NVIDIA is strongly promoting the 800V DC architecture. How should one position themselves?

The AI race has entered the 'Energy is King' era, with electricity becoming the key battleground defining the upper limit of computing power.

As global tech giants fiercely compete in computing chips, a more fundamental race is unfolding behind the scenes. Analysts at Morgan Stanley have recently sounded the alarm:Electricity has become the most critical physical constraint in the expansion of AI infrastructure.

Morgan Stanley's model predicts that U.S. data centers will face an electricity shortfall of approximately 55 gigawatts between 2025 and 2028. Data center projects worth $18 billion have already been directly canceled, while another $46 billion worth of projects have been delayed. The arms race for computing power is quickly evolving into an infrastructure war over 'watts.'

Guosheng Securities analysts point out: The market’s previous understanding of AI energy was mostly a linear extrapolation of 'expansion of computing power → increase in electricity demand.'Now, an increasing number of AI projects are not bottlenecked by GPUs, servers, or funding, but by issues like grid connection, transformer delivery, and interconnection approval.

AI development is forcing the overall reconstruction of the energy system on different time scales. From a time perspective, this can be divided into four phases: 'power supply upgrades—natural gas power generation—nuclear SMR—space-based computing.'

Short term: Enhance single-point power supply capabilities through power supply architecture upgrades.

