AI Boom vs. Tight Liquidity: Will the US Stock Rally Continue?

Wash's Debut Hearing: A Political Performance with More Style than Substance

Key Points

1. Wash’s nomination hearing for Fed Chair was essentially a political performance with more style than substance. By narrating an extensive biography, it systematically avoided core policy issues such as the interest rate path and balance sheet reduction plans. It only defined two boundaries through strong rhetoric: an inflation hawk stance and the reconstruction of the Fed's independence. At the same time, it exposed three major controversies: personal conflicts of interest, shifts in policy positions, and questionable decision-making independence.

2. The policy combination of 'quantitative tightening + interest rate cuts,' which is generally considered contradictory by the market, is underpinned by a complete and self-consistent theoretical logic and narrative framework. Its core objective is to push the Federal Reserve to exit its quasi-fiscal functions, return to its monetary policy role, and reconstruct the US money creation mechanism. Essentially, it represents the systematic extension of the 'America First' strategy into the realm of monetary sovereignty amidst the anti-globalization wave.

3. The confirmation process for Warsh's nomination still faces significant political game uncertainty. The current market may, to some extent, underestimate the probability and potential impact of two non-baseline scenarios: the obstruction of the nomination and a recess appointment.

4. The final implementation of Warsh's policy framework may depend on decisions regarding three core propositions: trading off non-core functions to gain independent space in key monetary policy areas, reconstructing the inflation analysis framework to achieve a dynamic balance between price stability and economic growth, and reshaping the dollar system through the contraction of the Federal Reserve’s global role.

5. The fundamental reconstruction of the Fed's policy logic brought by Warsh might trigger a structural increase in market volatility. June to September 2026 will be the critical observation window for verifying the implementation of the policy framework.Hearing debut: A political performance where style outweighs substance

(1) Characteristics: Structural avoidance in a 2,000-word statement

1. Increased length but hollow content: Resume storytelling replaces policy elaboration

On the evening of April 21, 2026, the nomination hearing for the Chair of the Federal Reserve held by the US Senate Banking Committee was expected to serve as a crucial indicator for anchoring the direction of global monetary policy. However, nominee Kevin Warsh completed his public debut in an almost paradoxical manner—submitting a written statement far longer than those of previous nominees while displaying striking vacuity on core policy issues. Warsh’s public statement approached 2,000 words, twice the length of the testimonies given by his predecessor, Jerome Powell, and former chair Janet Yellen during their respective debuts. Yet, the increased length did not bring about a corresponding rise in information density, instead revealing a strategy of structural avoidance. Extensive sections were devoted to detailing personal history, emphasizing grand narratives at 'critical historical junctures,' and expressing openness to cooperation with Congress, while substantive policy issues of greatest concern to global investors—such as the path of interest rates and plans for handling the balance sheet—were systematically excluded from the text.

Traditionally, while the nomination hearings for the Chair of the Federal Reserve are not devoid of political posturing, candidates typically release directional guidance in key policy areas to reassure market expectations and establish initial policy credibility. However, Warsh’s statement displayed a deliberate 'de-politicization' characteristic: he used large portions of the document to recount his experience as a Federal Reserve Governor, his academic research achievements at Stanford University, and his deep ties with Silicon Valley’s industry, striving to build an image of himself as 'experienced and up-to-date,' while entirely avoiding any specific commitments regarding future policy operations. We believe this strategy was no accident but rather Warsh's response to the current polarized political environment—against the backdrop of significant uncertainties surrounding the confirmation of his nomination, any concrete policy commitment could become a target for bipartisan political games in the Senate, directly constraining his policy flexibility after taking office. For these reasons, several Wall Street analysts have directly characterized this hearing as a 'political show where style trumps substance,' viewing it as more of a procedural political ritual rather than a serious policy debate.

2. Systematic silence on core monetary policy issues: Interest rate paths and balance sheet disposal

The most analytically valuable aspect of Wash's testimony is not what was explicitly stated, but rather the core issues that were deliberately omitted. In his statement, Wash made no directional judgment on the interest rate path, which is currently of high market concern—neither openly denying his recent repeated calls for rate cuts, nor providing clear confirmation. This deliberate ambiguity aligns with the overall avoidance of monetary policy details throughout his statement. More crucially, the central policy issue of aggressive balance sheet reduction, which Wash had long publicly advocated, was not mentioned at all in the 2,000-word text.

