2026 IPO bonanza! Over 90% of new stocks rose on their debut

Good Doctor Cloud Healthcare's gross margin has been declining continuously: sales expenses exceeding 20 billion over three years, with a 6-billion-yuan valuation adjustment bet adding pressure

On April 10, 2026, Sichuan Good Doctor Cloud Healthcare Technology Group Co., Ltd. (hereinafter referred to as Good Doctor Cloud Healthcare) submitted its prospectus to the Hong Kong Stock Exchange again, with Haitong International acting as the sponsor.

This is the company's renewed attempt following the expiration of its initial filing in September 2025. Notably, according to the valuation adjustment agreement signed with investors, if the company fails to complete a qualified IPO before December 31, 2026, investors have the right to demand share redemption. This means the window for the company’s listing is becoming increasingly tight.

The most significant change in this filing lies in the lineup of sponsors — during the initial filing, Haitong International and CITIC Securities were joint sponsors, but CITIC Securities withdrew on April 8, 2026, leaving Haitong International as the sole sponsor. In the eyes of the market, this is undoubtedly not good news.

A Hong Kong stock market observer pointed out, 'Generally speaking, for a Hong Kong IPO, a prestigious lineup of sponsors indicates a higher probability of passing the listing review and advantages in terms of issuance; conversely, if intermediaries are reduced, it will affect market confidence.'

Nearly 80% of revenue comes from direct drug supply, with gross margin declining by seven percentage points.

According to the prospectus and Tianyancha, Hao Doctor Cloud Healthcare was founded in 2016 as a service provider focused on primary healthcare terminals. The company's main businesses consist of three segments: direct drug supply and distribution services, specialized disease diagnosis and treatment solutions, and diagnostic testing solutions, aiming to extend quality medical resources to grassroots markets.

According to data from CIC, based on 2024 revenue, Hao Doctor Cloud Healthcare ranks second in China’s primary healthcare direct drug supply market and first in the diagnostic testing solutions market.

As of December 31, 2025, the company has directly served over 670,500 primary healthcare terminal clients, covering more than 99% of county-level administrative regions nationwide.

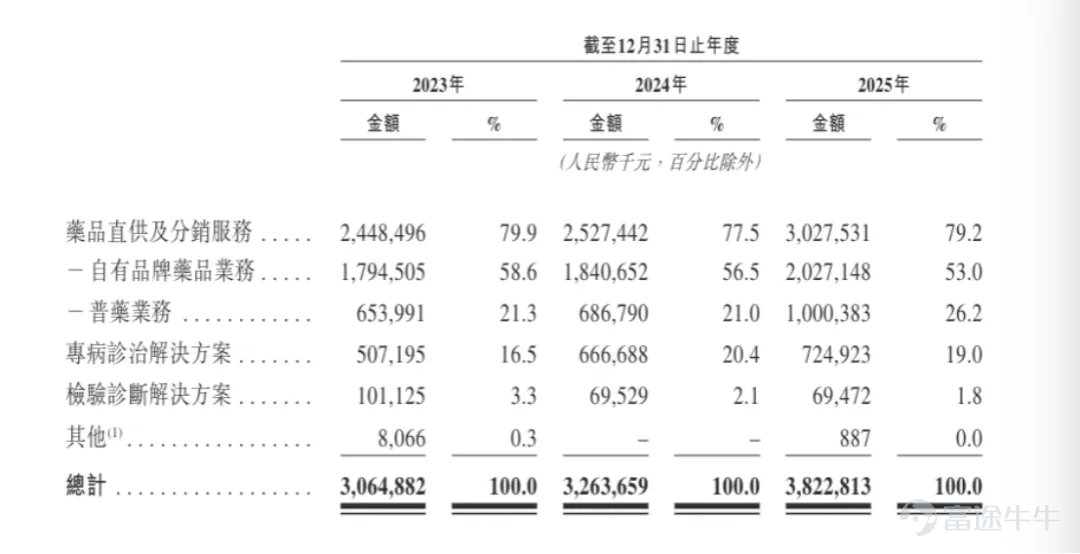

In terms of revenue figures (hereinafter referred to as the reporting period), the company reported total revenues of 3.065 billion yuan, 3.264 billion yuan, and 3.823 billion yuan, respectively, with a compound annual growth rate of 11.7%, showing apparent steady growth on the surface.

