CPU returns to the core of AI! Who are the big winners?

IPO Analysis | Xizhi Technology (01879): Star cornerstone investors lead funding of HKD 1.644 billion, the world's first AI silicon photonics chip stock begins bookbuilding

Pioneer in all-optical AI computing power infrastructure and optoelectronic hybrid computing unicorn Xizhi Technology (1879.HK) $XIZHI TECH-P (01879.HK)$ Begins bookbuilding today, entering the countdown to listing.

Zhitong Finance APP learned that Xizhi Technology's bookbuilding period is from April 20 to 23, with an offering price ranging from HKD 166.6 to HKD 183.2, planning to globally offer 13,795,200 H shares. At the midpoint offering price of HKD 174.9 per share, the global offering will raise approximately HKD 2.2669 billion net proceeds. At the lower limit of the offering price of HKD 166.6, the valuation at listing will be HKD 15.322 billion. It plans to list on the main board of the Hong Kong Stock Exchange on April 28.

This IPO has attracted multiple institutional cornerstone investors for Xizhi Technology, including industry giants such as Alibaba, CMCC Capital, Lenovo, ZTE, GIC, Blackrock, Fidelity International, Baillie Gifford, Schroders, Temasek, UBS, and other international sovereign funds and leading long-term funds from the US and Europe. It also includes top domestic private equity firms like Hillhouse, Greenwoods, CPE, multi-strategy tech funds such as 3W and Aspex, as well as mainstream investment forces like Ping An Asset Management, GF Fund Management, and ICBC Wealth Management. Numerous industry investors and global leading institutions have placed their bets on this cornerstone investment in Xizhi Technology's IPO, fully demonstrating their recognition of the company’s long-term value. Cornerstone investors will subscribe for USD 200.9 million (HKD 1.644 billion) worth of shares, accounting for 71.54% of the total offering. The high proportion of cornerstone subscriptions further highlights widespread market recognition. The company has garnered recognition from multiple star institutions prior to its IPO, completing rounds of financing from A-C4, bringing in well-known industry players and strategic capital such as Tencent, Baidu, China Mobile, and Shanghai Investment Corporation.

According to Frost & Sullivan, Xizhi Technology is the world's first company to achieve large-scale deployment of optoelectronic hybrid computing power. By revenue in 2025, the company ranks first among independent Scale-up optical interconnect solution providers with an 88.3% market share. The cumulative shipments of the company's optical computing chips in 2024 and 2025 rank first globally. From this IPO, the company plans to use approximately 70% of the net proceeds for R&D over the next five years, including continued development of optical interconnect and optical computing businesses, and about 20% will be used for commercialization efforts.

High industry growth, scarce supply in the track

Artificial intelligence is developing at an unprecedented speed, but constrained by Moore's Law and other physical limits, the shortage of computing power remains evident. Xizhi Technology’s optoelectronic hybrid computing power technology directly addresses the issue of insufficient computing power through 'enhanced single-card computing power' via optical computing and 'improved multi-card collaboration efficiency' via optical interconnects.

According to the prospectus, in the field of optical interconnects, Xizhi Technology focuses on the Scale-up optical interconnect market. Notably, optical interconnects were previously mostly applied to Scale-out networks (connections between computing nodes), but in recent years, Scale-up (high-speed interconnection between chips within computing nodes) has been receiving increasing attention. A landmark event was NVIDIA's introduction of a dual-track technical path of 'copper cable Scale-up' and 'optical Scale-up' at the 2026 GTC conference, aiming to break through bottlenecks in bandwidth, latency, and power consumption of traditional electrical interconnects. This sends a clear industrial signal: optical interconnects are moving from the periphery of data centers to the core computing clusters.