This silence starkly contrasts with Wash's previous public stance. According to Joe Gagnon, a researcher at the Peterson Institute for International Economics, Wash explicitly stated in a public speech that reducing the Federal Reserve’s balance sheet by $1 trillion would have a tightening effect on the economy equivalent to a 50-basis-point interest rate hike. Mark Cabana, head of U.S. interest rate strategy at Bank of America Global Research, further pointed out that balance sheet contraction is likely to become the core logic of Wash's policy framework—achieving implicit tightening through balance sheet reduction, thereby creating policy space for lowering nominal interest rates. However, these policy logics, which were clearly articulated in academic settings and media interviews, completely disappeared during the Senate's formal questioning. This sharp contrast between 'clarity off the field and ambiguity on the field' precisely reveals Wash’s risk management approach: before officially becoming the Fed chair, any specific commitment could transform into a rigid constraint in the future, while maintaining strategic ambiguity allows for maximum flexibility in policy operations after taking office.

(II) Core viewpoints, incremental information, and points of contention

While systematically avoiding specific policy paths, Wash used selective tough rhetoric in his testimony to clearly delineate two immovable boundaries—one being the hawkish characterization of inflation, and the other a reinterpretation of the Fed's independence. His deliberate ambiguity and avoidance on key issues also constitute the main market point of contention in this hearing.

In terms of core policy propositions, the framework built by Wash can be summarized along several dimensions:

First, the policy combination of 'balance sheet reduction + rate cuts' becomes the central thread of his monetary policy.

At the balance sheet level, Wash has continued his strong opposition to the normalization of quantitative easing (QE), explicitly stating that the Fed's balance sheet “should be smaller,” focusing on exiting quasi-fiscal functions and returning to its monetary policy role, particularly avoiding holding large-scale long-duration assets and real estate-related securities over the long term. At the interest rate policy level, although he made no explicit promise of rate cuts, he did state that “interest rate tools are more inclusive than balance sheet tools,” while emphasizing the need for coordination between interest rate policies and balance sheet policies, already showing some inclination toward rate cuts. The core logic of this combination involves achieving implicit liquidity tightening through balance sheet reduction to offset the risk of inflation rebound from potential rate cuts, while reconstructing the role of monetary policy tools.

Second, pushing for comprehensive reform of the inflation analysis framework is the key lever in his inflation governance.

As a research assistant to Milton Friedman, Wash’s inflation philosophy carries a distinct monetarist hue. He characterized the high inflation experienced by the Fed in 2021-2022 as a fundamental policy error, believing that the loss of control over inflation in recent years has severely weakened the Fed’s policy credibility, and the current inflation indicators used by the Fed are insufficient to guide policy decisions. He explicitly proposed adopting more representative metrics such as median inflation and trimmed mean inflation, focusing on underlying inflation trends while excluding one-off impacts like geopolitical conflicts and energy price volatility, even suggesting that the Fed lead a big data project covering “billions of commodity prices” to reconstruct the inflation observation system. Additionally, he incorporated the artificial intelligence (AI) wave into the core judgment of inflation prospects, believing that AI-driven productivity improvements will be a long-term core deflationary force, which forms the primary theoretical support for his interest rate cut advocacy.

Third, the systematic restructuring of the Fed's functional boundaries and communication mechanisms is the core goal of his reform.

Wash cited Friedman's assertion of the 'tyranny of the status quo,' emphasizing that the Federal Reserve must break free from its policy path dependency in the post-crisis era. The key is to stay within the lane of its statutory responsibilities—when the Fed ventures into areas like fiscal and social policies where it lacks statutory authority and expertise, its independence will face the greatest risks. Meanwhile, he sharply criticized the Fed’s current communication mechanism, explicitly opposing excessive reliance on dot plots and forward guidance. He argued that pre-setting interest rate paths would make policymakers 'prisoners of their own forecasts,' amplifying the impact of policy errors. He advocated for less forward guidance and more flexible meeting decisions, even bluntly stating that Fed officials currently speak too frequently, and over-transparency is no longer the core issue for market stability but instead creates excessive communication noise.

Fourth, the redefinition of the Fed’s independence became the most controversial statement during the entire hearing.