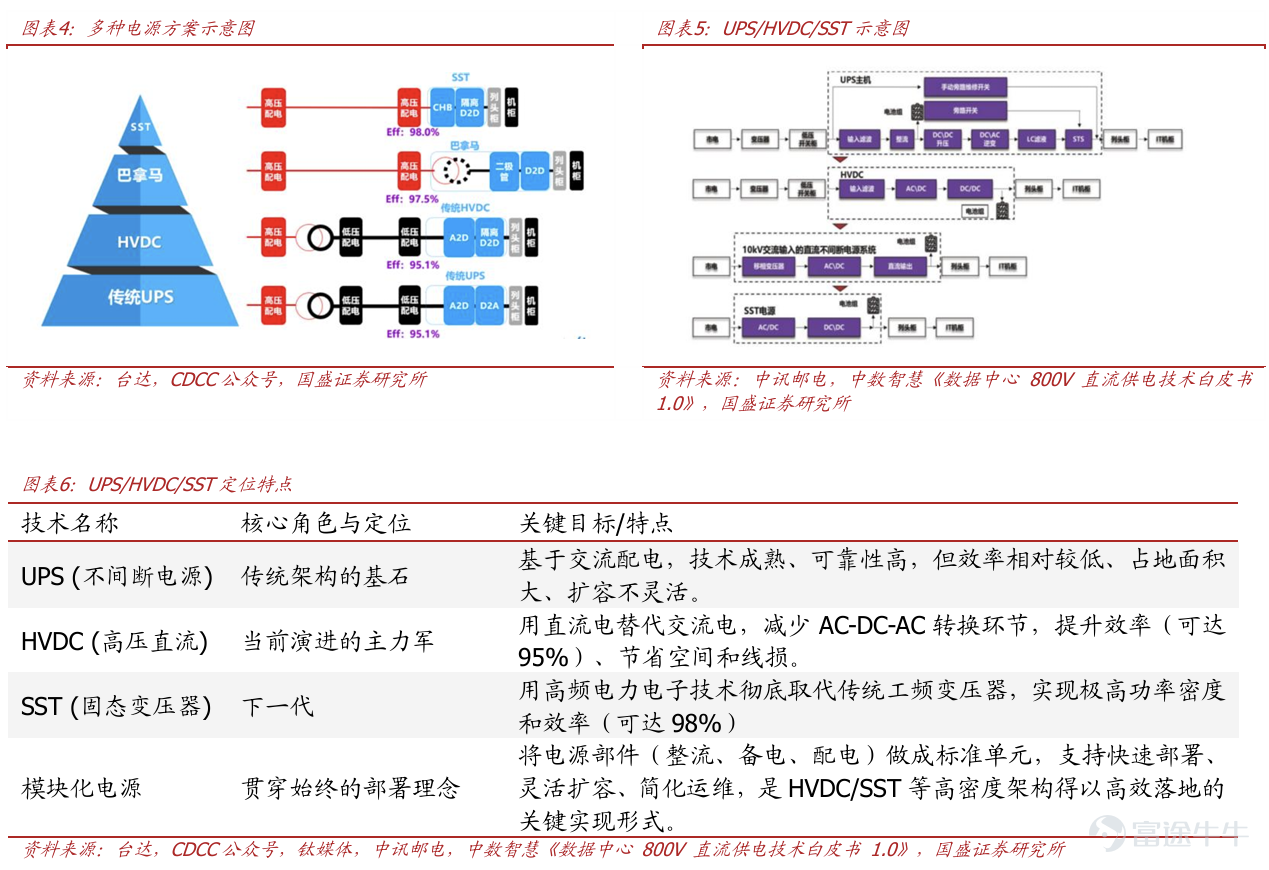

The battle first begins inside data centers. As NVIDIA's GB series evolves to the Rubin series, rack power density is experiencing a 'tectonic leap.' Traditional data center power architectures have now fully maxed out, with external cabinet power shifting towards high-voltage DC technology.

There are slight differences in product forms and technical approaches between domestic and overseas markets:

1) Domestically, cloud service giants represented by Alibaba and Tencent are taking the lead in promoting industrialization.240V/336V HVDC has been commercially deployed at scale, while the more revolutionary 'Panama Power' is becoming mainstream.This solution directly converts 10kV AC to 240V DC, with system efficiency reaching up to 97.5%, high integration, and significantly reducing initial construction costs. Dongwu Securities noted that the domestic HVDC market is expected to exceed 80 billion yuan by 2030, with a CAGR of approximately 122% from 2025 to 2030.

2) Overseas, the transition in technical routes is even more aggressive, primarily driven by NVIDIA's next-generation Rubin GPU platform’s mandatory requirement for 800V DC power supply.Overseas vendors are expected to bypass intermediate stages and directly adopt the 800V solution. Besides standalone power cabinet solutions, higher integration 'Sidecar' solutions have emerged overseas.(integrating power modules with the side of server racks), but its mass production difficulty is relatively high. Dongwu Securities pointed out that the overseas HVDC market is expected to surpass 140 billion yuan by 2030, with a CAGR of about 170% from 2025 to 2030.

Regardless of the path,the technological end goal points towards solid-state transformers (SST).SST eliminates bulky line-frequency transformers, achieving energy conversion and isolation through high-frequency power electronics technology, resulting in significant improvements in size and efficiency. SST is expected to begin large-scale deployment in the second half of 2027 and become the mainstream solution for AIDC external cabinet power supplies by 2029-2030, with the global market size potentially exceeding 100 billion yuan by 2030.

In this architectural upgrade, U.S. stocks $Vertiv Holdings (VRT.US)$ Playing a crucial role as NVIDIA's deep partner, Vertiv plans to be the first to mass-produce its 800VDC power supply series in the second half of 2026. The company’s Q1 2026 earnings report shows that revenue increased by 30% year-over-year to $2.65 billion, and net profit doubled from $164.5 million a year ago to $390 million. Vertiv’s stock price has also skyrocketed, rising from a low of $53.5 in 2025 to $330, repeatedly hitting new highs. As of the close on April 29, its cumulative increase in 2026 exceeded 89%. $GraniteShares 2x Long VRT Daily ETF (VRTL.US)$

This power supply revolution has also created opportunities for key upstream materials.Third-generation semiconductors, represented by silicon carbide, are at the core of supporting 800V architecture and solid-state transformers.US stocks $Wolfspeed (WOLF.US)$ , the Hong Kong stock market, $SICC (02631.HK)$ They are all leaders in silicon carbide (SiC).

