Reddit: Fully enjoying the dividends of accelerating commercialization

(This article was authored by Dolphin Research, and published by Titanium Media with authorization)

By Dolphin Research

Reddit's Q1 earnings report showed solid performance. On one hand, as one of the important data sources for AI, Reddit, known for its strong user engagement, is benefiting from traffic directed by major platforms like Google. On the other hand, Reddit is still in the early stages of commercialization and is advancing monetization efforts beyond brand advertising to include performance-based ads.

The shift from 'users searching for content' via Search to 'content finding users' via Feed will become a new growth driver for the company moving forward.This includes the fact that the platform’s ad load rate remains relatively low compared to industry peers, meaning there will likely be a period of strong earnings growth ahead. However, profit margins may rise more slowly due to increased investments in functionality development.

Before the earnings report, according to a Cleveland survey, the market indicated that 'due to macroeconomic volatility, merchants have cut brand advertising budgets since the end of March and shifted towards high ROI platforms.' This led to some adjustments in growth expectations for Reddit, resulting in continuous pressure on the stock price and a partial correction in its high valuation. Therefore, a stable quarterly report showing no slowdown in growth could effectively ease market concerns.

However, the earnings report is not without flaws. One issue is the persistently slow growth of U.S. users, and another is that the implied revenue growth guidance for Q2 would decline from 69% in Q1 to 45%, which may indirectly confirm the information reflected in the above industry research.However, management has always been conservative with guidance, and in the second quarter, the automated ad delivery toolReddit Max is expected to fully launch (released for beta testing in January, currently being used by thousands of advertisers), which could help drive Reddit to continue growing beyond guidance.

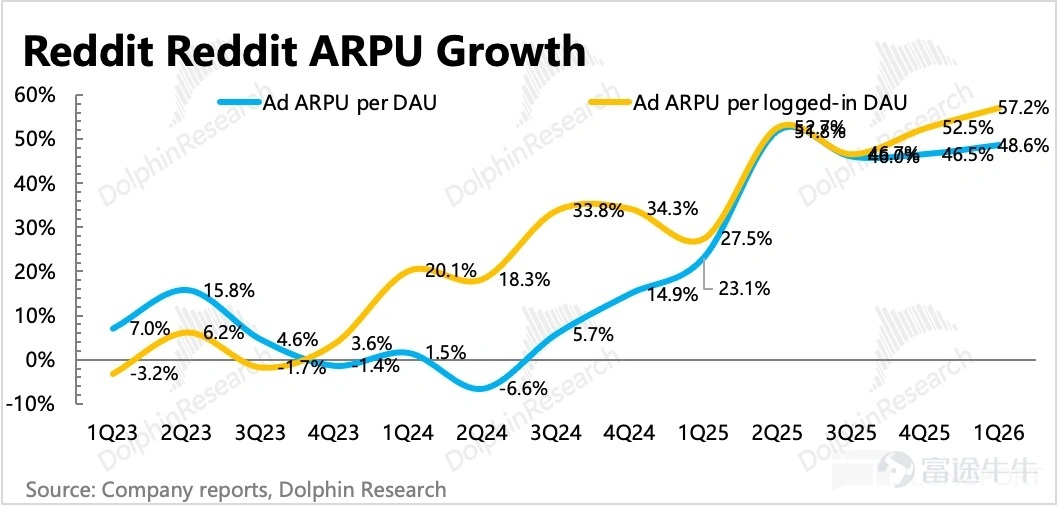

This year, starting Q3, logged-in and non-logged-in user data will no longer be separately disclosed because management believes that 'although logged-in users definitely view more ads due to longer session durations, there isn’t much difference between logged-in and non-logged-in users from a monetization perspective.'

However, Dolphin Intelligence believes that there is still a significant distinction between logged-in and non-logged-in users.Management’s belief that commercialization is similar likely stems from the early days when brand advertising was the primary ad format. However, as more performance-based ads are introduced, the personalized data and user profiles retained by logged-in users are richer compared to non-logged-in users, which facilitates better-targeted distribution of performance ads, improving conversion rates and commercial value.Thus, the subsequent growth performance of U.S. users (tracked via high-frequency app data) will also influence investor confidence and sentiment regarding Reddit's growth prospects.

In terms of valuation, before the earnings report, the market cap of $28.1 billion was basically flat compared to the previous quarter's earnings report, meaning no increase over the past two months. The main reasons are: 1) dissatisfaction with the lack of disclosure of logged-in vs. non-logged-in user data; and 2) recent negative news about industry competition and market share declines, collectively weighing on stock performance.

