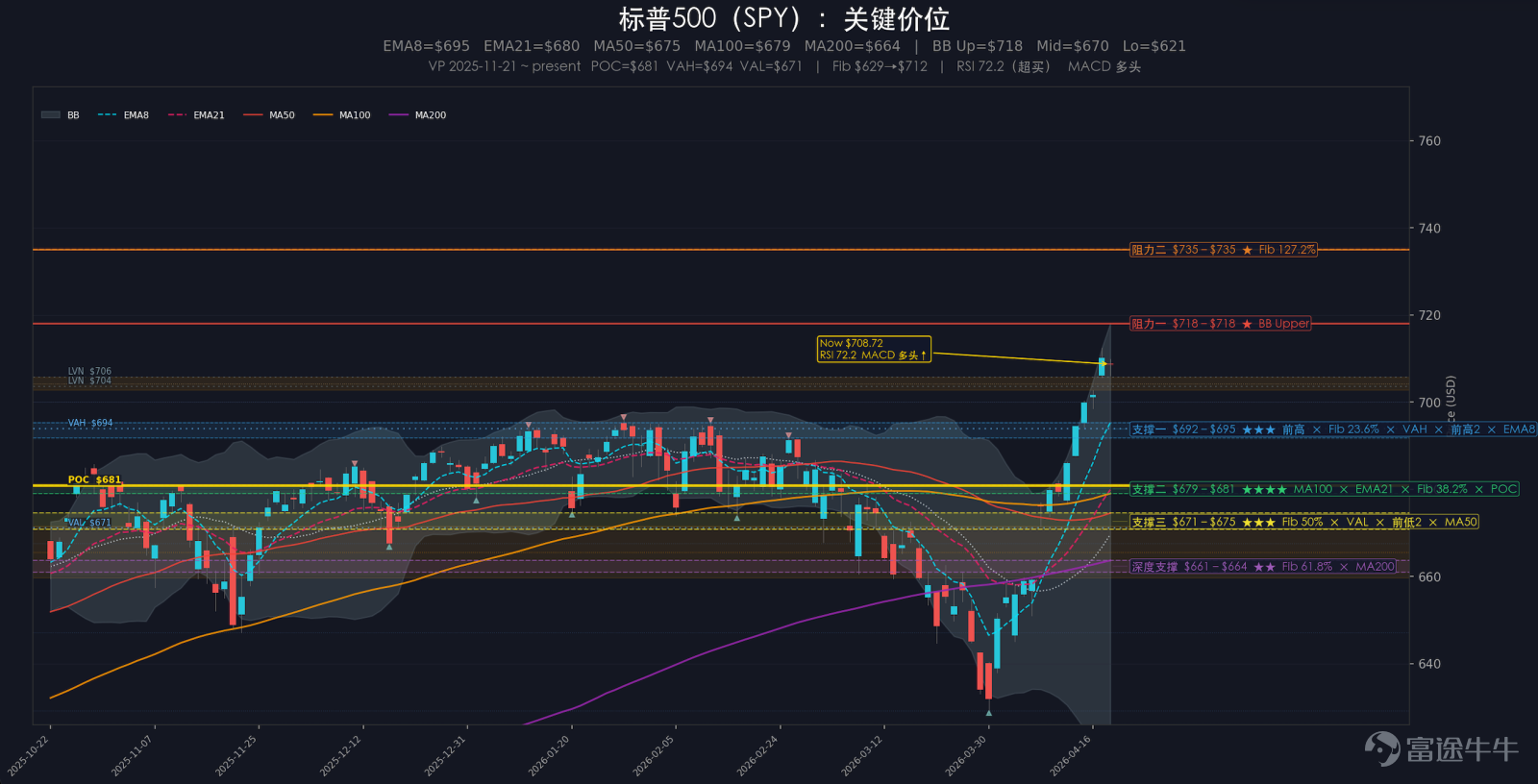

Wall Street Brief (April 21): US stocks consolidated at high levels on Monday, with optimism receding; the first 'repricing' after consecutive sharp gains; the market re-traded geopolitical risks, while earnings season provided important support.

Summary: On Monday, US stocks consolidated at high levels, with the S&P 500 down 0.24%, Nasdaq down 0.26%, Dow Jones slightly lower by 0.01%, and Russell 2000 up 0.58% against the trend. The Nasdaq ended its winning streak, but small-cap stocks still showed relative resilience. From an intraday perspective, Monday's trading was not a trend reversal, but more like the first 'repricing' after consecutive large gains. The VIX rebounded to 18.87, up 7.95% from the previous day, indicating sentiment had clearly retreated from last Friday’s overly optimistic state. That day, the market focus returned to rising risks in the Strait of Hormuz and oil price recovery: risk appetite shifted from 'smooth recovery' back to 'high-level consolidation.' Meanwhile, the overall strength of earnings season also supported the index floor. In terms of sector performance, materials were relatively resilient, tech sectors diverged again; as for major asset classes, the US dollar index fell 0.19%, gold dropped 0.25%, crude oil rose 2.25%, and Bitcoin increased by 2.60%.

I. Major Events

1. Risk in the Strait of Hormuz heats up again

The US military seized an Iranian-flagged cargo ship, and Iran’s stance on the second round of peace talks became shaky. On Monday, the market refocused attention on shipping risks in the Strait of Hormuz and crude oil supply concerns. Unlike last Friday’s 'rapid risk clearance' pricing, this trading day seemed more like reconfirming that although the worst-case scenario did not immediately materialize, geopolitical disruptions are far from over.