Wash repeatedly pledged to be an 'independent actor' and vowed not to become a 'puppet' of Trump, emphasizing that the president had never asked him to make a commitment to cut rates. However, at the same time, he proposed that 'the independence of the Fed mainly depends on the Fed itself,' suggesting that independence is not an inherent institutional right. Elected officials commenting on interest rates does not pose a particular threat to monetary policy independence. When faced with sensitive questions from Democratic lawmakers regarding the 2020 election results, Trump pressuring Fed officials, and the DOJ’s criminal investigation into Powell, Wash evaded all substantive responses by citing reasons such as 'the case is in the judicial process' and 'Congress has certified the election results.'

The incremental information from this hearing lies precisely in the details of these statements. On one hand, Wash clarified for the first time the prioritized path and accompanying logic of balance sheet reduction, proposing that it will be coordinated with the Treasury Department to avoid market disruptions. Mortgage-backed securities (MBS) will be the primary target for reduction, breaking market skepticism about the inability to push forward balance sheet reduction under high fiscal deficits. On the other hand, Wash outlined his prioritization of policy tools, designating interest rate tools as the core conventional means of monetary policy, while balance sheet tools serve only as unconventional crisis-response measures at the zero lower bound, fundamentally reversing the Fed’s post-crisis reliance on QE. Additionally, he addressed the linkage between regulatory reform and balance sheet reduction, hinting that optimizing liquidity supervision rules and reducing banks’ reserve requirements will create institutional conditions for balance sheet reduction. This also implies that his balance sheet reduction plan will be deeply tied to the easing of banking regulations.

The controversies of the hearing centered on three main layers: First, ethical and conflict-of-interest disputes. Wash’s personal assets, estimated at approximately $190 million, were not fully disclosed, including shares in SpaceX and cryptocurrency-related investments. Despite his pledge to divest these assets upon taking office, Democratic lawmakers widely questioned the potential conflicts of interest, arguing that undisclosed assets could influence his decision-making independence. Second, credibility disputes over policy stances. Known historically as an inflation hawk, Wash resigned from the Fed Board in 2011 due to opposition to quantitative easing but quickly pivoted to support rate cuts after 2024. His shift was questioned by the market as pandering to Trump’s demand for rate cuts. Furthermore, his deliberate vagueness on the prerequisites and pace of rate cuts during the hearing deepened market divisions over his policy path. Third, substantive disputes over independence. Wash’s avoidance of sensitive questions related to Trump led Democratic lawmakers to believe he lacked the courage to resist White House political pressure. As Warren noted, if a Fed chair cannot even state facts displeasing to the nominator, they cannot possibly stand up to the president when it matters most.

The underlying logic of Wash’s policy proposals: A seemingly contradictory combination but a coherent reconstruction

The market generally views Wash’s 'balance sheet reduction + rate cuts' policy mix as a paradoxical contradiction, but a deeper analysis of his policy logic reveals that this seemingly conflicting approach has a complete and coherent underlying narrative and theoretical foundation. Essentially, it represents a systematic extension and reconstruction of the 'America First' strategy in the realm of monetary sovereignty amid the wave of deglobalization.

The starting point of Wash’s policy logic is a comprehensive rejection and reflection of the Fed’s post-crisis monetary policy. In his view, the core issue with the normalization of QE over the past decade is that monetary policy has taken on excessive fiscal and social functions, deviating entirely from its statutory mission of price stability and full employment. On one hand, the continuous expansion of the balance sheet primarily boosted financial asset prices, benefiting a small number of asset holders while failing to reach ordinary citizens, further exacerbating wealth inequality in American society. On the other hand, the Fed’s excessive involvement in areas like climate change and social equity has led to significant mission creep, undermining its focus on core mandates like inflation and employment and entangling it in political controversies, fundamentally risking its independence. Therefore, the central thread of all Wash’s policy proposals is to bring the Fed 'back to basics'—exiting quasi-fiscal functions, systematically contracting the balance sheet, and refocusing monetary policy on interest rate tools and the statutory mission of price stability.

The 'balance sheet reduction + rate cuts' policy combination is precisely the implementation path for this core goal. The two are not contradictory but form a clear complementarity and synergy. From the perspective of rate cuts, Wash does not unconditionally support monetary easing; his rationale for cutting rates rests on two core judgments: First, the AI technological revolution will bring a systemic increase in total factor productivity, creating a long-term disinflationary effect that allows the U.S. economy to replicate the 'high growth, low inflation' Goldilocks scenario of the 1990s, thereby opening space for a decline in the neutral rate and policy rate cuts—a logic directly对标Greenspan’s classic move of betting on the internet technology revolution. Second, interest rate tools are more inclusive and equitable policy instruments; rate cuts can broadly reduce financing costs for households and small and medium-sized enterprises, directly benefiting the real economy, unlike QE, which benefits only Wall Street and financial asset holders. This reasoning addresses the Trump administration’s demand for rate cuts and provides solid academic and theoretical support for his policy stance shift.