Based on our adjusted expectations, yesterday's market cap of 28.1 billion corresponds to a 2026 earnings multiple of 33x GAAP P/E and 21x Non-GAAP P/E, which still looks reasonable given the projected CAGR of around 40% in profit growth over the next three years.With a 13% increase pre-market, there is theoretically still room for further upside.(If calculated based on a 40x P/E corresponding to the growth rate, there would still be a 10% upside).The potential short-term risk primarily lies in a continued deterioration of the macro environment.In such a scenario, advertisers would not only tighten their budgets but also prefer platforms with more stable ROI.

Below are the detailed charts:

1. User metrics: Growth remains sluggish in the U.S. region.

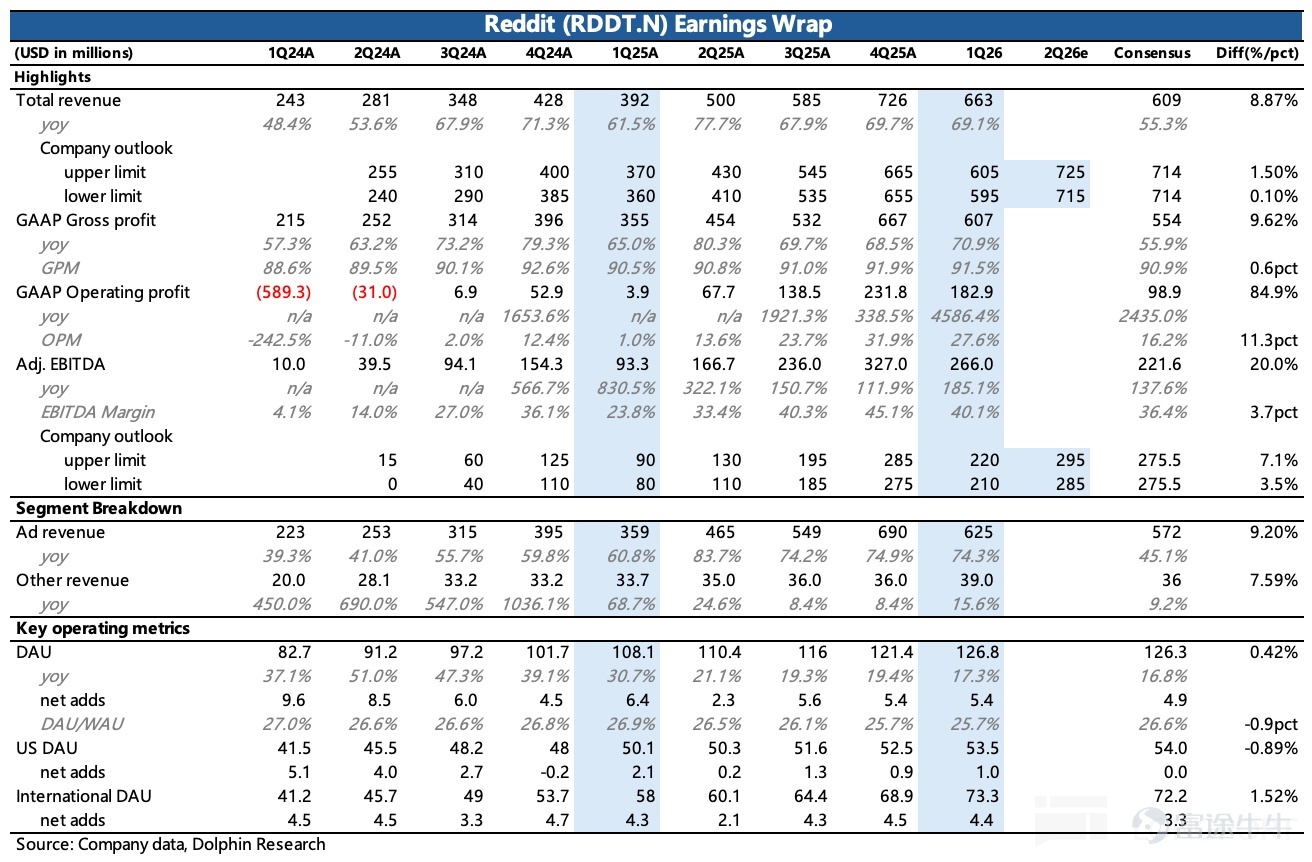

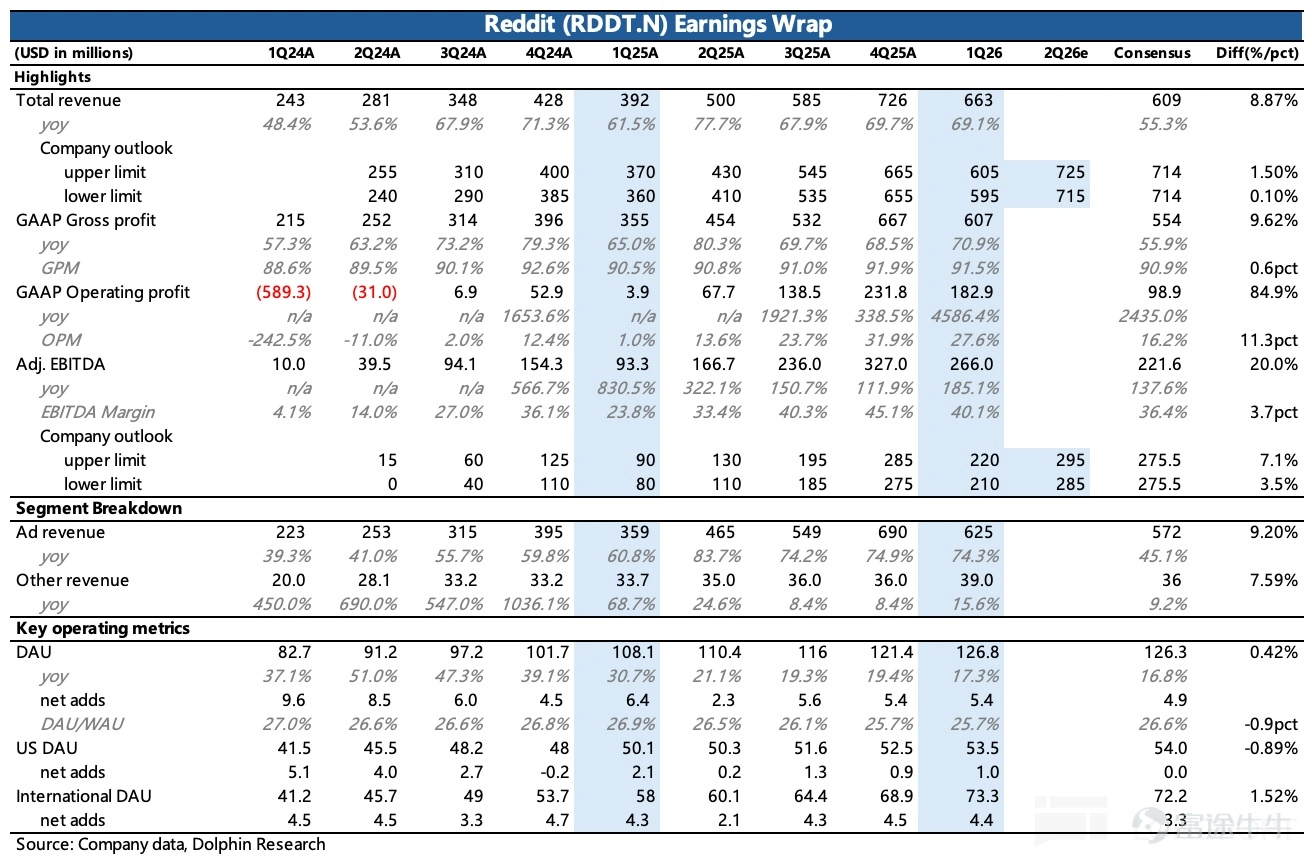

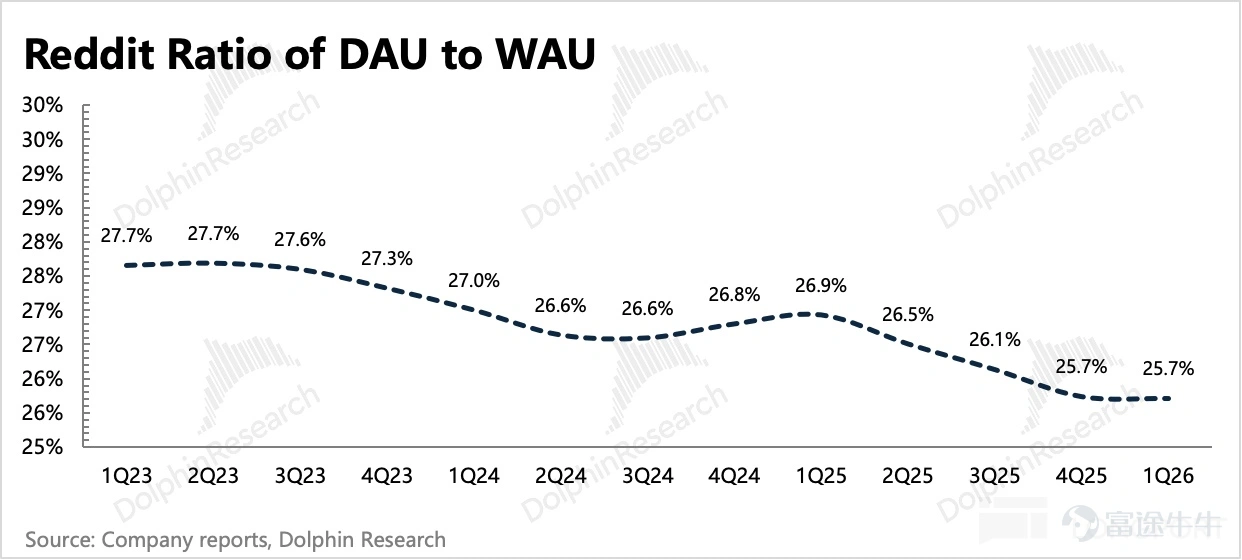

In Q1, platform DAU grew to 127 million, with a net addition of 5.4 million users. Weekly Active Users (WAU) increased by 23% year-over-year, adding 21.5 million users, while user stickiness (DAU/WAU) remained stable at 25.7% quarter-over-quarter.

Regionally, growth in the U.S., which contributes the majority of commercial value, continues to slow down from an already low base. Meanwhile, DAU in international regions grew by 26%, and the platform’s machine translation now covers over 30 languages worldwide.