$INFINEON TECHNOLOG (IFNNY.US)$ Infineon is technologically leading in high-voltage CoolSiC products and is also one of the main suppliers of core components for SST. Recently, its stock price surged to $65.76, with an annual increase of over 48%.

$First Trust Nasdaq Clean Edge Smart Grid Infrastructure Index Fund (GRID.US)$ The top five holdings include grid equipment leaders such as Eaton (ETN), ABB, and Schneider Electric. Since the beginning of the year, this fund has attracted more than $3.1 billion, six times that of the nearest competitor among similar ESG (Environmental, Social, and Governance) ETFs, with an annualized return of over 25% in the past three years.

Medium-term: Localized power generation through natural gas/SOFC, bypassing grid constraints.

When grid expansion requires 5-7 years while the construction cycle for AI data centers takes only 12-18 months, localized power generation becomes an inevitable choice. Among various options, natural gas power generation stands out—not because it has the lowest cost but due to its highest 'time value'.Time Value。

Natural gas units can start up and shut down quickly and offer flexible scheduling. They can serve as the primary power source or form a hybrid model with the grid. Additionally, laying natural gas pipelines is far easier and quicker than building new substations and high-voltage transmission lines. This makes natural gas a practical solution to push AI projects forward quickly when the grid is overloaded.

Specific to the technical pathway, the market has branched out into three main tracks:

First is theGas turbines,which operate on a principle similar to jet engines, with an enormous single-unit capacity (typically over 100 megawatts), making them suitable for providing stable base-load power to ultra-large-scale intelligent computing centers. Leading companies include global giants such as $GE Vernova (GEV.US)$ 、 $SIEMENS AG (SIEGY.US)$ 、 $Mitsubishi Heavy Industries (7011.JP)$ . The downside is their slower startup time and less responsive load adjustments compared to the instantaneous switching needs of AI computing power.

The second pathway isinternal combustion engine units,which utilize a piston reciprocating mechanism akin to automobile engines. Their greatest advantage lies in second-level startup capability and high modularity. This perfectly aligns with the frequent 'full load-idle' switching in AI training tasks, allowing rapid response during grid fluctuations. $Caterpillar (CAT.US)$ 、 $Cummins (CMI.US)$ Companies such as are leaders in this field.

The most disruptive technology issolid oxide fuel cellsBy using a solid oxide electrolyte to directly generate electric current through reactions between oxygen ions and fuel gases, this method boasts high efficiency with an energy conversion rate exceeding 60%, far surpassing traditional combustion approaches. $Bloom Energy (BE.US)$ As the global leader in SOFC technology, it directly converts natural gas into electricity through electrochemical reactions. The recent signing of a 2.8 GW mega-order with Oracle, along with explosive earnings growth, underscores the viability of this pathway. Year-to-date, BE has surged over 231.42%, demonstrating remarkable momentum.

Long-term: Nuclear power (especially SMRs) emerges as the ultimate engineering solution for AI applications.

Looking further into the future, AI data centers with gigawatt-scale stable loads require an ultimate solution: zero-carbon, stable, and powerful baseload energy. Increasingly, attention is turning towardnuclear energy, particularly Small Modular Reactors (SMRs).

Traditional nuclear power plants are massive reinforced concrete structures built on-site, with construction cycles spanning over a decade. In contrast, the core of SMRs lies in their 'modularity.' Take NuScale Power’s design as an example—each power module (77 MWe) is a cylinder about 23 meters high and 4.6 meters in diameter. Most of its construction and assembly can be completed in a factory, then transported by rail or road to the site for assembly like building with LEGO blocks. This approach reduces construction time to just 3-4 years, while occupying only one-quarter of the land required by traditional power plants, perfectly aligning with the rapid deployment needs of AI data centers.

Additionally, SMRs adopt a revolutionary 'passive safety system.' Utilizing physical principles such as gravity and natural convection, they can achieve long-term core cooling without external power or human intervention during accidents, fundamentally eliminating risks similar to those seen in the Fukushima nuclear disaster.