From the perspective of balance sheet reduction, Wash’s approach is not simply about tightening liquidity but represents a fundamental reconstruction of America’s money creation mechanism. In his view, the balance sheet expansion brought by QE is a typical form of exogenous money creation, with the central bank directly injecting liquidity into the market, distorting resource allocation efficiency. Reducing the balance sheet while relaxing bank regulations and promoting market-driven credit expansion by the banking system restores money creation to an endogenous model, returning resource allocation rights from the government and central bank to the private sector. This transformation aligns with his conservative policy orientation. As the AI technological revolution boosts productivity in the private sector, market-driven resource allocation is far more efficient than government intervention. At the same time, balance sheet reduction can offset inflation risks potentially caused by rate cuts at the base money level, tightening the overall monetary spigot to prevent inflation from rebounding after rate cuts, achieving the effect of 'policy balance between looseness and tightness, with each tool fulfilling its role.'

On a deeper level, Wash's policy framework essentially represents a repositioning of the Federal Reserve's global role. In the era of globalization, the Federal Reserve has long assumed the function of a 'global central bank,' endlessly supplying dollar liquidity worldwide through quantitative easing (QE), making the dollar a kind of global public good. However, in the era of deglobalization, Wash advocates for the Federal Reserve to completely abandon this role, tightening control over the dollar’s monetary supply and shifting from being a global central bank providing liquidity to focusing on domestic productivity and safeguarding the credibility of the dollar as a sovereign currency. This transformation is a core manifestation of Trump's 'America First' strategy in the monetary domain, and the ultimate focal point of all his policy propositions.

Nomination Outlook: Triple Scenarios Amid Political Maneuvering, Uncertainty Becomes the Greatest Certainty

Although the hearing has concluded, whether Wash will smoothly succeed Powell as the Federal Reserve Chair still depends on the complex bipartisan political maneuvering in the Senate. His nomination prospects are not the 'high-probability event' previously priced in by the market but instead are filled with unexpected uncertainty.

Based on the current U.S. political landscape, Wash’s nomination prospects can be divided into three scenarios, and the market may generally underestimate the possibility of his nomination being blocked.

Given that Republicans hold only a two-seat advantage in the Senate Banking Committee, Tillis effectively possesses a 'veto power': if he casts an opposing vote, the committee will reach a 12-12 deadlock, and the nomination will be shelved. Tillis has already publicly revealed his stance — 'No withdrawal of the investigation, no advancement of the nomination' — demanding that the Trump administration terminate the criminal investigation into the incumbent Chair Powell; otherwise, he will not approve the nomination. This positioning creates the following three scenarios:

Scenario One: Nomination Stalemate, Powell Remains as 'Acting Chair' Until the End of the Year

This is becoming the default path in the current market. Tillis’ position has shown no signs of softening, and Wash’s nomination cannot complete a full Senate vote before Powell’s term expires on May 15. According to U.S. law, when the chair position is vacant, the incumbent continues serving as acting chair until a new appointee is confirmed. Senior White House officials have publicly acknowledged that this 'temporary continuation' legal interpretation is feasible. By then, Powell would remain in a 'lame duck' status, and the Fed would avoid cutting rates in the short term, continuing its data-dependent strategy. Market expectations regarding policy shifts would face comprehensive corrections. A variable to watch is that Trump has repeatedly threatened to fire Powell directly, adding extreme tail-risk disturbances to this baseline scenario.

Scenario Two: Trump Compromises, Wash Passes Through Political Deal-Making

Achieving this scenario hinges on a major political concession from Trump — ordering the Department of Justice to drop the investigation into Powell in exchange for Tillis’s support. Even if Tillis changes his stance, Wash must ensure there are no dissenting votes within the party to narrowly pass through the Banking Committee and ultimately secure confirmation by the full Senate. If Wash assumes office, he will likely adopt a 'watch first, act later' gradual approach, deciding on rate cuts after inflation trends become clearer in the third quarter, finalizing the top-level design for balance sheet reduction within the year, and potentially initiating the reduction as early as the beginning of 2027. A more probable interim solution is that Wash first takes over Milan’s seat on the Federal Reserve Board, participating in decision-making as a 'shadow chair,' and officially succeeds Powell upon the expiration of his term, thereby shortening the policy vacuum. Given Trump’s recent public insistence that the investigation should continue, reaching this compromise path will be extremely challenging and should not be prematurely priced in.