2. Commercialization continues, but Q2 guidance indicates a notable slowdown in growth, likely due to macroeconomic factors and customary conservatism.

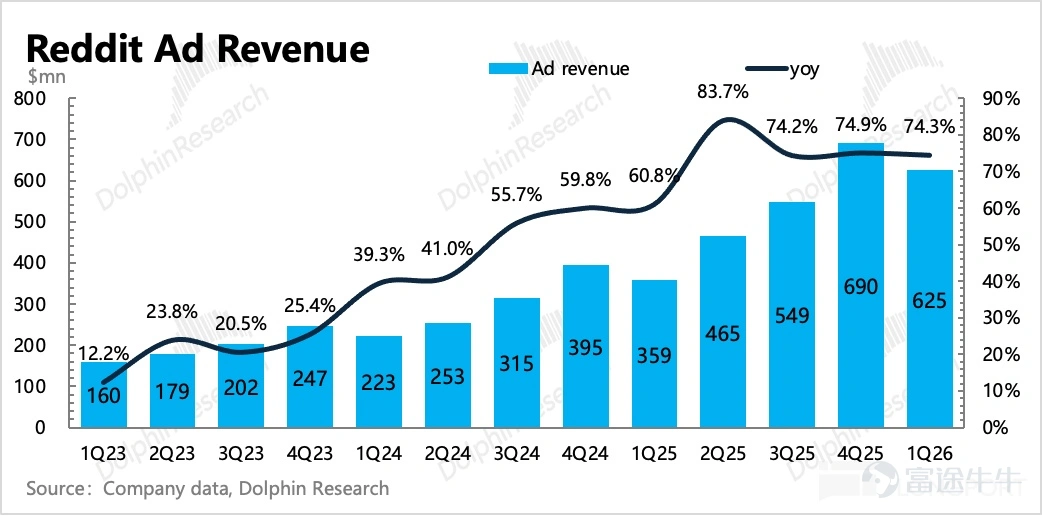

Q1 total revenue reached $730 million, a year-over-year increase of 69%, and remained largely flat quarter-over-quarter, significantly surpassing expectations. Management guided for a slowdown in Q2 revenue growth to 45%, which we believe is related to a high base effect, macro disruptions caused by geopolitical frictions, and management's habitual conservative guidance.