However, after breaking down the revenue structure in detail, the problem becomes clear: revenue from direct drug supply and distribution services accounted for 79.9%, 77.5%, and 79.2%, respectively. Among them, the proprietary branded drugs business accounted for approximately 53%, while the generic drugs business made up around 26%, together supporting nearly 80% of the total revenue. Revenue from specialized disease diagnosis and treatment solutions accounted for about 19%, whereas diagnostic testing solutions only made up roughly 1.8%, which is almost negligible.

This means that the company is essentially a drug distribution enterprise, and the so-called 'digital intelligence empowerment' is barely reflected in its revenue.

More notably, profitability levels are concerning. During the same period, the company’s adjusted net profit (non-Hong Kong Financial Reporting Standards measure) amounted to 65 million yuan, 87 million yuan, and 83 million yuan, corresponding to net profit margins of only 2.13%, 2.66%, and 2.17%, consistently fluctuating narrowly at the edge of profitability. A revenue scale of 3.8 billion yuan only translates into less than 100 million yuan in profit, making such profitability clearly unsatisfactory.

The trend in gross margin is even more concerning — 29.9% in 2023, dropping to 26.4% in 2024, and further declining to 22.9% in 2025, with a cumulative decrease of more than 7 percentage points over three years.

The continuous decline in gross margin may reflect the weakening bargaining power of the company within the industrial chain. Homogenized competition in pharmaceutical distribution is constantly squeezing price margins, and the company lacks the ability to obtain premium pricing through technological innovation, forcing it to trade volume for price, falling into a dilemma of revenue growth without profit improvement.

Prioritizing marketing over R&D, sales expenses exceed 2 billion over three years

Turning our attention to the expense side, the root cause of the company's poor profitability becomes glaringly obvious.

First, let’s look at R&D expenses. During the reporting period, the company's R&D expenditures were 8.5 million, 7.5 million, and 13.08 million respectively, accounting for only 0.28%, 0.23%, and 0.34% of total revenue during the same period. Although there was a 74.67% year-on-year increase in 2025, the absolute amount was still only 13.08 million. By the end of 2025, although the R&D team had 204 members, the average annual R&D investment per person was only about 64,200, offering almost no technical competitive advantage in industry competition.

The fundamental reason for such meager R&D expenses lies in the company's OEM model. The prospectus explicitly discloses: 'Sichuan Canon sells pharmaceuticals produced internally by Sichuan Canon, while the products sold by our company are mainly procured from upstream pharmaceutical enterprises and directly manufactured by OEM under our own brand.'

In other words, the company does not build its own factories nor control core pharmaceutical production processes but instead outsources manufacturing to upstream pharmaceutical companies. After branding the products with its own label, they are sold downstream through proprietary channels. Under this model, the company's core competencies are confined to product selection and channel management rather than product development, naturally minimizing R&D investment to the extreme.

Although the prospectus emphasizes that the company 'has created over 2,400 medical diagnostic tags using AI technology,' these digital tools are only used to assist in diagnosis and improve operational efficiency and cannot directly generate high-margin revenue streams.

The sales model is another key to understanding the company’s cost structure. The company adopts a dual-track system of 'APP-based online ordering + offline field promotion teams': customers primarily complete purchases through the 'Good Medicine Preferred' APP, while field promotion teams (internal sales and outsourced CSO) are responsible for developing, maintaining, and promoting academic activities for grassroots medical terminals.