Scenario Three: Trump Invokes Recess Appointment Authority, Forcing Wash as Acting Chair

This is the black swan scenario for the markets, but the urgency has decreased compared to before. If the nomination stalls in the Senate for too long, Trump has the authority to directly appoint Warsh as acting chair during a congressional recess. Once this precedent is set, it will completely undermine the long-standing narrative of Federal Reserve independence. The market will view Warsh entirely as Trump's man, leading to a sharp, temporary crash in the dollar, with gold and safe-haven assets experiencing a surge, plunging global financial markets into severe volatility. For now, recent statements from the White House have softened, making this option more of an extreme political bargaining chip rather than an immediate contingency plan, though it still needs to be monitored as a non-negligible tail risk.

We believe that regardless of which scenario ultimately unfolds, the policy uncertainty brought about by Warsh's nomination will remain a core pricing theme for global markets over the next 1-2 months, aside from geopolitical factors. History has repeatedly shown that there is a significant deviation between the stance taken by Fed chair candidates during confirmation hearings and their actual decision-making once in office. Greenspan was once a vocal opponent of interventionism but ended up being the most interventionist chairman in history. Bernanke didn’t mention quantitative easing at all during his hearing, yet QE came to define his entire tenure. For the market, placing excessive bets on Warsh’s policy path is essentially like grasping at straws; the real answers will only emerge through a series of decisions once he truly takes the helm.

Warsh's Policy Framework: Choices on Three Core Issues

Warsh's policy framework will ultimately boil down to choices on three core issues: the dynamic balance of Federal Reserve independence, strategic trade-offs in inflation control, and the fundamental reshaping of the dollar's global standing. These three issues will not only determine the future direction of Fed policy but will also profoundly influence the long-term evolution of the global monetary system and financial markets.

(1) Federal Reserve Independence: Functional contraction in exchange for political space, balancing dual pressures with an initial hawkish approach followed by dovish adjustments

Regarding the policy divergence between the White House and the Federal Reserve, Warsh’s balancing strategy was already evident during his hearing. The essence of his approach is neither outright defiance against political pressure from the White House nor complete capitulation as its “puppet,” but rather a strategy of functional contraction to secure political independence—maintaining independence on core monetary policy while showing goodwill in non-core areas towards Congress and the White House.

Warsh’s redefinition of Federal Reserve independence reveals the underlying logic of this strategy. He proposed that 'the Fed's independence depends on itself,' meaning that as long as the Fed stays within its core monetary policy boundaries and does not overstep into fiscal or social policy, it won’t give the executive branch justification to intervene in monetary policy, thereby safeguarding the foundation of its independence. In other words, he is willing to relinquish the Fed’s autonomy in non-monetary policy areas such as bank regulation, social policy, and international finance in exchange for respect from the White House and Congress regarding its monetary policy decision-making authority. This strategy addresses the Trump administration’s long-standing criticism of the Fed overstepping its bounds while leaving him room for independent monetary policy decisions, forming a delicate political balancing act.

In terms of specific policy implementation, Warsh’s optimal strategy is highly likely to follow a 'hawkish-first, dovish-later' approach. A Fed Chair’s policy legitimacy fundamentally stems from market trust in the institution's independence. If, upon taking office, he immediately cuts rates rapidly to meet Trump's demands, he would lose all market credibility and eliminate his main leverage in negotiations with the White House. Therefore, early in his term, Warsh will inevitably adopt a tough stance on inflation, using hawkish rhetoric to establish market credibility and demonstrate that his decisions are independent of White House political pressure. After substantial inflationary pressures ease and sufficient market credibility is built, he can then comfortably initiate rate cuts—delivering on policy responses expected by the White House while maintaining the narrative of 'data-driven decision-making' independence.

Notably, Warsh will not completely capitulate to White House political pressure. The precedent set by Powell in 2017 has already proven that a Fed Chair’s professional integrity and institutional pride will lead them to prioritize safeguarding the Fed’s institutional reputation and historical positioning rather than fully accommodating the president’s short-term demands. Trump himself once admitted, 'Once people become leaders, the change is unbelievably drastic.' For Warsh, whose career spans politics, business, and academia, the historical positioning of being a Fed Chair is far more important than catering to the president’s short-term interests, ensuring that he will not become a 'puppet' of the White House but instead seek the greatest common ground between political pressures and central bank independence within the policy framework.