Revenue growth was primarily driven by advertising, including the shift from traditional brand advertising to performance-based advertising, achieving higher ROI, which led to higher CPMs, as well as increased ad load rates to capture market share. Performance-based advertising currently penetrates rapidly among advertisers in sectors like e-commerce and retail, mainly through DPA products (which allow advertisers to directly integrate their product catalogs into Reddit, where the platform’s AI dynamically matches and displays relevant products based on user interests and community context).Automatically match and dynamically display relevant products.This has contributed significantly to commercialization in the current quarter, and going forward, the company will also push Feed-based in-stream ads.

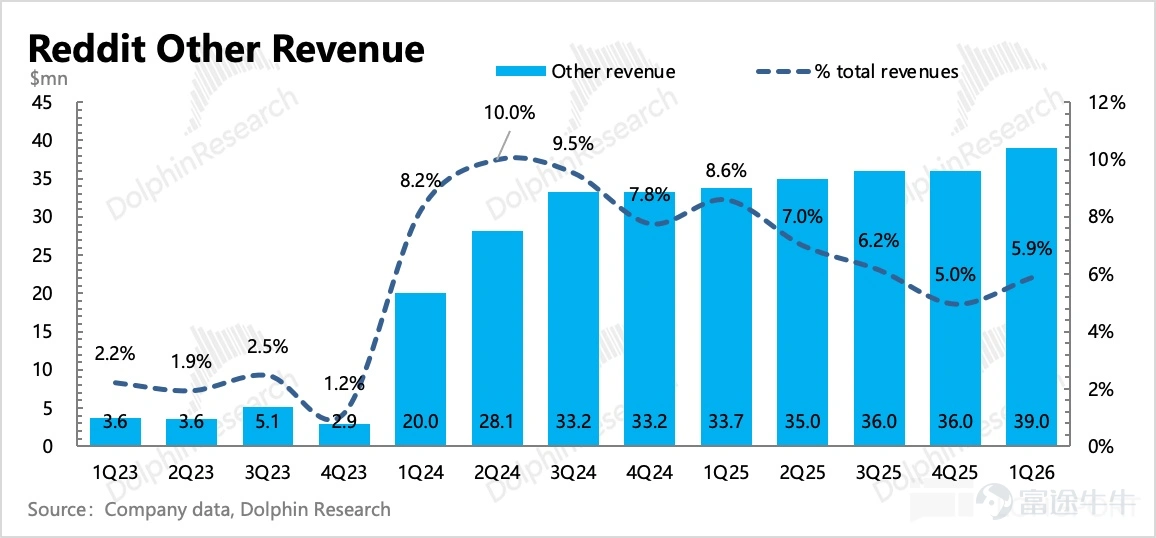

Data licensing revenue is recognized over time according to contracts and therefore remains relatively stable (major clients include Google, OpenAI, and other AI companies like Perplexity, which use the data for model training). By the end of this year, three-year contracts with Google and OpenAI will expire, and they are highly likely to renew. Meanwhile, Reddit hopes to deepen cooperation by having AI answers reference Reddit content and negotiating further commercial revenue sharing.