The rise of SMRs is reshaping opportunities within the nuclear energy supply chain:

Upstream fuel: New-generation SMRs predominantly use higher-enriched HALEU fuel, whose commercial production capacity is currently almost monopolized by Russia's state-owned atomic energy company. $Centrus Energy (LEU.US)$ is the only publicly traded company in the U.S. authorized to produce HALEU, currently at a critical stage of capacity building, with a prominent strategic position.

Midstream design and system integration: $NuScale Power (SMR.US)$ is currently the world's only SMR company to have received standard design certification from the U.S. Nuclear Regulatory Commission (NRC), possessing a first-mover advantage. However, NuScale also faces severe challenges, as the company is involved in securities class action litigation, accused of overstating the nuclear power experience of its partner ENTRA1. On April 21, Citi downgraded NuScale's rating to 'Sell' and lowered its target price to $9.

$Oklo Inc (OKLO.US)$ leverages its advanced fast reactor technology and deep partnerships with Meta and NVIDIA, boosting market confidence. HSBC initiated coverage on Oklo with a 'Buy' rating and set a target price of $96. NLR, as a high-purity nuclear energy ETF, not only bets on uranium prices but also benefits from the revaluation of nuclear assets and expectations of SMR construction, with cumulative gains exceeding 10% over 26 years.

Downstream operation and capital: Large electric utility companies such as $Duke Energy (DUK.US)$ 、 $Southern (SO.US)$ have extensive experience in nuclear power operations and are key forces driving the final implementation and grid connection of SMR projects.

Longer-term: Space computing power as an 'expanded dimension solution'

As the physical boundaries of Earth begin to constrain the expansion of computing power, the boldest thinkers are turning their eyes toward space. Establishing data centers in orbit, utilizing abundant solar energy and near-absolute-zero cosmic environments for cooling. Guosheng Securities noted that,Currently, the space computing power race has rapidly moved from conceptualization and feasibility verification stages into the engineering implementation phase.

Domestic and international companies are actively making moves, with overseas tech giants entering the market through self-research, partnerships, and technology empowerment, among other approaches.

$Rocket Lab (RKLB.US)$ : As one of the few commercial space companies with end-to-end capabilities (launch + satellite manufacturing), its Electron rocket is a key deployment vehicle for small satellite constellations and has drawn widespread market attention. In early 2026, RKLB's stock price hit a new high of $99.58 before recently entering a phase of consolidation and volatility.

$SpaceX (FT0002)$ : Its progress directly impacts the valuation and sentiment of the entire sector. According to the latest market reports, SpaceX plans to go public via an IPO in mid-June 2026, which could become the largest IPO in history, with a valuation potentially reaching $1.5 trillion to $2 trillion.

$Tema Space Innovators ETF (NASA.US)$ : The world’s first pure space economy ETF holds an exclusive position in SpaceX, while its other holdings include space infrastructure and operations companies such as Rocket Lab and Planet Labs. Launched at the end of March 2026, its unique ownership of SpaceX shares created significant market buzz, driving the stock price from $24 to $32.4 before undergoing a downward correction.

$Procure Space Etf (UFO.US)$ : A long-standing pure space-themed ETF, its holding EchoStar owns a small stake in SpaceX.

$ARK Space & Defense Innovation ETF (ARKX.US)$ : The space exploration fund actively managed by 'Cathie Wood' includes innovative firms such as Rocket Lab and Archer Aviation in its portfolio.

The competition in AI has entered the infrastructure era. For investors, understanding and positioning themselves within this grand narrative of 'energy defining computing power' might be the anchor to capturing the most robust value amid the AI wave.

P.S. How to seize investment opportunities? Make good use of the 'Industry Chain' feature to discover upstream and downstream opportunities ahead of time.

Path: Market --> US Stocks/HK Stocks --> Industry Chain

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments (4)

to post a comment

211

459