(2) Inflation Control Strategy: Prioritizing price stability, a new framework creates policy flexibility

As a traditional inflation hawk, Warsh has never changed his core stance on inflation control, but his strategic choices exhibit remarkable flexibility. In terms of specific policy implementation, he would not choose aggressive interest rate hikes to completely stamp out inflation and trigger a hard economic landing. Instead, he seeks a dynamic balance between 'controlling inflation' and 'stabilizing growth' by reconstructing the inflation framework.

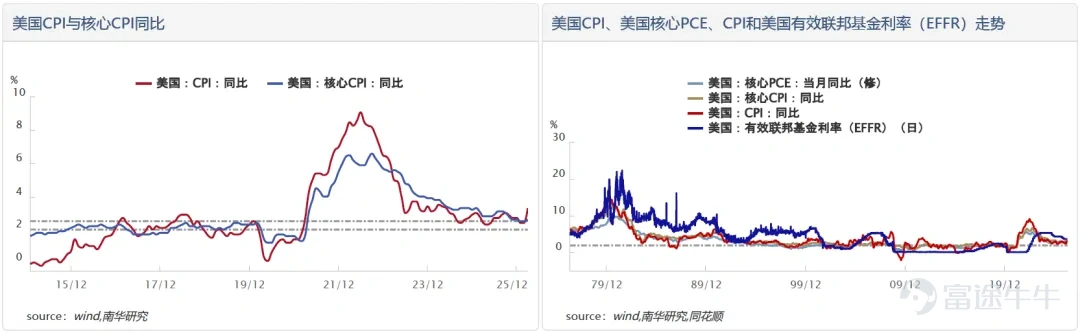

Looking at the current inflation environment, the US March CPI year-on-year has risen to 3.3%, the highest level in nearly two years, while core PCE excluding energy and food remains around 2.8%, with strong stickiness in service sector inflation; tensions in the Strait of Hormuz have driven oil prices from $70 at the beginning of the year to over $90, and the lag in the transmission of energy prices to CPI is still 2-3 months. The path for inflation to fall back remains uncertain. Against this backdrop, Warsh repeatedly emphasized at the hearing that 'once inflation takes root in the economy, the cost of bringing it down will be higher and more difficult.' This statement is not only a critique of previous policies, but also forms the core bottom line of his future inflation management - he will absolutely not tolerate runaway inflation expectations or repeat the policy missteps of the transitory inflation theory of 2021.

However, unlike traditional hawks, Warsh does not rely solely on interest rate hikes to manage inflation, but instead adopts an inflation governance strategy based on a combination of tools and a framework-first approach. First, by using new inflation indicators to distinguish between 'one-off shocks' and 'trend inflation,' creating space for policy decision-making. His preferred trimmed mean inflation and median inflation can exclude one-time price shocks such as energy and geopolitical conflicts. The current downward trend of these indicators has theoretically left room for subsequent rate cuts. In his view, as long as the underlying inflation trend continues to fall, even if core inflation remains high due to energy shocks, there is no need to respond with interest rate hikes, avoiding the cost of a hard economic landing caused by one-off shocks.

Second, using quantitative tightening rather than interest rate hikes as an auxiliary tool for inflation control. Warsh believes that excessive expansion of the balance sheet is a key source of inflation, so shrinking the balance sheet to contract base money can suppress inflation at its root while avoiding the excessive impact of interest rate hikes on the real economy. This strategy allows him to maintain a hawkish stance through quantitative tightening when inflation proves stickier than expected, without initiating a new round of interest rate hikes, minimizing the risk of the economy sliding into a hard landing.

Third, betting on AI’s disinflationary effects to address inflation issues from the supply side. Warsh believes that productivity gains brought by AI will systematically lower the inflation center from the supply side, which is a more sustainable way of controlling inflation compared to demand-side contraction. This judgment means that he will not pursue aggressive tightening policies to quickly bring inflation back to 2% at the expense of stifling economic growth potential. Instead, he will tolerate inflation running slightly above 2% for some time, waiting for AI's disinflationary effects to gradually materialize, achieving a soft landing for inflation.