During the reporting period, direct sales accounted for 96.1%, 87.3%, and 77.6% of revenue respectively, with distributor sales gradually increasing, but direct sales remaining the dominant force. Under the direct sales model, every transaction bears logistics fulfillment, manpower service, and customer maintenance costs, resulting in inherently high expense ratios.

This is precisely the root cause of the high selling expenses. During the reporting period, sales and marketing expenses reached as high as 747 million yuan, 698 million yuan, and 675 million yuan respectively, accounting for 24.37%, 21.39%, and 17.65% of revenue. The cumulative total over three years exceeded 2.12 billion yuan.

Renowned financial audit expert Liu Zhigeng stated: 'From the data, from 2023 to 2025, the company's sales and marketing expenses were 747 million yuan, 698 million yuan, and 675 million yuan respectively, with their share of revenue decreasing year by year from 24.37% to 17.65%. This trend indicates that as the business coverage expands (serving more than 670,000 grassroots terminals and covering over 99% of counties nationwide), its field promotion system and brand influence have formed a network effect, reducing marginal customer acquisition costs and improving marketing efficiency.'

At the same time, the company has a large sales team, with 476 full-time sales personnel and 8,881 outsourced CSO personnel as of the end of 2025, forming a 'field promotion force' that supports its deep penetration into lower-tier markets. This high-density coverage reduces the promotional cost per customer, which is the core reason for the decline in expense ratio.

It can be seen that the continuous decline in the proportion of Good Doctor Cloud Medical's sales expenses reflects the emergence of marketing scale effects, with unit customer acquisition costs trending downward.

Liu Zhigeng further pointed out: 'High sales investment significantly pressures net profit, with profitability clearly strained. Despite improved marketing efficiency, high sales investment still severely squeezes profit margins. From 2023 to 2025, the company’s net profit fluctuated dramatically: 62.479 million yuan, 37.806 million yuan, and 54.052 million yuan, with a net profit margin of only 1.4% in 2025. Sales expenses over three years cumulatively exceeded 2.12 billion yuan, far surpassing R&D expenditures during the same period (totaling less than 30 million yuan), reflecting the essence of the company’s 'sales-heavy, R&D-light' business model.

Additionally, the company's gross margin fell from 29.9% in 2023 to 22.9% in 2025, with all three major business segments experiencing margin declines, further compressing the profit buffer. Under the backdrop of being pushed by a valuation adjustment mechanism to go public (facing potential redemption pressure exceeding 600 million yuan if not listed by the end of 2026), the company finds it difficult to drastically cut sales investment to maintain growth, meaning profitability pressures will persist.

The breakdown of expenses reveals a noteworthy structural change: market promotion fees (mainly CSO promotion service fees) decreased from 505 million yuan to 393 million yuan, with their proportion dropping from 67.63% to 58.22%; while employee welfare expenses increased from 163 million yuan to 197 million yuan, with their share rising from 21.82% to 29.19%.

This indicates that the company is gradually replacing outsourced CSOs with its own field promotion teams, which, while temporarily reducing market expenses in the short term, results in rigid increases in labor costs, leaving limited room for a decrease in overall expenses.

Administrative expenses also showed an accelerating inflationary trend. They were 93 million yuan in 2023, 97 million yuan in 2024, and surged to 136 million yuan in 2025, a year-on-year increase of 40.21%, already 1.47 times that of 2023.

The prospectus attributes the growth to four aspects: increased employee costs due to administrative staff expansion, higher listing-related expenses, increased depreciation, amortization, and rental expenses with scale expansion, and rising third-party payment platform fees. The expansion rate of management costs significantly outpaced revenue growth, further squeezing the already thin profit margins.

Related-party transactions add another layer of concern to the quality of profitability. Canon Sichuan, one of the company's controlling shareholders, is also its largest supplier. During the reporting period, the company’s procurement from Canon Sichuan was RMB 302 million, RMB 404 million, and RMB 529 million respectively, with the proportion of total procurement rising from 10.30% to 13.70%, then to 15.40%, showing an increasing trend year by year.