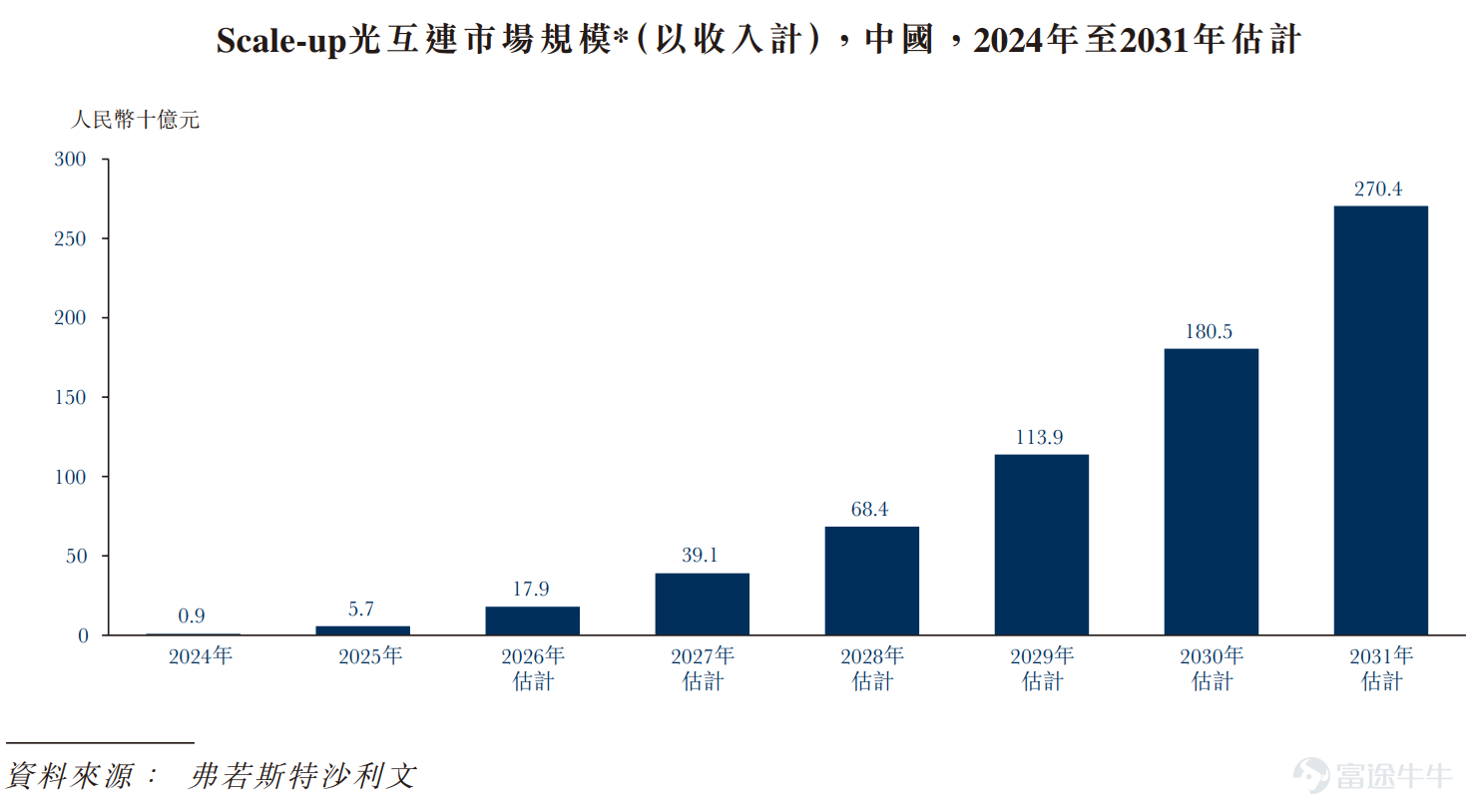

According to Frost & Sullivan, China’s Scale-up optical interconnect market is on the verge of an explosion. In 2025, the size of China’s Scale-up optical interconnect market will be 5.7 billion yuan, expected to reach 180.5 billion yuan by 2030, with a compound annual growth rate of 99.6%. However, there are few early participants in the industry, with extremely scarce supply. In 2025, only two companies achieved large-scale commercialization in China’s Scale-up optical interconnect market, with Xizhi Technology being the only independent Scale-up optical interconnect solution provider to achieve large-scale commercialization in mainland China, holding approximately 88.3% market share. In 2025, the company launched LightSphere X, the world's first distributed optical circuit switching solution for GPU super-node interconnection, which can increase model floating-point operation utilization by over 50%.

Image source: Company's hearing materials

Compared with optical interconnects, optical computing, although still in the early stages of commercialization, holds more disruptive potential — it could completely change the current computing paradigm. The core advantage of optical computing lies in its ability to perform high-speed matrix multiplication and other linear algebra operations in the optical domain, which are key workloads in large language models, neural networks, and scientific computing.

Currently, only two companies globally have achieved commercialization of optical computing, one of which is Xizhi Technology. Its cumulative shipments of optical computing chips in 2024 and 2025 ranked first globally.

The company has released the PACE series of optoelectronic hybrid computing accelerator cards, demonstrating significant performance advantages in target tasks under testing environments. In specific combinatorial optimization problems (e.g., maximum cut problems), the total solution time for core tasks executed by the PACE prototype is over 100 times faster than similar GPUs. This speed improvement is mainly due to PACE’s ultra-low iteration latency of approximately 5 nanoseconds — a direct result of the optical computing architecture. Meanwhile, as matrix multiplication is a passive process, energy consumption is significantly reduced. According to a research report published by Xizhi Technology in Nature, PACE's energy efficiency (including external laser power consumption) is approximately 2.38 TOPS/W (trillion operations per second per watt).

Currently, the company is developing PACE 3, which aims to support larger-scale commercial deployments and is expected to expand optical computing products into more promising business scenarios, including large language model inference, while also broadening the customer base beyond early adopters.

Image source: Company's hearing materials

The scarcity of its products and leading position in product technology provide Xizhi Technology with strong competitive advantages. These achievements are inseparable from the company's talent pool and intensive R&D investment: led by two founders with formal training, from the initial startup phase to rapid development, from R&D investment to commercial implementation, they have continuously pushed for the application of R&D results and efficient operations, consistently delivering strong performance.

High-intensity R&D investment, commercialization unleashes high growth performance

曦智科技 was founded in 2017. Its founder, Dr. Yichen Shen, published a cover article in Nature Photonics, which for the first time validated the feasibility of using light for computation, laying the foundation for the development of optical computing. Co-founder Dr. Huaiyu Meng has focused on optical interconnection technology and, as a core member, participated in the research and development of multiple key components for the world's first on-chip optical network project.

Under the leadership of these two technical experts, the company has formed a large technical team. The R&D department currently has 176 employees (including the two mentioned above), of which 117 hold master's degrees, accounting for 67.2% of the total workforce. To date, the company has registered 71 patents with the China National Intellectual Property Administration and 79 patents in other jurisdictions such as the United States, Hong Kong, the European Union, and Taiwan, China. Globally, it has 260 pending patent applications.

From 2023 to 2025, the company's R&D expenditures were 280 million yuan, 352 million yuan, and 479 million yuan, respectively, with a compound annual growth rate of 30.8%. The company has continued to increase its R&D efforts, building a comprehensive R&D platform covering all key aspects of optoelectronic hybrid computing power and three core technologies: inter-chip optical networks (oNET), on-chip optical networks (oNOC), and photonic matrix computing (oMAC), providing momentum for its two product lines of optical interconnection and optical computing.

In terms of commercialization timelines, the two core product series of optical interconnection, Scale-up and Scale-out, achieved commercialization in 2024, while the optical computing product PACE1, an optoelectronic hybrid computing accelerator card, began commercialization in 2022. In terms of revenue contribution, optical interconnection products have become the main source of the company’s revenue. By 2025, the revenue shares from the Scale-up product, Scale-out product, and optical computing product are expected to be 71%, 4.8%, and 19%, respectively.

Image source: Company's hearing materials

Driven by these two product lines, the company's revenue increased from 38 million yuan in 2023 to 106 million yuan in 2025, with a compound annual growth rate of 67%. Economies of scale have optimized the R&D expense ratio by 281.4%, administrative expense ratio by 124%, and operating expense ratio (sales, administration, and R&D) by 396.8% during this period.

As revenue scales up, the company’s expense ratios are further optimized, driving continuous improvement in profitability. Over the past two years, the commercialization of the company’s two business line products has been in a rapid growth phase. By 2026, the AI+ sector is expected to drive explosive growth in computing power demand, compounded by market scarcity and strong product capabilities, which will propel the company's performance into a scaled explosion.

Large valuation re-rating space; institutions optimistic about future prospects

So, how should 曦智科技 be valued?

Looking at the performance of secondary market peers, domestic AI chip companies received full value re-ratings from the capital market upon listing – Wall Street’s 壁仞 saw its market cap briefly break through 100 billion Hong Kong dollars on its first day of trading in Hong Kong, while 摩尔线程 and 沐曦股份 broke through 280 billion yuan and 330 billion yuan, respectively, on their first day of trading in mainland China, representing multi-fold increases over pre-IPO valuations. Post-listing, as of April 20, the market caps of 壁仞, 摩尔线程, and 沐曦股份 have grown by more than 1.5x, 4.7x, and 5.7x, respectively, compared to their IPO prices. Considering the current stage of development of 曦智科技, as the company accelerates its scaled commercialization, the Hong Kong stock market is expected to offer similar valuation re-rating potential.

In addition to the scarcity of the track that XtalPi Tech is in, as previously mentioned, there are no comparable companies in the Hong Kong stock market that integrate optical and electronic solutions. The company's upcoming listing in Hong Kong will become the sole avenue for Hong Kong investors to invest in optical-electronic hybrid solutions, making its investment scarcity highly prominent.

Looking globally, players in the same track have already gained significant recognition from the capital markets: Lightmatter is valued at $4.4 billion, Ayar Labs at nearly $4 billion, Celestial AI was acquired by Marvell for $5.5 billion (including contingent consideration) by the end of 2024, and DustPhotonics was acquired by Credo for over $1 billion (including contingent consideration) in April 2026. The three comparable U.S. companies have each raised more than $500 million, yet their commercial progress remains in the early stages; in contrast, XtalPi Tech has only raised $330 million historically but has already achieved scaled revenue. Compared to similar overseas companies, XtalPi Tech demonstrates significant discount potential, and its premium upon listing is well justified.

Overall, XtalPi Tech is positioned at the forefront of two major tracks: optical interconnects and optical computing. Backed by a strong talent pool and intensive R&D investment, the company is progressively achieving scaled commercialization of products in both tracks, driving continuous high growth in performance. Ongoing heavy R&D investment enables the company to maintain technological leadership and scarcity in its offerings, further solidifying its leading position in the industry and fully capitalizing on policy and market development dividends over the next decade.

As the only listed entity in the Hong Kong stock market offering optical-electronic hybrid computing power, XtalPi Tech’s current IPO valuation is relatively low. Moreover, compared to other track-focused companies, the strength of its talent team adds value to its valuation. Investing in people is key, and the two academically grounded founders may attract long-term institutional investors to assign a higher valuation.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

1

7