The S&P 500 has risen for seven consecutive weeks—should you chase the rally or take profits?

Global Weekly Insights | US mid-term upstream price pressures persist, China's Q1 economy off to a strong start

On the macroeconomic front

United States: The lower-than-expected rise in PPI in March eased short-term inflation concerns, but medium-term upstream price pressures remain.

Last week, core macroeconomic data in the United States showed characteristics of 'short-term inflation easing while medium-term risks persist.' PPI in March rose by 4% year-on-year and 0.5% month-on-month, while core PPI increased by 0.1% month-on-month and 3.8% year-on-year.All indicators were significantly below market expectations. Although the energy component was the main driver of the increase, the actual increase was weaker than the movement of oil prices during the same period.Market expectations that 'Iran tensions would impact inflation' were proven wrong, and short-term inflation panic has somewhat subsided.However, it should be noted that indicators measuring upstream inflation 'pipeline pressures' continue to rise, indicating that the potential risk of price pressures being transmitted downstream is still accumulating.This does not signify a substantial retreat of inflationary pressure; there is still a possibility for inflation to rise again in the future. Additionally, the previously released CPI for March, driven by energy prices, rose to 3.3% year-on-year, with core CPI rising moderately. High oil prices will continue to push up nominal inflation.

China: The economy started well in the first quarter, with import-export and industrial production maintaining robust resilience.

China's core macroeconomic data for the first quarter showed impressive performance,marking a strong start to the national economy.The GDP in the first quarter grew by 5.0% year-on-year, accelerating by 0.5 percentage points compared to the fourth quarter of last year, with consumption and industrial production improving in tandem. In terms of imports and exports, exports in March increased by 2.5% year-on-year and imports surged by 27.8%, resulting in a trade surplus of $51.13 billion.Both import and export cumulative growth rates maintained double-digit increases in the first quarter. Hong Kong and ASEAN were the main pillars of export support, while high-tech and high value-added products such as integrated circuits and new energy vehicles performed particularly well in exports,and the structural benefits from order transfers due to the Middle East conflict began to show. On the industrial production front, the added value of industrial enterprises above designated size increased by 5.7% year-on-year in March. Growth in manufacturing and mining remained robust, with notable expansion in sectors like railway, shipbuilding, aerospace equipment, and electronic devices. Export delivery values grew by 8.7% year-on-year,highlighting the resilience of industrial production. The consumer side also saw a recovery,with retail sales of consumer goods in the first quarter increasing by 2.4% year-on-year. Catering consumption rebounded strongly, and the potential of service consumption continued to be unleashed.

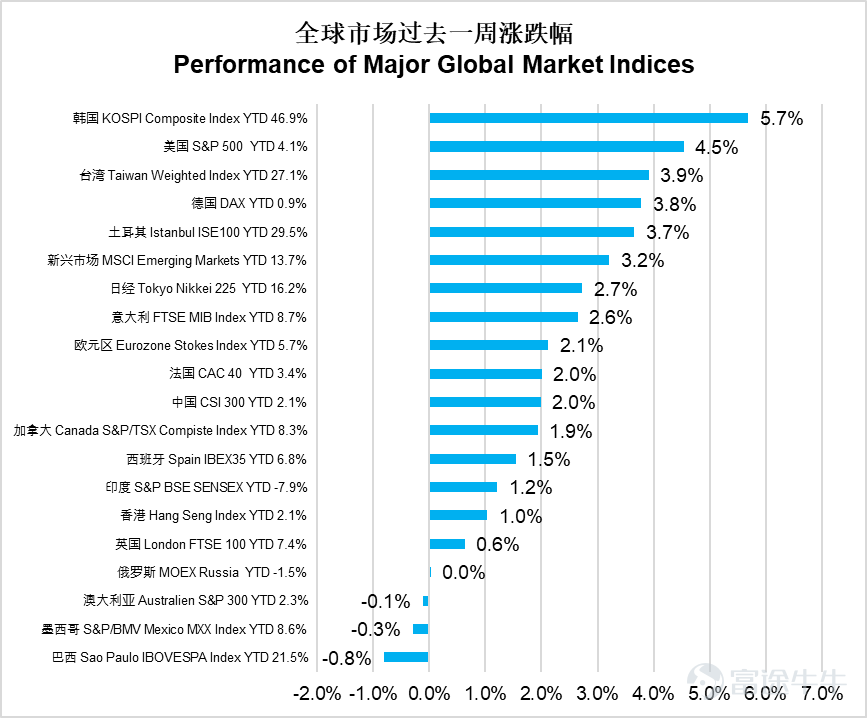

In terms of the equity market

Last week, global markets generally rose, with South Korea’s KOSPI leading the way by surging 5.7% globally,the S&P 500 climbed 4.5%, and Germany’s DAX increased by 3.8%. Emerging markets as a whole gained 3.2%, Taiwan’s weighted index rose 3.9%, and the Hang Seng Index went up by 1.0%. Brazil’s IBOVESPA fell 0.8% and Mexico’s MXX dropped 0.3%, becoming one of the few declining markets.Overall, major markets in Europe, America, and Asia performed strongly, while Latin American markets remained relatively weak.