Under the terms of ongoing related-party transactions, the upper limits for procurement in the years 2026 to 2028 are set at RMB 624 million, RMB 749 million, and RMB 899 million respectively, indicating that the proportion of related-party transactions will likely continue to rise. Although the prospectus claims that transactions were conducted on 'normal commercial terms,' the dual role as both a supplier and controlling shareholder raises persistent doubts about the fairness and independence of the pricing.

The runaway growth of receivables is the most direct signal of declining earnings quality. As of the end of 2023, the net amount of the company's trade receivables and notes receivable stood at only RMB 300 million. By the end of 2024, this figure increased to RMB 780 million and skyrocketed to RMB 1.54 billion by the end of 2025, marking an increase of over 413.33% within two years. The corresponding turnover days extended from 2.70 days to 6.10 days, and further lengthened to 11.20 days, with the collection speed in 2025 being less than a quarter of that in 2023.

Family holding 65.99%, valuation adjustment agreement looms

The company’s equity structure is highly concentrated, featuring typical characteristics of family control. GENG Jie, Chairwoman of the Board and Executive Director, is married to Xue Yuan, the Chief Technology Officer. Xue Yuan is also the brother-in-law of Geng Yuefei, a non-executive director. Geng Yuefei’s father, Geng Furen, is the actual controller of Good Doctor Pharmaceutical Group Co., Ltd.

According to the prospectus, the controlling shareholder group — encompassing GENG Jie, Geng Furen, Geng Fuchang, Geng Yuefei, Xue Yuan, Canon Sichuan, Cloud Healthcare Hong Kong, Hengqin Cloud Healthcare, Hengqin Guoyi Investment, and Jiayue Ruihe — collectively controls approximately 65.99% of the company’s voting rights. Even after the completion of the IPO (assuming no exercise of the over-allotment option), this percentage will remain at an absolute controlling level.

Under a governance structure where family members occupy the majority of board seats and major decisions are made internally, whether mechanisms to protect the interests of minority shareholders can function effectively is a matter of concern.

However, a more pressing risk than family control stems from the valuation adjustment agreement. Pre-IPO investors (including OrbiMed Asia Partners IV, Shanghai Kangrang, Desai Innovation, and Shibei Hi-Tech) have been granted a full set of special rights: director nomination rights, preemptive rights, co-sale rights, anti-dilution rights, information and inspection rights, and most crucially, withdrawal rights. Although withdrawal rights have been suspended, they come with four automatic reinstatement triggers: if the company or its representatives withdraw the listing application; if the company terminates its listing plan; if the listing application is not accepted by the Stock Exchange or is returned; and if the listing is not completed by December 31, 2026, whichever occurs first.

This means the company is racing against time. From the second filing on April 10, 2026, to the hard deadline of December 31, 2026, the company has less than a nine-month window to complete the entire process of hearing, offering, pricing, and listing — an extremely tight schedule for any Hong Kong IPO-bound enterprise.

Once the valuation adjustment agreement is triggered, Pre-IPO investors will have the right to demand that the company redeem their shares.By the end of 2025, the company's current portion of redemption liabilities has reached 623 million yuan, far exceeding its net asset value of 17 million yuan. Whether the company will have the ability to repay at that time remains a big question mark.

The proceeds from this IPO are proposed to be allocated across four key areas: First, national market expansion for core businesses, increasing coverage, growing the customer base, and enhancing brand recognition; second, research and development infrastructure, including upgrading technological foundations and creating new service solutions; third, strategic investments and acquisitions targeting upstream pharmaceutical companies, downstream distributors, and related technology firms; and fourth, supplementing general working capital. (Produced by Harbor Finance)

"Harbor Business Observation" Xu Huijing

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment