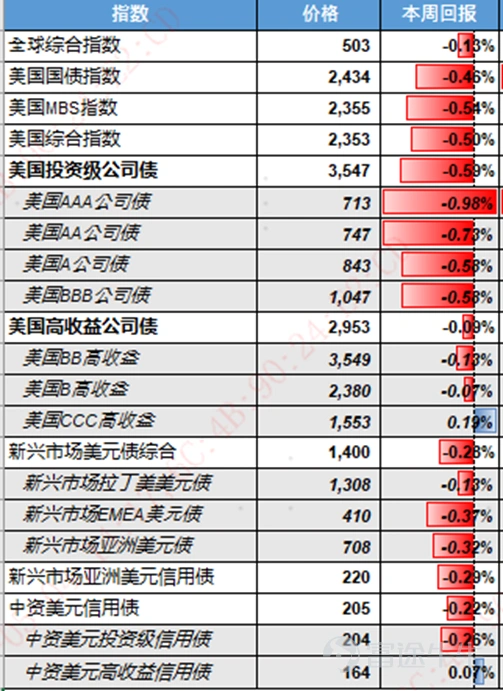

In the bond market,

The global bond market continued to decline over the past week, with the global aggregate index falling by 0.13%, and the US aggregate index dropping by 0.50%.US investment-grade corporate bonds fell by 0.59%, while US high-yield corporate bonds dropped by 0.09%. The emerging market USD bond composite index fell by 0.28%, and the Chinese USD credit bond index declined by 0.22%.

In terms of interest rates, US Treasury yields rose overall,The 2-year US Treasury yield rose by 9 basis points to 3.87%, and the 10-year US Treasury yield increased by 7 basis points to 4.37%.

Market outlook

– Large cloud vendors continue to revise upward their capital expenditure forecasts for 2026, with the computing power supply chain remaining the market's focal point.

This week's market focus was on the Q1 earnings reports of US stocks and the performance of several large technology companies. Overall, US companies were not significantly affected by the surge in oil prices triggered by the US-Iran conflict that began in March.Among the nearly two-thirds of companies in the S&P 500 that have reported so far, approximately 84% have exceeded earnings expectations, surpassing the historical averages over the past five and ten years.Moreover, the extent to which companies have exceeded earnings expectations is far greater than the average over the past five and ten years. This outperformance has been primarily driven by the strong results from three major tech firms: Google, Amazon, and META.The market had closely watched whether large cloud providers would revise their AI-related capital expenditure budgets for 2026 during this earnings season, and all have seen some upward revisions.Previously, the market expected large cloud vendors to allocate about $670 billion in capital expenditures for 2026, but after this earnings season, it was revised upward by $80 billion to approximately $750 billion. Judging by the post-results reaction, it has been a case of 'some winners and some losers': although both revised their capital expenditure plans upward, Google and Amazon’s cloud businesses showed signs of significant acceleration, prompting a very positive market response.However, Microsoft faced a relatively slower growth in its cloud business compared to the other two companies and encountered short-term computational bottlenecks. META's advertising business also saw slower returns on substantial infrastructure investments.The market responded negatively. For the upstream of the entire AI industry chain, this earnings season has alleviated earlier concerns about potential peaks in capital expenditures. The computational power supply chain will remain the market’s focus.

In addition, as mentioned in last week’s review, the US-Iran conflict has shifted from 'armed warfare' towards 'economic warfare.' With the Strait of Hormuz still under effective blockade,the second round of US-Iran negotiations has been indefinitely postponed, and oil prices rose further this week, reaching new highs since the start of the conflict. Although global markets have not broadly declined in response to higher oil prices, investors have begun pricing in expectations that the European Central Bank may soon raise interest rates due to inflation triggered by high oil prices.Currently, the market expects the Federal Reserve to raise interest rates zero to one time this year.If oil prices rise further due to the closure of the strait, this expectation for rate hikes is expected to increase further. At that point, elevated inflation expectations combined with rising rate hike forecasts will create significant headwinds for risk assets.

Key economic data and events this week

On Monday, the US will release March durable goods orders.

On Tuesday, the US will announce the April ISM Non-Manufacturing Index.

On Friday, the US will publish April's non-farm payroll data.

Disclaimer:The issuer of this report is E Fund Asset Management (Hong Kong) Co., Ltd. This report does not constitute an invitation or recommendation to invest in fund units. Fund unit subscriptions should only be made using application forms accompanied by the fund prospectus. Investment involves risks; fund prices may go up or down, and past performance is not indicative of future results. Before investing, investors should carefully read the fund prospectus (including the 'Risk Factors' section) to understand the investment risks associated with the fund.

This report may only be distributed within certain jurisdictions. In any jurisdiction where distributing such information or making any invitation or recommendation is illegal, or if distributing this report or making an invitation or recommendation to anyone constitutes a violation, this report does not constitute such distribution or invitation or recommendation. This document is exempt from prior review and approval by the Hong Kong Securities and Futures Commission and has not been reviewed by them.

Recognition by the CSRC does not constitute a recommendation or endorsement of the plan, nor is it a guarantee of the plan's commercial merits or performance. It also does not represent that the plan is suitable for all investors or an endorsement that the plan is appropriate for any individual investor or any category of investors.

All rights reserved © 2012 - 2026. E Fund Management (Hong Kong) Co., Ltd.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1