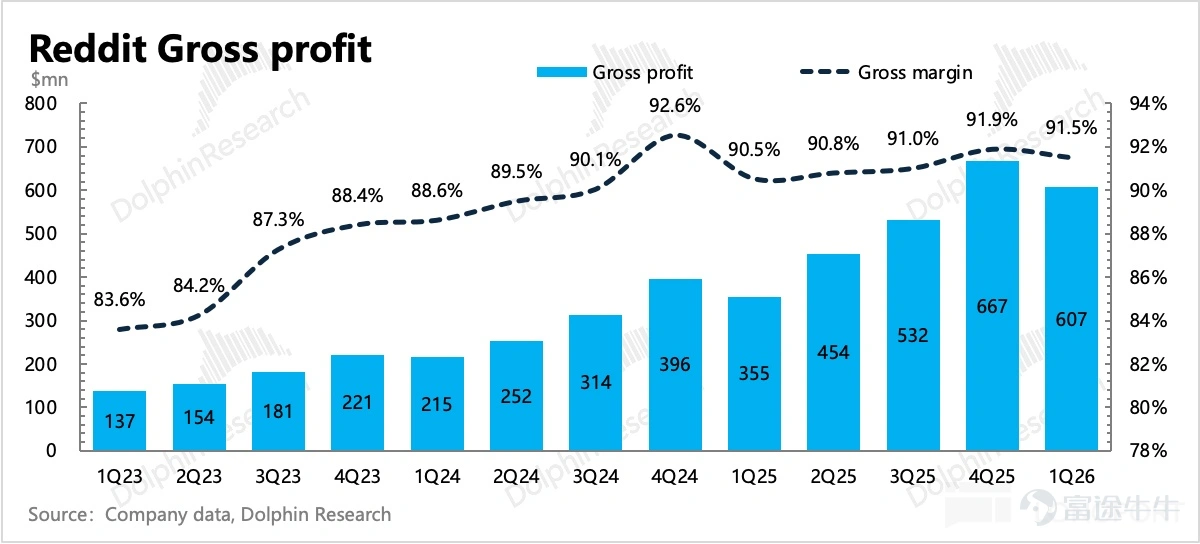

3. Profit margins continue to improve along the trend.

Gross margin in the first quarter improved by 1 percentage point year-over-year but experienced a slight decline quarter-over-quarter due to seasonal fluctuations. Compared to peers, it has basically peaked.

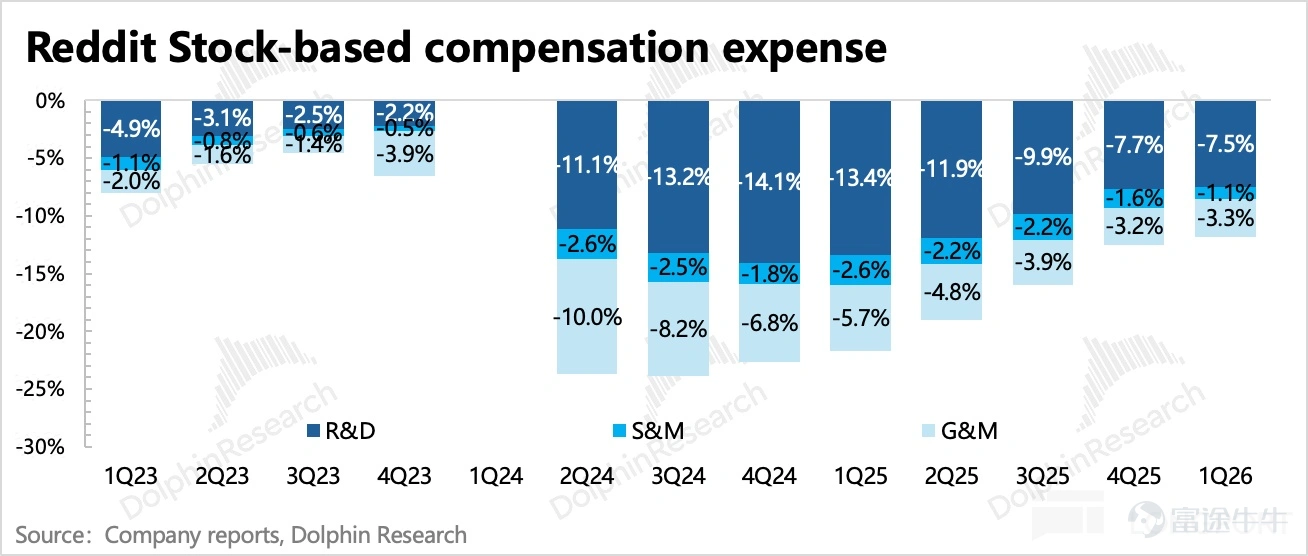

Sales expenses within operating expenses continued to grow rapidly, with a year-over-year increase of 80%, though this growth slowed compared to the previous quarter. This is likely due to ongoing efforts to promote advertising products and acquire end users. However, overall expenses were still significantly optimized by 14 percentage points, and equity incentive expenses as a percentage of revenue decreased from 22% last year to 12%.

The company’s profitability target—an adjusted EBITDA margin of 50%—was 40% in Q1, reflecting seasonal fluctuations (Q1 is typically a slower quarter compared to Q4), but remains on an upward trend. Free cash flow continues to reach new highs, accounting for 47% of revenue, consistent with the advertising industry's asset-light, cash-generating business model.

The $1 billion acquisition announced last quarter officially began execution in Q1, but only $5 million was spent, repurchasing 35,000 shares. The company had $2.7 billion in net cash at the end of Q1, and quarterly free cash flow has now reached $300 million, making the continuation of the share repurchase program manageable. However, the pace of repurchases has been relatively slow, and since there is no expiration date set for the $1 billion repurchase plan, the shareholder return rate cannot yet be calculated.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

1