Overall, Warsh's inflation governance strategy centers on 'holding the line and flexible policymaking' – he will absolutely not tolerate inflation deviating from the 2% target in the long term or allow inflation expectations to spiral out of control, but he will avoid a hard economic landing as much as possible through indicator reconstruction, tool innovation, and efforts on the supply side, rather than pursuing radical policies aimed solely at completely extinguishing inflation.

(III) The Global Status of the Dollar and De-dollarization: From 'Global Central Bank' to 'US Central Bank,' a de-dollarization process that slows in the short term but accelerates in the long run.

We believe that Warsh’s actions on quantitative tightening and international coordination after taking office will fundamentally differ from the Powell era, and these differences will profoundly affect the evolution of global de-dollarization.

The Federal Reserve under Powell, despite undergoing cycles of interest rate hikes and quantitative tightening, essentially maintained its role as the 'global central bank' – providing liquidity globally through dollar swap mechanisms during crises and continuously exporting dollars under常态化QE (normalization of QE), strengthening the dollar's role as a global public good. Warsh's policy core differs fundamentally from Powell's in three main aspects:

First, the essential difference in the path of quantitative tightening. Quantitative tightening under Powell was a technical adjustment for monetary policy normalization and did not change the long-term expansionary trend of the Federal Reserve's balance sheet. Warsh's quantitative tightening represents a systematic contraction of the Federal Reserve's balance sheet, with the core aim of withdrawing quasi-fiscal functions, tightening the dollar's monetary spigot, and reducing global dollar supply. At the same time, Warsh advocates that the Federal Reserve should reduce holdings of long-term Treasuries and hold more short-term bonds, returning the pricing power of long-end rates to the market through 'buying short and selling long.' This will fundamentally alter the supply-demand structure of the Treasury bond market, contrasting sharply with the long-standing distortion of the Treasury yield curve under Powell.

Second, a fundamental shift in the stance of international coordination. During Powell's era, the Federal Reserve would still use tools such as dollar swaps to maintain stability in the global dollar liquidity system during periods of turbulence in global financial markets. In contrast, Kevin Warsh explicitly stated that the Fed should focus on its domestic mission and avoid overstepping into non-statutory responsibilities in the international financial sphere. Its policy formulation will be entirely centered on domestic economic and inflation targets in the United States, reducing the responsibility for providing global dollar liquidity. This implies that in future global dollar liquidity crises, the Fed’s rescue efforts will become more restrained, significantly diminishing the reliability of the dollar as a global safe-haven asset.

Third, a divergence in the underlying logic of dollar policy. The dollar policy under Powell's era still maintained the traditional tone of a 'strong dollar, stable currency value,' with maintaining the dollar's status as a global reserve currency being one of the core objectives. However, Kevin Warsh’s dollar policy is fully aligned with the 'America First' domestic strategy. His combination of 'balance sheet reduction + interest rate cuts' essentially aims to lower domestic financing costs through rate cuts and boost the domestic economy, while maintaining the credibility of the dollar’s value through balance sheet reduction, rather than preserving the dollar’s role as a global public good.

These actions will have a dual impact on the global process of de-dollarization: 'short-term delay, long-term acceleration.' In the short term, the tightening of dollar liquidity caused by balance sheet reduction will support a strong dollar index, while the improvement in U.S. economic fundamentals brought about by interest rate cuts will also enhance the attractiveness of dollar assets, temporarily slowing down the pace of global de-dollarization. However, in the long term, Kevin Warsh's policies will fundamentally undermine the foundation of the dollar as a global reserve currency. When the Fed abandons its role as the 'global central bank' and the dollar shifts from being a global public good to a sovereign credit currency of the United States, the underlying logic of its position as a global reserve and settlement currency will have changed.

Especially in the field of energy trade, the use of the dollar by the United States as a geopolitical sanction tool has already caused Middle Eastern energy exporters to strongly distrust the dollar settlement system. Kevin Warsh’s weakening of the responsibility for global dollar liquidity will further push Middle Eastern countries to accelerate the diversification of energy settlements, significantly speeding up the process of Petro-Yuan. At the same time, the trend of global central banks toward reserve diversification will further strengthen, with gold’s share in global official reserves continuing to rise, and the reserve shares of non-dollar currencies such as the euro and the yuan steadily increasing. The process of the global monetary system evolving from dollar unipolarity to multipolarity will see substantial acceleration during Kevin Warsh’s era.