The US information technology sector surged 8.1%, leading performance, while consumer discretionary rose 6.6% and communication services climbed 6.3%.Real estate increased by 3.8%, financials gained 3.3%, industrials were up 1.2%, and healthcare inched up 0.9%. Consumer staples remained flat. However, the energy sector fell 3.5%, utilities dropped 1.7%, and materials edged down 0.4%.The market exhibited a pattern of tech and consumer sectors leading gains, while energy and utilities lagged.

In Hong Kong stocks, the non-essential consumption sector rose 4.4%, performing the best, the Hang Seng Tech Index climbed 3.8%, and the information technology sector gained 2.1%.Healthcare rose 2.0%. Real estate and construction, as well as telecommunications, increased by 0.5% and 0.6%, respectively, while the energy sector slightly gained 0.4%. However, essential consumption fell 3.1%, utilities declined 1.9%, and industry dipped 0.4%. Finance and conglomerates both slipped 0.2%, while materials edged down 0.1%.The market showed divergent characteristics, with technology and consumer sectors leading gains while defensive sectors came under pressure.

In the bond market,

Global bond markets continued to recover over the past week,The global composite index rose 0.88%, the US composite index climbed 0.55%, US investment-grade corporate bonds increased by 0.67%, and US high-yield corporate bonds gained 0.66%. The emerging markets USD bond composite index rose 0.99%.The Chinese dollar-denominated credit bond index increased by 0.41%.

In terms of interest rates, US Treasury yields have generally declined,The 2-year US Treasury yield fell 9 basis points from last week to 3.71%, while the 10-year US Treasury yield dropped 7 basis points to 4.25%.

Market Outlook

– The S&P 500 surged over 12% in 13 trading days, with the market already fully pricing in a US-Iran ceasefire.

Global markets continued to rebound this week against the backdrop of significantly eased concerns over Middle Eastern conflicts, with the S&P 500 rising more than 12% in 13 trading days after hitting a low on March 30.We have compiled statistics on how long it has historically taken the S&P 500 to break through previous highs after a pullback exceeding 8%. Since 1950, this has occurred 37 times, with an average of 197 days needed to reach new highs.However, this time, the S&P 500 hit a new high in just 11 trading days.This is the fastest in history.The second-fastest was in 1997 when the market pulled back nearly 10% and reached new highs in 16 trading days. Behind this rapid rebound is investor optimism about the U.S. economy and corporate earnings. Before the current conflict, the forward price-to-earnings ratio of the S&P 500 at its January peak was 22x; as of the latest close, the S&P 500 has risen another 2% compared to its January high, but the current forward P/E ratio is only 21x. As we mentioned in our previous weekly commentary,during the conflict in March, the market mainly sharply raised earnings estimates for energy sector companies but did not revise down expectations for non-energy sectors.The final outcome was that the market's earnings forecasts for 2026 and 2027 were revised upward by 4% and 5%, respectively, compared to before the conflict. Current market sentiment has significantly recovered from the panic selling at the end of March.Market expectations suggest a partial agreement could be reached or the temporary ceasefire extended before the expiration of the two-week temporary truce between the U.S. and Iran to facilitate further negotiations.However, since the market has already fully priced in the ceasefire, investors should also be wary of the risk of renewed geopolitical tensions if an agreement is not reached, which could impact the market.

Key economic data and events this week

On Monday, China will announce the April LPR interest rate.

The US will release March retail data on Tuesday, and the Senate will hold a hearing on Wash's nomination for Federal Reserve Chair.

Disclaimer: The issuer of this report is E Fund Asset Management (Hong Kong) Co., Limited. This report does not constitute an invitation or recommendation to invest in fund units. Fund units can only be subscribed using the application form accompanied by the fund prospectus. Investment involves risks; fund prices may rise or fall, and past performance is not indicative of future results. Before investing, investors should carefully read the fund prospectus (including the 'Risk Factors' section) to understand the investment risks associated with the fund. This report may only be distributed within certain jurisdictions. Where distribution of this material or any invitation or solicitation contained herein is restricted in certain jurisdictions, or where it would be unlawful to distribute this report or make any invitation or solicitation to any person, this report shall not constitute such distribution, invitation, or solicitation. This document has been exempted from prior review and approval by the Hong Kong Securities and Futures Commission but has not been reviewed by the SFC. SFC authorization does not imply a recommendation or endorsement of the scheme, nor does it guarantee the commercial merits or performance of the scheme, nor does it represent that the scheme is suitable for all investors, or endorse that the scheme is suitable for any particular investor or any class of investors. All rights reserved ©2026. E Fund Asset Management (Hong Kong) Co., Limited.

Risk Disclaimer: The above content only represents the author's view. It does not represent any position or investment advice of Futu. Futu makes no representation or warranty.Read more

Comments

to post a comment

2

1