2. Resilience during earnings season continues to prop up the lower end of the US stock market

Amid the resurgence of geopolitical risks, US stocks did not experience a uniform sell-off, with the resilience of earnings season providing significant support. In the first-quarter reports disclosed so far, a high proportion of companies have exceeded profit expectations. As a result, even as oil prices rebounded and the VIX rose, the market’s trading logic did not easily revert to 'full risk-off'.

II. Major Trends

From an intraday structural perspective, Monday's session looked more like consolidation at higher levels rather than a trend reversal. The S&P 500 and Nasdaq fell by 0.24% and 0.26%, respectively, while IWM rose by 0.57%. This indicates that the market is not weakening uniformly, with small-cap stocks still absorbing some risk appetite. Rather than viewing it as the starting point for a new round of pullbacks, it's better understood as the first 'repricing' after Friday's sharp rally.

When extending the time horizon, the elasticity of the rebound is still primarily determined by technology and growth stocks. Over a two-week period, QQQ gained 9.90%, significantly higher than DIA's 5.95%; SPY rose by 7.56%, also surpassing RSP's 5.09%. This implies that although the Monday session showed 'small caps relatively outperforming,' in the medium-short term, the dominant forces remain technology and large-cap assets.

The recovery in market breadth has not fully caught up with leading performances. The two-week gain in SPY surpassing RSP shows that this rebound has not yet reached a state of comprehensive and balanced diffusion; however, IWM's ability to close in positive territory on Monday indicates that the market has not retreated to a condition where only a handful of leading stocks are propping things up. A closer description would be: the structure is converging but not collapsing.

III. Market Sentiment

Market sentiment returned to a more cautious position from last Friday's overheated state. The VIX rose to 18.87, increasing by 7.95% compared to the previous day, with protective demand clearly rebounding; the CNN Fear & Greed Index rose to 70, still within an optimistic range, indicating that the underlying sentiment hasn't turned bearish. On the options level, the Cboe total Put/Call ratio increased to 0.84, the index options Put/Call ratio rose to 1.37, and the equity options Put/Call ratio was 0.65, showing a notable increase in institutional-level index hedging. Overall, the market has not fallen back into panic but has added a layer of 'insurance' against possible recurring geopolitical risks amid an optimistic backdrop.

IV. Market Scan

1. Index ETFs

Among major index ETFs, IWM rose by 0.57%, making it the strongest performer of the day; QQQ fell by 0.32%, relatively the weakest. This contrast encapsulates Monday's market behavior: rather than a full retreat, the faster-rising tech sectors took the lead in consolidating, while small caps absorbed part of the rotational capital.

2. Sector Performance

On the sector level, materials gained 0.67%, performing the strongest; healthcare fell by 0.93%, relatively the weakest. Overall, sector fluctuations were limited, indicating that the disturbance brought by rising oil prices mostly stayed at the sentiment and marginal pricing levels, without triggering widespread or clearly directional sector repricing. It seemed more like reordering at higher levels.

3. Seven tech giants

Within the seven major tech stocks, there was renewed divergence. Apple rose by 1.04%, the strongest in the group; Meta fell by 2.56%, Netflix dropped by 2.55%, and Tesla declined by 2.03%, landing on the weaker side. In an environment of elevated indexes and converging sentiment, funds still prefer to stay in the tech main theme, but screening criteria have noticeably tightened, with indiscriminate chasing no longer occurring.

4. Chinese Equities

Chinese concept stocks did not form a unified direction. Baidu rose by 1.28%, relatively strong; Futu fell by 1.29%, performing weakly. Judging from the day's trading, it appeared more like individual stock strength differences rather than sector performance driven by a common policy or industry thread, so it should not be interpreted as a new Chinese concept mainline.

5. Cryptocurrencies

The crypto direction showed overall strength on the day. Bitcoin gained 2.60%, and MSTR rose by 2.58%, both moving higher in sync, indicating that although risk appetite on the US main board has contracted, funds have not significantly withdrawn from high-elasticity crypto exposures. A more appropriate interpretation is that this trend continues to reflect risk appetite, but its intensity mainly concentrates on Bitcoin itself and high-Beta correlated targets, without evenly spreading to all related assets.

$S&P 500 Index (.SPX.US)$ $SPDR S&P 500 ETF (SPY.US)$ $NASDAQ 100 Index (.NDX.US)$ $Invesco QQQ Trust (QQQ.US)$ $Dow Jones Industrial Average (.DJI.US)$ $State Street® SPDR® Dow Jones Industrial Average® ETF Trust (DIA.US)$ $Russell 2000 Index (.RUT.US)$ $iShares Russell 2000 ETF (IWM.US)$ $Roundhill Magnificent Seven ETF (MAGS.US)$ $USD (USDindex.FX)$ $U.S. 10-Year Treasury Notes Yield (US10Y.BD)$ $iShares 20+ Year Treasury Bond ETF (TLT.US)$ $XAU/USD (XAUUSD.CFD)$ $SPDR Gold ETF (GLD.US)$ $CBOE Volatility S&P 500 Index (.VIX.US)$ $Bitcoin (BTC.CC)$ $BTC/USD (BTCUSD.CC)$ $Ethereum (ETH.CC)$ $ETH/USD (ETHUSD.CC)$ $iShares Ethereum Trust ETF (ETHA.US)$ $NVIDIA (NVDA.US)$ $Tesla (TSLA.US)$ $Meta Platforms (META.US)$ $Amazon (AMZN.US)$ $Alphabet-C (GOOG.US)$ $Microsoft (MSFT.US)$ $Apple (AAPL.US)$

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

5