Commodities and Financial Markets: A Period of Repricing Turmoil

1. Core Logic of Asset Differentiation

The fundamental reconstruction of the Fed’s underlying logic brought about by Kevin Warsh’s policy framework will inevitably trigger systemic repricing in global financial markets and commodities. During the phase where the policy path is not yet entirely clear, the market will enter a high-volatility period of pricing reconstruction, with the differentiation of asset performance and periodic turmoil becoming the central theme.

1) Beneficiaries: Value stocks with solid fundamentals and short-duration U.S. Treasuries

Among beneficiaries, value stocks with solid fundamentals and short-duration U.S. Treasuries will emerge as relative winners during the policy reconstruction phase. Value stocks benefit from rising real yields and improved economic growth expectations. Their stable cash flows and predictable earnings make them more attractive in an environment of heightened market volatility. Short-duration U.S. Treasuries, due to their lower exposure to interest rate hike risks and ability to gain price support from rate cut expectations, become a 'core allocation choice that can advance or retreat as needed.'

A more specific rationale for these beneficiaries lies in Kevin Warsh’s 'term premium release' strategy: through asset structure adjustments of 'buying short-term bonds and selling long-term bonds,' short-term rates may decline or remain stable, while long-term rates will gradually increase. The steepening of the yield curve will directly improve the net interest margin of the banking system, benefiting the financial sector. Additionally, Kevin Warsh’s optimistic outlook on AI-driven productivity gains will also favor infrastructure providers in the tech sector (chips, data centers, cloud computing), rather than purely speculative concept-based stocks.

2) Under pressure: High-valuation technology growth stocks, crypto assets, and long-duration bonds

On the pressured side, high-valuation growth stocks, crypto assets, and long-duration bonds will face continuous repricing pressure. High-valuation growth stocks are the most sensitive to rising real yields, as the discounting factor for forward cash flows in their valuation models will be continuously compressed due to an upward shift in the interest rate center. Crypto assets, acting as 'zero-coupon' risk assets, may remain under sustained pressure amid tightening liquidity and increasing regulatory scrutiny. Long-duration bonds are directly exposed to the dual pressures of rising term premiums and potential sell-offs by the Federal Reserve, posing significant downside risks to prices.

Wash's explicit stance on 'tolerance for market volatility' further amplifies downward pressure on risk assets. The position that 'the Fed will not intervene unless it threatens the core solvency of the financial system' contrasts sharply with the 'Fed Put' approach during Powell's era, implying that market participants need to completely restructure their risk management strategies. They must shift from the old assumption of 'central bank backstopping' to a new reality of 'risk自负'.

2. Structural increase in market volatility

In addition to the divergence in asset prices, another key market change brought about by Wash's policy framework is the structural rise in volatility, driven by two fundamental shifts in underlying mechanisms. First, a fundamental transition in liquidity management from 'unlimited supply' to 'precise adjustment.' Second, the weakening of forward guidance.

3. Short-term observation window and allocation strategy

For global investors, the short-term observation window for Wash’s policy framework focuses on June to September 2026. The FOMC meeting on June 16-17 will be Wash’s first policy meeting if he assumes office, and whether the widely anticipated first rate cut materializes and its magnitude will directly validate the true orientation of his policy framework. A more critical verification point lies in the September meeting and subsequent policy communications. If Wash initiates quantitative tightening early in his term, even in a gradual and symbolic manner, the credibility of his 'quantitative tightening + rate cuts' framework will gain initial confirmation, and the market will gradually adapt to and price in this framework. Conversely, if quantitative tightening is continuously delayed or downplayed while rate cuts proceed, the market will reassess the consistency of Wash’s framework, and the pricing logic of 'verbally hawkish, substantively dovish' will fully emerge.

In terms of allocation strategies, the core principle to address market turbulence caused by policy uncertainty is to acknowledge and adapt to 'Wash uncertainty.' Specifically, one can capture structural opportunities through steepening yield curve trades, leveraging 'buy short, sell long' operations and the release of term premiums. Additionally, a balanced allocation portfolio can be constructed by reducing concentrated exposure to high-valuation U.S. stocks, increasing allocations to value stocks and emerging market assets with fundamental support, shortening durations in fixed income, improving credit quality, and maintaining core allocations to safe-haven assets like gold to hedge against policy uncertainty and geopolitical risks.

Author: Assistant Director of Nan Hua Research Institute, Zhou Ji Z0017101

Important Disclaimer: The content and opinions in this article are for learning and reference purposes only and do not constitute any investment advice. The market carries risks, and investments should be made with caution.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment